On October 24, 2018 Tesla announced its best quarter ever. Sales rose to $6.8 billion from $4 billion the previous quarter. Gross margin improved to 22.33% from 15.46% in the second quarter of 2018 and 15.05% in the third quarter of 2017. Most importantly, earnings per share turned positive and reached a record level of $1.75 per share.

Q3 hedge fund letters, conference, scoops etc

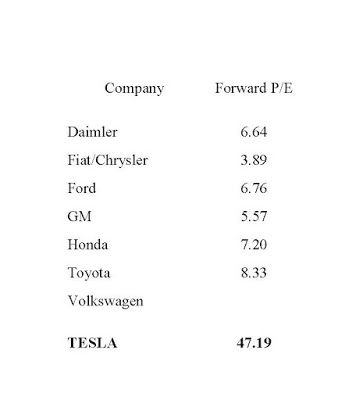

With Tesla’s new-found profitability, for the first time it is possible to compute meaningful P/E ratios and to make comparisons with other auto manufacturers. To do so I assume that Tesla earns the same $1.75 per share for the next four quarters. Some might say it should be more because Tesla is a growth company. Others may say it should be less because Tesla pulled out all the stops to be profitable in the third quarter, including selling only high margin Model 3s. Those of you who disagree can alter the table below to reflect your own assumptions.

The table reports the forward P/E ratios for Tesla and the other major auto manufacturers. The first thing to note is that all the major manufacturers tend to trade around a forward multiple of 6. Toyota is a bit higher at 8.33 and Fiat/Chrysler is a bit lower at 3.89, but not of them approach double digits. In contrast, Tesla’s multiple is 47.19. While one would expect Tesla’s multiple to be higher because of its greater growth opportunities, the gap is so large that it appears as if Tesla is in a different business. It seems hard to believe that as Tesla matures its multiples will not drop toward the industry average. If that happens, the growth in earnings will have to be dramatic to maintain the current stock price.

Article by Brad Cornell’s Economics Blog