What is the best way to predict success?

Q4 2019 hedge fund letters, conferences and more

In baseball, the game’s strategy was forever changed when Oakland Athletics traded in the standard scout’s intuition for a data-driven approach. It was a switch that eventually led the team to an impressive 20-game winning streak, depicted in the movie Moneyball—it also kickstarted a broader revolution in sports analytics.

Similarly, successful data patterns are also being discovered by experts in the investing world. One such framework is factor investing, where securities are chosen based on attributes that are commonly associated with higher risk-adjusted returns.

Factor Investing 101

Today’s infographic comes to us from Stoxx, and it explains how factor investing works, as well as how to apply the strategy in a portfolio.

A Selective Approach

There are two main types of factors. Macroeconomic factors, such as inflation, drive market-wide returns. Style factors, such as a company’s size, drive returns within asset classes.

Analysts have numerous theories as to why these factors have historically outperformed over long timeframes:

- Rewarded risk

Investors can potentially earn a higher return for taking on more risk. - Behavioral bias

Investors can be prone to acting emotionally rather than rationally. - Investor constraints

Investors may face constraints such as the inability to use leverage.

Astute investors can capitalize on these biases by targeting the individual factors driving returns.

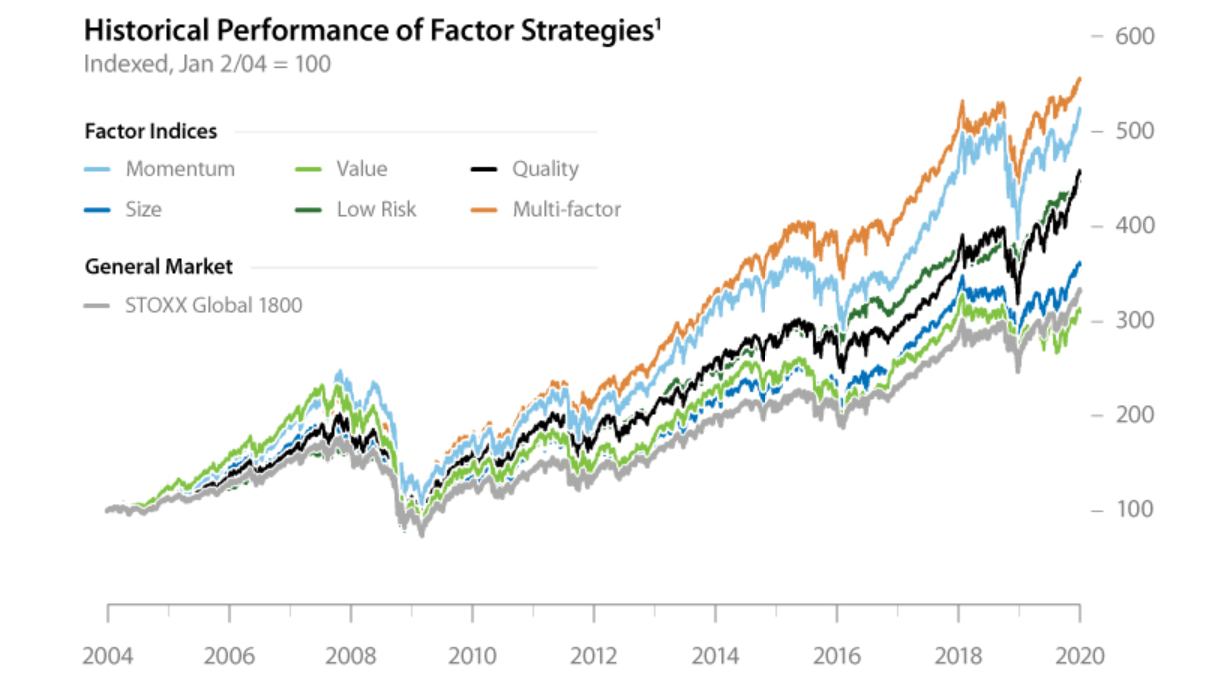

The Common Style Factors

Based on academic research and historical performance, there are five style factors that are widely accepted.

- Size: Smaller companies have historically experienced higher returns than larger companies

- Low Risk: Stocks with low volatility tend to earn higher risk-adjusted returns than stocks that have higher volatility.

- Momentum: Stocks that have generated strong returns in the past tend to continue outperforming.

- Quality: Quality is identified by minimal debt, consistent earnings, steady asset growth, and good corporate governance.

- Value: Stocks that have a low price compared to their fundamental value may generate higher returns.

It is becoming more straightforward for investors to implement these factors in a portfolio.

How Can You Apply Factor Investing?

All investors are exposed to factors whether they are aware of it or not. For example, an investor who puts capital in an ESG fund—targeting companies with good corporate governance—will have some level of quality exposure.

However, there are various approaches investors can take to implement factors intentionally.

Single Factors

Factors perform differently over the course of a market cycle. For example, low volatility stocks have historically performed well during market downturns such as the 2008 financial crisis or the 2015 sell-off.

Investors can consider macroeconomic information and their own market views, and adjust their exposure to individual factors accordingly.

Multi-factor

Factors tend to exhibit low or negative correlation with each other. For a long-term strategy, investors can combine multiple factors, which increases portfolio diversification and may provide more consistent returns.

Long-short

For each factor, there are investments that lie on either end of the spectrum. Experienced, risk-tolerant investors can employ a long-short strategy to play both sides:

- Hold long positions in attractive securities, such as those with upward momentum

- Hold short positions in unattractive securities, such as those with downward momentum

This diversifies potential return sources, and reduces aggregate market exposure.

Capturing Factors Through Indexing

Active managers have been selecting securities based on factors for decades. To capture factors with precision, managers must carefully consider numerous elements of portfolio construction, such as the starting investment universe and the relative weight of securities.

More recently, investors can access factor investing through another method: indexing. An indexing approach provides a framework for capturing these factors, which helps simplify the investment process. Based on objective rules, index solutions provide a higher level of transparency than some active solutions.

Not only that, their efficiency makes them more suitable as tools for building targeted outcomes.

The Future of Factors

In light of indexing’s various benefits, it’s perhaps not surprising that exchange-traded factor products have seen immense growth in the last decade.

In addition, there’s still plenty of room for factor ETF expansion in equities and other asset classes. Only about 1% of factor ETFs invest in fixed income, and 70% of surveyed institutional investors believe factor investing can be extended to the asset class.

As solutions continue to evolve, factor products could become the foundation of many investors’ portfolios.

Article by Visual Capitalist