In 1980, Congress passed an amendment to the Investment Company Act of 1940, giving way to a new investment vehicle known as Business Development Companies or BDC’s. Although the legal structure of BDC’s came about in 1980, the creation of these entities didn’t take off until the early 2000’s. In 2004, Apollo Investment Corporation raised $930 million, igniting a rush of BDC IPO’s. In this article, we will explore the components of a BDC and why you may or may not consider adding them to your portfolio.

Q3 2019 hedge fund letters, conferences and more

What Are BDCs

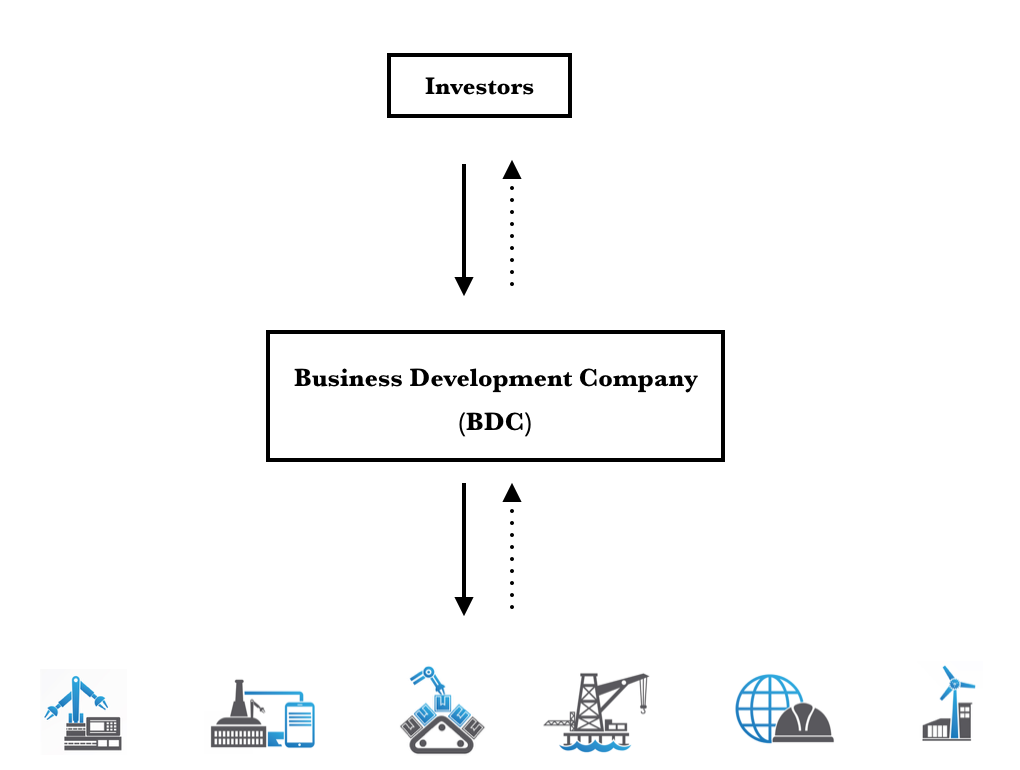

Business Development Companies were set up as a way for smaller and middle market companies to access capital from regular investors. Investors looking for exposure to smaller and middle market US companies can do so by investing in a BDC. Similar to a REIT, a BDC is traditionally structured as a regulated investment company (RIC), and can avoid paying corporate income tax as long as 90% of taxable income is distributed to shareholders in the form of a dividend. Not all but most BDCs are publicly traded. The liquidity and accessibility of publicly traded shares give investors exposure to a private equity-like vehicle without the headaches of a lockup period. BDCs use equity and debt to create a investment portfolio of lower and middle market companies.

BDC Investments

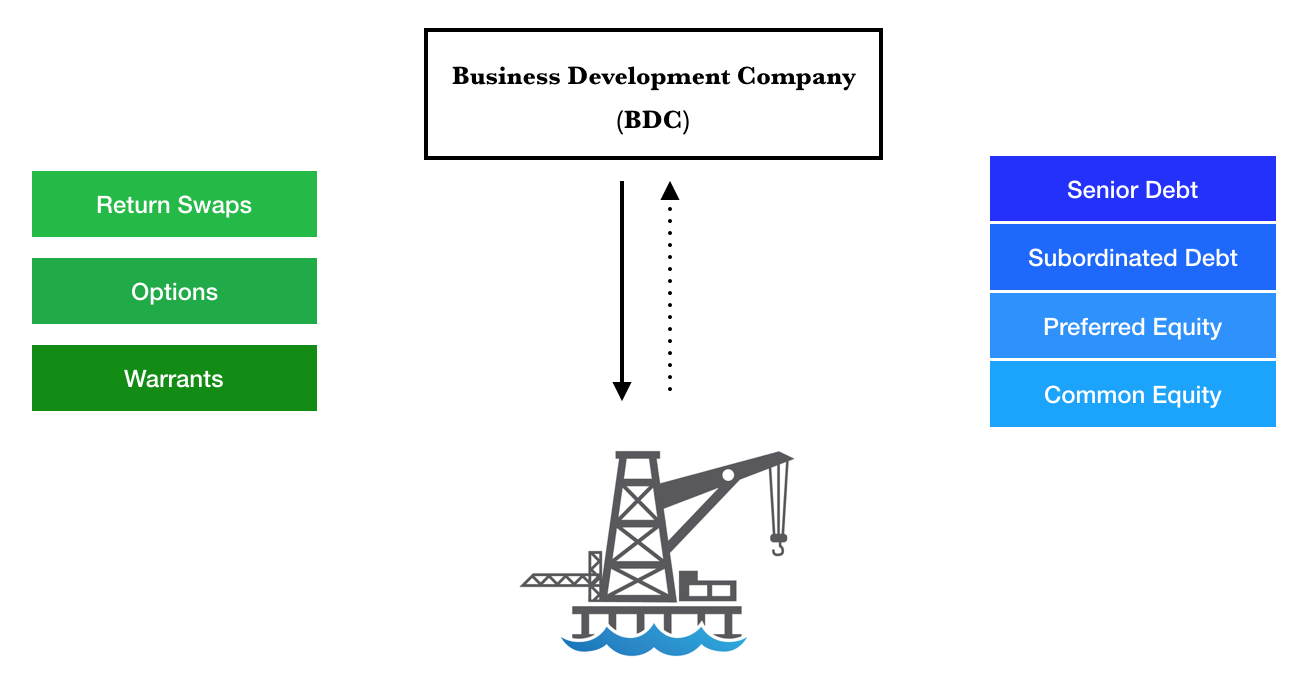

What makes BDC’s unique among many traits, is their ability to invest up and down the capital structure of various companies. As long as the BDC is compliant with the legalities of placing 70% of its investable assets in private businesses, they have the freedom to direct where that investment occurs within the capital structure. This component creates a similarity to private equity. Senior Debt, Subordinated Debt, Preferred Equity, and Common Equity are all positions a BDC can take in an investment. In addition, BDCs can use things like Return Swaps, Options, and Warrants to generate a targeted IRR. The advantage of these type of investments is that it allows the BDC to hit a targeted IRR while providing financing that doesn’t suffocate the capital structure for smaller companies.

Typically a BDC will focus on a defined niche of expertise. Some BDCs focus on specific areas of the capital structure (ex, senior versus subordinated debt), while others choose to direct more of an industry focus (ex. tech versus manufacturing). Having a predefined niche allows BDCs to create an edge on certain deal types, a trait also similar to private equity.

The Inner Workings of a BDC

BDC’s can be categorized into internally managed and externally managed funds. Both have benefits and drawbacks and it’s important to understand the differences.

An internally managed BDC directly employs the individuals managing the BDC. The compensation structure is built around performance similar to a hedge fund. Typically performance is measured against overall improvement in Net Asset Value (NAV). Internally managed BDC’s are the minority in the industry as most have difficulty replicating the structural advantages that traditional externally managed BDCs control.

Externally managed BDC’s are compensated on Assets Under Management. The BDC itself does not directly employ anyone, instead, it pays out a management fee. Typically externally managed BDCs have a larger infrastructure that can be extremely helpful when creating proprietary deal flow.

Speaking with Aaron Peck, CIO / CFO of Monroe Capital (MRCC), it was clear to understand the advantages infrastructure can create for a BDC. For example, Monroe Capital has a team of 17 deal originators who can source over 2,000 deal opportunities in a typical year. This deal flow allows Monroe Capital to look at a lot of opportunities and make investments in what they deem the most appropriate. After placing an investment, Monroe Capital has a team of close to 30 underwriters and portfolio managers who constantly monitor the companies. This infrastructure allows Monroe Capital to be in constant contact with management. Actions like monitoring weekly (and sometimes daily) KPIs, supporting management and keeping an eye on general performance allow Monroe Capital to support its portfolio companies. Not only can Monroe Capital help a business perform well, they can also reinvest in the company as it grows. This allows more access to already proven winners and the potential for improved performance across the portfolio over time. This structural advantage can potentially increase longterm value that is difficult to replicate in other investment vehicles.

New Legislation

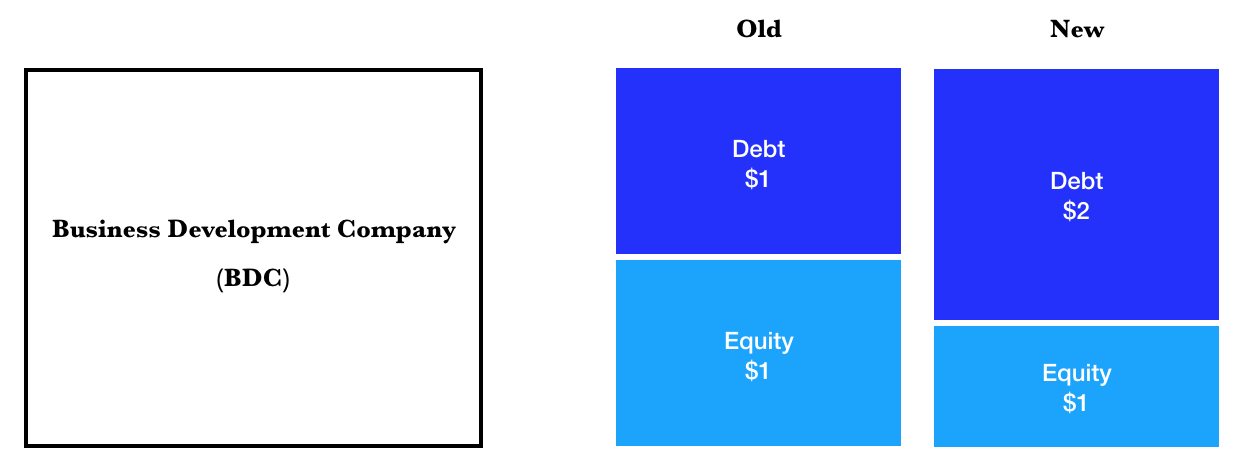

Recently, President Trump signed a bill giving BDCs access to additional capital. Prior to the bill being signed a BDC could only leverage its capital on a 1:1 ratio. Prior to the bill, every dollar of equity, meant one dollar of debt the BDC could take on. Now for every dollar of equity, a BDC can take on two dollars of debt. Having more capital, in theory, should make BDCs more competitive when going up against Private Equity firms and other lenders. Although not everyone is in favor of increased leverage, the legislation was viewed as a bipartisan win, passing 58 to two in the House Finance Services Committee. Advocates of the increased leverage argue that more capital in the hands of BDCs will open up more capital for small private businesses in the US.

Daniel DiMomenico of Murray Devine, a firm that provides valuation and reporting services for BDCs explained how this new legislation might unfold through the industry. As DiMomenico detailed, “BDCs are required to approve their increase in debt capacity. This approval can happen through majority support from the Independent Directors of a BDC, or through traditional Board approval.” DiMomenico estimated it would take six to twelve months for the process to fully ramp up and take shape.

Choosing a BDC

When evaluating a BDC there are a few things you should consider.

NAV/ Share – Much like book value per a share is extremely important when analyzing banks, the Net Asset Value (NAV) per share is extremely important when analyzing BDCs. NAV is calculated by taking the total value of all securities and dividing by the total number of outstanding shares. BDC’s typically trade at a price trend that follows their NAV per share, making this an extremely important metric to monitor.

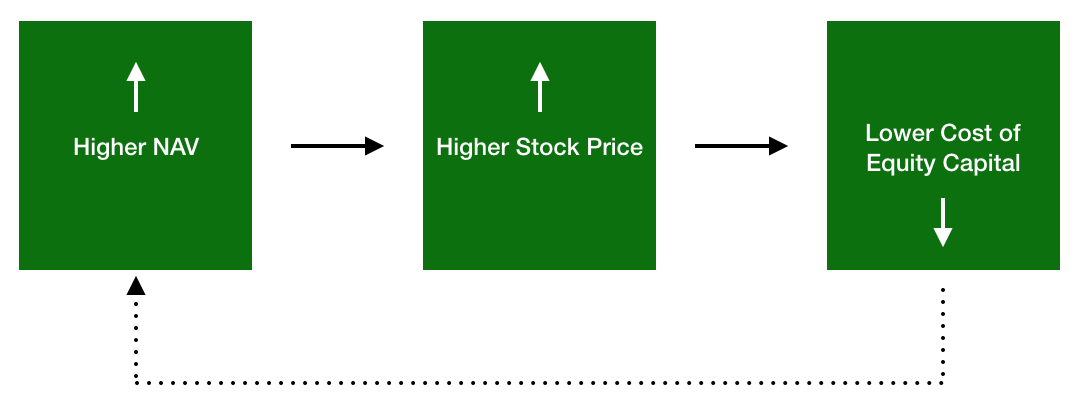

High quality BDCs are typically priced at a premium over their NAV per share. This premium allows the BDC to grow by issuing equity at a less drastic dilution to shareholders over time. Having a high premium to NAV is somewhat of a competitive advantage, because it keeps the overall cost of equity capital lower. This pattern can create a spiral effect for BDCs creating an environment where premium over NAV generates more premium. Conversely BDCs that struggle to maintain a premium over NAV can see a downward spiral of discounts widening to larger discounts.

Weighted Average Portfolio Yield – The weighted average portfolio yield is a metric that can give good insight into the quality of the BDC portfolio companies. Higher yields can indicate riskier investments. Generally, you want to see a weighted average portfolio yield in excess of the promised dividend payout level. If a BDC has to cut dividends (which happens when mass defaults and other circumstances occur), it can severely hurt investor sentiment and send share prices lower. Typically, the excess portfolio yield over the committed dividends is paid out in the form of a special dividend at some point in the year. BDCs must pass through 90% of income to avoid corporate income tax, so eventually that money makes its way to investors. Searching through annual and quarterly reports you’ll be able to find a detailed breakdown of the portfolio yield.

Net Investment Income – Net Investment Income (NII) is another highly important metric to monitor. The NII it is what funds the dividend. Monitoring the ratio of NII to the dividend payment can tip your understanding as to what might be ahead. If a trend emerges of dividend payout consistently exceeding NII, it might signal a cut to future dividends and a resulting lower share price.

BDCs In Summary

BDCs offer a unique opportunity of exposure to smaller private companies. The fact that most of their income is paid to investors via regular dividends serves as another attractive trait for appropriate investors. While some may argue their structure is too complex to adequately analyze, a little digging can produce the necessary insight to judge the specifications of any given BDC. If you would like to learn more about BDC’s or follow the specifics of the industry check out BDC Buzz and BDC Investor. Both offer fantastic insight that can further your understanding of these investment companies.

Sources:

Special Thanks to Aaron Peck of Monroe Capital and Daniel DiDomenico of Murray Devine.

–Bluevaultpartners.com BDCInvestor.com BDC Buzz

Article By Carter Johnson, Finbox