Triton is an intermodal shipping container company (i.e. the ubiquitous steel boxes on ships, trains and trucks), and it offers a tempting 6.3% dividend yield. But before you consider owning shares (or hanging on to the shares you already own), you might want to consider a couple big risks.

Q3 hedge fund letters, conference, scoops etc

Overview:

Triton is the world’s largest lessor of intermodal containers and chassis. Intermodal containers are large, standardized steel boxes used to transport freight by ship, rail or truck. Because of the handling efficiencies they provide, intermodal containers are the primary means by which many goods and materials are shipped internationally.

Triton operates its business in one industry, intermodal transportation equipment, and has two business segments:

Equipment leasing – Triton owns, leases and ultimately disposes of containers and chassis from its lease fleet, as well as manages containers owned by third parties.

Equipment trading – Triton purchases containers from shipping line customers, and other sellers of containers, and resells the containers to container retailers and users of containers for storage or one-way shipment.

The Shares are Attractively Priced:

Triton’s shares have recently sold off, as shown in the following chart.

Before getting into the big risks, we first consider some reasons why we believe the shares are attractively priced. For starters, here is a look at Triton’s decreasing enterprise value to EBITDA, an increasingly attractive valuation, in our view.

And despite the decreasing valuation, the business is getting better, mainly because the economy is getting better (as the economy strengthens, more goods are shipped in Triton’s containers). And more specifically, here are some drivers of Triton’s profitability:

Economies of scale are another contributor to the improving business, as shown in the following graphic (Triton benefits from being bigger than its competition).

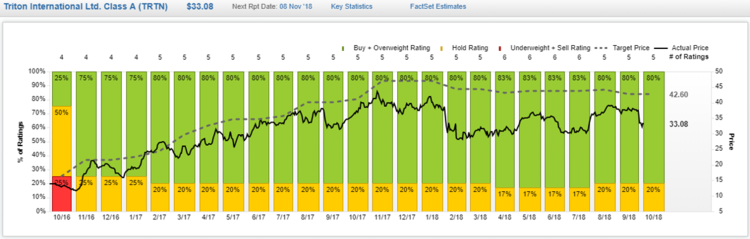

Also worth noting, the Wall Street analyst that cover Triton, like the business, and believe the shares are undervalued, as shown in the following graphic.

And more specifically, analyst earnings per share (“EPS”) estimates have been improving.

Analysts also expect dividends, cash flows, and book value to increase in the years ahead, as shown above.

The Big Risks:

Yet if the business is strong and improving, why have the shares sold off. In a word, the answer is: Fear. Unwarranted fear, in our view. Specifically, China “Trade War” fears, and general market disbelief as stocks (and the economy) continue to “climb the wall of worry.”

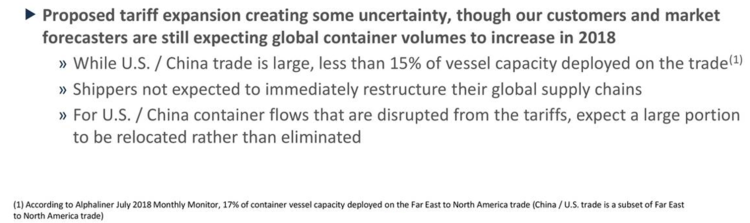

Regarding the Trade War, Triton acknowledges this is a risk, but perhaps not as significant as many market participants believe. In our view, the media pundits have over-sensationalized and exaggerate the trade war risks, and this has contributed to the shares selling off. For example, according to JP Morgan CEO, Jaime Dimon “it’s not a trade war, it’s a trade skirmish.” Nonetheless, here is what Triton has to say about it:

Regarding Global Economic Conditions, it is true that international markets have not been as strong as the US, and that can be a drag on Triton’s stock price, but in reality Triton’s business has been strong and is improving (as described earlier in this report, and as we’ll describe in more detail later when we get into cash flows). It seems the market continues to climb the proverbial “wall of worry,” and the strength of the US will continue to spill over to the rest of the world (despite what media pundits and fearmongers say). International markets are connected, and a rising tide raises all ships. Further, bull markets don’t end due to time, they end due to something specific, such as lower earnings or an economic shock, neither of which we are experiencing yet in this recovery.

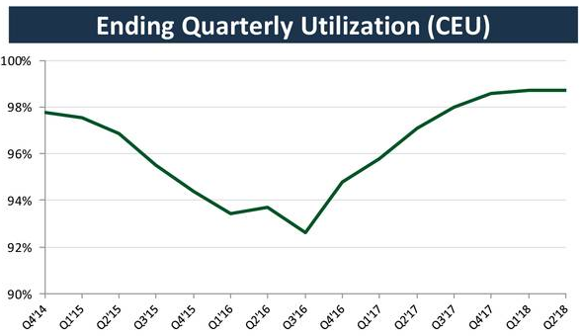

Also, in Triton’s case in particular, the market is too backward looking. Specifically, the entire industry faced challenges in recent years due to challenging supply/demand dynamics, which have since stabilized. For example, Triton’s quarterly Utilization Rate has improved.

Cash Flow:

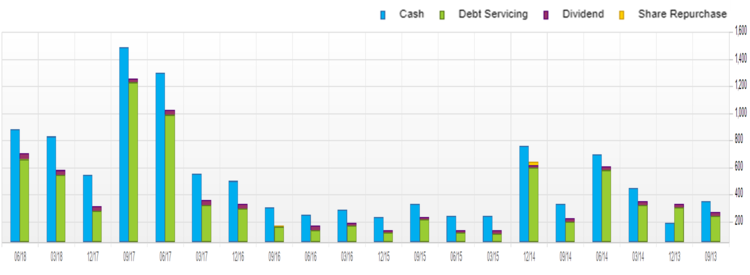

We’d be remiss not to cover Triton’s cash flow situation. For starters, the company has lots of cash flow, but also plenty of debt to service, as shown in the following chart.

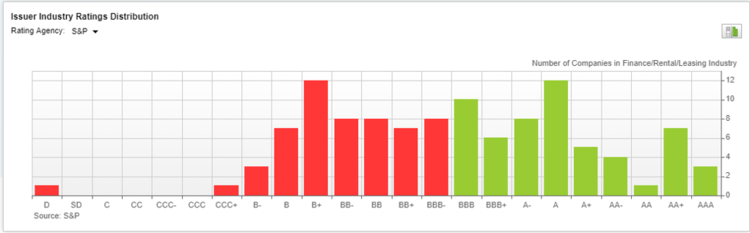

Triton’s debt is rated BB+ by S&P which is not the greatest or the worst for the industry as shown in the following graphics.

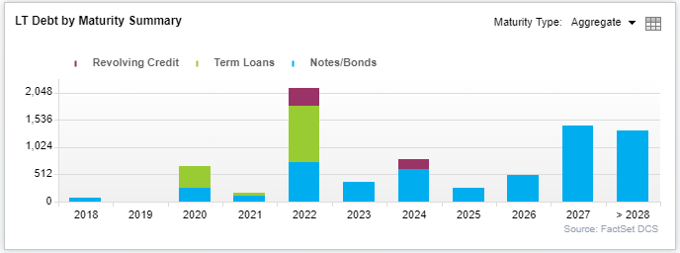

Importantly however, the debt maturities are well staggered, which helps make it more manageable, and is a smart move by management.

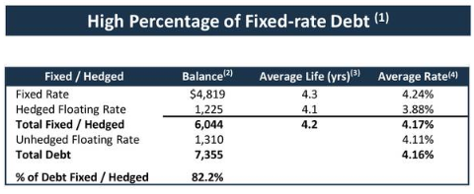

Also, a high percentage of the debt is fixed, which is compelling in our current rising interest rate environment.

Further still, the quarterly dividend was increased to $0.52 (from $0.45) earlier this year, an indication of strength from management, and also consistent with improving financial conditions expected by Wall Street analysts, as described earlier in this report (Note: Triton’s dividend has been historically classified as a return of capital, which can have important tax implications, particularly when you sell your shares). Further still, Triton’s board of directors recently authorized up to $200 million in share repurchases, another indication of financial strength.

Conclusion:

Triton faces two big risks (the threat of a full-blown trade war, and backward looking investors in fear of an over-extended bull market run). In our view, both of these risks are overblown and exaggerated. Triton’s business is healthy, and has room to strengthen further. We believe shares of Triton are priced too low, and the stock has significant upside, and for these reasons—we have specifically highlighted Triton in our recent report: 100 High-Yielders Down Big: These 5 Are Worth Considering. If you are looking for attractive yield, and the potential for strong price appreciation, consider Triton.

Article by Blue Harbinger