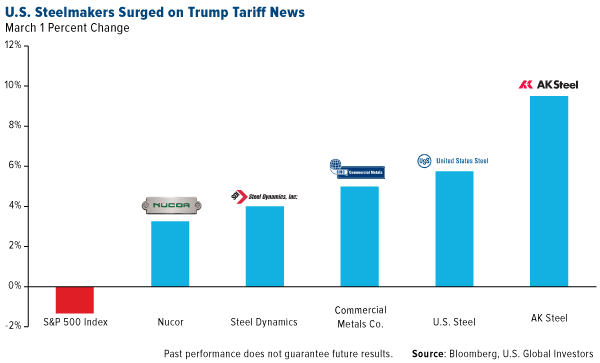

President Donald Trump’s proposed tariff on imported steel and aluminum, at 25 percent and 10 percent, is much more than a shot across the bow. Indeed, this could be the official kickoff of the trade war we all anticipated. The protectionist trade policy, announced this week as the president met with metals executives, raised fresh inflation worries and had an immediate impact on capital markets.

As expected, the winners were domestic steelmakers. AK Steel, the only manufacturer in North America that produces carbon, stainless and electrical steels, rose as much as 9.5 percent Thursday.

AK Steel CEO Roger Newport praised Trump’s decision, saying he fully supports “the actions he plans to take to stem the tide of unfairly traded steel imports that threaten the national security of our country.”

Newport wasn’t alone. Drew Wilcox, vice president of steel giant Nucor, called the tariffs “a clear message to foreign competitors that dumping steel products into our market will no longer be tolerated.”

Among the biggest losers from the news were automakers, which account for a little more than a quarter of steel demand in the U.S., according to the American Iron and Steel Institute (AISI). That makes the industry the second-largest consumer following construction. Ford, General Motors and Fiat Chrysler all fell more than 2 percent Thursday, and losses extended into Friday.

Get Ready for Higher Consumer Prices

To be clear, this is a huge deal, with serious inflationary implications. The U.S. is the world’s largest steel importer, so it’s very possible we could see retaliation from multiple trading partners on exports ranging from Florida orange juice to Kentucky bourbon to Wisconsin cheese. It’s hard to imagine a scenario where this is not passed on to consumers.

Trump was reportedly advised to exempt select allies, but it appears he’s chosen a no-exemptions option. Canada, the top supplier of steel and aluminum to the U.S., was spared in 2002 when former President George W. Bush imposed tariffs as high as 30 percent on steel.

When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win, President Trump tweeted Friday morning.“Example, when we are down $100 billion with a certain country and they get cute, don’t trade anymore we win big. Its easy!”

The country with which the U.S. has the biggest trade deficit is China. In 2017, the deficit stood at $375 billion, which accounts for about 65 percent of the total U.S. trade deficit. The tariff on steel and aluminum should have a negligible impact, however, as the U.S. imports a relatively small percent of those metals from China.

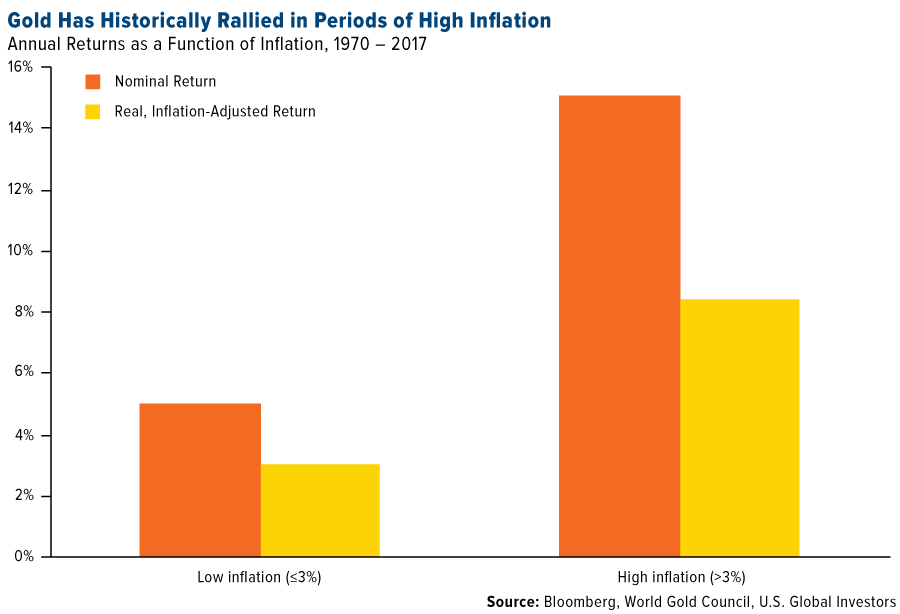

Gold Has Done Well in Times of High Inflation

As I’ve explained numerous times before, one of the most prudent ways investors have positioned their portfolios in times of rising inflation is by adding to their gold exposure.

The chart below, courtesy of the World Gold Council (WGC), shows that annual gold returns were around 15 percent on average in years when inflation was 3 percent or higher year-over-year, between 1970 and 2017. In real, or inflation-adjusted, terms, returns were closer to 8 percent. This is still higher, though, than average returns in years when inflation was lower.

According to the WGC, “gold returns have outpaced the U.S. consumer price index (CPI) over the long run, due to its many sources of demand. Gold has not just preserved capital, it has helped it grow.”

The most recent report from the Bureau of Labor Statistics (BLS) shows that consumer prices rose 2.1 percent year-over-year in January, but as I said earlier, real inflation could be grossly understated.

To learn more about how gold could be the solution to high inflation, click here!

My Journey Through the Blockchain and Cryptocurrencies

Gold and metals were definitely top of mind this week at BMO Capital Markets Global Metals & Mining Conference, held in sunny Hollywood, Florida. I had the pleasure to be on a panel at the four-day event, which was attended by more than 1,500 curious investors and advisors, representing approximately 500 different organizations from 35 countries.

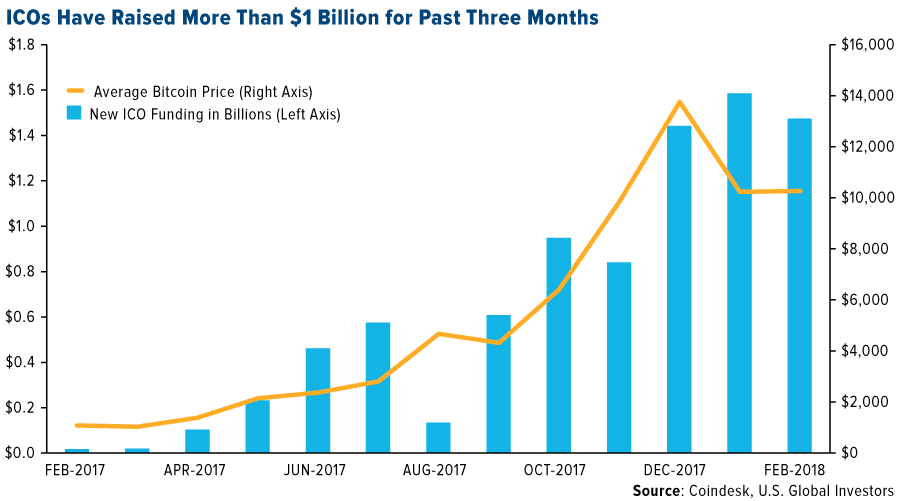

The panel I was on focused on blockchain technology and cryptocurrencies, which are reshaping how transactions are made and how companies raise funds across the globe. Startups raised more than $1.5 billion in February, the third straight month for initial coin offerings (ICOs) to generate over $1 billion.

Last year, $6.5 billion was raised through ICOs, according to Token Report, and it looks as if that amount will be exceeded in just the first few months of 2018. As I wrote back in October, more and more companies are opting to raise funds through ICOs instead of going public to bypass many of the restrictive rules and costs associated with getting listed on an exchange. And unlike with private equity, smaller retail investors can participate, though I must stress that this is a very speculative trade.

The head of the Securities and Exchange Commission (SEC), Jay Clayton, strongly agrees with that last point. In December, he issued a statement explaining why he believes certain ICOs should fall under the jurisdiction of federal securities law and, as such, be filed beforehand.

Up until this point, the agency has taken few actions, but it appears it’s ready to start getting more aggressive against fraud. The Wall Street Journal reports this week that the SEC has issued “dozens” of subpoenas and information requests to cryptocurrency firms and advisors.

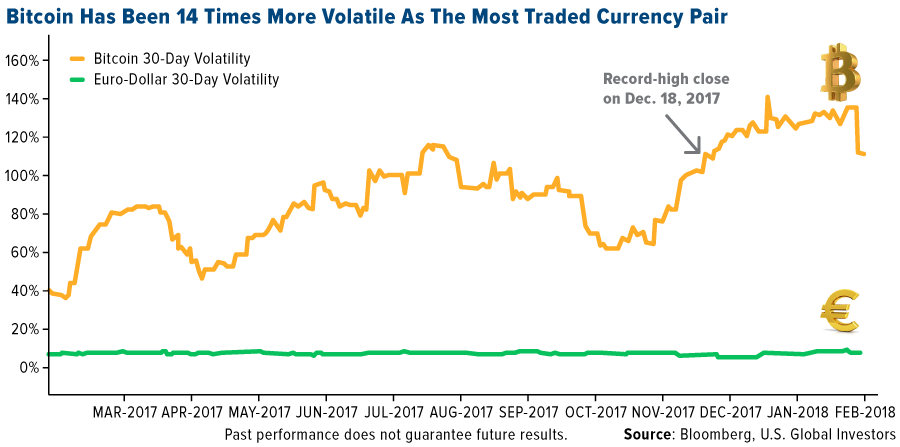

You might think this would hurt cryptocurrencies, but the prices of a number of them were up following the news. Bitcoin jumped nearly 6 percent on Thursday, as the token has often been seen as a “safe haven” in the cryptocurrency market.

HIVE Involved in Minting Virgin Coins

As many of you reading this know, U.S. Global Investors made a strategic investment in HIVE Blockchain Technologies in September, and as of today, it remains the only publicly-listed company that’s engaged in the mining of virgin tokens. HIVE and its partner Genesis Mining—the world’s largest cloud bitcoin mining company—are the leading miners and owners of Ether, the “crypto-fuel” for the Ethereum network. None of these assets has been used in any transaction, just as a newly-minted U.S. dollar, hot off the press, has never been used.

I continue to be optimistic about cryptocurrencies and see a very bright future for blockchain technology. The sentiment was similarly good among many of the attendees of this week’s conference. It’s only just the beginning.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 3.05 percent. The S&P 500 Stock Index fell 2.04 percent, while the Nasdaq Composite fell 1.08 percent. The Russell 2000 small capitalization index lost 1.03 percent this week.

- The Hang Seng Composite lost 2.32 percent this week; while Taiwan was down 0.89 percent and the KOSPI fell 2.01 percent.

- The 10-year Treasury bond yield remained essentially flat at 2.87 percent.

Domestic Equity Market

Strengths

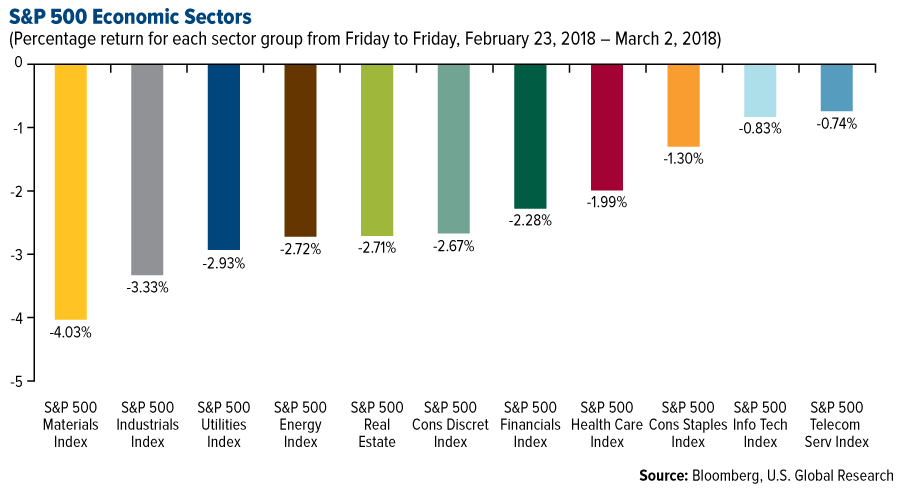

- Telecommunications was the best performing sector of the week, decreasing slightly by 0.74 percent versus an overall decrease of 1.99 percent for the S&P 500.

- Macy’s was the best performing stock for the week, increasing 13.72 percent.

- Salesforce raised its guidance. The cloud-software company beat on both the top and bottom lines and raised its revenue guidance for 2019 by $150 million, to between $12.60 billion and $12.65 billion.

Weaknesses

- Materials was the worst performing sector for the week, decreasing 4.03 percent versus an overall increase of 1.99 percent for the S&P 500.

- Patterson was the worst performing stock for the week, falling 22.47 percent.

- The Dow booked its worst month since 2016 this week. The Dow Jones Industrial Average fell 382 points on Wednesday, bringing its February loss to 4.28 percent.

Opportunities

- Bank of America Merrill Lynch has identified what it views as the two catalysts that can keep the almost nine-year bull market going strong. The two catalysts are an unanticipated surge in productivity growth and a speculative bubble from a rotation out of negative yielding debt into stock markets.

- Trump’s tariffs could make U.S. Steel’s operating income ‘laughably high.’ Cowen and Company analyst Novid Rassouli told Business Insider if steel prices increase 25 percent, which he believes is a distinct possibility, the company’s earnings before interest, tax, depreciation and amortization (EBITDA), “would be over double what it is right now.”

- According to Citi, buying shares in companies that spin-off assets has been a highly effective strategy. Citi analysis shows that, historically, both the parent and the spun-off company outperform in the year after the announcement. Citi’s analysts identified 14 U.S. companies that could unlock more value in a spin-off, mostly in the industrials and information technology sectors: NuStar GP Holdings, SemGroup, Orascom Construction, NuStar Energy, J2 Global, Conduent, Trinity Industries, Citrix Systems, Symantec, CNH Industrial, DXC Technology, Eaton Corp., Honeywell and General Electric.

Threats

- Optimism among American households about the stock market’s prospects was the highest on record in January. Now, not so much, after a volatile month. Figures from the Conference Board’s consumer confidence report on Tuesday showed 41.3 percent of respondents in February expected higher equity prices in the coming year, down from 51 percent a month earlier. The S&P 500 Index is down about 2 percent in February. In March 2007, the last time expectations weakened as much, the gauge was coming off a 3.5 percent slide a month earlier.

- Goldman Sachs’ base-case scenario calls for a 10-year U.S. Treasury yield of 3.25 percent by the end of 2018, though a “stress test” out to 4.5 percent indicates that such a move would cause stocks to tumble, economist Daan Struyven wrote in a note Saturday. He also said the economy would probably suffer a sharp slowdown but not a recession. “A rise in rates to 4.5 percent by year-end would cause a 20 percent to 25 percent decline in equity prices,” the note continued.

- Capitalism, as it is described in textbooks, is dead, according to Victor Shvets, global strategist at Australian investment bank Macquarie. The traditional business cycle that characterized post-World War II capitalism until the 1980s has been replaced by increasing debt levels and an abundance of capital and labor. “The key driver is what we refer to as ‘declining returns on humans and conventional capital’. Value and role of labor inputs (measured in hours worked) and conventional capital (finance, infrastructure, machinery) is declining,” Shvets said this month in a note to clients. Shvets said countries have reached the limit of borrowing to maintain their wealth levels. As a result, there has been “no clearance of past excesses,” leading to an unequal society, confusion among investors and the potential for a destabilizing war.

The Economy and Bond Market

Strengths

- U.S. factories expanded at the fastest rate since May 2004 in February, indicating sustained strength in manufacturing as demand remains solid, figures from the Institute for Supply Management showed. The factory index climbed to 60.8 (estimate of 58.7) from 59.1 in the prior month.

- U.S. consumer confidence jumped to a 17-year high in February as optimism about employment prospects grew and Americans began seeing additional money in their paychecks from recently enacted tax cuts, data from the Conference Board showed. The confidence index rose to 130.8 (estimate of 126.5), the highest since November 2000, from a downwardly revised 124.3 in January.

- The weekly U.S. jobless figures continue to reflect a tight labor market. U.S. filings for unemployment benefits fell last week to the lowest level in almost five decades, indicating the job market remains tight, Labor Department figures showed. Jobless claims decreased 210,000 (estimate of 225,000) in the week ended February 24, the lowest since December 1969. The four-week average of initial claims fell to 220,500, also the lowest since 1969.

Weaknesses

- Sales of new U.S. homes unexpectedly fell 7.8 percent in January to a 593,000 annualized rate, the lowest level since August, government data showed Monday. Borrowing costs and winter weather probably depressed demand that had been forecast to rise to a 647,000 rate, according to the median estimate of economists surveyed by Bloomberg.

- The Chicago-area PMI fell to a level of 61.9 (estimate of 64.1) in February from 65.7 in the prior month. Prices paid, new orders, employment, inventories, supplier deliveries and production all rose at a slower pace, but still signal expansion.

- The U.S. merchandise trade deficit expanded in January to the widest level in more than nine years, while inventories rose at wholesalers and retailers, according to preliminary Commerce Department figures. The goods-trade gap increased to $74.4 billion (estimate of $72.3 billion) from $72.3 billion in the prior month. Wholesale inventories rose 0.7 percent from a month earlier, while retail stockpiles climbed 0.8 percent.

Opportunities

- The Atlanta Fed’s GDP Now Index for predicting U.S. economic growth has become more optimistic than the forecasts of Wall Street economists for the first quarter of 2018. The index forecasts U.S. GDP will expand 3.54 percent in the quarter, up from 2.58 percent in its previous release on February 27. This compares with the 2.7 percent consensus forecast of 64 economists and contributors in a Bloomberg survey. The New York Fed’s first quarter GDP forecast was unchanged at 3.11 percent on February 23.

- Weakness in overall household consumption in January was foreshadowed by lackluster retail sales. However, softness in personal spending should be temporary, likely the result of two factors: adverse weather hindered retail sales at the beginning of the month, and the January data may be a payback after a stellar fourth quarter. Robust disposable income growth, driven by tax cuts, will likely boost consumption as the first quarter progresses.

- Hedge funds and other large speculators dialed back a record wager against 10-year U.S. Treasury futures, signaling that bearish sentiment is fading in the world’s biggest bond market. The group, known for trading on momentum, cut its short position by 59,575 contracts, the steepest reduction since November, to 896,019 contracts, according to Commodity Futures Trading Commission data through February 20. The benchmark 10-year yield reached a four-year high of 2.95 percent on February 21.

Threats

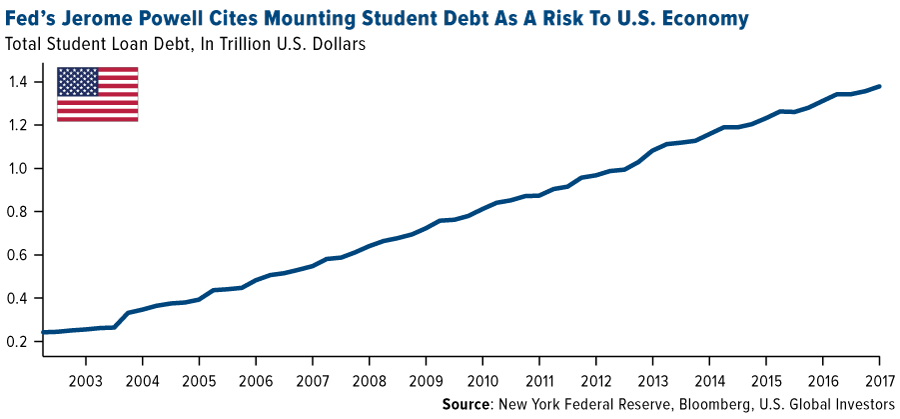

- Jerome Powell is concerned about the finances of America’s youth. In testimony to the Senate Banking Committee on Thursday, the head of the Federal Reserve said that growing student debt “absolutely could hold back growth” in the U.S. economy. Total student debt climbed to $1.4 trillion in the fourth quarter of 2017, the highest in New York Federal Reserve data going back to 2003.

- The leader of the House infrastructure panel said Wednesday it will be difficult to enact President Trump’s plan to upgrade U.S. public works this year, and lawmakers may have to take it up in a lame-duck session after the November election. Transportation and Infrastructure Committee Chairman Bill Shuster said he hopes to pass a bill before Congress leaves Washington for its August recess, but if that doesn’t happen an option may be to vote after the election.

- The highest gasoline prices in three years may force U.S. consumers to change driving habits this spring or curtail their spending, according to the nation’s biggest motoring group. Prices at the pump are expected to climb to nearly $2.70 a gallon in early April, the highest since the summer of 2015, amid increased demand and more expensive crude, AAA said. In states like California, a return to $4 a gallon is also possible.

Gold Market

This week spot gold closed at $1,322.52, down $6.23 per ounce, or 0.47 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.88 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 0.01 percent. The U.S. Trade-Weighted Dollar finished the week fairly flat with a lift of just 0.07 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-26 | New Home Sales | 647k | 593k | 643k |

| Feb-27 | Hong Kong Exports YoY | 16.1% | 18.1% | 6.0% |

| Feb-27 | Germany CPI YoY | 1.5% | 1.4% | 1.6% |

| Feb-27 | Durable Goods Orders | -2.0% | -3.7% | 2.6% |

| Feb-27 | Conf. Board Consumer Confidence | 126.5 | 130.8 | 124.3 |

| Feb-28 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Feb-28 | GDP Annualized QoQ | 2.5% | 2.5% | 2.6% |

| Feb-28 | Caixin China PMI Mfg | 51.3 | 51.6 | 51.5 |

| Mar-1 | Initial Jobless Claims | 225k | 210k | 220k |

| Mar-1 | ISM Manufacturing | 58.7 | 60.8 | 59.1 |

| Mar-6 | Durable Goods Orders | — | — | -3.7% |

| Mar-7 | ADP Employment Change | 195k | — | 234k |

| Mar-8 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Mar-8 | Initial Jobless Claims | 220k | — | 210k |

| Mar-9 | Change in Nonfarm Payrolls | 200k | — | 200k |

Strengths

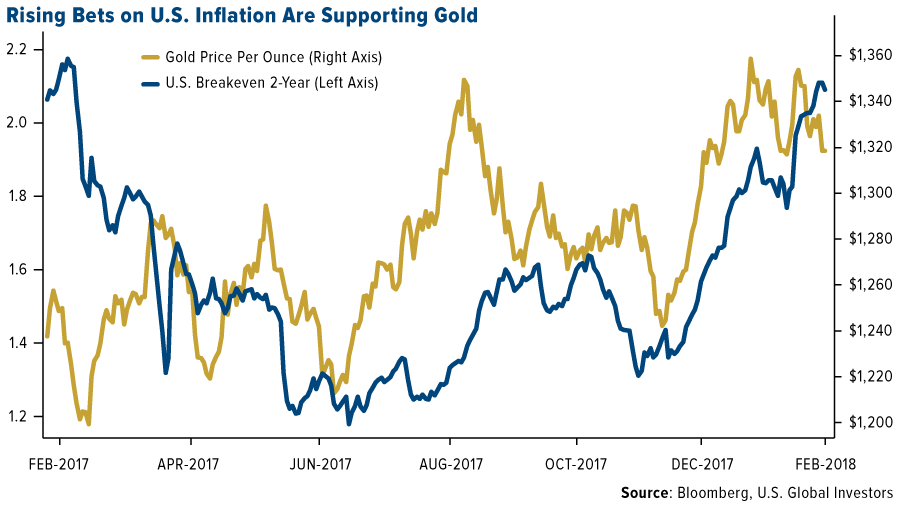

- The best performing metal this week was silver, nearly flat with a drift lower by just 0.06 percent. Sharp’s Pixley notes gold demand is on the rise while supply has begun to fall, signaling a potential increase in the gold price. Many see gold as appealing in the medium and long term due to the sustained demographic move into the middle class in China and India, the world’s two most populous nations.

- President Donald Trump announced tariffs of 25 percent on imported steel and 10 percent on aluminum. This aggressive position angered manufacturers and trade partners across the globe, resulting in a weaker U.S. dollar and declining equity markets across the U.S., Europe and Asia, according to Bloomberg. Gold, however, rallied on Friday after the market digested the news as inflationary. The formal order is expected to be signed next week and continue for “a long period of time.”

- Earlier this year, the price of Bitcoin plunged, along with the number of daily transactions. And while the cryptocurrency’s price has made a 50 percent comeback, reports Bloomberg, the trading level has not recovered, leaving some investors puzzled. The confusion on this decline hasn’t stopped the use of cryptocurrencies globally, though. In fact, Swiss gold trader Degussa Goldhandel is now allowing clients to pay with digital coins including Bitcoin, Ethereum and Litecoin, Bloomberg reports. Increased inflows into another popular investment, ETFs, were also recorded this week with the largest flows going toward commodity-focused products. Based on data from Bloomberg, the ETF asset class with the biggest inflows was precious metals.

Weaknesses

- The worst performing metal this week was palladium, down 5.25 percent. Both gold and copper futures fell on Tuesday as the dollar rose shortly after Federal Reserve Chairman Jerome Powell gave a statement indicating interest rates will continue to rise, according to Bloomberg. On Thursday, the U.S. dollar hit its highest level in seven weeks, on the heels of Powell’s testament to the strengths of the economy, while gold slipped to a three-week low.

- The platinum price fell below $1,000, and platinum group metals were hit as well after a German court ruled that the cities within the eurozone can ban diesel cars. Palladium also fell as the steel and aluminum tariffs might slow down auto demand as Canada will be hit the hardest by the new proposal and they are vital supply link in the automobile supply chain.

- Due to a boom in metals to fill battery demand, huge gold producers are struggling to compete for investments. At the BMO Metals & Mining Conference this past week, many executives echoed this sentiment as cobalt companies were flooded with interest. David Harquail, CEO of Franco-Nevada and chairman of the World Gold Council, said in an interview at the conference that “right now, gold has been so boring and asleep that nobody cares.”

Opportunities

- Newcrest Mining, Australia’s largest gold producer announced that it will invest $250 million for a 27.1 percent stake in Lundin Gold to increase its presence in Ecuador, which is known for untapped metal deposits, writes Bloomberg Markets. During the BMO Global Metals & Mining Conference this week in Florida, Ron Hochstein, CEO of Lundin Gold, told Kitco News that although gold mining is not in an exciting space right now, “We’ll get there.”

- Interest in North American-based gold equities has hit its lowest point since 2015, when the gold price came close to hitting $1,000 per ounce. Scotia Mining Sales believes this means that, despite bullion prices holding very well through the first two months of the year, the generalist investor doesn’t care about gold equities. As a result, the market as a whole is underweight in gold equities.

- Iamgold reported positive findings from its drilling program near the Rosebel Gold Mine in Suriname, with results showing high-grade intersections. Craig MacDougall, senior vice president for exploration at Iamgold, said that the project was upgraded to reserve status and that they are advancing toward production in 2019.

Threats

- The University of Texas Management Co. (Utimco), which manages the largest public university endowment in the U.S., will examine its $1 billion gold position in the portfolio, reports Bloomberg. The gold position is around 3 percent of the total portfolio, and Utimco CEO Britt Harris said, referring to the position, “We’re in no rush to sell, but it may not be a long-term strategic hold.”

- In his state-of-the-nation speech, Russian President Vladimir Putin warned that “efforts to contain Russia have failed,” as their latest nuclear weapon technology can supposedly overcome American defenses. His presentation included underwater drones, intercontinental missiles and a hypersonic system. Despite these reported developments, Putin stated that Russia is “not threatening anyone.”

- Saudi Arabia hopes to significantly grow its defense industry during the next decade, according to Bloomberg. This oil-rich country has a long history as a customer of arms sellers; however, Crown Prince Mohammed bin Salman wants to make these weapons in Saudi Arabia instead. Its goal is producing half of its weaponry at home by 2030, as opposed to 2 percent now. Should the U.S. and European governments be reluctant to assist, Saudi Arabia has other options through Russia, where it is already planning to purchase the S-400 air-defense system, according to Bloomberg.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 2 was MktCoin, which gained 405 percent.

- Circle Internet Financial, a financial services firm focused on cryptocurrency and backed by Goldman Sachs, announced this week that it acquired Poloniex Inc., a digital-token exchange. According to Bloomberg, the combined companies will compete with digital wallets and exchanges such as Coinbase.

- A collection of more than 1,100 islands in the Pacific, known as The Marshall Islands, is planning to launch a cryptocurrency to serve as its official legal tender, reports Seeking Alpha. This week members of parliament voted to proceed with the plan, indicating “long-term needs of the country,” where around 70,000 people live. The digital coin would be known as the Sovereign.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 2 was DIBCOIN, which lost 71.22 percent.

- Craig Wright, who is the self-proclaimed inventor of Bitcoin, is now being accused of swindling $5 billion worth of the digital currency, reports Bloomberg. Wright “allegedly schemed to use phony contracts and signatures to lay claim to bitcoins mined by colleague Dave Kleiman,” the article continues, who died in 2013. A lawsuit filed by Kleiman’s brother shows that the family contends they own rights to more than 1 billion bitcoins and blockchain technology that Kleiman mined.

- According to BlackRock, the world’s largest asset manager, cryptocurrencies should only be considered by investors who can stomach potentially complete losses, reports Seeking Alpha. Richard Turnhill, global chief investment strategist of BlackRock, commented that the group sees potential of wider adoption in the future, but says for now cryptocurrencies are too volatile for mainstream investment portfolios.

Opportunities

- Vancouver-based Lucara Diamond Corp. has joined the race to utilize blockchain technology in its business operations, reports Bloomberg. The company bought the operator of a digital platform selling rough diamonds, as well as blockchain technology “that seeks to track gems through the industry’s long and often opaque supply chain,” the article continues.

- To trim costs and cope with tighter profit margins, some of the biggest oil producers, traders and banks want to do away with the long-used “bill-of-landing” system, reports Bloomberg. Instead, these buyers are turning to blockchain technology methods. “The way we do our title transfers and post trade execution is very heavy on paperwork,” said Alistair Cross of Mercuria Energy Group. Using a shared online ledger would eliminate this.

- It’s no secret that blockchain technology is gaining popularity and “buzzword status,” reports Forbes, underpinning cryptocurrencies by allowing distributed ledger software to transfer information securely and quickly. For those looking to be part of this rapid change, one way to do so is find a job in the space, but what cities hold the most promise? According to Forbes’ “Top 15 Cities for Blockchain Technology Jobs in America,” New York, San Francisco and Boston come in as the top three places for blockchain employment.

Threats

- According to a report by Bloomberg, the use of Bitcoin (or any cryptocurrencies) is beginning to make many divorces end even worse. One of the reasons for this is the fact digital currencies make it much easier for a spouse to hide assets. In addition, the wild volatility in these coins makes it difficult to determine exact valuation of assets.

- Crypto-exchanges have been overwhelmed, reports Bitcoin News, as “record demand has caused throttling or restriction of service altogether.” While some have been forced to temporarily shut their books, others have moved to hiring staff by the hundreds. Bitstamp, for example, announced that it plans to recruit 100 new call center staff.

- JPMorgan has listed cryptocurrencies in warnings of possible risks to its business, reports Seeking Alpha. In its annual report the bank writes, “Both financial and their non-banking competitors face the risk that payment processing and other services could be disrupted by technologies, such as cryptocurrencies, that require no intermediation.”

Energy and Natural Resources Market

Strengths

- Steel was the best performing major commodity this week rising 2.71 percent. The commodity outperformed other major commodities as President Donald Trump suggested he is likely to introduce tariffs on imported steel, leading to a revaluation of domestic steel production, and possibly a weakening of the overall seaborne steel market.

- The best performing sector this week was the S&P1500 Steel Index. The index rose 1.3 percent on news that U.S. domestic steel producers may enjoy trade protection from the federal government as a result of the introduction of tariffs on imported steel, which allows domestic producers to raise their prices.

- The best performing stock for the week was Nine Dragons Paper Holdings Ltd. The Chinese manufacturer of containerboard products rose 10.41 percent after it announced plans to drastically increase its dividend policy as a result of its ability to increase prices on certain product lines.

Weaknesses

- Coal was the worst performing commodity this week. The commodity dropped 5.28 percent after China imposed new “special air pollutant restrictions” on major industries which are heavy coal users.

- The worst performing sector this week was the FTSE 350 Mining Index. The index dropped 6.37percent after disappointing Chinese PMI data suggests the pace of global industrial expansion may be stalling. In addition, the proposed U.S. steel import tariffs have led to declines in foreign iron ore and steel manufacturers, many of which are listed in London as part of this index.

- The worst performing stock for the week was Fresnillo PLC. The Mexican precious metals miner dropped 8.66 percent to a 52-week low as earnings were reported below the lowest estimates, with cost inflation being responsible for the earnings miss.

Opportunities

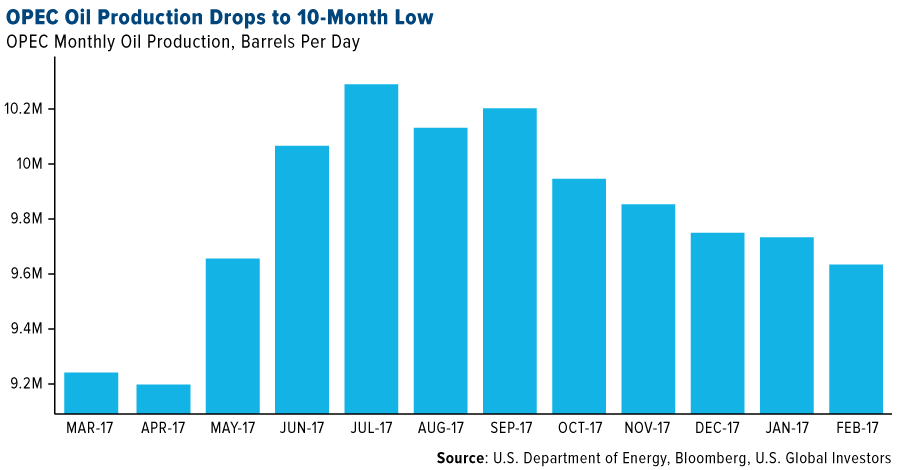

- OPEC oil production dropped to a 10-month low in February, mainly due to maintenance at a field in the United Arab Emirates and continued output declines in Venezuela, according to a Bloomberg report. Output from the 14 members of OPEC dropped 80,000 barrels per day last month to 32.28 million barrels per day.

- China’s Commerce Ministry removed anti-dumping duties on U.S. chicken imports, ending a multi-year long dispute between the world’s largest economies. The removal of these duties has been read by macroeconomic analysts as a willing sign and gesture of good will to maintain trade integrity, at a time when President Trump has threatened to introduce major steel and aluminum duties against China and others, a move that could trigger a protracted global trade war.

- The South African mining industry welcomed the appointment of Cyril Ramaphosa as President, and the appointment of a new minister for mineral resources, which the industry expects can bring a much needed boost to the struggling sector. The industry has long had constructive and respectful relationships with President Ramaphosa from his earlier post as General Secretary of the National Union of Mineworkers and his subsequent political and private industry positions.

Threats

- China’s factory-gate inflation is anticipated to slowdown after strong rallies in 2016 and 2017. The reading, which is linked to an increases in PMIs and industrial production, and a key factor in China’s reflationary trend, may indicate that the recovery in commodity demand could be about to stall.

- U.S. Senate action on infrastructure bill is unlikely to take place this year, according to Senator (R-TX) John Cornyn. One of the questions being asked by Republicans is how to play for the plan, which comes on the heels of passage of $1.5 trillion package of tax cuts, which together with extra federal spending may balloon federal deficits, thus making core Republican senators uncomfortable. Any such delays could be negative for commodity prices.

- Inflation is creeping into commodity producers’ income statements. After warnings from a slew of Australian metals and mining giants, which expect inflation pressures to pressure margins this year, now its turn for the oil and gas sector. This week, Carrizo Oil & Gas Inc., a sizeable U.S. shale producer, joined Pioneer Natural Resources Co. and Occidental Petroleum Corp. executives, in warning that oilfield service costs will raise by double digits this year as fracking crews and equipment are on high demand.

China Region

Strengths

- Thailand’s SET Index held up particularly well throughout an otherwise relatively rough week for global markets, rising 33 basis points over the last five trading days. Vietnam’s Ho Chi Minh Stock Index performed even better, jumping 1.68 percent in the same timeframe.

- Both imports and exports came in stronger than expected in Hong Kong for the January period. Imports rose 23.8 percent, beating estimates of an 18.9 percent rise, while exports were up 18.1 percent year-over-year, ahead of analysts’ estimates for a 16.1 percent pace.

- Utilities constituted the best-performing sector in the Hang Seng Composite for the week, rising 1.09 percent.

Weaknesses

- The Hang Seng Composite (HSCI) declined by 2.32 percent for the week, while South Korea’s KOSPI Index wasn’t far behind, falling by 2.01 percent.

- Manufacturing PMI in China came in significantly weaker than expected, falling to 50.3 from 51.3 in the prior period, and coming in well below of the collective 51.1 print expected by analysts.

- Hutchison Telecom (215 HK) tumbled 17.84 percent for the week in Hong Kong, the worst performer in the HSCI over that time. The company announced it did not expect to pay a special dividend at the present time.

Opportunities

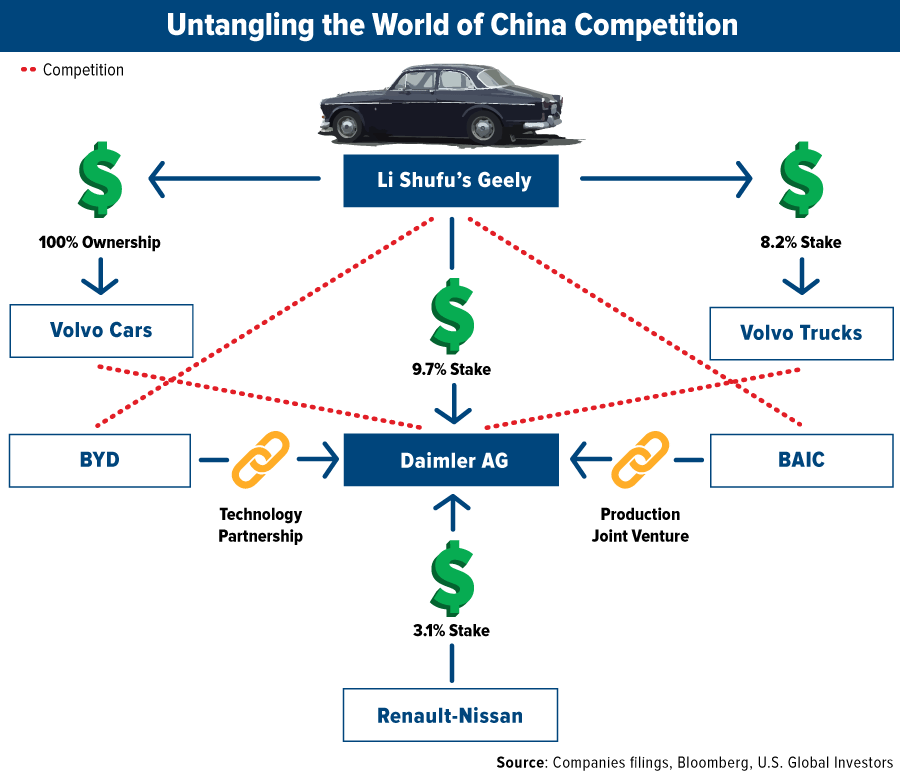

- At the tail end of last week it came out that Zhejiang Geely Holding Group—the parent company of HK-listed Geely Automobile (175 HK)—had quietly amassed a 9.7 percent stake in Daimler AG (DAI GY), the producer of Mercedes-Benz.

- Xi Jinping will likely remain president for life. At the upcoming National People’s Congress, term limit restrictions are expected to be scrapped formally, effectively granting Xi power for life, à la Mao. Suffice it to say there is great downside to this development. At the same time, however, for investors this has been reasonably well-telegraphed, and it means that certain stated items on Xi’s agenda, like environmental and economic reform, for example, should continue with the sort of stability expected in a one-man show that needs to retain credibility. With Xi’s power uncontested, i.e. with no foreseeable lame duck period, the political outlook remains “stable” in China, for better or for worse.

- U.S. Secretary of the Treasury Mnuchin announced this week that while the resurrection of the Trans-Pacific Partnership (TPP) is not a high priority at the moment, it remains officially in play and the administration could favor something under the right conditions and terms. Mnuchin explained that he had had high-level meetings with some counterparts on the matter. This was all, of course, out prior to the tariff announcements, so it remains to be seen what might come of TPP.

Threats

- Revelations this week from a new United Nations report demonstrate that North Korea “shipped 50 tons of supplies to Syria for use in building what is suspected to be an industrial-scale chemical weapons factory,” the Wall Street Journal reported this week. “The shipments,” the story continued, “are part of a steady stream of weapons-related sales by Pyongyang to Syria and to Mr. Assad’s patron, Iran, estimated to be valued at several billion dollars a year.”

- The Trump administration announced new U.S. import tariffs of 25 percent on steel and 10 percent on aluminum, applicable globally. President Trump also specifically mentioned “trade wars” by name and announced such trade wars could be “easy to win.” It might be as simple as that, but there remains, of course, the threat of repercussions or reciprocal tariffs and/or barriers to trade that might worry investors. Time will tell.

- Finally, and on a lighter note, we leave you with this important headline, featured in The New York Times this week: “Toilet Paper Panic Engulfs Taiwan.” Reports of imminent price increases have led to significantly higher demand…and a resultant shortage “[f]rom Taipei in the north to Tainan in the south.” Consider yourselves forewarned.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 1.4 percent. Erste Group Bank, Austria’s largest lender trading on the Prague exchange, was the best performing equity, gaining 6.4 percent. The bank announced its first revenue gain since 2010 and increased its dividend payout by 20 percent.

- The Czech koruna was the best performing currency this week, gaining 21 basis points against the U.S. dollar. Czech policy makers hiked rates three times in the past six months helping to strengthen the county’s currency. On Friday, preliminary annual economic growth was reported at 5.2 percent; the Czech Republic is one of the fastest growers in the region.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3.7 percent. Greece must implement 77 reform measures in the next three months to conclude the fourth review of its current bailout, and to successfully exit the bailout program in the summer.

- The Russian ruble was the worst performing currency this week, losing 1.25 percent. The ruble is highly correlated with the price on Brent crude oil, which declined almost 5 percent in the past five days. Trump’s administration is proposing tariffs on imported steel and aluminum, which could have global implication and be the start of a trade war.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

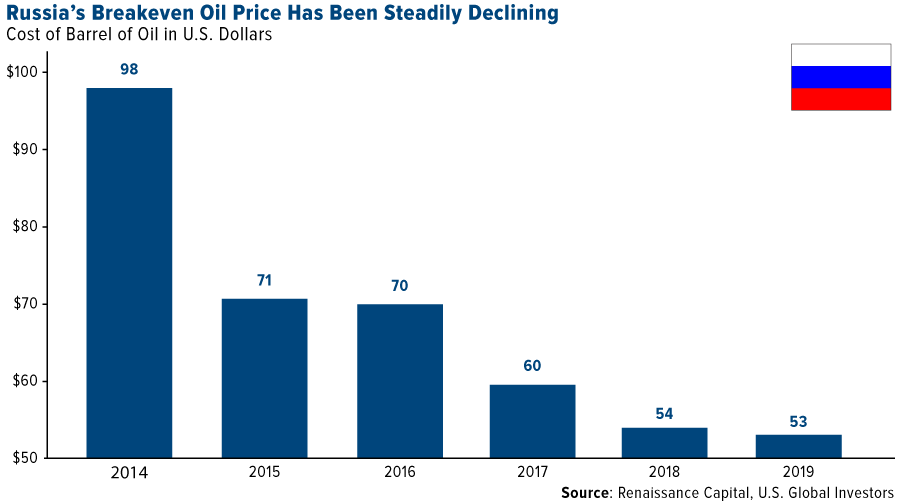

- In 2014, Russia needed the oil price to be $98 per barrel in order to balance its budget, but its 2018 oil breakeven cost dropped to $54 per barrel, according to Oleg Kouzmin’s research from Renaissance Capital. Russia’s fight against corruption and implemented tax reforms made it easier for the economy to be less dependent on oil exports. Russia recorded a budget deficit for the past few years, but went into profit in January, running a RUB 190 billion ($3.4 billion), or 2.8 percent GDP surplus. And, with many analysts predicting higher oil prices, Russia’s budget surplus should grow.

- Estimated inflation for the eurozone in February was reported at 1.2 percent versus a prior reading of 1.3 percent. Europe is experiencing good economic expansion without a pickup in inflation, but this could change soon. Euro-area average earnings per hour are accelerating, and it should put upward pressure on consumer prices.

- Vladimir Putin, in his state of the union speech, promised to turn his attention to restoring the prosperity Russia sacrificed over the past five years to finance the military modernization program. Two of the main topics of Putin’s speech were, 1) improving the quality of life for the average Russian, and 2) keeping up with technology development. He also promised to increase the size of the economy by 50 percent during his next term in office. That would require economic growth of around 7 percent per year. Russia is expected to grow at 2 percent this year. Presidential elections in Russia are scheduled for March 18.

Threats

- Two important events are scheduled in Europe for Sunday, March 4. Italy will hold parliamentary elections and the populist, euro-skeptic parties – the Five Star Movement and the far-right Eurosceptic Northern League, may gain ground. The latest poll shows the pro-EU ruling Democrats are likely to lose many seats along with its ability to govern the country on its own. The same day in Germany, members of Germany’s Social Democrats (SPD) will announce their decision on whether to enter a new coalition with Angela Merkel’s Christian Democrats (CDU).

- Final February PMI data for the eurozone was reported at 58.6, down from January’s 59.6, but slightly better than the flash estimate of 58.5. Germany’s PMI slid to 60.6 from 61.1. Poland, Russia, the Czech Republic and Hungary reported weaker PMI numbers, while Greek and Turkish PMIs were reported higher, with Greece’s PMI at a multi-year high of 56.1.

- S&P upgraded Russia’s sovereign debt to investment grade from junk, and now the cost of insurance against default has dropped to the lowest since 2008. Russia’s credit-default swaps are now cheaper than those of Mexico, which is rated two levels higher by S&P’s Global Rating Agency. However, the threat of further sanctions may keep investors on the sidelines. U.S. Treasury Secretary Steven Mnuchin said that the U.S. will announce additional sanctions on Russia in the next thirty days.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.71 | +0.08 | +3.20% |

| SS&P/TSX Venture Index | 826.06 | -0.03 | -0.00% |

| 10-Yr Treasury Bond | 2.87 | -0.00 | -0.03% |

| Gold Futures | 1,322.80 | -7.50 | -0.56% |

| S&P/TSX Global Gold Index | 181.43 | -1.16 | -0.64% |

| Russell 2000 | 1,533.17 | -16.01 | -1.03% |

| Nasdaq | 7,257.87 | -79.52 | -1.08% |

| Korean KOSPI Index | 2,402.16 | -49.36 | -2.01% |

| S&P 500 | 2,691.25 | -56.05 | -2.04% |

| XAU | 78.75 | -1.78 | -2.21% |

| Hang Seng Composite Index | 4,234.48 | -100.77 | -2.32% |

| S&P Energy | 491.86 | -13.73 | -2.72% |

| DJIA | 24,538.06 | -771.93 | -3.05% |

| Oil Futures | 61.41 | -2.14 | -3.37% |

| S&P Basic Materials | 368.11 | -15.47 | -4.03% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 2.87 | +0.16 | +5.95% |

| Gold Futures | 1,322.80 | -20.30 | -1.51% |

| Nasdaq | 7,257.87 | -153.62 | -2.07% |

| Russell 2000 | 1,533.17 | -41.81 | -2.65% |

| SS&P/TSX Venture Index | 826.06 | -38.29 | -4.43% |

| S&P 500 | 2,691.25 | -132.56 | -4.69% |

| Oil Futures | 61.41 | -3.32 | -5.13% |

| DJIA | 24,538.06 | -1,611.33 | -6.16% |

| Korean KOSPI Index | 2,402.16 | -164.30 | -6.40% |

| Hang Seng Composite Index | 4,234.48 | -300.00 | -6.62% |

| S&P Basic Materials | 368.11 | -26.39 | -6.69% |

| S&P/TSX Global Gold Index | 181.43 | -13.06 | -6.71% |

| Natural Gas Futures | 2.71 | -0.29 | -9.55% |

| XAU | 78.75 | -8.91 | -10.16% |

| S&P Energy | 491.86 | -61.59 | -11.13% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 2.87 | +0.51 | +21.38% |

| Nasdaq | 7,257.87 | +410.28 | +5.99% |

| Hang Seng Composite Index | 4,234.48 | +222.89 | +5.56% |

| Oil Futures | 61.41 | +3.05 | +5.23% |

| SS&P/TSX Venture Index | 826.06 | +37.06 | +4.70% |

| Gold Futures | 1,322.80 | +36.10 | +2.81% |

| S&P 500 | 2,691.25 | +49.03 | +1.86% |

| DJIA | 24,538.06 | +306.47 | +1.26% |

| Russell 2000 | 1,533.17 | -3.85 | -0.25% |

| S&P Basic Materials | 368.11 | -1.16 | -0.31% |

| XAU | 78.75 | -0.91 | -1.14% |

| Korean KOSPI Index | 2,402.16 | -73.25 | -2.96% |

| S&P Energy | 491.86 | -21.47 | -4.18% |

| S&P/TSX Global Gold Index | 181.43 | -9.88 | -5.16% |

| Natural Gas Futures | 2.71 | -0.35 | -11.50% |

Article by Frank Holmes