Recent articles in Advisor Perspectives by David Blanchett and by Zvi Bodie and Dirk Cotton have dealt with single-premium immediate annuities (SPIAs) used to generate lifetime income in retirement. The focus of those articles was the pricing and the risks of going without inflation protection. In addition to SPIAs, insurers also offer variable annuities (VAs) and fixed-indexed annuities (FIAs) with optional riders known as guaranteed lifetime withdrawal benefits (GLWBs). I’ll expand on the recent articles by comparing the income-generating properties of SPIAs versus VAs and FIAs, and place particular emphasis on how inflation risk impacts inflation-adjusted income.

Q1 hedge fund letters, conference, scoops etc

Example

This analysis is based on a 65-year-old female making a $100,000 purchase of an annuity product. She has the following purchase options:

- An inflation-indexed SPIA (also called a “real annuity”) with lifetime payments that adjust annually based on actual inflation (CPI-U) – Principal Financial;

- A “COLA” SPIA with lifetime payments that increase by fixed percentage each year – Penn Mutual;

- A VA/GLWB providing lifetime withdrawals that may ratchet up based on underlying investment performance – Vanguard/Transamerica; or

- A FIA/GLWB – providing lifetime withdrawals that increase each year based on the credited returns in the contract – Allianz.

Q1 hedge fund letters, conference, scoops etc

In projecting retirement income, I assume this individual lives to age 90, which is the expected average for a female annuitant based on the latest Society of Actuaries annuity mortality table.

Inflation and investment modeling

The modeling for this analysis involves Monte Carlo projections of variable future inflation and investment performance. The inflation-indexed SPIA has the unique property that real, inflation-adjusted income will remain level regardless of inflation. Real income generated by the COLA SPIA will vary with inflation, and both inflation and investment performance will impact real withdrawals for the VA and FIA.

For investment modeling, stocks are assumed to earn an arithmetic average nominal return of 7% and bonds 3%, with standard deviations of 20% and 7% respectively.

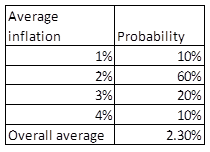

For inflation modeling, there are strong indications pointing to a 2% future average. The current Treasury/TIPS spread is just under 2% and we also know that the Fed is targeting 2% inflation. However, my purely subjective view is that there is a somewhat greater risk of higher inflation, and I’ve modeled future average inflation based on the following probability distribution:

The modeling involves generating 10,000 25-year inflation scenarios. Each of the 10,000 scenarios involves random selection of average future inflation based on the above probability distribution. Then, based on inflation volatility since the early 1980s, I generate random year-by-year inflation assuming a 1.3% standard deviation.

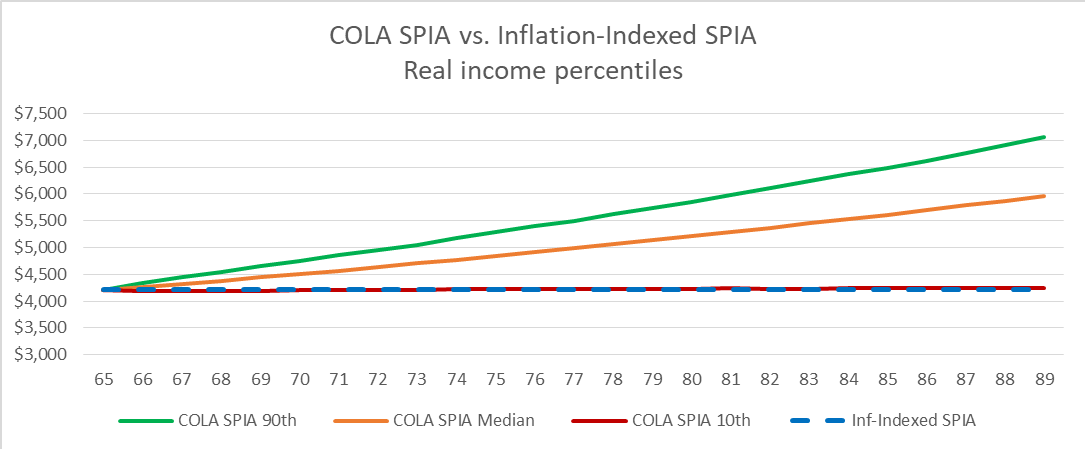

Inflation-adjusted indexed SPIA versus COLA SPIA

The first analysis compares a COLA SPIA to an inflation-indexed SPIA, similar to the analysis in the Blanchett article. Principal Financial is the only insurer currently offering an inflation-indexed SPIA, and, as of early June 2019, $100,000 would purchase an annual lifetime income of an initial $4,211 increasing with inflation each year.

For the COLA SPIA, I determined what fixed annual percentage increase in payments this individual could obtain for $100,000 with the same initial $4,211 payment as for the inflation-indexed SPIA. The pricing service CANNEX provides pricing for 15 companies offering COLA SPIAs, and, for this 65-year-old female, the best rates are from Penn Mutual. By combining COLA SPIAs with 3% and 4% step-ups, we can construct a SPIA that will pay an initial $4,211 with payments increasing by 3.6% each year. These are nominal payments, so the real inflation-adjusted payments will vary depending on Monte Carlo generated inflation. The chart below provides a comparison of the inflation-indexed SPIA versus the COLA SPIA.

Read the full article here by Joe Tomlinson, Advisor Perspectives