In Part I of this report, we reviewed the U.S. current account problem and examined how the persistent deficit affects the economy. We also discussed how the U.S. current account deficit is tied to American hegemony and ways the deficit could be addressed.

Q2 hedge fund letters, conference, scoops etc

This week, using the background established in Part I, we will introduce the Competitive Dollar for Jobs and Prosperity Act (CDJPA). Along with details of the proposed law, we will discuss the macroeconomics of the CDJPA and how it would affect the dollar’s reserve currency status. We will then examine the potential political effects of the bill, the likely retaliation from foreign nations and, as always, conclude with potential market ramifications.

The Competitive Dollar for Jobs and Prosperity Act

The Competitive Dollar for Jobs and Prosperity Act (CDJPA) is a bill introduced by Senators Hawley (R-MO) and Ballwin (D-WI). The bill is designed to address the problem of America’s persistent current account deficit. The bill contains these elements:

- The Federal Reserve is given an additional mandate to reduce the value of the dollar to a level consistent with a balanced current account over a five-year time frame.

- In addition to lowering interest rates to achieve its new mandate, the U.S. central bank will be given two additional tools:

a. The first tool is described as a “market access charge,” which is effectively a tariff on foreign investment. The Federal Reserve would be given discretion over its application of the level and duration of the fee. It would also have discretion on the types of foreign investment to be taxed.

b. The Federal Reserve will be granted the power to directly intervene in the foreign exchange markets to move the dollar to a desired level.

This bill is simplistic in construction but has the potential to be remarkably effective if implemented. The new mandate would probably tend to trump the current central bank mandates of full employment and low inflation. Why? Because the current account target is so explicit. The Fed’s current mandates are for stable prices and full employment, neither of which is necessarily subject to a hard number. The new mandate would be enshrined in legislation.

The other two tools in the CDJPA are quite interesting as well. Federal Reserve officials would have broad discretion in applying the market access charge, which is essentially a tax on foreign investment. The Fed could decide, for example, to levy a high tax on Treasuries but leave direct foreign investment untaxed. In other words, financial instruments that are held as foreign reserves would likely face a higher tax than

other instruments.

The second tool gives real teeth to the bill. The Treasury has limited liquidity to buy foreign currency to depress the dollar. The Fed has literally an unlimited ability to weaken the dollar by purchasing foreign assets; simply put, the Fed could expand its balance sheet to infinite levels to weaken the dollar.

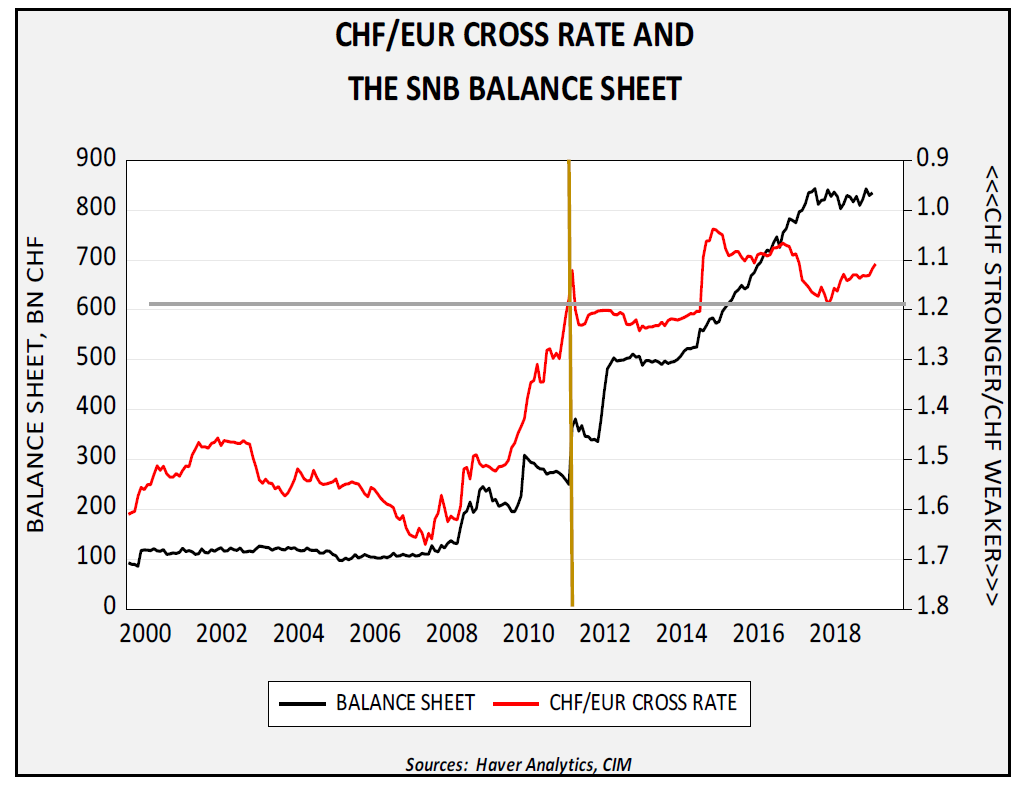

An example of how this process would work is shown through the Swiss National Bank’s (SNB) management of its exchange rate policy.

On this chart, we have overlaid the CHF/EUR exchange rate and the SNB balance sheet. The exchange rate’s scale is inverted. During the Eurozone crisis in 2010, European investors began to flock to Swiss assets due to uncertainty surrounding the Eurozone. This caused the CHF to appreciate; in response, in 2011, the SNB announced it was putting a ceiling on the currency at CHF 1.20 per EUR. Essentially, the SNB indicated it would expand its balance sheet to whatever level necessary to prevent its currency from appreciating beyond the aforementioned level. It maintained this peg for three years, and then unexpectedly ended the peg due to worries about inflation. This ending of the peg led to a sharp appreciation of the CHF. As the chart indicates, scrapping the peg did not end the balance sheet expansion; in fact, the SNB had to expand its balance sheet to contain the appreciation.

The lesson from the SNB is that if a central bank is willing to expand its balance sheet without limit, it can set its exchange rate where it wants. Of course, this also means that a central bank charged with providing a fixed exchange rate will see its independence severely curtailed. In our example, it appears that maintaining the peg became the dominant policy of the SNB, overshadowing other policy goals. We would expect the same outcome if the Fed is forced to adopt the CDJPA mandate.

The Macroeconomics of the CDJPA

The CDJPA is designed to force a desired economic adjustment on the rest of the world, especially those nations that run large current account surpluses to accumulate large foreign reserves. To understand this outcome let’s again refer to the savings identity:

0 = (I-S) + (G-Tx) + (X-M)

Nations that run large current account surpluses (X>M) do so by lifting private and public saving. So, they may engage in policies that lift household and business saving above the level of desired investment or run fiscal surpluses. As long as the combination of private and public saving is greater than zero, a current account surplus will result.

Tariffs are designed to cause two outcomes. In the foreign nations that are subject to tariffs, export prices will increase, making them less competitive. If the exchange rate doesn’t depreciate or export prices are not reduced to offset the tariffs, inventories will rise. In macroeconomic accounting, this increase in inventories becomes a rise in unplanned investment. Therefore, in the savings identity, I rises and absorbs S.

However, tariffs also have an effect on the nation implementing them. If import prices rise, real consumption declines. The rise in import prices will reduce consumption and, assuming steady income, lead to higher saving. Again, assuming nothing else changes, overall saving will rise and the current account deficit will decline or the surplus will increase.

The CDJPA would work differently than tariffs. First, the bill would not raise import prices, but a current account surplus nation that accumulated dollars would get an effectively lower yield on their Treasuries by paying a higher price in the form of the market access charge. Instead of making imports less attractive, the market access charge would make buying Treasuries less attractive. For profit-seeking entities holding dollars, the market access charge would reduce the incentive to recycle those dollars into Treasuries and likely increase the use of other financial instruments or spur direct foreign investment.

On the other hand, governments are less profit-sensitive. Their behavior would be changed by the power given to the Fed to depreciate the dollar. Currency depreciation would have a similar impact on imports as tariffs. It would raise import prices, lifting the real cost of goods to U.S. consumers. That would reduce consumption and lift saving. For foreigners, the opposite would occur; the weaker dollar would reduce consumer prices and boost consumption, reducing saving and the current account.

So, again using the savings identity, let’s create a simple example, a nation we will call Xanadu:

0 = (10-15) + (10-15) + (20-10)

Xanadu is running a current account surplus of 10. The U.S. wants to force that surplus to zero. Weakening the dollar reduces import costs to Xanadu, likely raising consumption and reducing saving. The other major policy tool, the market access charge, would discourage the accumulation of foreign reserves. Discouraging those purchases should either lead to higher private or public consumption in Xanadu, which should further incentivize Xanadu to reduce its current account surplus. The goal of the CDJPA is to force macroeconomic adjustment on the rest of the world to consume more and save less.

Making the Adjustment

As noted above, the CDJPA is designed to force a significant macroeconomic adjustment on the rest of the world, to get the world to rely less on U.S. domestic demand to support their economic growth. The Trump administration is trying to force this adjustment through tariffs, but the goal is being frustrated by dollar strength. In response, the Trump administration has admonished the Fed for not cutting interest rates, in part to weaken the dollar.

The CDJPA appears better suited to force the change on foreign economies than the current tariff tactics being deployed by the Trump administration. It focuses on the capital account and not the current account, thus reducing the overall incentive to conduct policy to merely build foreign reserves. Additionally, by giving the Fed the mandate to address the current account through balance sheet expansion, the odds of successful currency depreciation are far higher.

The Reserve Status Issue

The geopolitical ramifications center on the impact the CDJPA would have on the dollar’s reserve status. One of the compelling reasons for maintaining the dollar/Treasury foreign reserve system is that it makes foreign nations dependent on the U.S. economy for their economic growth and stability. By forcing depreciation and creating the threat to make Treasuries less attractive for foreign reserve purposes, other nations would be forced to adjust their economies away from using American domestic demand to lift their economic growth. Although the goal of the bill is to reduce this dependence, it will also consequently reduce the influence that the U.S. has on foreign nations. Being dependent on U.S. consumption gives America leverage over other nations and this leverage can be used to change behavior in other areas. For example, the U.S. may be able to put a military base on foreign soil or force a country into an alliance by threatening that nation’s exports to the U.S. If the level of dependence on the U.S. consumer is reduced, so is the leverage. In addition, by making U.S. Treasuries less attractive as a reserve asset by levying a market access charge, the ability to use sanctions as a tool to force geopolitical compliance will likely be reduced.

It should be recognized that, at present, there is no substitute for the dollar as a reserve currency. The most likely alternatives, the EUR and CNY, have serious deficiencies. The former does not have a Eurobond that is backed by the full faith and credit of the member states of the Eurozone. As the crises in Greece, Spain, Portugal, Ireland and Cyprus showed, it would be a major problem if a reserve manager investing in euro-denominated bonds picked a bond for the “wrong” nation. China has a restricted capital account and thus regular access to Chinese government debt cannot be guaranteed.

Although the CDJPA would spur the creation of other potential reserve assets, such as a global cryptocurrency, in reality, finding a substitute for the dollar will be difficult. Under this bill, the U.S. could still operate as importer of last resort, but the incentive for other nations to use the U.S. for that role would be diminished by the expectations of a weaker dollar and the market access charge. Over time, the dollar might be replaced. But, even the CDJPA would not trigger an immediate shift.

The Political Issues

The CDJPA has numerous political issues that will tend to reduce the odds of its passage, at least in its current form. Here are the main ones:

- Setting the proper rate for the dollar will be difficult. In the SNB example, the bank only had to focus on one exchange rate. The Fed would need to focus on all the world’s rates, although, in practice, it would likely create a basket of the critical ones and peg those to some index exchange rate. Nations would likely lobby to be excluded from the basket, and the more currencies the Fed has to monitor, the more involved the process will become. In addition, the Fed would have to create some methodology to establish the proper exchange rate for each member of the basket, which will be difficult. It isn’t obvious that the current composition of the FOMC has the expertise to handle this new mandate.

- At some point, if an inflation issue develops, the Fed could face cognitive dissonance. It may want to raise policy rates to address increasing price levels but that may conflict with its exchange rate policy. In an ideal world, the Fed should coordinate the policies to achieve its inflation goal but forcing the dollar to appreciate could prove even more unpopular than raising interest rates.

- Currently, the Fed is not popular. This bill would give the Fed even more power which might be difficult to find support for in Congress.

- Trade policy will move from the executive branch to the Fed. Although the Fed will have a mandate to bring the current account into balance over a five-year period, the White House will become mostly a bystander in this process. We would not expect the executive branch to easily acquiesce any of its current powers without careful consideration.

- Applying the market access charge would give taxing authority to a body that isn’t in the Treasury. Although I don’t claim expertise in constitutional law, giving the Fed the ability to levy taxes is an issue that will need to be resolved.

- The Treasury has held the mandate on currency policy since the inception of the United States. Although the mandate can be changed by Congress, it is a major change in the allocation of responsibilities.

- This bill would effectively reduce the independence of the Federal Reserve. Although independence is not enshrined in the Constitution, central bank independence is considered important for inflation control. Nations where the central bank isn’t independent tend to have inflation problems.

At present, we doubt this bill gets passed in its current form and under this administration. President Trump is at odds with the Fed and would likely not want to give the FOMC more power, and he likes the flexibility to use the tariff threat in negotiations. The CDJPA would reduce the tariff threat to some degree. Passage might be more likely under a different administration, especially a left-wing populist White House, which would be open to a non-independent Fed. Another potential change in the bill would be for shared management of the exchange rate mechanism and the market access charge with the Treasury. That might make the bill more politically palatable to where the CDJPA could find its way into law.

Retaliation

No nation likes its economic policy dictated from abroad. Foreign nations resent the U.S. using the dollar’s reserve status to increase the effectiveness of sanctions. The famous quote from Nixon’s Treasury Secretary, John Connally, who told foreign nations after the dollar was delinked from gold, that the dollar “is our currency but your problem,” was unpopular. We would expect the CDJPA to lead foreign nations to offset dollar weakness through either equally aggressive counter-depreciation actions to prevent the depreciation of their own currencies, or the deployment of tariffs to prevent cheaper U.S. imports from undermining domestic producers. However, the abilities of foreign nations to effectively retaliate are limited until an alternative reserve currency is developed. As we discussed above, the likelihood of this outcome, at least in the near term, is low. Accordingly, we would expect the CDJPA to be unpopular abroad but, in the end, foreign nations will be forced to accept the policy change.

Ramifications

The market ramifications from this bill would be profound. It would be safe to assume that the dollar would weaken. This outcome would have several effects on markets:

- All else held equal, it would be inflationary. The weaker dollar would lift import prices and reduce foreign competition on domestic producers. Currently, inflation is low and the Fed is concerned about disinflation. However, that may not always be the case.

- We would expect a weaker dollar to boost commodity prices. Since most commodities are priced in dollars, a weaker dollar reduces the price of commodities to foreign buyers. All things held equal, falling prices should boost commodity demand.

- Gold and precious metals prices will likely benefit. Although some consider these to be commodities and covered in point #2, precious metals also have a store of value role. If concerns about the dollar’s stability increase, demand would rise for gold and precious metals for saving purposes. Foreign nations may opt for more gold in their reserves as a way to avoid the market access charge on Treasuries.

- U.S. interest rates will likely rise. The threat of inflation and the use of a weaker dollar as a policy tool will reduce the need for extraordinary policy actions, such as zero or negative nominal policy rates.

- The effect on equities will likely be mixed. Usually, a weaker dollar favors large caps and demonstratively supports international investing. However, some of these usual effects could be mitigated by the structural change in the dollar’s management. Still, a weaker dollar is a clear tailwind to foreign assets and will likely boost foreign stocks.

Article by Bill O’Grady of Confluence Investment Management