Dividend investors look for sustainable and decent dividends with upside potential. Value investors chase undervalued stocks on an absolute and relative basis with catalysts that could unlock significant shareholder value while also closing the valuation disconnect.

Q1 hedge fund letters, conference, scoops etc

TransGlobe Energy (TGA), at the current price of $1.90 per share, can satisfy both types of investors. Actually, we believe that TGA offers a combination that’s hard to find and we will elaborate on this in the next paragraphs.

Assets Overview

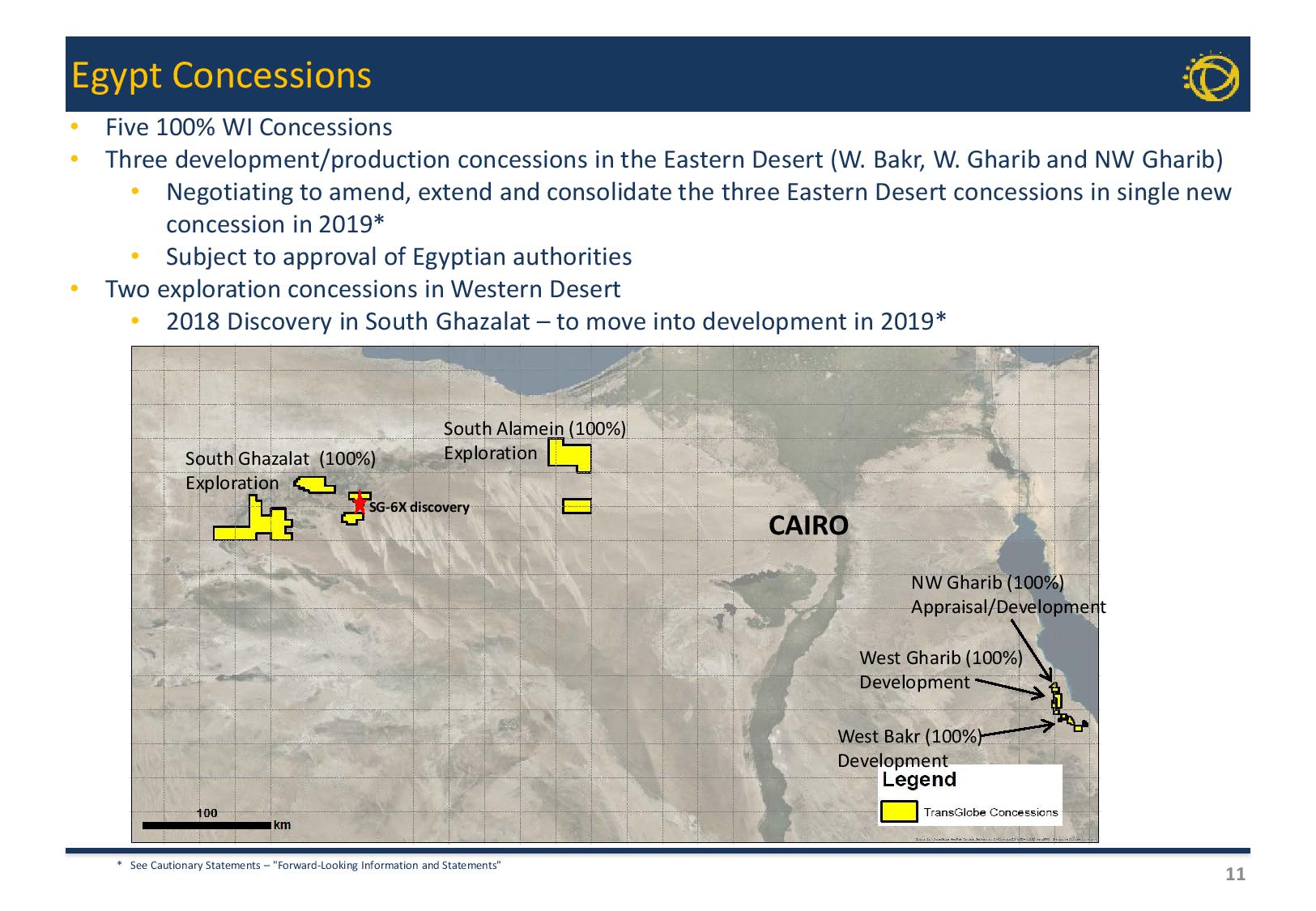

The company has a diversified asset portfolio with acreage in Egypt and Canada, as illustrated in the following 3 images:

Jan 2019 Corporate Presentation

Jan 2019 Corporate Presentation

Jan 2019 Corporate Presentation

TGA has been operating in Egypt over the last 15 years. The developed and producing assets in Egypt are located in the Eastern Desert (West Bakr, West Gharib, North West Gharib) while the undeveloped exploration assets are in the Western Desert (South Alamein, South Ghazalat). The assets in Egypt currently produce approximately 12,200 boepd (100% light oil).

The Canadian assets are located in the Harmattan area in Alberta and consist of producing and undeveloped land (38,000 and 39,000 net acres, respectively). TGA sold all its Canadian assets and exited Canada in 2008, but it re-entered Canada in late 2016 when it acquired the aforementioned assets from heavily indebted Bellatrix Exploration (BXE.T) in order to diversify its business into OECD countries and balance out its geopolitical risk associated with its operations in Egypt.

The Canadian assets currently produce approximately 2,500 boepd (~60% light oil and natural gas liquids [NGLs]) from the Cardium and Mannville formations. Offset operators include companies like Obsidian Energy (OBE), Whitecap Resources (WCP.T), Yangarra Resources (YGR.T), InPlay Oil (IPO.T), Surge Energy (SGY.T) and Bonterra Energy (BNE.T) that have largely de-risked these formations.

Strong Balance Sheet With Free Cash Flow And Zero Leverage

TGA produced 14,439 boepd and 15,270 boepd (95% oil & liquids) in 2018 and Q4 2018, respectively. Based also on the latest news, January 2019 production hit 15,400 boepd and February 2019 production was 15,000 boepd.

The slight increase in production is primarily driven by significant increases in the West Bakr and North West Gharib Concessions in Egypt where the well optimization recompletion programs in K and H fields are underway and production from new wells in M field continue to exceed forecast.

Meanwhile, TGA has maintained a pristine balance sheet without debt problems thanks to its discipline strategy and its low cost wells whose DCET (drilling, completion, equipping & tie-in cost) is approximately $1.5 million in Egypt and $2 million in Canada.

Actually, net debt is negative at approximately $34.2 million (as of December 2018), which means that cash & cash equivalents exceed the interest-bearing debt by this amount. Specifically, cash & cash equivalents are $51.7 million and interest-bearing debt is $52.4 million, while the estimated market value of inventoried crude oil of approximately 600,000 barrels is $34.9 million (as of 12/31/2018), according to the latest presentation.

As a result, TGA’s market cap is approximately $138 million and TGA’s Enterprise Value is approximately $104 million at the current price of $1.90 per share.

From a cash flow standpoint, TGA generated $63.3 million from its operations last year, up from $55.6 million in 2017. In other words, TGA currently trades less than 2 times its annual cash flow from operations.

This is absurdly cheap for a company with a pristine balance sheet. We believe that the geopolitical risk associated with its operations in Egypt is overdone and does not justify this extreme undervaluation. Hosni Mubarak, Egypt’s President from 1981 until 2011, was a key reason for the country’s long stability. Mubarak took the reins in the turmoil after Sadat’s 1981 assassination bringing stability in the social and economic life of this populous country with his business-friendly policies. Social unrest emerged in 2011 and the Arab Spring took place because Mubarak refused to hand over power, but the new President Abdel Fattah el-Sisi who became President in 2014 has restored stability while also having the support from the Trump administration.

Furthermore, 2018 CapEx was $40.7 million, which resulted in free cash flow of $22.6 million. This free cash flow was more than enough to cover a semi-annual dividend of $0.035 per common share, which translates into a cash payout of approximately $5 million annually.

And the free cash flow generation will continue this year because we project that operating cash flow will exceed $65 million based on futures strip prices, while CapEx will be just $34.1 million ($24.1 million for Egypt and $10 million for Canada), according to guidance. As such, TGA can afford to pay the same dividend this year while a dividend hike is not out of the question.

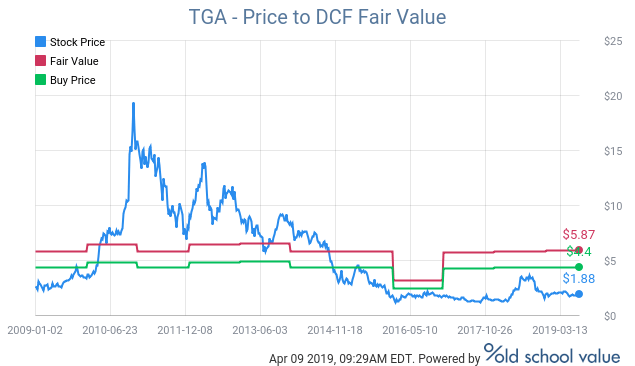

If you plug in $30M in FCF with a 2% growth and terminal value and a 10% discount rate (extremely conservative assumptions) into Old School Value’s DCF tool, you’ll get this:

This shows that TGA’s fair value is more than 3x the current price. The Margin of Safety is 68%. And that’s before you look at the upside potential.

Net Asset Value (NAV) Per Share

We guess that value investors will love this paragraph, too.

A few weeks ago, TGA released its reserves report. The Net Present Value (NPV) discounted 10% after tax of its PDP (Proved Developed Producing) reserves and 1P (Proved) reserves are $137.7 million and $227 million, respectively, while NPV discounted 10% after tax for 2P (Proved and Probable) reserves is $323 million.

Given also that the company’s net debt (December 2018) is negative at approximately $34.2 million, we will calculate the NAV per share in the table below:

| PDP reserves | 1P reserves | 2P reserves | |

| NPV discounted 10% after tax ($ million) |

137.7 | 227 | 323 |

| Net Debt ($ million) | 34.2 | 34.2 | 34.2 |

| Total ($ million) | 171.9 | 261.2 | 357.2 |

| Outstanding Shares (million) |

72.4 | 72.4 | 72.4 |

| NAV per share ($) | 2.37 | 3.61 | 4.93 |

The valuation gap is significant given that TGA currently stands at $1.90 per share. And it must be noted here that the calculation above gives zero value to the undeveloped acreage that is approximately 600,000 net acres in Egypt (after the recent relinquishment of North West Sitra) and 40,000 net acres in Canada.

If we add a minimal value of $10 per acre for the undeveloped acreage in Egypt and CAD$100 per acre for the undeveloped acreage in Canada, NAV per share obviously climbs higher.

Catalysts In 2019

Aside from the potential increase in oil prices, TGA has additional catalysts that could move the stock in the next quarters. Specifically:

1) South Alamein discovery in Egypt:

During the 2017 exploration program at South Alamein, TGA drilled the Boraq 5 well, which was a major disappointment with the well failing to recover oil on test. Nevertheless, TGA didn’t give up and drilled the Boraq 2 well, another exploration well in South Alamein in 2018. Boraq 2 was successful and was tested at 1,140 bopd of 35 API oil in Q4 2017.

Unfortunately, the Boraq 2 discovery doesn’t have sufficient scale to proceed with development, so TGA needs additional exploration success on the South Alamein Concession. As such, TGA approved another exploration well for South Alamein in the 2018 capital plan to test one of several exploration prospects identified on 3D seismic, which, if successful, could provide the additional reserves and productivity to bring forward a South Alamein development. However, the key problem with this acreage is that it’s located in a military area where access is currently restricted. TGA has resubmitted a request for military access to drill the SA 24X Jurassic exploration prospect and entered into extension discussions with the EGPC, which are ongoing.

On that front, TGA notes in the latest press release:

“Additional investment in South Alamein is conditional on negotiating the necessary extensions following the military rejection of access to the SA 24 X exploration well surface location.”

2) South Ghazalat discovery in Egypt:

TGA had a significant discovery last fall. Its South Ghazalat exploration well flowed at a rate of just over 3,800 bbls per day, which was a combined rate from two zones.

Based on this positive test result, the company filed a declaration of commerciality last December, and the development plan in February 2019. TGA expects to conclude negotiations and receive approval of a development lease from the Egyptian government in the next few months. If its plan is approved, it will begin the delineation of the existing discovery along with an early development and production later this year. TGA will also be merging and processing two existing 3D seismic surveys in the discovery area to firm up additional drilling locations for 2020.

However, the 2019 production guidance plan doesn’t currently include any production from the South Ghazalat oil discovery. Therefore, if this well of 3,800 bbls per day is producing prior to the year end, it can definitely move the needle given that the company’s original guidance for 2019 is 14,500 boepd.

3) Upward revision for 2019:

The 2019 production guidance is for 14,500 boepd (95% oil & liquids) but TGA is currently running above guidance thanks to significant increases in the West Bakr and North West Gharib Concessions in Egypt, according to the latest CC linked above:

“In the Eastern desert, we have provided 2019 full year production guidance in the range of 11,500 barrels to 12,400 barrels of oil per day. As Lloyd just mentioned, we are currently running above guidance, but at this time we are not revising our full year estimates.”

If the Canadian operations remain smooth in the next months, we expect the company to revise the original guidance upwards in H2 2018.

4) The NW Gharib and West Bakr exploration wells in Egypt:

Based on its exploration program for 2019, TGA is targeting an undrilled fault block north of the NWG 38A pool at the NW Gharib concession.

Also, at West Bakr, the company will be targeting the formation that is proven to be successful by a neighboring company, so the company says that it’s cautiously optimistic about its chances of having discovery there, as quoted from the latest CC below:

“With respect to the West Bakr exploration well, the target on that one, it’s a bit, a bit challenging to give you a whole prospect size on that. We do know that the wells to the south there’s a pool down there that is producing something in the order of 2,500 barrels a day from three wells. So we’re optimistic, we’re going to get a positive well if it extends that far north. Typically those wells would recover in the three to five hundred thousand barrels per well range, but until we test the structure it’s hard to say.”

5) The South Harmattan exploration well in Canada:

The company will drill 4 Cardium horizontal wells in 2019 including an outpost well to begin evaluating the South Harmattan acreage acquired in 2018. According to the latest presentation, success in the South Harmattan area could add between 30 and 40 additional potential drilling locations (one mile Hz wells at four per section).

6) Acquisitions:

Aside from the organic growth in Egypt and Canada, TGA states in the latest presentation linked above that its 2019 plan is to maximize its free cash flow by targeting value growth opportunities in Egypt and in Canada.

The company has also stated that it has a long-term goal of building its Canadian business up to the size of its Egyptian one. And it recently repeated this goal during the latest CC linked above, as quoted below:

“For any of you on the line who are new to TransGlobe, we bought West Bakr these assets in late 2011. The fields had been producing consistently since the early 1980s between three and four thousand barrels a day. Since we took them over in 2011, we have more than doubled the average daily production. This is exactly the type of opportunity we are looking for from an M&A perspective, under loved and underdeveloped or under exploited opportunities.”

7) Pipeline news in Canada:

Due to its exposure to Canada, TGA is negatively impacted by the ongoing pipeline egress issues in the country. To get a better idea of this problem, WTI decreased in Q4 2018 by 15% over the third quarter of 2018 but the Western Canadian Select (WCS) average benchmark price decreased by 59% while the Edmonton Light (MSW) price decreased by 48% over the third quarter of 2018 due to a lack of egress optionality.

Therefore, positive news regarding the egress problems facing Alberta could have a material impact on sentiment. Currently, vital infrastructure projects such as Trans Mountain pipeline, TransCanada’s (TRP) Keystone XL and Enbridge’s (ENB) Line 3 keep facing delays, but the pressure is mounting to get some or all these projects built, while elections in Canada will take place this fall.

Takeaway

TGA pays a sustainable dividend while currently trading less than 2 times its annual cash flow and significantly below its NAV per share (PDP, 1P, 2P). Moreover, it has zero leverage while generating free cash flow that allows it to look for growth opportunities in Canada and Egypt.

As a result, we believe that TGA at the current price of $1.90 per share deserves a place in a diversified and value-driven energy portfolio.

Disclaimer: The opinions expressed here are solely my opinion and should not be construed in any way, shape, or form as a formal investment recommendation. Value Digger does not accept any liability for any loss or damage whatsoever caused in reliance upon such information. Investors are advised that the material contained herein should be used solely for informational purposes. Investors are reminded that before making any securities and/or derivatives transaction, you should perform your own due diligence. Investors should also consider consulting with their broker and/or a financial adviser before making any investment decisions.

What is Old School Value?

Old School Value is a suite of value investing tools designed to fatten your portfolio by identifying what stocks to buy and sell.

It is a stock grader, value screener, and valuation tools for the busy investor designed to help you pick stocks 4x faster.

Check out the live preview of AMZN, MSFT, BAC, AAPL and FB.

Article by Nathan Kirykos, Old School Value