Vltava Fund letter to investors for the year ended December 31, 2017.

Dear Shareholders,

We stand at the close of another year, and, instead of presenting a more general topic in this letter to shareholders, now is a good time to look once again, after several years, at the historical performance of the Vltava Fund portfolio. Let us take it from the beginning.

[munger]

Prehistory

We established the Fund a long 14 years ago. Back then, we were young and ambitious, and this was reflected also in the investment strategy with which we started out. Our initial assumption was that we would be able to pick stocks the returns from which, over the long term, would substantially exceed those from the market as a whole, and we intended to build upon that. We were not satisfied with just this simple approach, however, but endeavoured to come up with a structure that would in its overall effect reduce our dependence on market returns and increase the impact of our individual stocks selection.

We came up with the idea that if we would combine with our long-positions portfolio a short position in the index for the entire market and then use the cash thereby obtained to double our long positions, then the influence of our stock picking on the Fund’s return would double and the dependence on equity market movements would be relatively reduced.

We knew that the success of this strategy would depend upon two conditions: First, that we truly could pick stocks which would beat the market, and second, that we would be able to hold our positions for as long as necessary. The first condition was never a problem, but the second one was.

Initially, all went well. In the first three years and four months, that is from September 2004 to the end of 2007, our return was 85% while the return of the global equity markets (MSCI World Index) was 44%. Then came 2008, however, and along with it extreme dislocations in the markets and chaotic behaviour of equity prices.

A sharp drop in equity markets in 2008 brought great losses to most investors. This in and of itself would not have been a reason to change the Fund’s investment strategy. Markets do drop sharply from time to time, and that is to be expected, and this is always just a transient phenomenon. The problem we were facing was record-setting price volatility and chaos on the markets.

In autumn of 2008, when the financial crisis was at its worst, regulators began increasingly to intervene in market operations. For example, they prohibited the shorting of certain stocks. This caused great chaos and closing of positions and, among other things, a steep rise in share prices even of companies which should have feared for their very survival (and some of which later did go bankrupt). Insufficient liquidity in the markets created a hunger for cash, and the source of needed liquidity became liquid stocks with no regard for their fundamentals. By contrast, other, less-liquid stocks took a hard hit. This was reflected in the VIX volatility index, for example, which spiked to an incredibly high 80 points. VIX values in the range of 15–20 are more usual.

We could continue to cite anomalies at great length. In short, the effect was that the long positions in our portfolio were sharply declining for some time even as the short positions were rising sharply. Such combination very quickly slashes the Fund’s assets and, most importantly, rapidly increases the financial leverage, which is expressed as a ratio of all positions relative to the Fund’s equity capital. One cannot just stand by and watch this impassively. Instead, the increasing risk must be managed in a certain way. In our case, this meant selling long positions and buying back short ones. As you can imagine, the prices were not advantageous for such operations and the feeling was as if we were cutting into our own living flesh.

Then what?

The second condition, the possibility of holding positions for an unlimited time, was therefore breached. At the end of 2008, we faced a decision what to do next concerning our investment strategy. It was clear to us that we would abandon the strategy which to a large extent involved combining long and short positions. At the same time, we knew this was not an error in the investment philosophy itself or in the selection of the individual stocks, but rather a conceptual error caused perhaps by an effort to make money for our shareholders too quickly.

We considered two options. One of them was to formally close down the Fund and open a new one. The second was to continue with the same fund, even with the knowledge that the investment strategy into which we switched in early 2009 would be so diametrically different from the previous one that the Fund’s historic performance would in fact consist of two separate periods and two wholly unrelated strategies.

In the end, we decided to continue with the Fund. We did not want by closing the old fund and opening a new one to create an impression as if the first years of the results were not attributable to us. The main reason, however, was a clear wish among all of our shareholders at that time for us to continue with the same fund. When we saw that all the shareholders at the time were remaining invested in the Fund, and that some of them even were increasing their investments, there was nothing more to equivocate over. Nevertheless, the Fund’s name and the valuable lessons learned are today the only things that join these entirely different stages and strategies to one another.

A new beginning

It was easy transitioning the Fund over to the new strategy. The selection of stocks for the portfolio did not change; we only abandoned the large combination of long and short positions. We therefore entered 2009 with an approach whereby complexity was replaced with simplicity. This may seem trivial, but it is an entirely different investment strategy. It is like the difference between tennis and table tennis. Both are played by hitting a ball over a net, both names include the word tennis, but they are two entirely different sports.

With the new investment strategy, it cannot occur that some situation in the market will compel changes in the portfolio. Our strategy is a long-term one, and therefore it still is founded on the possibility of holding the individual stocks for as long as necessary. Without financial leverage, this possibility is threatened by nothing. We therefore can focus fully on what creates the greatest added value for our shareholders, which means picking individual stocks.

This had never been a problem in and of itself. Even the year 2009 shows, for example, that our result for 2008 was really caused by the reasons described above, and not by poor stocks selection. In 2009, we achieved a return of 201% (the equity markets just 22%), while our equity portfolio in early 2009 was the same as that at the close of 2008. Changing the investment strategy was the right decision, and we will stick to our current strategy also into the future.

Results of the current investment strategy

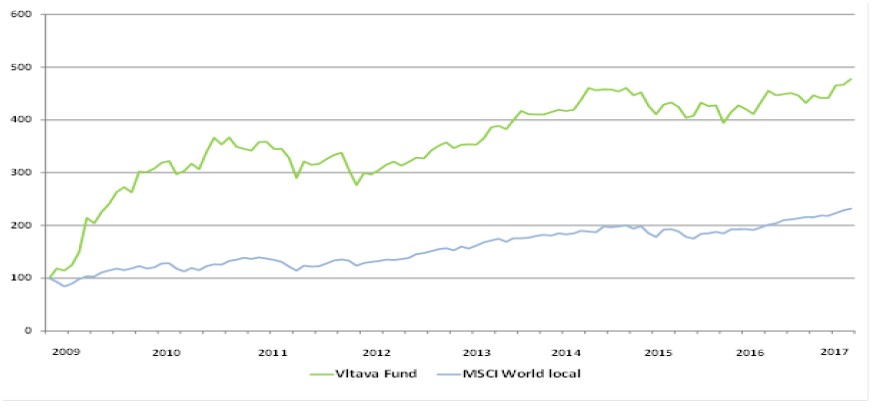

When we assess the results of our current investment strategy, we use the following graph.

This graph compares the development of the Fund’s NAV with the development of world equity markets as represented by the MSCI World Index for the entire period in which we were following the current investment strategy, that is for the nine years since the beginning of 2009. The graph’s point of origin is not selected at random. Rather, it is the point in time when we abandoned the original investment strategy and switched to our current one. This comparison is also relevant for contemplating future returns, because we do not intend to change anything about the current investment strategy, and our previous strategy does not relate in any way to the future. In considering comparisons with the market, our fund is a global one, and this is why a comparison with a global equities index such as MSCI World is necessary.

The graph indicates that the Fund’s NAV increased over the entire period by almost 5 times or, more precisely, by 397 %. World equity markets grew by 134 % for the same period. Although it is not our objective to beat any specific index, this nevertheless helps to paint a certain picture of our results. In any case, it is necessary to make the comparison for at least five years, as it has practically no informative value over a shorter period. This is due to two reasons: The first reason is that we set no short-term objectives. Our strategy is a long-term one, and we do not try to achieve certain results within short-term horizons of less than three years. The second reason is that our strategy is founded on a concentrated portfolio of selected, attractive investments. There are 22 such investments today, and the 10 largest ones account for approximately 65% of the portfolio. In shorter periods, portfolio returns must always diverge from those of the equities markets as a whole, and in both directions.

Over those long nine years, we bought shares in 71 different titles. The portfolio’s turnover was higher during 2009–2011 because it was necessary to respond quickly to rapidly changing equity prices. In the following years, the turnover gradually came down. Out of the 71 stocks acquired, we have already sold 49 and are currently holding 22. Of the 49 stocks sold, we realised gains from 44 stocks and lost money on 5 stocks. Of the 22 stocks we are still holding, we are in positive-returns territory in 20 cases and in negative returns in 2 cases. Our history to date thus shows that we are making money on approximately 9 stocks out of every 10 we buy. We presume this will be similar also in future.

Sometimes a person takes a misstep, but that is not something one can always avoid. The important thing, however, is that we did not lose much on those few stocks we closed out at a loss. Our longest-held stock is Total Produce, and the earnings we have from that are greater than the losses of the seven losing stocks put together. By the way, Total Produce was the first stock upon which we made a tenfold return. Of all stocks sold, we recorded the greatest loss in percentage terms on Bed Bath and Beyond (−30%) and the greatest profit on preferred shares of Fannie Mae (+376%). In certain of the stocks currently held, we have even higher gains.

Striving for constant improvement

The crux of our work today is in seeking out high-quality companies that are run by their managers in the best interests of shareholders, and especially in buying them at attractive prices. We are constantly striving to improve the definition of what we consider to be a high-quality company, and therefore we have gradually moved most of our investments to developed markets. The level of corporate governance – which refers to those mechanisms, processes, and relationships that are ongoing in managing a company – are very important for us. We are essentially very conservative investors and do not like to undertake unnecessary risks.

Our view as to what we regard as a high-quality company has also been developing over time. In the past, we considered it sufficient if we believed that a company has a certain sustainable competitive advantage. Today, we consider it more important whether a company is working to strengthen and enhance that advantage. We also put greater emphasis than before on company management and culture. Perhaps corporate culture is the most valuable competitive advantage, and yet it is very difficult to discern. It is no accident that more than half of our portfolio is comprised of companies managed by their founders or their direct descendants.

Our view of risk has developed similarly. The older we are, the more emphasis we put on the correct definition of risk and its management. This is not a completely straightforward matter. There exists no generally used definition of risk, risk is not measurable, and it is highly subjective. We occupy ourselves more and more in addressing this indispensable aspect of investing. Every human activity involves risk, and investing is of course no exception. We do not mind undertaking risks, but we want to have our own clear definition of risk, so that we can be compensated for it with sufficiently large returns.

Our work involves evaluating a set of approximately 2500 companies from all around the world. Among these, we progressively seek out those where we feel we understand what they do, those which have some sustainable competitive advantage, and those which are managed in the interests of shareholders. Only then do we attempt to estimate the value of each of these companies. Most of them are too expensive according to our measures most of the time. We therefore wait patiently for individual companies to reach advantageous prices. If and when this occurs, then we can consider including them into our portfolio.

Changes in the portfolio

We sold the shares of Proxima. It was our smallest position. The company has recently been gradually changing the focus of its activities in a manner that was not in accord with our thinking. Our profit was 6%.

On the other hand, two new positions have been added to the portfolio. One is in South Korea and the other in the UK.

South Korea is by no means an unknown country for us. We have had two investments there previously and were very satisfied with both. The Korean market has been among the least expensive for a long time. This is a price that South Korea pays for the frequently weaker level of corporate governance in Korean companies. In some cases, however, the situation is substantially better and the market frequently does not take that fully into account in the pricing of these stocks.

Our new position is in the technology sector. When several years ago we visited the managements of several companies in Korea whose stocks we were following, we could see at every turn that Korea is a country where the people literally live by technology and electronics. It is no accident that Korea ranks number-one in the world for the number of patent registrations per inhabitant. Several Korean technology companies are among the world’s best, and we now own one of them.

Our new British company is active in the financial services sector. Here we faced a dilemma: This is a relatively small company, also partially owned by the founder’s family. That means we will not manage to buy enough stock to form a typical 5% share in our portfolio. We do not want to have too many individual positions in our portfolio, so we pondered whether it makes sense to buy. In the end, we decided to start buying the shares, even with the knowledge that it will be a small position. This is because we historically have achieved the highest percentage earnings on smaller and medium-sized companies, and every crown counts.

The past nine years have been rather favourable for stocks. The markets have been rising at an above-average pace, and it is easier to make money in such an environment. We have no idea what the next nine years will bring. We estimate, however, that our earnings as well as the earnings of the global equity markets will be somewhat lower than those in the past nine years. Their returns, however, will very probably continue to exceed those of the other basic asset classes.

Today, our portfolio is valued at approximately 12 times the earnings achieved in the past year. Paying low prices for select stocks is the basis of our investment philosophy and the basis of our risk management. Price always has a large influence on the amount of investment risk, and the lower the price the lower the risk. We have therefore recently been avoiding popular, rapidly rising, but predominantly very expensive large US stocks. It is currently very difficult to find an attractive investment on the US market. This is why we have been buying on other markets in the past year – in Denmark, Canada, Japan, the UK, and Korea. These markets are much less expensive, their asset prices are not deformed by passive investing into indices, and one can invest well on such markets. A time when more and more investors are jumping onto a running train and buying index funds like crazy is a golden era for active investing. What could be better than a situation wherein more and more market participants are not concerning themselves at all with the pricing of individual stocks?

Our estimate of Vltava Fund’s fundamental value is 17% higher than the Fund’s current NAV, and for the next three years we expect it to grow by 10% per year. This would mean that at the end of 2020 the portfolio’s fundamental value could be about 50% higher than today’s NAV. Essentially three things influence the development of the portfolio’s fundamental value. First, our estimates as to the fundamental values of the individual companies. Second, the passage of time itself, because a company’s fundamental value develops over time and has a strong tendency to grow as more and more capital is earned and then reinvested. Third, our transactions through which we replace lower-potential companies with those having higher potential. The prices of individual stocks are something we cannot influence, but we can influence their selection, and that is what we fully focus upon. Long-term growth in the fundamental values of well-selected stocks will also pull up their prices. That is one of the few things that a person can rely upon.

On behalf of all of us, I wish you a peaceful and pleasant new year.

Daniel Gladis,

January 2018

See the full PDF below.