Our systematic stock selection process is far from just “value.” It wasn’t just value back when we started AQR in 1998 and given many other additions to our process since then, it’s even less “value” now. And yet from 2018-2020 for the bad and 2021-2022 for the good, our world has indeed been all about value. What gives?

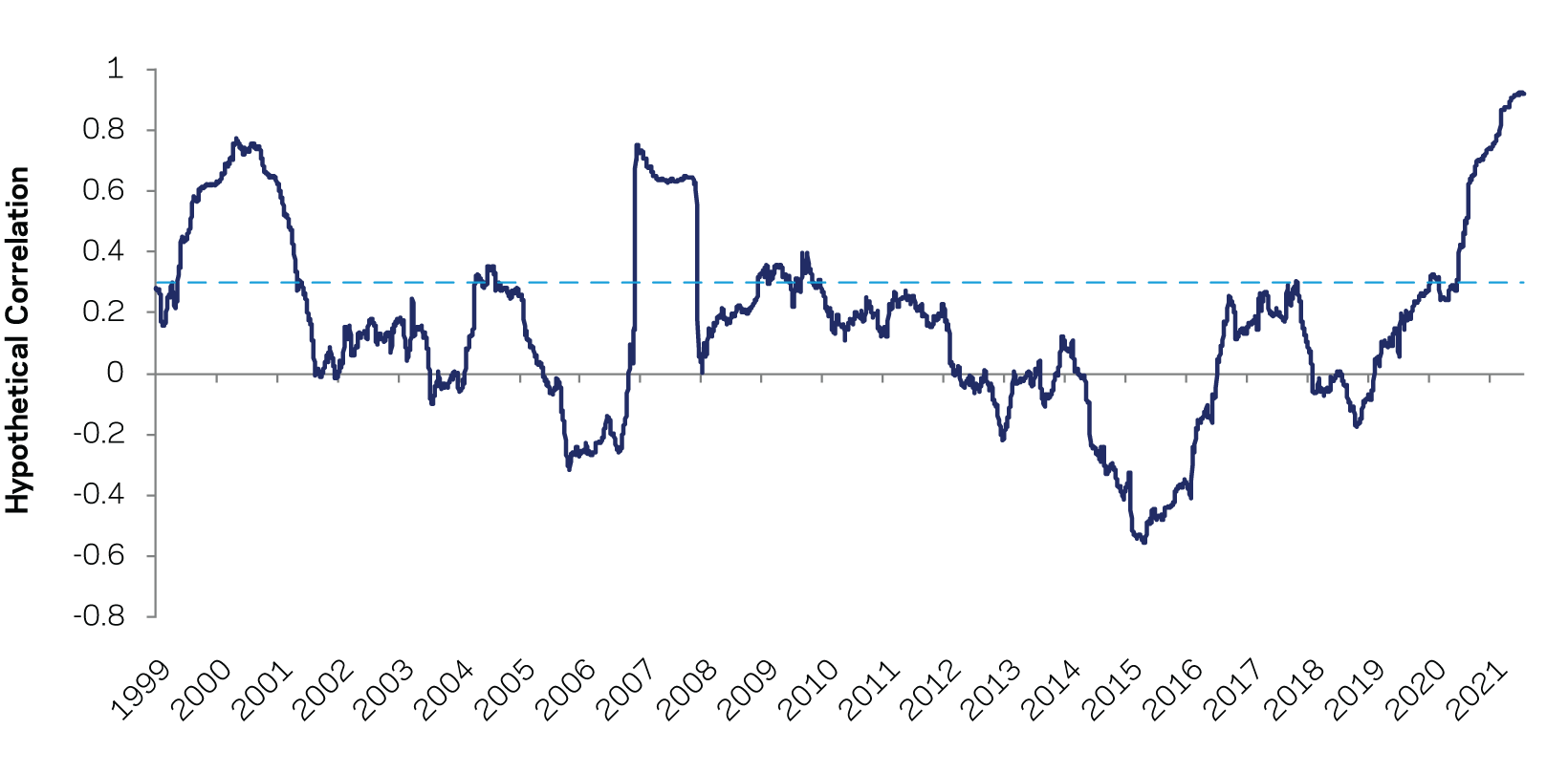

Below is the rolling correlation of a “carve out” of AQR’s Absolute Return Portfolio’s stock selection strategy (i.e., a proxy for our stock selection investment process) with a backtest of a simple global value strategy. Both are designed to be market neutral and largely industry neutral. The former goes long a diversified portfolio of global stocks favored by our process and short their disfavored counterparts. The latter does the same but using only a few value measures to decide the longs and shorts.

Q2 2022 hedge fund letters, conferences and more

Hypothetical Correlation of Absolute Return Portfolio’s Stock Selection and Value Backtest

August 31, 1998 – March 31, 2022

Source: AQR. Correlation is 12-month rolling, using 5 day overlapping returns. For illustrative purposes only and not representative of an actual portfolio AQR currently manages. This hypothetical data does not refle …

Source: AQR. Correlation is 12-month rolling, using 5 day overlapping returns. For illustrative purposes only and not representative of an actual portfolio AQR currently manages. This hypothetical data does not refle …Over the whole approximately 24 years the correlation of our full hypothetical strategy with pure value has been +0.30. Frankly, without being able to back it up specifically, this strikes me as pretty reasonable. Value is an important part of our process in steady state, but not a majority of it, and parts of the rest (notably momentum but also quality) are negatively correlated with value. So you would expect positive correlation but wouldn’t expect anything close to 1.0.

But over shorter periods (here I look at rolling years) the degree to which we look like value has varied a lot. We’ve peaked around or over 0.8 three times and troughed lower than -0.5 (yes, even with value being an important part of the process, if most of the rest of the process disagrees with it, we can come in negative).

The current 0.9 reflects a few things:

- Our extra tilt to value right now

- Value not disagreeing with the other factors, but on net trading very correlated to them compared to history (said another way, it seems the bubble fans don’t just like expensive names—they like expensive, high-beta, low-quality names)

- Value as a standalone factor trading more volatile lately than the others (though all are elevated versus long-term norms)

This currently high correlation is conscious and we believe reflects the incredible 1-3 year tactical opportunity. But, when (and I do mean when) this period is over, I expect to return to our more sedate 0.3ish correlation to value for a long, long time.

With that said, looking at the extremes is instructive.

Quant Flash Crash

First let’s look at the short spike in early August 2007. That month saw what amounted to a quant “flash crash.” Pretty much any factor used by quantitative investors suffered very large losses over a few days and then pretty much made it all back over the next few weeks. You get a very high correlation to value over rolling periods that include that period, as value was no different from the other factors. This will be a theme. We are more correlated to value when the other factors in our process (e.g., momentum, low versus high beta, quality, quite a few others) are more correlated to value. August 2007 is interesting for a lot of reasons, but not so much for the point of this piece. Moving on to the next extreme…

Long Periods of Low to Negative Correlation with Value

Next let’s look at the biggest negatives. From around 2012 to somewhere around 2015-2016, the rolling correlation was almost always negative, hitting a nadir of almost -0.6 in early 2015. This is kind of interesting. We’ve noted many times that from the Global Financial Crisis (GFC) to about late 2020, value’s performance was somewhere between subpar and terrible. That’s a long time! Yet from the GFC through 2017, despite value’s troubles, our process performed well. This is because the other factors we trade were both negatively correlated with value (often making the whole process negatively correlated with value) and these non-value parts delivered strong positive returns.

I think I have a useful way to describe value’s tough 2009-2017 and I think it’s consistent with us doing well over this same period. In a nutshell: many forms of value “deserved to lose.” By “deserved” I mean the expensive companies grew earnings (relative to the cheap) more than what was priced in. Now, we believe value “works” over the long-term precisely because this is the exception, not the rule (i.e., more often than not, the expensive companies deserve to be more expensive but by less than what the market is pricing in, and that’s how value on average wins).

Another way to say “deserved to lose” is “value lost for rational reasons.” In contrast—and staying with this oversimplified lexicon—“irrational reasons” are those based simply on large relative multiple expansion for expensive versus cheap without any fundamental victory behind it, and ending at unreasonable valuation differentials. A more mild way to put it than “irrational” might be “it wasn’t fundamentals at all, rather it was the ‘taste’ for expensive versus cheap stocks that changed.”

In 2010-2017 tastes didn’t change much (value spreads were relatively stable and normal). In fact, very late in that period (up to 2017) I was still taking the other side versus those value managers who said investors should buy or overweight value ASAP as it’s so beaten up. They were looking at realized returns, not the current state of valuations; and if realized returns are justified by improving relative fundamentals for the expensive stocks, then the valuation spread doesn’t get crazy. Despite losing (or our versions underperforming their norm) from 2010-2017, value just didn’t look especially cheap versus growth. Most of the time when you lose for a long while, you get cheaper (at least in reasonably slow turnover strategies like value). But not every time. Again, if you lose on the fundamentals coming in better for your shorts versus the longs (compared to what was priced in), you lost, but you ain’t necessarily cheaper going forward. That was the case, as I saw it, in 2017.

Now, again, one thing of more than a little interest to us was that despite value’s poor (or desultory for us) performance 2010-2017, it was, in general, a very strong period for our stock selection process. That’s essentially the point of this note. We ain’t all value, not by a long shot. In particular, when value loses for what I have been calling “rational reasons,” the rest of our process has historically done a pretty nice job of picking up for it. I think that’s intuitive. Much of the rest of our process (e.g., fundamental and maybe price momentum, quality, even low-risk investing, and other more proprietary measures) are uncorrelated or negatively correlated with value and collectively have great hope of picking up the “rational reasons” for value’s losses (i.e., they like the strong winning companies that value is eschewing at these times). Basically, we don’t fear a value loss, short or long term, if it’s fundamentally justified. It seems the rest of our process picks that up pretty well.

Irrational Value Crashes

This brings us to 2018-2020. I’ve been putting this one off for last as it’s painful! But here it goes. Over this period value was obliterated and the other factors didn’t help (or didn’t help nearly enough). What was different? Well, to continue my taxonomy from above, we believe this was an “irrational loss” for value. Unlike 2009-2017, the fundamentals didn’t come in worse than what was priced in for value versus growth (actually a bit the opposite), but the multiples that people were willing to pay for expensive versus cheap just exploded. It turns out, and we knew this from basic logic and the 1999-2000 experience, that when value loses for irrational reasons, we suffer. Pretty much only price momentum has great hope in such a period, and there’s a limit to how much of that anyone, even someone who wrote a dissertation showing momentum works thirty freaking years ago, is willing to have in a process. Not only do we suffer but we look a lot more like value during these periods (hence the very high correlations in the graph above during 1999-2000 and its aftermath and then 2018-today). That makes sense. Value is dying and the other factors are not fighting it because value is not dying for the rational reasons these factors try to pick up.

Basically I just said that’s there’s a type of market we know our process hates (irrational bubble losses for value— not rational losses for value). Now, if our process works over the long term, it’s not a tragedy if there’s one type of market it suffers in. In fact that’s probably pretty normal for any investment process. Few work in all possible environments and few to none that are available at institutional scale. Going further, both in 1999-2000 and 2018-2020 the suffering occurred in very bullish markets where people were generally pretty happy with their other investments, and then our process came back (well more than all the way in 2000-2002 and on the way, we hope, in 2021-2022) when our investors were suffering elsewhere. That’s not a terrible property to have long term (even if it makes the bubble periods, when everyone else is happy but thinks you’re an idiot, quite difficult)!

But it does beg the question, can we find something to add to the process that fixes this. The short answer is probably not. Finding something that goes up when AQR is suffering in an irrational value bubble (again, rational losses for value are OK!) isn’t hard. You can short value, or, if you’re feeling cheeky, you could find a way to short AQR. But I do not recommend either over the long term! An actual holy grail for us would be finding factors that do very well in an irrational loss for value and make money on average over the long term (the prior two examples nail the first part but get the second part tragically backwards). We will never stop looking, and we do think there are a few factors with some potential,28 but mostly we don’t think this holy grail exists. We think we have a great long-term process (shocking that we think that I know) that tends to suffer when the world is irrationally happy and then helps when it has its inevitable hangover. If we ever find a way to ameliorate the suffering without reducing the long-term performance, we’ll be very excited – but until then we’ll continue to work tirelessly on improvements that we think are more realistic and sustainable!

Summary

Whew, OK that was a lot. Basically, to sum up, value is an important part of our process but not usually a dominant part. When it has been dominant it has usually been in bubble periods of irrational losses for value (and in their more pleasant aftermaths). Furthermore, these losses have tended to be when most traditional portfolios were doing great and the large gains that followed when traditional portfolios were suffering. Over normal (non-bubble) periods, value can lose (or fail to deliver) for long stretches, and we can do quite well if it’s driven by fundamentals.

But, once every twenty years or so, when value loses for terrifically irrational reasons, we do strap on our armor and become value warriors (you see that in performance and in our rolling correlation to value). We think round trip that adds returns (it did in 1999-2000 when we made more in 2000-2002 than the prior losses, and it’s off to a good start for 2021-2022 but still has a way to go before I can say that again). We think in non-bubble times (i.e., most of the time!) we look like a process that’s pretty themeless with very nice return/risk/correlation characteristics. We think the combination of these two states of the world leads to a great addition to most portfolios. But we know it means there will be some years of great pain along the way. We’re still working on the holy grail that would deliver the long-term positives without having to suffer along the way, but I’m not holding my breath!