We all make investing mistakes.

Q1 hedge fund letters, conference, scoops etc

I’ve written about some of mine before.

But as I’ll show today, investing in two types of stocks could blow up your portfolio.

Maybe you’ve made the mistake of investing in stocks like this before… and hopefully you won’t again.

Or hopefully, by reading today’s essay, you won’t make the mistake of investing in these companies at all…

Don’t buy the “story stock”

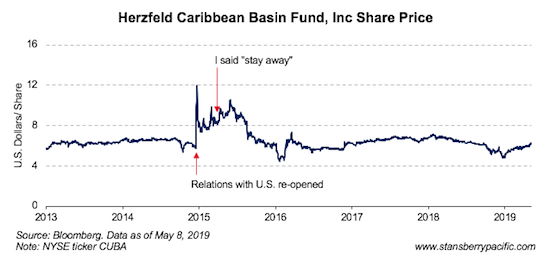

In late 2014, the United States and Cuba – an island 177 kilometres off the coast of Florida that (according to some) posed a grave and existential threat to American sovereignty – re-opened relations after a 54-year freeze.

Eager stock investors raced to invest in Cuba – even though it had (and has) no stock market. But a conveniently named closed-end fund with the ticker symbol CUBA had a ready answer.

CUBA invests in the shares of companies that stand to benefit from the economic opening and growth in Cuba. With Cuba all over the news in 2014, investors piled into the lightly traded CUBA fund, doubling its share price in two weeks. The premium of the shares (relative to the underlying value of the portfolio) peaked at an incredible 71 percent. So investors were paying US$1.71 for every US$1 of assets. (Needless to say, the forecast earnings of the stocks in CUBA did not double during those two weeks.)

I visited Cuba a few months later. It was clear to me that Cuba’s economy faced (and still faces) a very long and difficult road to prosperity. And contrary to what the CUBA share price suggested, the country’s opening wouldn’t help the financial performance of companies in the fund’s portfolio.

At the time, I told readers of my investment newsletter to stay away from CUBA.

Sure enough… after a brief continued surge (expensive shares that are riding a wave of irrational optimism can always get more expensive), CUBA shares fell 32 percent in the next five weeks. And they’re down 48 percent since 2014 highs.

Cuba is a wonderful place, and its re-entry into the global economy was a great story. But CUBA was a terrible stock.

The “it’s so cheap” trap

Russia’s Gazprom is the world’s largest gas company, based on total reserves (of an enormous 36.4 trillion cubic metres). It supplies one-third of the natural gas consumed by Europe. Back in Soviet times, Gazprom was big enough to be an entire government ministry on its own. It has supported remote cities in Siberia and sponsored football teams.

And the stock? It’s impossibly cheap… it trades at a price-to-earnings (P/E) ratio of 2.5. Other gas companies trade at multiples three to 10 times higher. Gazprom shares are also a fraction of the price of global oil producers… ExxonMobil shares, for example, trade at a P/E of 17. Chinese producer China Petroleum & Chemical Corp. trades at a P/E of 10. On an assets basis – that is, market capitalisation compared to total reserves, or total production, Gazprom shares are even cheaper. And even better, the shares offer a dividend yield of 4.8 percent.

But there are a few problems with Gazprom.

First… it’s been that cheap for years. And I don’t mean a few years… I mean decades (except when earnings collapsed, which is the worst reason for a P/E ratio to rise).

Worse… it’s been a terrible stock to own. It’s down 77 percent from its 2008 highs, when its market capitalisation reached a high of US$366 billion (compared to US$59 billion today). The shares have fallen 17 percent over the past five years.

Why the underperformance?

Gazprom – which is controlled by the Russian government – accounts for around 8 percent of Russia’s GDP, and a large chunk of Russian government revenues. When the Russian government needs money to plug a budget deficit, it turns to Gazprom.

Also, the company is as much a geopolitical hammer – used to threaten its customers from Europe to China (twist a few taps, and no more gas for, say, Ukraine) – as it is a gas company. And Gazprom is also a convenient source of cash to top up well-placed government ministers’ retirement plans.

This means that Gazprom isn’t run like a company… it’s managed like a cross between a government piggy bank and a big ATM for the Russian government and friends. Minority investors, like you and me, will never benefit from higher profits.

Gazprom is a classic value trap. It’s a stock that looks cheap on a valuation basis (that is, using the P/E ratio or a similar measure)… but it isn’t that cheap at all (and will likely remain “cheap” indefinitely).

What could change that? A value trap can stop being a value trap – and become an attractive, under-valued investment – if there’s a trigger for change. A change in management, a big change in the industry, higher commodity prices, a regulatory change – all of these things can turn a value trap into a great investment.

That may happen someday for Gazprom. But you could have said the same thing in 1996, when I started looking at Gazprom during my first job with a brokerage house in Moscow. And nothing’s really changed. Holding those perma-cheap stocks is hugely expensive in terms of opportunity cost.

Don‘t do it

Story stocks are everywhere… great concepts that may change the world. But for every great story, there are hundreds of stocks that went nowhere because the path from “story” to “make investors money” proved to be too bumpy. Or maybe (like CUBA) the story’s time just hasn’t come… yet.

And value traps? Also… everywhere. But too often there aren’t enough reasons for it to stop being cheap. Stay away from them, too.

Good investing,

Kim Iskyan

Publisher, Stansberry Pacific Research