Dear fellow investors,

Q1 hedge fund letters, conference, scoops etc

At the age of 35, I’m almost thirteen years into my career in the investment business. I was lucky to get a job right out of college in the brokerage business before joining Smead Capital Management at our formation. For most millennials like myself the last ten years have formed what we believe the business to be: a bull market reinvigorated by the whims of the Federal Reserve Board. If anchoring is a powerful force in investor behavior, the anchor at the depths of our millennial beliefs is that value hasn’t worked. We’d like to contextualize value stocks underperforming to frame whether this is a fundamental problem or if other factors outside of value are deluging the underperformance.

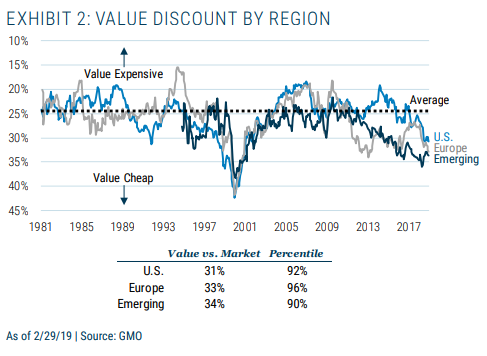

GMO’s Ben Friedman in a piece titled “Value Investing: Bruised by 1000 Cuts,” brought this conversation to a head by presenting the discount of value stocks to the average stocks in the chart to the right. As readers can see, based on their data we are in the 92nd percentile of value’s cheapness relative to the average stock in the U.S. It’s discount as of the end of February 2019 was 31% to the average stock. This compares to their historical average of 24%. In the piece, Friedman goes on to say:

We believe that value will continue to exhibit the same characteristics it has historically: lower growth, higher yield, and positive return from multiple expansion and rebalancing. After losing 1% per year over the last 12 years as value stocks cheapened relative to the market, they are currently trading at abnormally wide discounts that should provide helpful tailwinds going forward. The increasing cheapness of value will reach a limit at some point. Given value’s relative growth has not deteriorated, we do not see any fundamental reason value stocks deserve to trade cheaper than they normally have. Even if the relative cheapness of value does not revert but simply stops widening, value stocks should outperform thanks to its other drivers of return. From a cyclical perspective, value globally is priced to win.

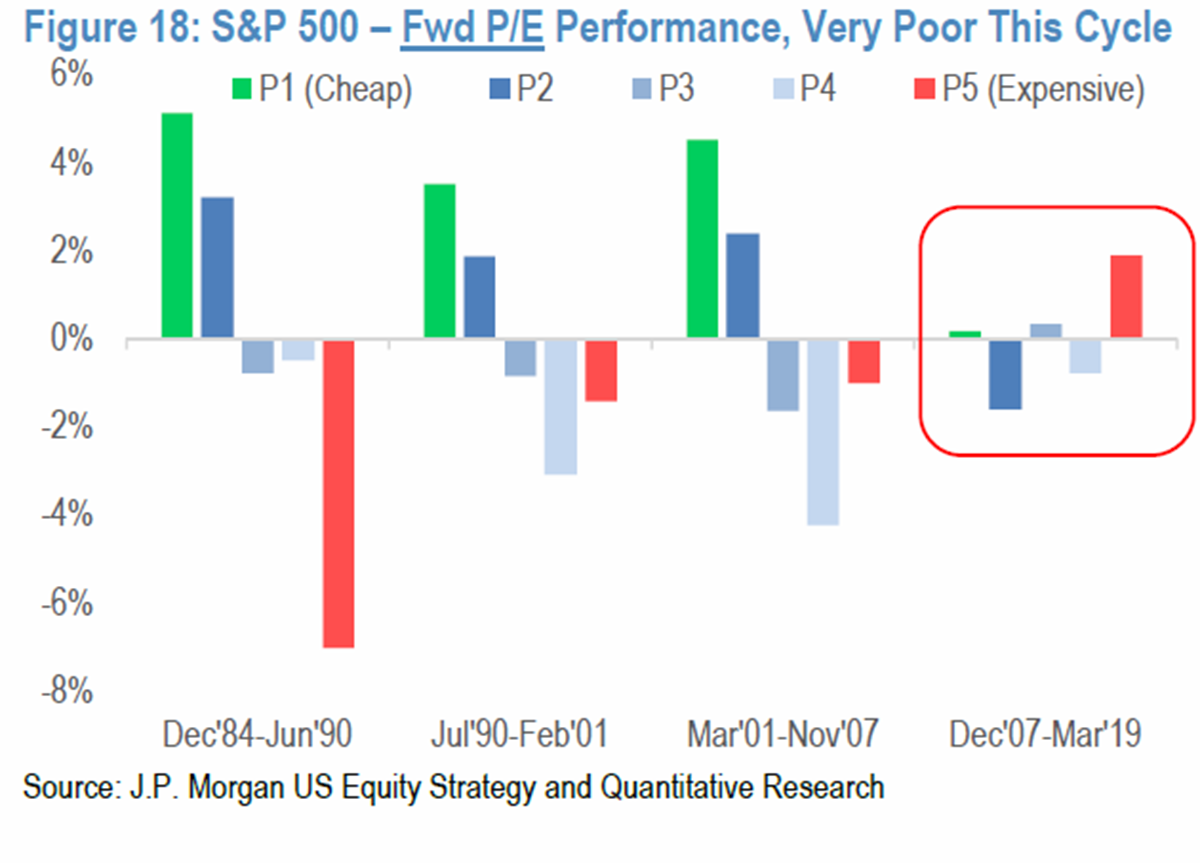

To follow on this, we came across a prescient piece by JPMorgan’s research team titled “The Value Conundrum.” Their note broke out examples of inverse relationships that value has exhibited in the last 12 years. To the right is a chart that shows how the relationship has been true using forward price-to-earnings (P/E) ratios.

This is the only cycle that has rewarded the forward P/E ratios of the most expensive stocks and provided little or no benefit to the cheapest.

While this seems extreme, the old adage is that the market can stay irrational longer that you can stay solvent. Is the market’s irrationality based on the value factor or are other factors muddying the water?

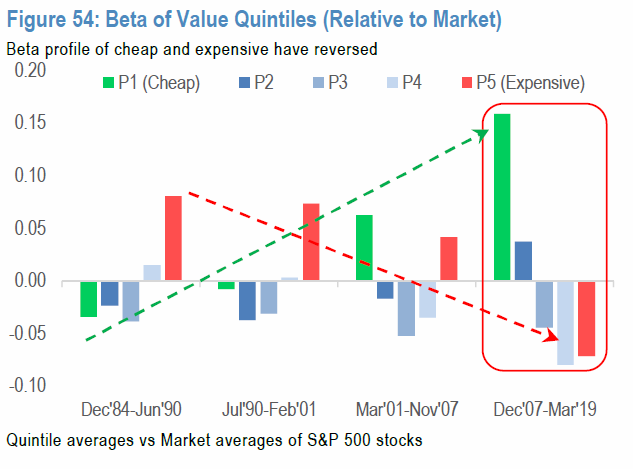

In our CIO Bill Smead’s piece “The Risk Pendulum,” we highlighted how the volatility of stocks is playing a major role in this. To the right is another illustration. The cheapest stocks have exhibited the highest beta, while the most expensive stocks have exhibited the lowest beta.

They say don’t confuse brains with a bull market. Based on this great work, we’d say don’t confuse near-term stock price movements as a forecast of the future. As Charlie Munger said at the 1995 Berkshire Hathaway Shareholder meeting, “People don’t seem to care what floor they’re at, just whether the elevator is going up or down.” Yes, value has underperformed the last 12 years. Yes, lower volatility stocks have done great the last 12 years. Yes, younger generations of investors are completely anchored by this.

In our opinion, there is not much that needs to go right over the next five years. If the discount of value stocks to the average stock in the market just holds its current levels, value should outperform. If volatility picks up for all stocks, that would be more painful for the lower volatility stocks. For value investors, the volatility would just be business as usual.

Warm regards,

Cole Smead, CFA

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Cole Smead, CFA, Managing Director and Portfolio Manager, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2019 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.