Third Point letter to investors for the third quarter ended September 30, 2019.

Q3 2019 hedge fund letters, conferences and more

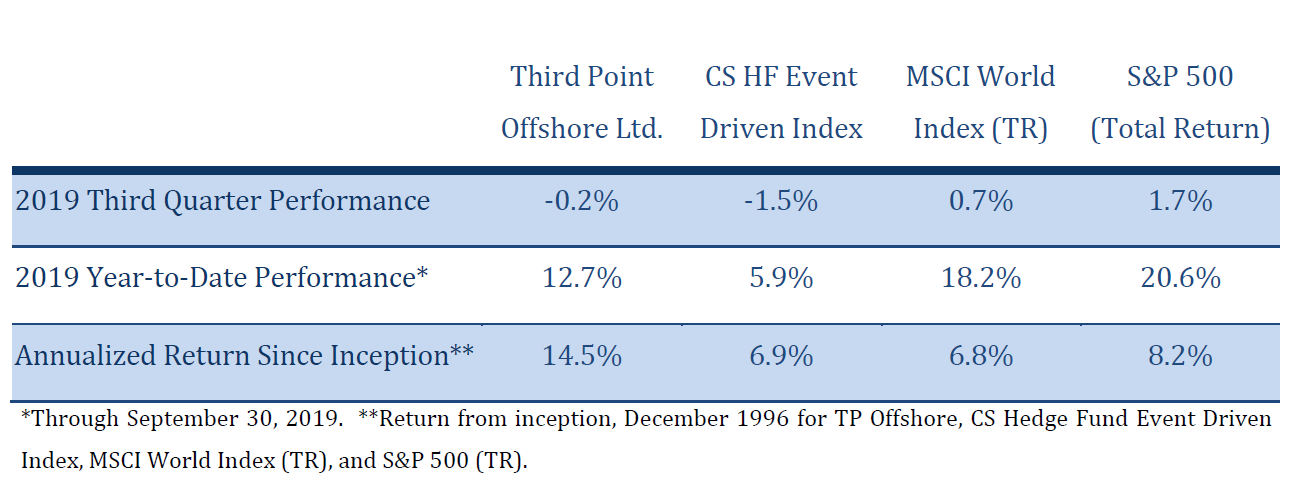

Third Point’s Offshore Fund lost -0.2% during the Third Quarter of 2019 and returned +12.7% through September 30, 2019.1 For the year through Q3 2019, our RoA for equity positions was +30.1% and equities contributed over 94% of our total net P&L. Returns for the year were driven by core activist equity positions including Baxter, Nestlé, Sony, Campbell’s, Sotheby’s and United Technologies Corp.; by a distressed credit position, Pacific Gas & Electric; and by two equity positions bought at attractive prices during a period of market dislocation. The main detractors for the year through September 30, 2019 were a sovereign bond investment in Argentina and single name shorts.

The market’s slight gain in Q3 masked tumultuous factor rotation. In August, equity portfolios tied to momentum or the near inverse – “laggards” – outperformed, as markets inflated assets reflecting economic weakening in a low inflation/low growth world. These momentum asset biases – favoring large cap over small cap stocks, growth versus value, or “min vol” strategies – became increasingly correlated, crowded, and sometimes expensive. The equation extended itself more acutely in secular growth names and similarly punished unloved shorts.

In September, and so far into October, this extreme positioning has been challenged by declining fears of an adverse trade war outcome, positive directional change in economic surprise indices, talk of fiscal stimulus outside the U.S., and an increasingly accommodative Federal Reserve. A steepening yield curve also has given life to under-owned assets at the expense of the over-owned. We were able to identify many of these shifts in Q3 and provided some protection to the long side of our book through position management, hedging, and directional optionality. However, the scale and suddenness of these factor moves caught us offsides in certain short positions.

As we look at conditions for Q4, U.S. consumer data is holding up but the gap between manufacturing and non-manufacturing data is wide. The large decline in interest rates over the past year has boosted financial conditions, and at a minimum, this should stabilize growth. With a base case of three rate cuts, the market has been sanguine that weak manufacturing data is not infecting consumers, but a continued implementation of tariffs poses a serious risk. With the election looming and weakness in the global economy, most observers expect we will get a mini deal on trade between China and the U.S. this year, putting further tariffs on hold. As we approach year-end, we like the flexible positioning of our portfolio, have a strong buy list in the event of further dislocations, and continue to re-underwrite our positions continuously as markets fluctuate.

Quarterly Results

Set forth below are our results through September 30, 2019:

The top five winners for the quarter were Sony Corp., Baxter International, Inc., Campbell Soup Co., Nestlé SA, and EssilorLuxottica. The top five losers for the period were Republic of Argentina, Centene Corp., The Chemours Co., Netflix Inc., and PayPal Holdings, Inc.

Assets under management at September 30, 2019 were $14.5 billion.2

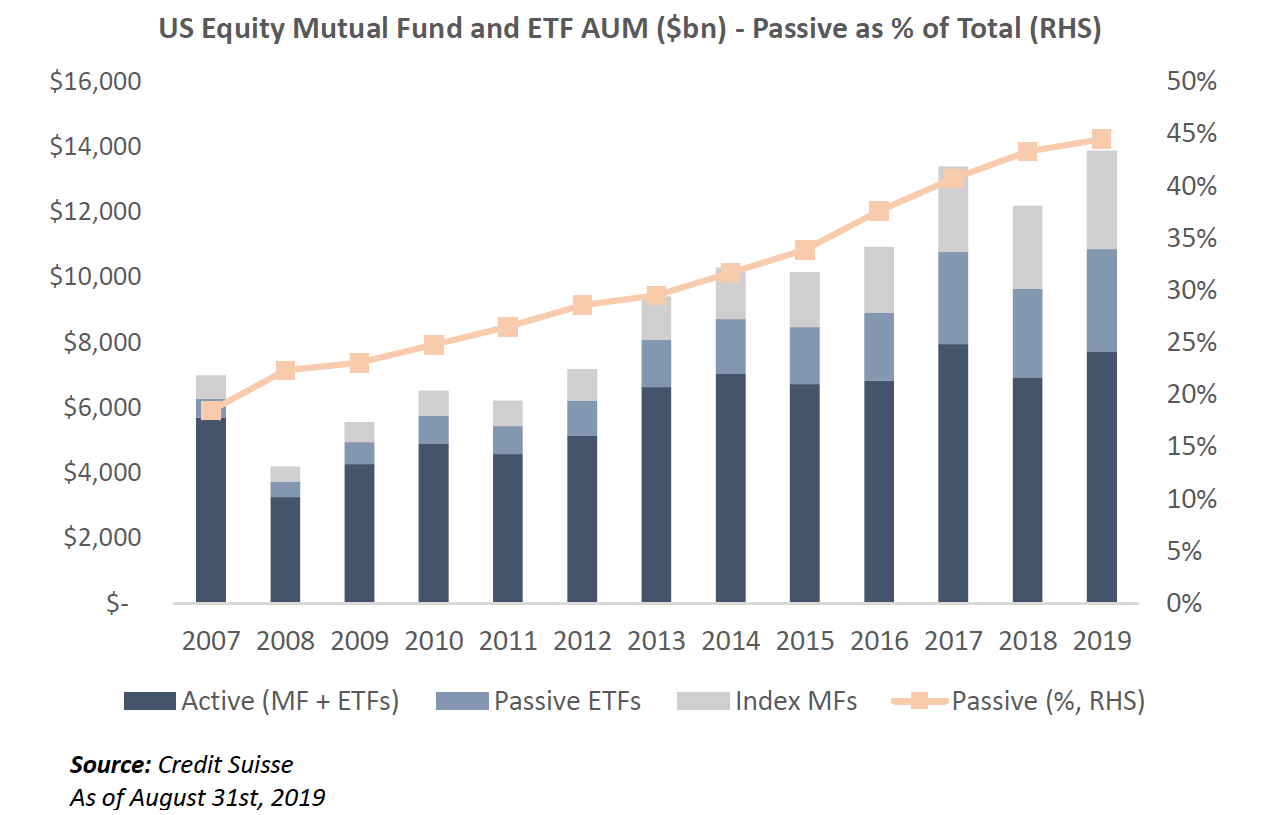

Activism: Generating Alpha in a Passive and Quantitatively-Driven Market

Investing with an event-driven approach by focusing on specific catalysts has been a core element of our process since our founding in 1995. Event-driven techniques can be applied to both credit and equity investments and act as a valuable discipline when screening ideas and timing entry and exit points. As our engagement methods in governance have evolved, we have demonstrated the many ways in which our activist investing can generate alpha for our investors. Activism allows us to create our own catalyst in concentrated positions where, by definition, we have a differentiated view of a company’s potential value based on our intervention. After many years of doing this, we benefit from pattern recognition in finding and sourcing ideas that we believe have favorable risk/reward characteristics – heads we win, tails we don’t lose too much. Today, we are dedicating more time and capital to activism, which has become an even more valuable strategy in markets increasingly dominated by passive and quantitative players.

The shift from active to passive holdings has been substantial and velocity is increasing, at the expense of active management:

Traditional investment frameworks are becoming less useful for active investors, particularly over the short-term, because stock ownership is increasingly concentrated among owners who are agnostic to company fundamentals and valuation.

Quants are also making it more difficult to generate equity alpha as their algorithms evolve. A typical fundamental analyst has behavior and biases that quant algorithms attempt to replicate and exploit. Quants are showing that analysts’ seemingly divergent viewpoints, which were thought to be their primary source of alpha generation, may actually be successful directional bets on momentum, growth, sector, or strategy factors that can be more effectively expressed via their models.

In a world where traditional forms of alpha are increasingly being commoditized and beta can be cheaply replicated, activism stands out as a valuable source of alpha available only to a small cohort of investors. Recognizing this, we created a dedicated governance team to enhance our activist idea generation and raised our second SPV this year to bring capital to a high-conviction activist idea. Over 40% of our portfolio today is in activist names – our highest percentage in history.

We have several strengths we believe distinguish our activist abilities that cannot be replicated by systematic players, including:

1) A successful track record and reputation for making change: As management teams, advisors, institutional investors, and fellow board members attest, Third Point brings credible insights to companies when we engage. We are selective with our investments, thoughtful in our proposals, and our recommendations are always in the long-term interest of the company. Our media and communication capabilities allow us to bring our message to market participants with precision and transparency.

2) A wide range of engagement techniques with companies: Our preferred method of activism is a constructive approach, where we work collaboratively with management teams to increase shareholder value. However, in the rare instances where constructive dialogue does not progress or a company is ossified, we can push for board and management changes. Our track record of working collaboratively with boards – whether invited on or otherwise – has enabled us to attract extraordinary candidates for board service.

3) An ability to invest globally: Our collaborative approach has enabled us to present ideas that might initially seem controversial but are later understood and adopted by companies across the globe. We have achieved this by presenting convincing ideas and often forming consensus with fellow shareholders and other stakeholders. Very few firms have a successful track record of engaged investing in North America, Europe, and Asia, and we see foreign markets as an enormous opportunity going forward.

4) Deep sector expertise: We have few generalists on our investment team. Most analysts are sector-focused with deep domain knowledge. These sector specialists work closely with Dan, Munib and our governance team on each investment. We believe the sector-specialist model improves the quality of our interaction with management teams and fellow investors and reduces the probability of errors in our investment theses.

5) Sophisticated hedging strategies: In order to maximize alpha and reduce idiosyncratic risk, we have bolstered our trade construction and risk management capabilities. This allows us to make a deliberate decision on how much market, sector, or factor risk we want to take. These bespoke hedges are created on an individual investment level and we layer in volatility strategies to enhance positioning.

6) A large capital base with a substantial portion of long duration capital: Our asset base includes two publicly listed vehicles and substantial employee capital that amounts to almost 30% of AUM and allows us to take positions in some of the largest companies in the world to advocate for change on behalf of shareholders. Our significant percentage of sticky capital and ability to raise SPVs with multi-year terms allow us to patiently wait for long-term changes and even undertake turnarounds.

So far in 2019, our top five performers and six of our top ten profit generators are activist positions that demonstrate our range of engagement techniques – from collaborative to contested. Our intention is to maintain or increase our exposures to activist ideas and continue to invest in our platform. Below we discuss our exit from a nearly six-year investment in Sotheby’s, a new position in EssilorLuxottica, and an update on Sony.

Sotheby’s

During the Third Quarter, Sotheby’s (“BID” or the “Company”) was sold to an entity controlled by Patrick Drahi. The sale marked the end of our six-year investment in BID, which began as an activist campaign at an “old master painting desperately in need of a restoration” and ended with an attractive acquisition at a 61% premium following a total operational overhaul of the business. When we first invested in Sotheby’s in 2013, we saw an iconic brand in need of new leadership after many years of middling growth despite strong art market tailwinds. The Sotheby’s campaign was hard-fought but ended with Dan and two Third Point director nominees joining the board. As a director on several committees, Dan worked closely with the rest of the board to bring in Tad Smith as CEO. Tad and his team (many of whom he recruited) revamped Sotheby’s corporate strategy around revenue growth and expense discipline and embraced technology to transform a centuries-old business model. They also dramatically improved capital allocation practices and optimized the balance sheet.

All these initiatives took time to play out but ultimately put the Company on a solid path to growth and made it an attractive acquisition target. In the five years Dan spent on the Board, our team collaborated with Sotheby’s in numerous ways, advising both formally and informally on communications, strategy, and shareholder interests, something made possible by the trust that developed between us. Sotheby’s is far stronger after our six years of involvement and we are confident that returning the Company to private hands is an excellent outcome for all of Sotheby’s stakeholders.

EssilorLuxottica

Third Point holds a ~$700 million stake in EssilorLuxottica (the “Company” or “EL”), which we purchased in early 2019. EssilorLuxottica is the world’s largest eyecare company, generating over €17 billion in revenue and nearly €4 billion in EBITDA annually. Formed in late 2018 through the merger of Essilor, the world leader in ophthalmic lenses, and Luxottica, the world leader in eyeglass frames and sunglasses, the pro forma Company has the industry’s only vertically integrated business model from design to manufacturing to retail sales. The logic behind the merger was elegant: combining frames and lenses allows the Company to control the entire eyewear value chain and transform an antiquated industry structure. Both consumers and shareholders should reap the benefits.

Eyecare is an attractive industry, with over €100 billion in revenue and several structural growth drivers. Over the next 30 years, secular trends including an aging population, consumer lifestyle changes such as staring at screens and less time outdoors, and emerging markets penetration will lead to ~2 billion more consumers with vision correction needs.3

EssilorLuxottica has many of the key characteristics we look for in an investment: compelling end-market growth in a defensive category, strong market share, high returns on invested capital, potential for incremental capital deployment, and competitive moats created by brands and technology.

The combined EssilorLuxottica has the potential to grow well ahead of the industry. Eyecare is an underdeveloped consumer category – online and omni-channel selling is in its infancy, the retail channel is highly fragmented, and many consumers, particularly in emerging markets, do not have access to vision care. EL plans to use its scale, global footprint, and product innovation to optimize the market. For example, the Company is improving access to vision diagnostics equipment and leveraging its consumer touchpoints to increase awareness around vision correction. By driving conversion rates of high-value lens coatings and premium eyewear brands, EL will accelerate growth across the eyecare industry.

Despite EL’s scale and strong brands, the Company sells less than 10% of glasses purchased worldwide each year and independent optical stores account for over half of the global market and upwards of 80-90% in emerging markets like India and Latin America. This fragmented industry structure, combined with EssilorLuxottica’s clean balance sheet, presents a significant opportunity for consolidation, particularly in retail distribution. These types of acquisitions have proven highly accretive for EL due to its ability to in-source procurement and distribute well-known brands through a new retail network. The proposed acquisition of GrandVision is the latest example of this successful strategy.

Synergy Opportunity

The merger provides a runway to create additional value over the next several years. Our analysis of potential merger synergies points to over €1 billion in additional profit through efficiencies and revenue growth, almost double the Company’s current targets. In the near-term, this will be driven by cross-selling to wholesale customers, in-sourcing lens procurement, and supply chain efficiencies. The longer-term opportunity to disrupt the industry value chain is even more appealing: combining lens and frame to shrink raw material need and waste, reducing shipping costs by merging prescription labs with global distribution hubs, and providing a true omni-channel sales offering. These initiatives will transform the way glasses are sold, significantly improving the customer experience.

The combination of two powerful franchises in the eyecare space, meaningful top and bottom-line synergies, and ongoing capital deployment, present a compelling long-term opportunity to increase earnings. We expect EssilorLuxottica to grow earnings and free cash flow at a mid-teens CAGR for the next several years. Combined with the GrandVision acquisition, we expect EL to earn over €8 of EPS in 2023, nearly doubling the figure from 2019.

Governance

While both Essilor and Luxottica had impressive track records of value creation as independent entities, the combined Company is challenged by a poor corporate governance framework. The 2017 Combination Agreement currently in place effectively permits Essilor and Luxottica to continue to run as independent companies. A deadlocked board and management team has slowed integration and strategic decision making.

Despite its many advantages, EssilorLuxottica is losing favor among shareholders who are frustrated by the lack of synergy realization. With an array of potential threats – upstart brands, insourcing by major fashion houses, and disruptive technologies – the board and the Company should accelerate leadership transitions and delineate a timely merger strategy.

We have met with many of EL’s executives and shared with their board our views formed through many years of experience in partnering with companies to upgrade governance and drive strategy. We are confident that actions to improve governance can unlock a compelling multi-year value creation opportunity that will benefit all stakeholders – shareholders, employees, and the billions of consumers who will gain access to life changing vision care.

Sony Update

In late September, Sony (the “Company”) disclosed the results of an in-depth review conducted by the Company with the assistance of its advisor, Goldman Sachs, over the past several months. The review was undertaken in response to our earlier conversations and to a presentation we shared on June 13, 2019 at www.astrongersony.com where we proposed numerous portfolio improvements and a more coherent capital allocation policy to improve Sony’s valuation and position the Company for long-term success.

Most investors expected that following a lengthy review, Sony would share some meaningful plans to close the yawning gap between its share price and intrinsic value. We were looking forward to a thoughtful articulation of a strategy to streamline Sony’s portfolio, including a plan to use proceeds from divestitures either to strengthen and grow the Company’s core businesses or reduce share count at the currently steep discount. While we did not expect that all our requests, such as the separation of the image sensor business, would be addressed immediately, we did expect that the Company would make some recommendations to address the structural impediments to long-term value creation for Sony’s shareholders.

Instead, Sony revealed that the review’s conclusion was to maintain the status quo with no concrete proposals to improve the business. As students and practitioners of Japanese business principles like kaizen, it is difficult for us to imagine that a company of Sony’s size and complexity could not find a single concrete action to improve its business and valuation.

We are committed to a continued constructive dialogue with the Company and to creating long-term value at Sony for all stakeholders. Discussions are ongoing, guided by our view that Sony remains one of the most undervalued large capitalization stocks in the world.

Argentine Credit Update

Our largest loss in the Third Quarter was in Argentine sovereign debt, when a surprising outcome in the August 11th presidential primary caused a panic in the capital markets. Argentine credit generated significant profits for us from 2014-2016 and our return to the sovereign bonds was driven by our view that: 1) the incumbent President, Mauricio Macri, had a good chance of prevailing in the national election in October as he had been gaining in polls and nearly every piece of data correlated with his electability was improving. We expected Macri to lose in August but by a slim margin to the opposing, market-unfriendly ticket of Alberto Fernández and Cristina Kirchner; and 2) even if the Fernández ticket prevailed in the general election, Argentina’s economic fundamentals and Fernández’s background suggested that the draconian restructuring the market feared was unlikely.

In failing to anticipate the extent of Macri’s loss in the primary election, our most significant mistake was missing the second order thinking that in such a scenario, Argentina would be rudderless for almost three months between the August primary and the October election and economic mayhem could ensue. The huge margin in the primary effectively made Alberto Fernández the country’s President, but he had limited opportunity or incentive to calm the market while Macri remained in power. In this vacuum, investor fears spiraled into a massive sell off in the currency and reserve depletion, making a debt restructuring inevitable.

Opportunistic investing success comes from having a differentiated view at the right time; in this case, our thesis was left in limbo and to avoid unacceptable downside risk, we reduced our position at higher levels than are prevailing today. When the October 27th election presumably makes Alberto Fernández president-elect, we expect debt restructuring negotiations to begin and while this process will likely lead to more volatility, we anticipate that the bonds will ultimately recover significantly more (30-50%) than current prices.

Business Team Updates

Since Bob Boroujerdi joined Third Point last September, he has made a meaningful impact in upgrading all aspects of portfolio management including our research processes, data analytics, hedging strategies, risk management, and technology infrastructure. He also works closely with senior leadership on strategic initiatives around talent development, cross-asset efforts, and counterparty relationships. With his many contributions, Bob has quickly become an important leader at the firm and has assumed the newly created role of Head of Markets and Portfolio Strategy. Bob will continue to oversee his broad agenda around managing markets and risk but also increase his focus on the breadth of the portfolio, its synchronicities, and where it – and the organization – can be improved.

In October, Parker Quillen joined Third Point, where he will focus primarily on short selling. Before joining Third Point, Parker was an analyst serving on Bridger Capital’s investment committee. He began his career in 1987 at Lazard Freres & Co’s Equity Capital Markets, before forming Quilcap Corp., a short-biased equity management firm, in 1994. He is a graduate of New York University with a B.A. in Economics.

Elissa Doyle formally joined our governance team as Head of ESG Engagement this summer. She remains Chief Communications Officer, a function she has held since joining Third Point over a decade ago and one in which she leads strategic communications for our activist investments. In the ESG role, Elissa will bring additional focus to our external governance initiatives, including engaging in dialogue with institutional shareholders. She will also develop internal ESG practices for Third Point and implement their integration throughout the firm.

In September, we welcomed Jenny Wood as our new Global Head of Marketing and Investor Relations. Jenny has been in the financial services industry for over two decades, since graduating from Dartmouth College. She started her career as an investment banker. After joining the hedge fund marketing world at Cantillon Capital, she moved to Senator Investment Group where she led marketing and strategy efforts for a decade.

Quarterly Investor Update Call

Our Q3 Portfolio Review and Business Update will be held on October 24, 2019. A replay of the call will be available for two weeks following the event. Please contact Investor Relations at ir@thirdpoint.com or at 212.715.6707 with questions.

Sincerely,

Third Point LLC