Wedgewood Partners commentary for the second quarter ended June 30, 2019, titled, “Punch Bowl.”

“Is not the Fed now operating on the dual mandate of arsonist – and fireman?” – Jim Grant. Grant’s Interest Rate Observer, June 2019

Review and Outlook

Our Composite (net-of-fees)i gained +4.30% during the second quarter of 2019. The benchmark Russell 1000 Growth Index gained +4.64%. The S&P 500 Index gained +4.30% during the quarter.

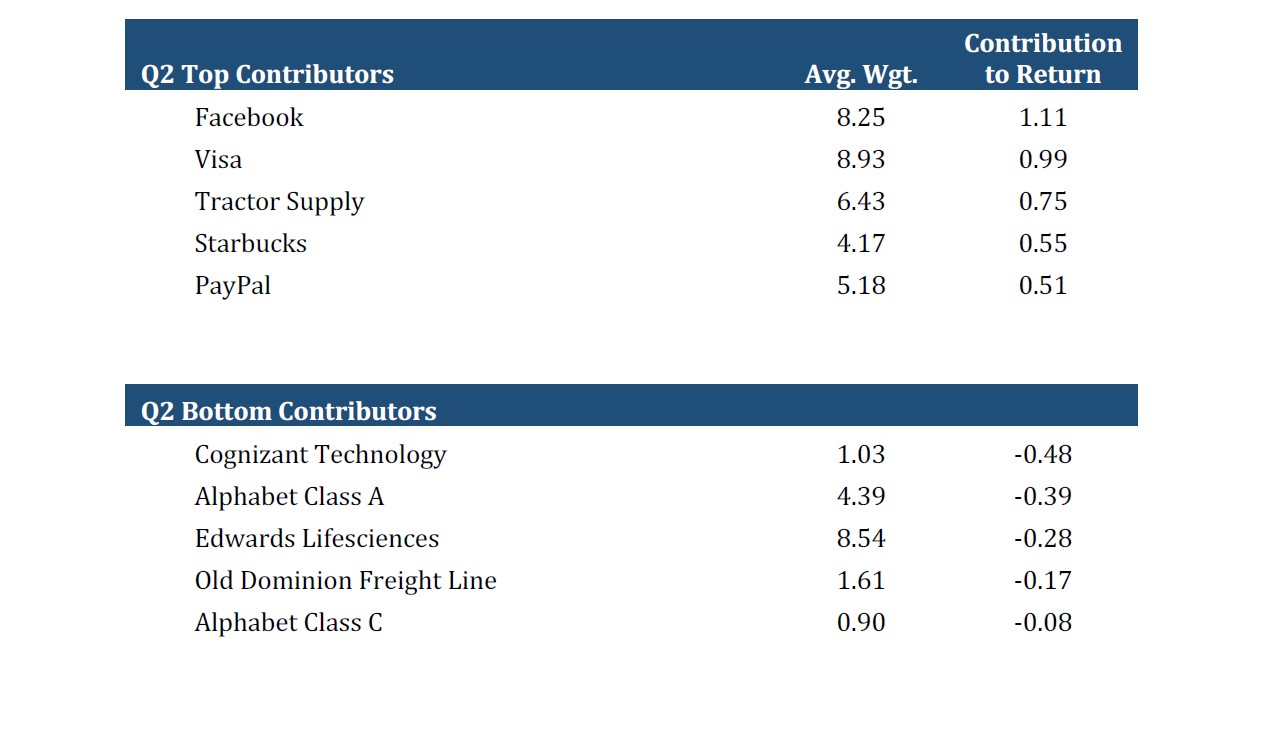

Top second quarter performance detractors include Cognizant Technology Solutions, Alphabet Class A, Edwards Lifesciences, Old Dominion Freight Line, and Alphabet Class C. Top second quarter performance contributors include Facebook, Visa, Tractor Supply Company, Starbucks, and PayPal.

We were unusually busy during the quarter. We sold Charles Schwab, Cognizant Technology Solutions, and Old Dominion Freight Lines and trimmed Berkshire Hathaway. New buys included Alcon, Electronic Arts, and Motorola Solutions. We increased our positions in both C.H. Robinson and Ross Stores.

As mentioned, we sold our position in both Cognizant Technology and Old Dominion in the quarter and trimmed Berkshire Hathaway. We discuss these at length below. Alphabet Class C appears in this list with a very small average weighted position in the quarter. Alphabet Class A underperformed in the quarter as management reported disappointing advertising revenue growth. Earlier this year, eMarketer estimated that Google’s and Facebook’s combined market share in digital advertising would decline (albeit only slightly) for the first time in 2019 – with Amazon being the winner of said share. With the company’s revenue growth missing expectations, investors took that as the proof point needed that competition was taking share. Google is holding tight to its advertising dominance however, and with paid click growth of +39% in the quarter, there is no concern about a lack of demand. As the company continues to report both high-teen organic revenue and profit growth rates, we continue to believe its shares remain an attractive use of our clients’ capital.

Edwards was also an underperformer in the quarter as TAVR (Transcatheter Aortic Valve Replacement) numbers came up slightly short in the quarter (please note, against a standout performance since late 2016). During the earnings call, management reiterated its expectation that growth will accelerate in the second half of the year, as well as reaffirmed its 2019 guidance. Despite the slight miss to first quarter estimates, we still expect strong growth for Edwards, mainly through the adoption of low-risk procedures which we believe the size of the overall addressable market continues to underestimate. In addition, during the quarter the Centers for Medicare & Medicaid Services (CMS) updated its national coverage determination pertaining to TAVR that offers greater flexibility for hospitals and providers. This update should result in the expansion of U.S. centers, further assisting in the growth potential for Edwards.

Facebook reported revenue growth of +26% in the previous quarter as well as steady growth in both daily and monthly active users. Management has also indicated that the growth of expenses will abate, and we saw evidence of this in the most recent quarter. Their advertising and user trends remain strong and the company continues to deliver successful ROI for its advertising customers offering an attractive growth and valuation profile.

Visa and PayPal continue to benefit from the shift away from cash, which to this day remains the dominant way people pay in many countries. Visa reported metrics that improved throughout the first quarter and continued into the start of the second quarter. PayPal announced a new $750 million global partnership with MercadoLibre, one of the largest online commerce and payments ecosystems in Latin America. Both Visa and PayPal currently trade at healthy, yet deserved, valuations on both an absolute and relative basis. However, as the secular shift to cashless and even digital payments continues, we expect both companies to continue to generate strong longer-term growth in volume, revenue, and earnings.

Tractor Supply continues to execute in its niche retail space despite the broad sector headwinds experienced during the quarter of weather and tariffs. We expect margins to improve throughout the year and valuation remains attractive as the company grows the bottom line at a double-digit pace.

Starbucks rounds out our top performers as the Company reported steady growth in its two largest markets – the U.S. and China – both of which are the focus of the Company’s current expansion plans. We continue to believe the Company can achieve double-digit growth through its planned store expansion, modest growth in its existing store base, margin improvement, and its capital return program.

Company Commentaries

Alcon

We initiated positions in Alcon, the largest ophthalmic surgical device company and second largest vision care company in the world. Alcon started trading in April after being spun out from pharmaceutical manufacturer Novartis, where Alcon spent close to a decade as a subsidiary.

We think Alcon has attractive prospects for sustainable double-digit earnings growth, driven by several near-term and long-term company-specific and secular trends. First, Alcon has a leading global share in advanced technology intraocular lens (ATIOL) but it has yet to launch a few key products in the U.S., which happens to be its largest market. ATIOL uptake tracks in-line with an aging demographic. These artificial lenses are used to replace clouded natural lenses (cataracts) and simultaneously alleviate other common eye problems such as astigmatism and the increasingly prevalent presbyopia. Over the past five years Alcon was slower to market in the U.S. due to nothing more than Novartis prioritizing pharmaceutical R&D ahead of Alcon’s ATIOL franchise. More recently, Alcon has no longer needed to prioritize R&D spending relative to pharmaceutical R&D and will be able to continue allocating toward its best ideas, including faster growing, higher margin ATIOL products, including next generation technologies (such as accommodative ATIOL) from organic and inorganic means. We estimate Alcon’s ATIOL business will be able to grow 15-20% per year over the next several years, more than offsetting its flat but steady, legacy monofocal lens franchise, and grow well in excess of the mid-single digit growth rate of the surgical eyecare market.

Second, Alcon controls around 50% of the installed base of ophthalmic surgical equipment, globally, which drives a steady consumables business that grows in-line with procedure volumes for cataracts, vitreoretinal diseases, and refractive errors. We expect cataract and refractive error surgery volumes to grow in the low-to-mid single digits and vitreoretinal disease surgeries to grow faster, as diagnosis and treatment opportunities expand in-line with the highly correlated growth in diabetes. We also expect Alcon to launch a new equipment platform in the next two to three years, that should drive incremental consumable growth.

In addition, Alcon has the second largest market share in optical health care, including contact lenses, contact lens care, and over-the-counter treatments for dry eye. Over the past year Alcon has embarked on an expansion program to build out its daily contact lens manufacturing capacity and enter into previously untapped segments, particularly in the mid-priced tier. We expect this capacity to come on-line later this year and into 2020, which should drive an acceleration in daily contact lens revenue growth. We estimate daily contact lenses generate two to three times more revenue per year than reusable contact lenses. We view the high up-front capital expenditures as significant barriers to entry, as even Novartis would routinely shelve capacity expansion despite being #2 in market share. This should allow for relatively unimpeded growth as plants take three to four years to get to optimal production rates. In addition, we think Alcon has recently developed novel manufacturing solutions that should reduce capex requirements by a third, and significantly reduce cost per lens and generate double-digit returns for this segment.

Finally, over the next several years we expect Alcon to be able to expand gross margins by several hundred basis points, both from manufacturing efficiencies as well as a mix shift to higher-margin ATIOL and surgical products. Further, as Alcon completes stand-alone overhead investments, along with revenue and gross margin dollars acceleration, we expect the Company to leverage its overhead and drive overall operating margin expansion in to the mid-20%’s, compared to the 17% margin reported in 2018. This margin expansion and revenue growth should yield an attractive mid-teen earnings per share growth rate over the next several years.

In summary, we think Alcon’s leading market position in ophthalmic surgery and optical health will be successfully leveraged into double-digit earnings per share growth, as the Company’s independence allows for more rational and aggressive capital allocation decisions over the next several years. We initiated a position during the quarter and would expect to add to that position as more attractive absolute valuation multiples present themselves.

Berkshire Hathaway

We trimmed our multidecade-long large weighting in Berkshire Hathaway to an average portfolio weighting based on our growing concern that Berkshire Hathaway has become too large, both in size ($525 billion in market cap) and in the size of the Company’s +$100 billion cash hoard. Simply put, the cash drag has become a stultifying impediment for the Company to achieve our hurdle rate of +10% growth. Now it must be said (admitted?) that we have long stated that Buffett’s fat-cash wallet is a high-class problem for any CEO. In the case of arguably one of the best capital allocators and investors extant in Buffett (and Munger too) the prospective strategic optionality of investing large sums of cash wherever Buffett finds opportunities to not only increase the ever-important diversity of the Company’s earnings streams (much to the delight of insurance regulators), but to also significantly increase the permanent earning power of said low-yielding cash has been acute during this bull market. That historic fact noted, the current and future prospects of Buffett & Co. deploying tens of billions in numerous gazelles, much less bagging that much vaunted elephant, both in terms of a truly attractive high return-on-asset business, plus at Buffett’s strict valuation criteria, have diminished significantly in the era of Quantitative Easing and of concomitant roaring bull markets.

Indeed, since Buffett Partnership time-immemorial Buffett and Munger have warned shareholders that size is the anchor of future performance. Relatedly, Buffett, given his wont, congenitally under promises, and given his delight has over delivered for decades. Except for the past decade – at least compared to earlier decades.

We would be less concerned (or more bullish) if Buffett reordered his preferred lineup of capital allocation targets. Buffett’s long-held preference is buying businesses outright first, followed by large, focused purchases of common stock and lastly, purchases of Berkshire Hathaway stock itself.

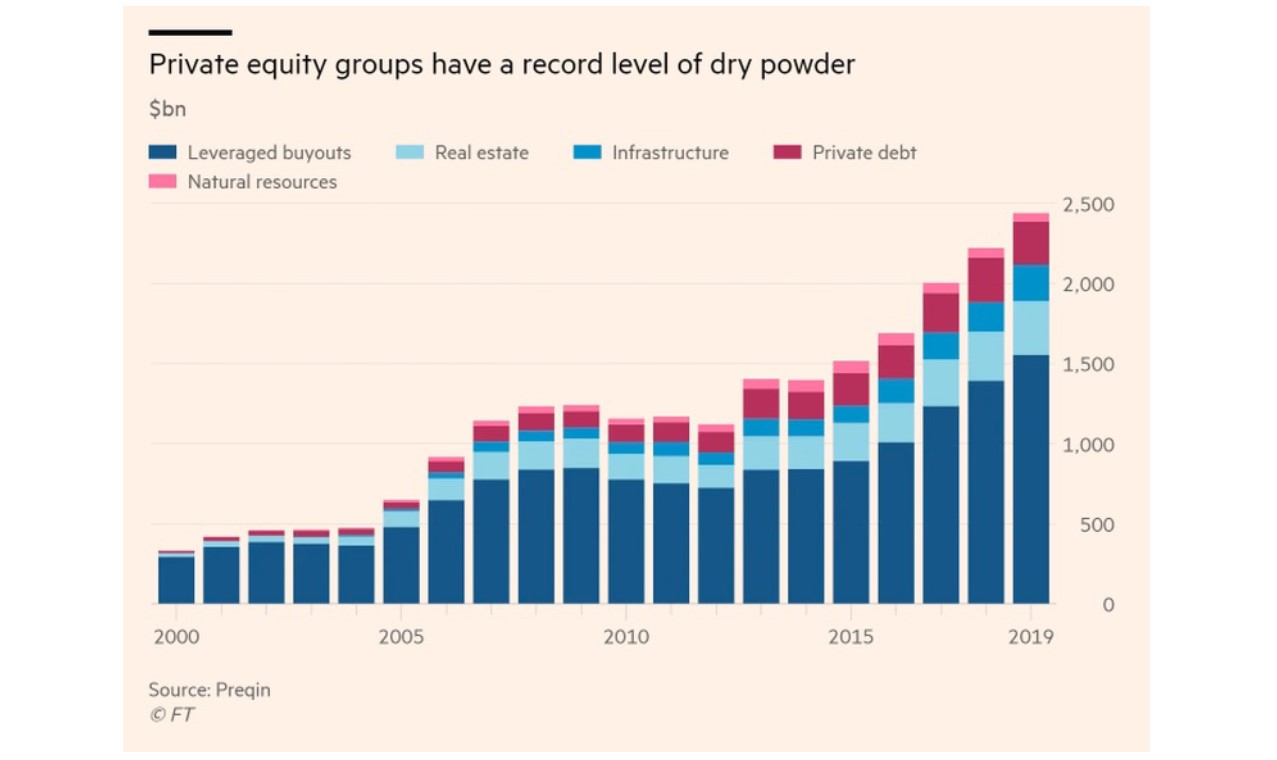

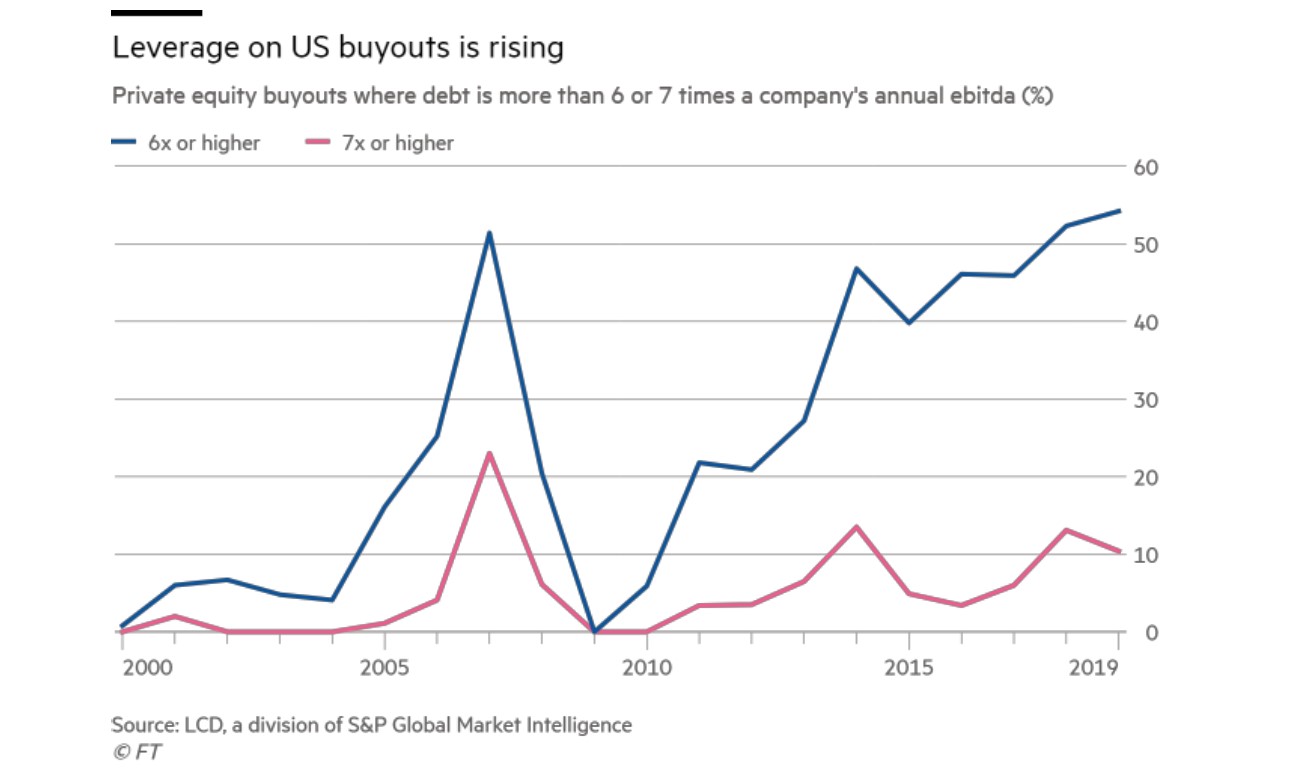

Take a look at the two graphics below. Buffett and Munger have long warned that they can’t compete in the bidding process of acquiring companies against private equity firms that have countless tens of billions at their disposal and who willingly will leverage such equity to pay top bidding-valuations in their respective hunt for acquisitions. In addition, Buffett & Co. refuse to compete in an acquisition if it involves an auction process, plus he refuses to go “hostile” in acquiring companies. Such conservatism, patience, and moral rectitude are no doubt admirable as Buffett & Co. wait for fat-pitch, multibillion-dollar opportunities to come knocking in Omaha. In addition, Buffett has little, if any, patience with investment bankers. Indeed, Buffett plays his singular game of acquisition by his invitation only. This game has turned into solitaire.

That said, for all intents and purposes, we have calibrated our expectation of successful gazelle and elephant hunting to literally zero in our near and longer-term operating earnings estimates for Berkshire. We hope our conservatism is wrong.

In addition, recent bagged gazelle in Lubrizol and elephant in Precision Castparts, which have thus far turned out to be turkeys. Precision stumbled right out of the gate after the acquisition in 2016 posting earnings declines, write-downs and impairment charges. Hopefully better results in 2018 portend to a long future of the rosy expectations at the time of the $37 billion acquisition.

Lubrizol too had high expectations after the $10 billion acquisition in 2011. Results early on were strong enough to impress Buffett so much that he “Sainted” Lubrizol, but the subsidiary has mostly struggled since. Operating earnings were flat in 2013, up a nice +10% in 2014, negative in both 2015 and 2016 and up slightly (+3%) in 2017. Pricing drove revenue growth of +6% in 2018, off of just +2% unit growth. Capital allocation at Lubrizol has been an admitted “big mistake” too. Lubrizol bought Weatherford’s oilfield chemical business in late 2014 for $750 million. The unit was disposed of shortly thereafter in late 2016, incurring a $365 million loss. Such results do not inspire one to assume too that “great multi-billion-dollar companies, at reasonable prices” are expected to be spotted in Omaha anytime soon.

Buffett has long taken great, and deserved, pride in his ability to make unconventional, fast decisions when the phone rings in Omaha when opportunities come calling. Buffett brags too that Berkshire’s checks will always clear. Fast multi-billion decisions are no doubt rare, but it must be stated, in the hunt for gazelles and elephants, private equity’s and most of large Corporate America’s checks are just as large and certainly clear just as swiftly as Berkshire’s. Unfortunately for shareholders, in a world flush with cash and where debt isn’t a four-letter pejorative, Buffett’s phone will likely continue to ring less than the Maytag repairman.

When we reflect on Buffett’s seminal acquisition of Burlington Northern Santa Fe back in late 2009, we have come to a new understanding that it may have been too good of an acquisition. At least “too good” for future elephantine acquisitions. To torture an analogy, we all know that elephants have prodigious memories. We suspect that prospective elephants on Buffett’s short hunting list, seared with decade-long bull market memories, may become ever more elusive targets.

Consider the fate of a BNSF shareholder on November 3, 2009: Buffett announced the acquisition of BNSF for $100 per share – a seemingly rich +30% premium to BNSF stock at the time. Tendering BNSF shareholders could elect to receive $100 in cash or a combination of cash and Berkshire stock. Let’s ask ourselves a hypothetical question about what might have been the fate for shareholders if BNSF had stayed independent. A very good proxy for BNSF is Union Pacific railroad. Both businesses have been of a similar size, growth, and profitability for more than a few years. Union Pacific has been a terrific operator, doubling its return on assets and net margin over the past decade. UNP stock – not surprisingly – has boomed over the great bull market. $10,000 invested in UNP stock on November 2, 2009 would have grown to just over $75,000 by June 30 this year. $10,000 in Berkshire Hathaway stock would have “only” grown to just over $32,000. If said BNSF shareholder would have heeded Buffett’s long-held advice and invested in a market index fund, $10,000 invested in the S&P 500 Index would have grown to almost $35,000. BNSF has turned out to be an elephant-home run for Berkshire shareholders. We’ll leave it to former BNSF shareholders to determine if Berkshire’s acquisition of BNSF was a home run for them, considering what they would prosectively leave on the table.

The point of the hypothetical is to illustrate two new realities that Berkshire shareholders need to consider; Berkshire Hathaway stock as a desired currency in an acquisition has lost its former considerable luster. Truth be told, this is not new news to Berkshire faithful shareholders. Plus, would any CEO/corporate board – public or private – circa-2019 agree to put their respective company up for sale in today’s cash flush environment without a bidding/auction process? In our opinion, we think not. If it’s a “bagged” gazelle or elephant – and earning the requisite Buffett-level returns on assets – we are doubtful that Buffett gets the sole call any longer. Even in a unique situation of a mastodon private Company such as Cargill or Mars whereby an all-stock acquisition (even at a “market discount”) by Buffett might be familial appealing for minimum capital gains tax, plus perhaps a heightened diversity desire (given Berkshire’s inherently diversified conglomerate), we would still be quite surprised that such a transaction could be pulled off absent an auction. We thank our lucky stars that Burlington Northern was willing to be sold (stolen?) in 2009. We don’t think BNSF could be bagged by Buffett circa-2019.

On the second preference of sizable common stock purchases, Buffett (and CIO’s Ted and Todd) have a tough task in size as well – a $200 billion common stock portfolio will see to that conundrum. We hope that in the next bear market, Buffett turns his two lieutenant portfolio managers loose to swing fat-sized bats. For that matter, Buffett too. Buffett’s “Buy American. I am.” slogan circa-2008 spawned numerous “bail-out” fixed income and fixed income/equity warrant spending sprees. (Mars-Wrigley, Goldman Sachs, Bank of America, General Electric, Harley-Davidson, Dow Chemical). Our hope is that during Buffett’s next “Buy American. I am. Redux.” spending spree is focused solely on great stocks, of great businesses, at great prices.

Lastly, on the matter of share buybacks, we, along with Berkshire shareholders who read and listen carefully to Buffett’s words on this matter, know full well Buffett’s share buyback philosophy, strategy, and intent. He has been more than transparent informing those shareholders-partners who may foolishly sell Berkshire shares back to Buffett himself. We have long wished that share buybacks would be a greater priority with Buffett. Alas, we now have carbureted our expectations of little meaningful share buybacks as long as Buffett is CEO (and alpha dog CIO). Share buybacks, executed at least at reasonable discounts to intrinsic value and in enough size, would be terrifically accretive to earnings per share growth. However, share buybacks are a reduction in capital. Again, in our view, the last thing Buffett wants to do is to reduce Berkshire’s capital base while he’s still in the captain’s chair.

Buffett and Munger have long lectured investors to stay within one’s “circle of competence.” Hindsight may not be fair (welcome to investing), but is it not fair to ask if the $50 billion acquiring these two companies would have served shareholders better if Buffett & Co. had stayed within their respective circle of competences and spent $50 billion buying back the stock of the company that Buffett knows better than anyone else?

We wish that Buffett would take to heart the share buyback wisdom that he has passed on to CIOs in the past – particularly to the last two CEOs of Apple. Steve Jobs listened intently to Buffett back in the day. But he never pulled the buyback trigger. Tim Cook on the other hand has turned out to be Professor Buffett’s A+ student.

Since 2012 Apple has returned an astonishing $364 billion in capital to Apple shareholders. $271 billion in share buybacks alone. All told, Apple’s share count has been shrunk by a none-to-small -27%. Given the net cash $135 billion on Apple’s balance, plus their ability to generate about $70 billion in operating cash flow per annum, multi-billion share buybacks should continue for years to come.

Share buybacks are new news for Berkshire’s $68 billion bank stock portfolio. In late June the Federal Reserve approved the stress test (CCAR) and the nation’s largest banks were approved to return billions in capital back to shareholders. Berkshire’s windfall is significant. In terms of Berkshire’s bank stock holdings Bank of America announced a $31 billion buyback over just the next 12 months. Over a similar time-frame Wells Fargo ($23 billion), U.S. Bancorp ($3 billion), J.P. Morgan (29 billion), Goldman Sachs ($7 billion) and Bank of New York ($4 billion).

To repeat our long-held view, the best elephant Buffett & Co. can bag is sitting in wide open fields at the Omaha Zoo – mastodon Berkshire Hathaway stock itself.

On the economic front, the U.S. Treasury slipping below 2.00% speaks to that not insignificant business cycle headwinds forming in Berkshire’s cyclical businesses. We expect the growth rates in Berkshire’s numerous cyclical businesses to continue to post decelerating earnings growth for the foreseeable future. Thus, another reason in our calculation to trim our holding.

All told, we are no doubt reluctant to sell any shares in Berkshire at valuations not much higher than at valuations where Buffett has been nibbling at buybacks himself. Our ongoing conviction in Berkshire Hathaway shares will closely mirror that of Buffett’s own conviction in Berkshire shares.

Charles Schwab

We sold our remaining position in Charles Schwab after reducing the position during the first quarter. Schwab remains an exceptionally well-run company that we think is coming to the tail-end of a couple of favorable multi-year trends. First, as the Company expanded profitability and compounded earnings over the past several years, Schwab’s balance sheet capacity expanded, which allowed it to transfer over $70 billion in off-balance sheet client assets into Schwab deposits. Those deposits provided the capital for Schwab to meaningfully expand their interest earning assets and revenues in a lower-risk manner. We think the Company still has opportunity here, longer-term, to grow their balance sheet, but more inline with the mid-single digit rate consistent with its asset-gathering growth. In addition, the multi-year tailwind of favorable monetary policy, relative to Schwab, has leveled out and is at risk of turning into a headwind. For example, 10-year U.S. treasury yields have retreated over 100 basis points in the last six months – after a multi-year march higher. Further, as we have chronicled in recent Letters, the Federal Reserve halted its Fed Funds rate hiking spree earlier this year. We are not sure what the Federal Reserve targets, despite what they say, as inflation isn’t much different today than any of the past 5-7 years along with mostly robust macroeconomic data – at least in early 2019. While neither the backup in 10-year yields, nor the pause by the Fed are unprecedented by any means, we are concerned that they represent future, and significant, headwinds to Schwab’s growth rates.

Bullishly, over the past several years, Schwab has diligently managed expense growth to be below revenue growth. We would expect the Company to be able to continue this practice despite slowing top-line growth, and supplement earnings per share growth with buybacks, given the stock is trading at undemanding, though potentially understated, multiples. However, and in conclusion, we recognize a couple of multi-year tailwinds to the Company’s growth rate have faded, so we sold our remaining position.

Cognizant Technology Solutions

As a long-time holding, we liked Cognizant’s positioning as an IT and BP outsourcing service provider, adding value by helping companies simultaneously manage legacy IT business while ramping up investment in constantly emerging digital technologies. However, over the past few years there has been increasing turnover in Cognizant’s longer-term managerial ranks, and while the company continued to function smoothly, the recent handoff to the Company’s new CEO turned out to be more disruptive than we expected. Despite recently assuring shareholders that its value proposition and positioning were strong enough to drive high single-digit revenue growth along with margin expansion – a good recipe for doubledigit earnings growth – the Company came up well short of these expectations and are now outlining, in our view, vague plans to take up investments in building out consulting capacity while refocusing its selling and go-to-market strategy.

We agree with the Company that there are plenty of addressable market opportunities for Cognizant to capture, but we now think there will be a period of higher investment and lower top-line growth as it repositions to better compete relative to more integrated outsourcing and consulting service providers. Despite performing quite well over the years, we had trimmed Cognizant down to one of our smallest positions and decided to liquidate the remaining position in favor of opportunity elsewhere.

Electronic Arts

We recently initiated a position in Electronic Arts. The Company is one of the largest sports publishers in the video game industry. We estimate the Company generates close to half of its $5 billion in revenues – and well over half of the Company’s profits – from sports-related franchises, such as FIFA and Madden. We view the Company’s sports franchises to be unique and durable over a multi-year time frame, as well as to generate above-corporate average profitability and returns, facilitating reinvestment into attractive new segments of the nearly $100 billion video game industry.

For example, in February 2019 the Company launched Apex Legends, a “battle royale” genre, free to play title that we estimate is already on pace to generate nearly 5% to 10% of the Company’s total fiscal 2020 bookings – and at a highly attractive +60% margin. Apex was developed in-house by EA’s Respawn subsidiary, which is also responsible for developing the blockbuster series, Titanfall. While Apex is often compared to Fortnite and Player Unknown’s Battle Grounds – both very successful, genre-defining gaming titles – we think the addressable market is substantial enough and growing quickly enough to support multiple offerings.

EA’s core gaming franchises include Madden and FIFA, with FIFA generating the substantial majority of the roughly $2.5 billion in sports-related revenue. The Company has been licensing from FIFA the rights to develop the FIFA video game for various gaming platforms, for over 25 years, often launching a new title once a year. There are more than 15,000 professional soccer players in over 100 countries, playing across hundreds of club leagues and divisions, represented by FIFA around the globe. This sprawling, largely exclusive global licensing estate that EA has amassed over the past few decades makes it especially difficult for competitors to create a coherent, and globally relevant competing soccer title.

Further, the addressable market for soccer-related video gaming is especially attractive due to the sport’s massive global fan base. For example, FIFA announced that the 2018 World Cup drew over 3.5 billion viewers for the month-long tournament and over 1 billion viewers for the World Cup final. More recently, FIFA estimated its Women’s World Cup France 2019 viewership total would eclipse 1 billion. EA is a significant, albeit indirect, beneficiary of the billions of dollars in marketing support, and effectively content, that clubs, players, leagues, and FIFA generates for the sport. Additionally, the Company is able to allocate a meaningfully higher amount of investment to R&D, rather than to sales and marketing, relative to larger publicly traded peers, as EA’s FIFA titles benefit from the indirect marketing support of the live sport.

Of course, EA’s addressable market is limited to the installed base of gaming devices, but this base continues to grow at a healthy clip. Meanwhile the proliferation of more powerful smartphones and cloud-based services has dramatically increased the addressable market. While EA’s mobile revenues have been stagnant, at best, over the past few years, it uses mobile as an incremental source of revenue for sunk, console-based R&D, rather than as a separate cost-center that requires revenue. Many of the industry’s most popular mobile gaming titles are entrenched, some having been around for a decade or more, so we applaud the Company’s current strategy of using mobile as a revenue supplement.

While the shift of video games away from physical retail-store based sales, toward digital and online distribution sales has been the norm for a few years, we expect there remains a good opportunity for EA to improve the profitability of existing titles and launch new titles into untapped segments, at higher returns than we have seen historically.

For example, EA will be launching its EA Access subscription service for PlayStation later this year after amassing millions of subscribers through Xbox. This subscription service has an attractive value proposition as it represents a low-cost way for gamers to access EA’s legacy titles, while enhancing returns for shareholders, as most of the EA Access title development costs are sunk. We expect digital sales to be a higher margin business relative to more traditional video games and to drive attractive margin expansion. In addition, we expect EA to be able to expand its sports franchise revenues at a mid-single digit growth rate over the next several years. This will be supplemented by the launch of new non-sports titles and sequels to existing titles, driving a high-single digit or low double-digit revenue growth rate. The Company also maintains a significant and likely unnecessary net cash balance of about $4.5 billion. With the stock trading at what we estimate to be an undemanding, mid-teen Enterprise Value to Free Cash Flow multiple, we think even modest repurchase activity should help drive double-digit earnings per share growth over the next several years.

Motorola Solutions

We have established a position in Motorola Solutions. First, we need to point out that this is not the old Motorola mobile handset business. The Company spun that business off into a separate company in 2011 and sold it in 2012. This potential confusion is an important point, as we believe this company has flown under many investors’ radars due to MSI’s former ties to the mobile phone business.

This new Motorola, known as Motorola Solutions, is the world’s leading provider of highly secure and reliable communication networks, products, and services for use in global police and emergency services, a variety of government and military applications, and other commercial and public safety applications where security and reliability are of the utmost importance. This business is known as Land Mobile Radio (LMR) and involves building the infrastructure for customized, secure networks for their customers, providing handsets and other devices, and layering in a variety of software and services.

The nature of their business and the nature of their customer base make this a very steady, somewhat non-cyclical business. For example, a municipal police force will not turn off its first-responder communications network in a recession, and it will need to maintain the network, at least. To be fair, though, such a customer might choose to delay upgrades or additions of ancillary services if the municipal budget is under some constraint.

Between the expansion of its installed base of network/handset customers, and its ability to sell new software/services/analytics into this installed base, we see Motorola as a consistent high single-digit percentage revenue grower, and at least low double-digit percentage profit grower over the next several years – all with relatively less economic sensitivity than most technology companies. We expect organic revenue growth to account for roughly 4-6% of the revenue growth, with regular acquisitions rounding out the rest of the expected growth.

Valuation is very attractive considering this steady growth profile, and we see an opportunity for valuation to expand. Additionally, we believe the stock has been under the radar of most investors, with many investors still thinking the Company is a broken mobile phone business. We believe investors’ knowledge of the company, estimates of the company’s earnings potential, and valuation multiples all have the opportunity to expand over the next few years.

Old Dominion Freight Line

We have decided to liquidate our holdings in Old Dominion Freight Lines in order to pursue opportunities elsewhere. We remain impressed with Old Dominion’s best-in-class business model and with the quality of its management team and operations, so we wouldn’t call this sale a vote against the Company. Results have been quite good while we have owned this company, although the market has lost interest in the broad transportation industry generally. Macroeconomic doubts, driven in large part by uncertain international trade dynamics, have weighed on sentiment. In addition, tremendously strong results from Old Dominion in 2018 – partially before we owned the company, and partially during our ownership – have created very difficult year-over-year comparisons. While, of course, this has been no surprise to us, we believe this also has weighed on sentiment to some degree.

As a reminder on 2018, the tremendous strength in Old Dominion’s business (which created difficult comparisons for 2019) was driven by a few issues above typical macroeconomic factors:

• Old Dominion, like other Less-than-Truckload (LTL) carriers, has significant industrial exposure, and changes to U.S. tax law at the beginning of 2018 drove incremental industrial strength and increased capital investment, both of which provided additional juice to Old Dominion’s already thriving industrial business.

• The extreme shortage of capacity in the Truckload (TL) industry, driven by Electronic Logging Device (ELD) mandate we’ve discussed extensively, actually caused some traditional Truckload business to slip into Less-than-Truckload, especially toward the end of 2017 and in the first half of 2018. This had been nearly unheard of in trucking previously. As the Truckload industry and its customers adjusted to the lower level of TL capacity over the course of several quarters, this particular anomaly has reverted to normal, with the overflow of capacity into LTL disappearing.

Unlike our holding C.H. Robinson, which has been and will remain a primary beneficiary of the shrinking capacity in the Truckload industry over the long term, the fundamental drivers of Old Dominion’s business model have been more purely cyclical in nature. As a result, we have chosen to retain our C.H. Robinson position while liquidating Old Dominion in favor of other recent buys and additions, such as Motorola Solutions and Ross Stores, both of which present growth opportunities which are less cyclical in nature.

Punch Bowl

In our previous Client Letter, we wrote the following:

The verdict is in. The mystery is over. The “Powell Put” has been launched. Mr. Market has celebrated. January was the best start of a calendar year since 1987. The Standard & Poor’s 500 Index’s gain of +13.7% was the best first quarter since 1998.

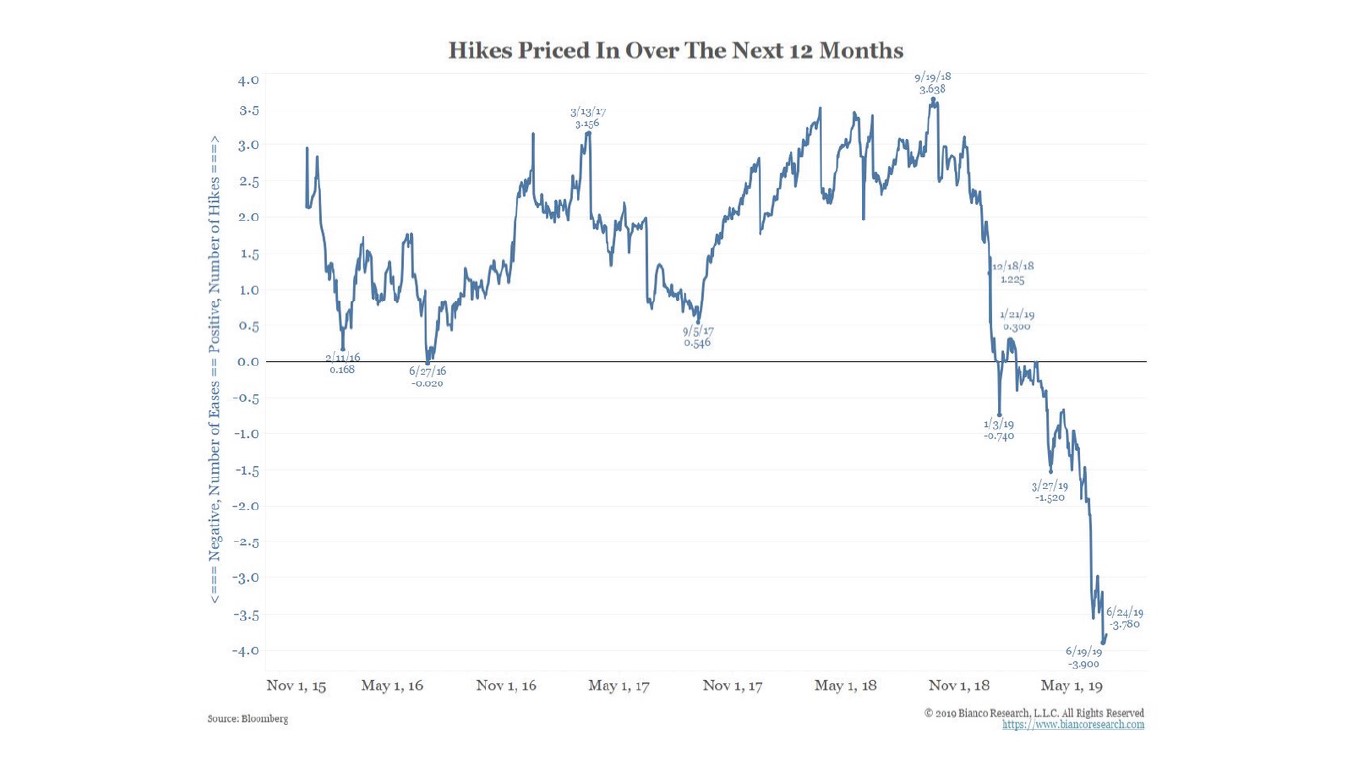

Recall the setup during last year’s fourth quarter; starting in October, Federal Reserve Chairman Jerome Powell remained an adamant hawk to reign in the Federal Reserve’s monetary punch bowl professing the need for three to four more interest rate hikes over the course of 2019. In addition, the reduction of $50 billion per month from the Fed’s balance sheet (QT – Quantitative Tightening) was set in stone as policy. The prior eight interest rate increases, with the usual lag effect, had begun to bite. The U.S. economy was slowing – GDP growth over the past four quarters has slowed from a “4” handle, to a 3, to a 2, to the current “1” handle. Earnings expectations have been falling since October, and stock prices began to fall in earnest that October as well.

Powell “blinked” in a speech at the end of November, noting that the U.S. economy was susceptible to the rapid slowdown in global growth. The stock market remained nonplussed and dropped sharply in December – the sharpest December drop since 1931. On that December 24, the Fed raised short rates by another 25 bps, the Fed’s ninth interest rate hike of this cycle of tightening. The stock market fell. Yet, the verbiage in the Fed’s comments noted the Committee’s future policy “…assessment will take into account a wide range of information, including readings on financial and international developments.” Mr. Market read that statement and the specific word “financial” as the initiation of the “Powell Put.” The stock market bottomed on the day, December 24.

As of this Letter, since then, the stock market (S&P 500 Index) has ripped +25% to a new alltime high – its best start to a year since 1997. Not to be out done, the Dow is at an all-time high, as are the NASDAQ 100 and U.S. Bonds. The U.S. economy is now at its longest expansion in history – coupled with the longest jobs gain (105) in straight months. Unemployment is the lowest since 1969. Yet all this wonderful news has largely been priced in financial assets based not on even stronger economic growth, nor stronger future corporate earnings, but rather on the paradoxical expectation (hope?) of worse economic news.

Concomitant expectations of monetary ease continue to soar. Indeed, the Administration, while still boastful about the growing (best-ever) economy is jaw-boning the Fed to cut rates by 50 basis points. Financial market expectations are currently focused on a 50-bps cut on July 31st. If Powell & Co. fail to satiate the market’s never-ending appetite for more cowbell punch, we may have another round of best-ever fireworks in July.

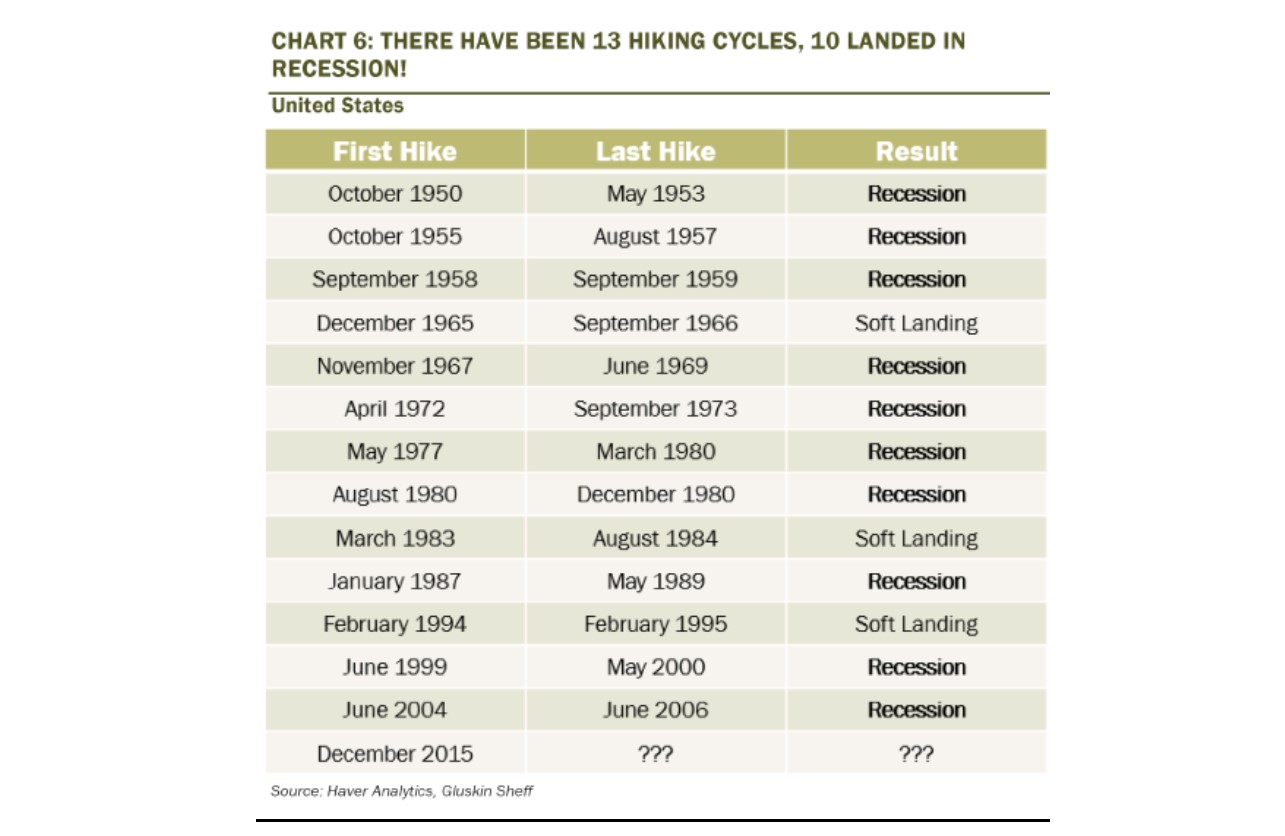

We say be careful what you wish for. In the past 40 years, the last time the Federal Reserve found the necessity to initiate a new round of monetary easing with a 50-basis point cut in the Federal Funds was in January 2001 and September 2007 – the beginnings of the last two recessions. Since 1950, the Fed has engineered just three soft landings. Note too, that during the last two recessions the Fed needed to cut rates 5.50% in 2000-2002 and 5.25% in 2007-2009. QE4 will most assuredly introduce negative rates in the U.S.

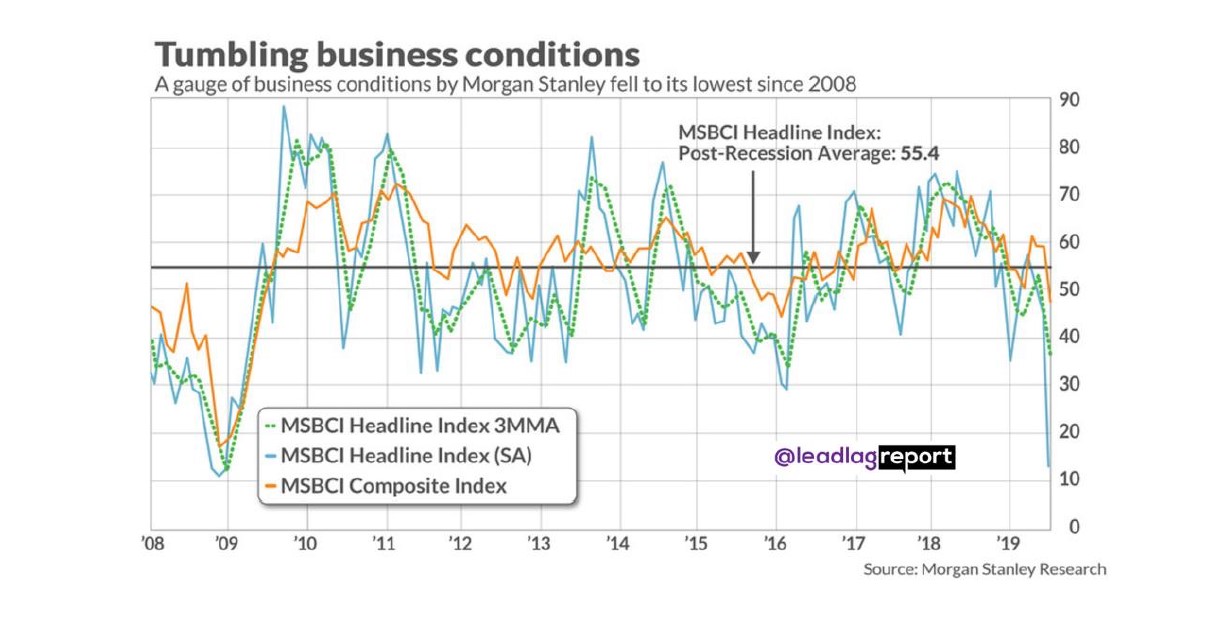

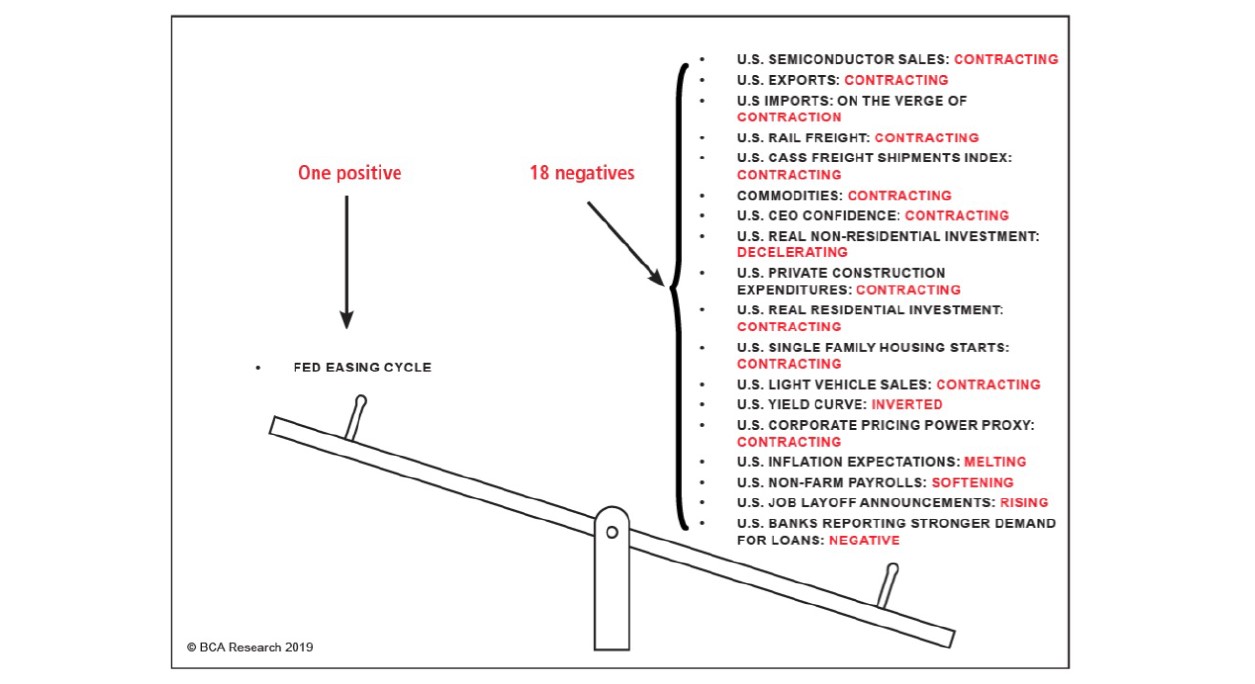

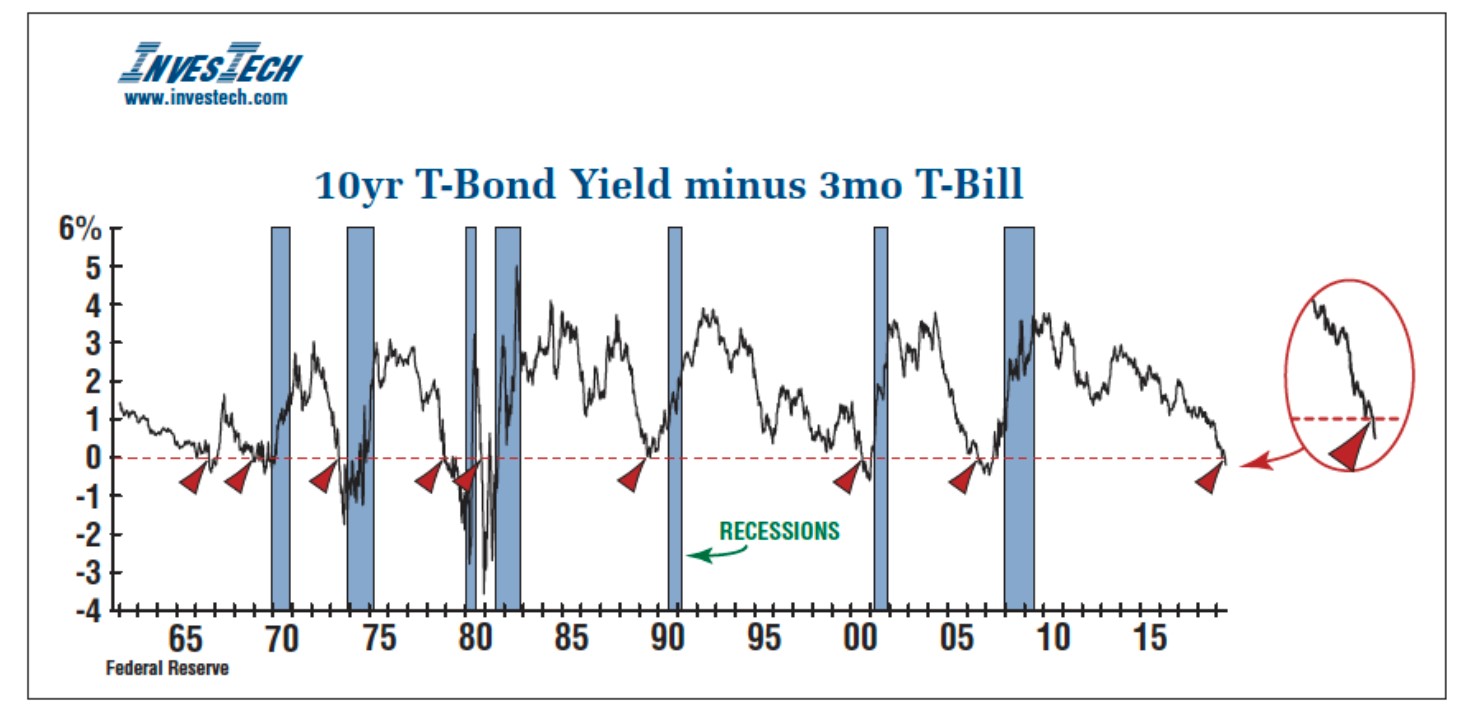

In our previous two Client Letters we outlined the accumulating evidence of the former robust U.S. economy beginning to stagnate and posing risk to domestic corporate profit growth. As we enter mid-summer, the news continues to be negative on balance. Most of the developed world’s economies continue to worsen. The risk of recession in the U.S. refuses to abate. The U.S. yield curve as a predictor of recession is currently as ominous as it gets. The two-year Treasury has now dipped 75 basis points below the high target range of the Fed Funds rate, signaling that the Fed is at least 100 basis points too tight. Note too, with the exception of just 1967 and 1995, every episode of the Fed easing monetary policy has been part and parcel of a recession.

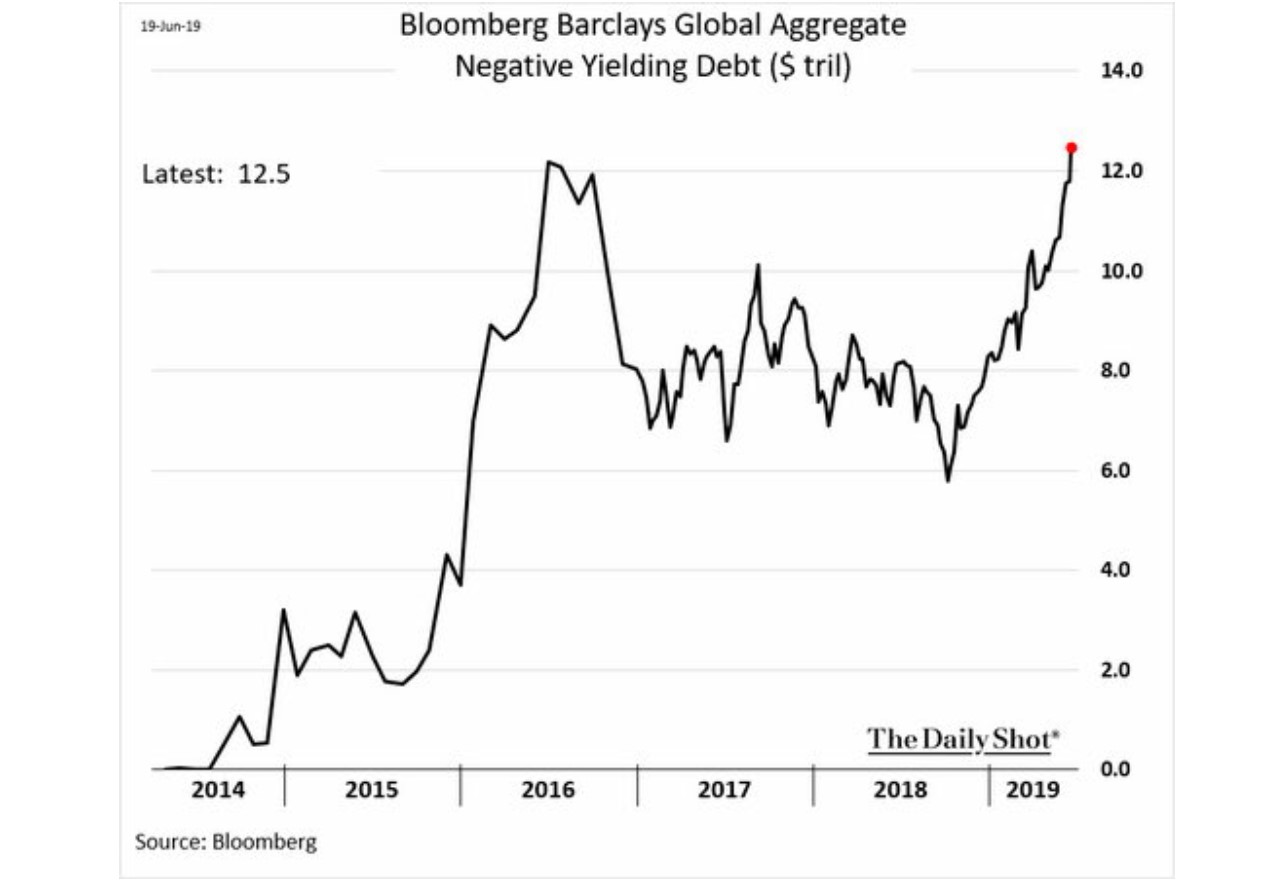

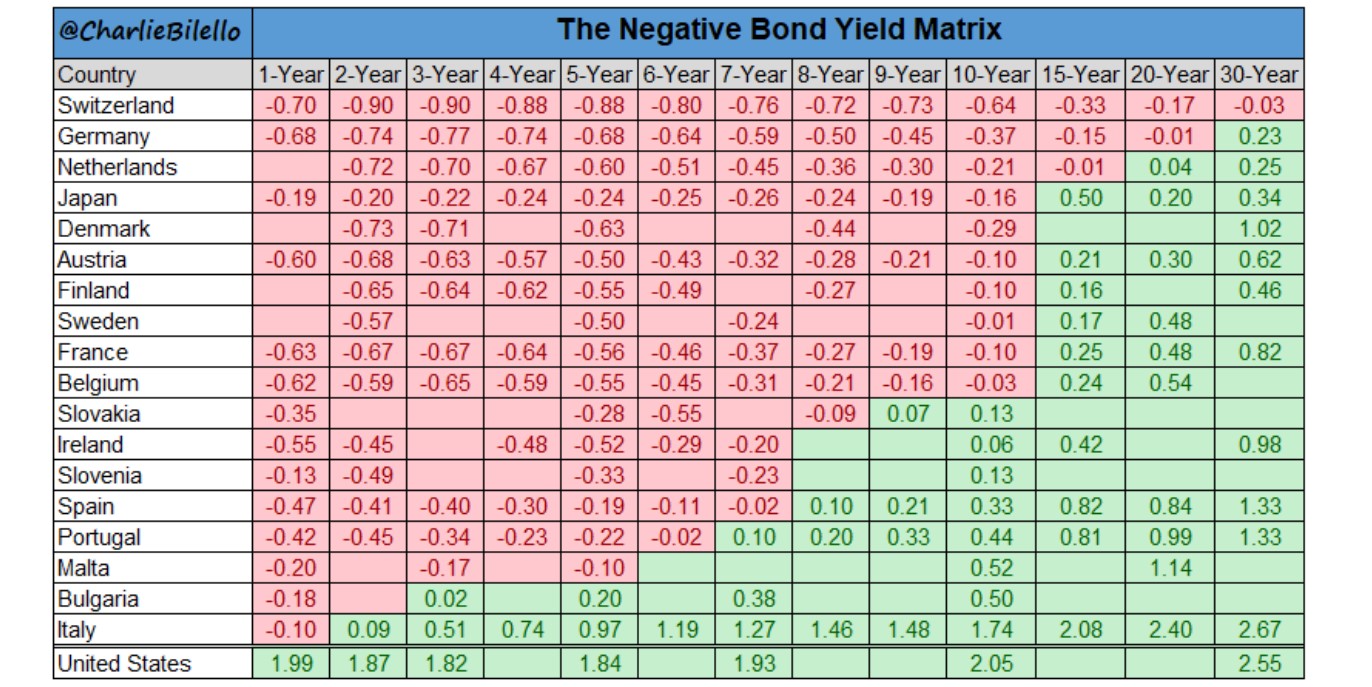

Astonishingly, $13 trillion in sovereign debt now sports negative yields in nominal terms – of course in real terms, even more. Investors across the globe are literally flying blind trying value assets against “risk free” rates. Switzerland’s entire yield curve now trades at negative yield – 80% of Germany’s $850 billion bond market.

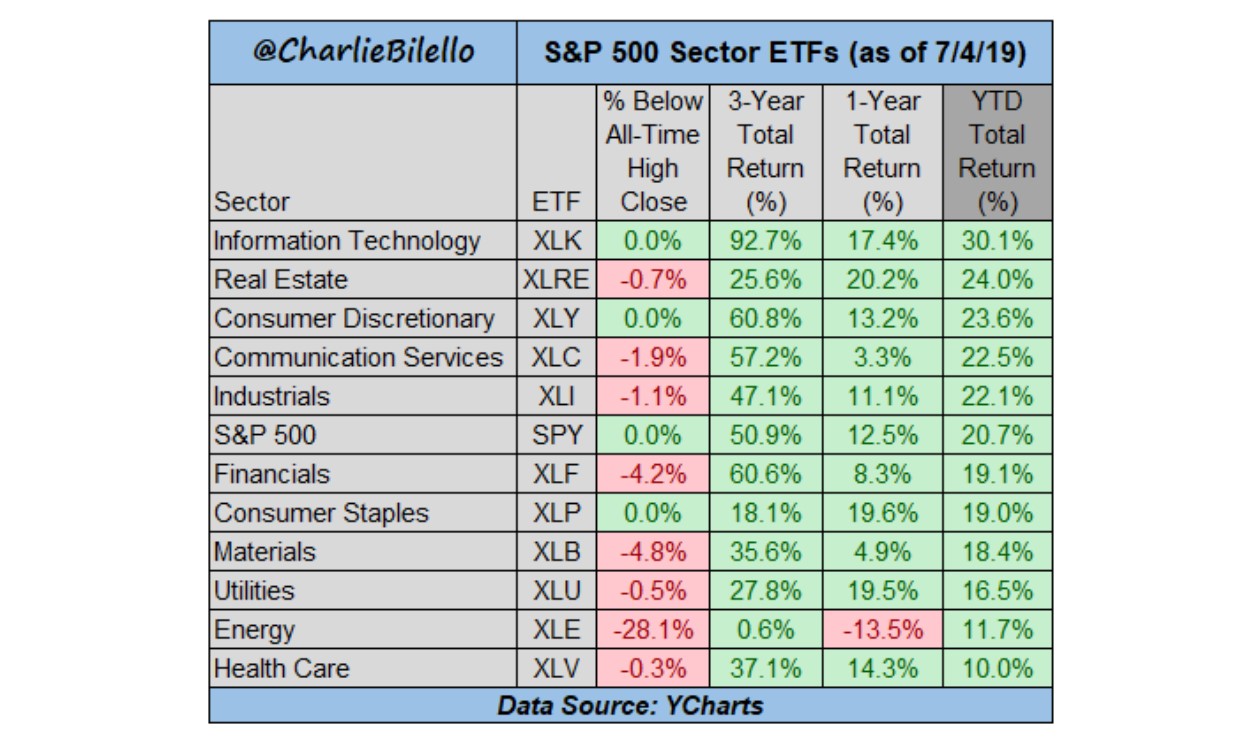

The biggest winners in this remarkable bull market continue to be Technology stocks. (If you want to know how your investment manager ranks in the performance derby just ask them what their Technology weightings have been.) Given the collapse in U.S. interest rates over the past year it’s no surprise that Real Estate, Consumer Staples and Utility stocks have caught a large bid. In fact, “low-vol” stocks posted their best six-month performance since 2009.

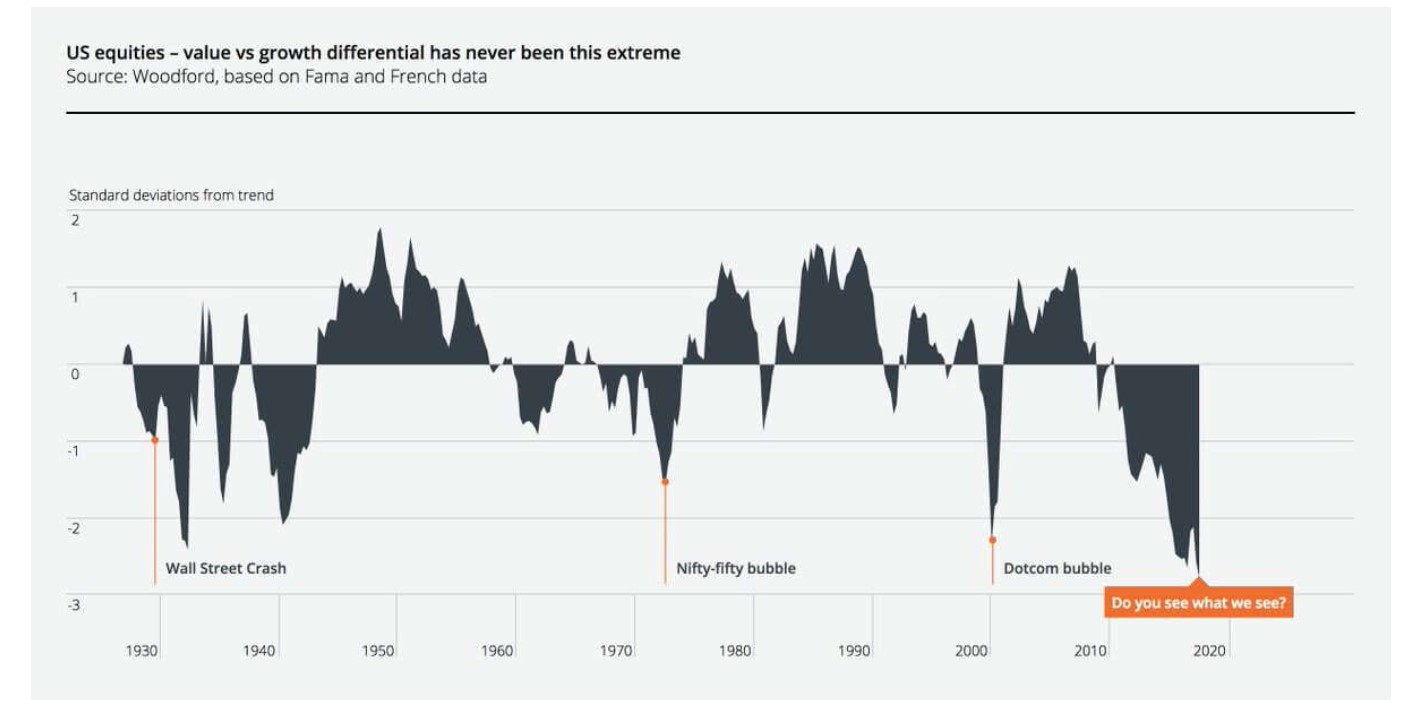

Lastly, Value-oriented strategies have been nearly career-ending endeavors. Value has underperformed Growth during this bull market by amounts that we never thought possible again after the Nifty Fifty bubble in the early-1970’s, as well as the Dotcom bubble still fresh in many investors’ minds today. The contrarian in our collective Wedgewood bones literally aches at the mismatch in such strategies. That said, the penalty of paying top valuation-dollar for Growth companies (particularly sales growth only companies) has been literally riskless since the start of the great bull market. Further, employing valuation strictures has typically been the performance penalty paid since the initiation of QE2 way back in 2012.

In sum we refuse to believe that “Quantitative Easing” creates permanent economic prosperity. We do believe though, that much like Pavlov’s dog, “QE” has been psychologically ingrained in investors to such extents and extremes that far too many have abandoned any prudence of “risk-adjusted returns.” We at Wedgewood refuse to believe that central bankers have permanently “nationalized” a new doctrine that more risk will always generate more return.

We wish to once again thank those clients who have been steadfast in support of Wedgewood Partners.

July 2019

David A. Rolfe, CFA

Chief Investment Officer

Michael X. Quigley, CFA

Senior Portfolio Manager

Morgan L. Koenig, CFA

Portfolio Manager

Christopher T. Jersan, CFA

Research Analyst