Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

[REITs]

Q2 hedge fund letters, conference, scoops etc

Because Treasury bonds are the safest fixed-income securities, they have the lowest yields in the U.S. dollar universe. This can make them seem boring in a portfolio; something you must own to be prudent, but a drag on higher returns. The reality is different and will surprise you.

This article compares the performance of the premier investment-grade bond index, theBloomberg Barclays Aggregate Bond Index (AGG), to the performance of its subset U.S. Treasuryindex. Surprisingly, the long-term performance of the Treasury index is nearly that of the AGG, and outperformed it in several crucial periods.

Treasury bonds perform nearly as well as investment-grade bonds over the long-term.

The AGG captures the performance of U.S. taxable investment-grade bonds. This includes Treasury bonds, investment-grade corporates, mortgage-backed bonds (MBS), commercial mortgage-backed bonds (CMBS), and other asset-backed bonds (ABS). Some of the largest and most familiar bond funds use the AGG as a benchmark, including the PIMCO Total Return Fund(PTTRX) and DoubleLine Total Return Bond Fund (DBLTX).

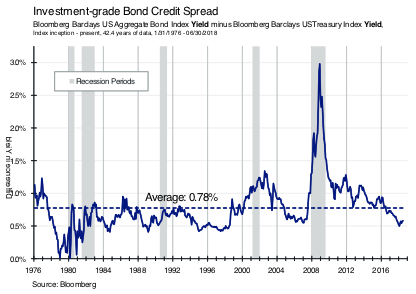

The performance of U.S. Treasury bonds, 38% of the index, is isolated in a subset index, the Bloomberg Barclays U.S. Treasury Index. As you might expect, because Treasury bonds have no credit risk, the yield of the Treasury index is less than that of the whole index. This yield difference (also known as the credit spread) varies as the perceived risk of default changes over time and averaged 0.78% over the full period (see chart below).

It is logical that the long-term performance difference of the two indices would be approximately the same, but it isn’t…not even close. Despite the Treasury index yielding 0.78%less, it performed just 0.15% annualized less over the full period (see chart below).

How could this be? There are three reasons. Bonds with credit only have higher yields because they have a chance of default. In the aggregate, if the market is efficient, the yield premium should compensate for the amount of bond defaults. Said another way: Over the long-term, there is no reason for the universe of credit bonds to outperform Treasury bonds; the performance loss from defaults should be equal to the yield premium. It is only when you bet on subsets of them that don’t default that an outperformance can develop.

Bonds may start in the index but, within their lifetime, may be downgraded to below investment grade and therefore are taken out of the index at distressed prices; regardless of whether they default.

The third reason is that, at any given time, the index is valued where all the bonds are marked-to-market and so their performance is the combination of cash flow as well as price changes from movements in interest rates.

No matter the reason, if Treasury bonds perform virtually as well as the AGG, what is the point of adding complexity where none is needed?

Read the full article here by Eric Hickman, Advisor Perspectives