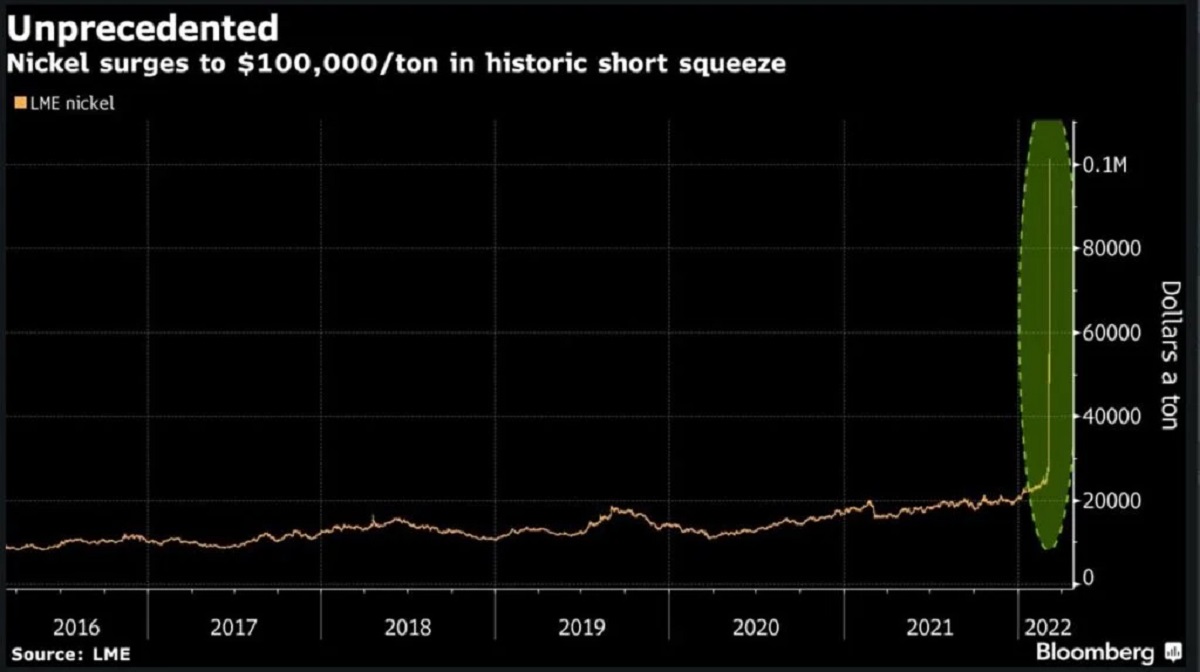

A Chinese tycoon can’t meet the margin on $2 Billion in Nickel losses, so what happens next? Well, here’s a look at the move in Nickel over on the LME (London Metals Exchange) that has everyone talking:

Q4 2021 hedge fund letters, conferences and more

And here’s the scoop about a Chinese “tycoon” being unable to meet Billions in margin calls:

Xiang Guangda, a Chinese tycoon who built a massive short position in nickel futures, is facing billions of dollars in mark-to-market losses after the metal surged more than 170% in two days, sources say https://t.co/QPM6aPBfZq via @cangsizhi @jfarchy pic.twitter.com/GSyz9OYYno

— Stuart Wallace (@StuartLWallace) March 8, 2022

So, how’s all this work? Participants in the futures markets put up a so-called “performance bond” or margin to hold a long or short futures position. This is different from the margin on the securities side, which is borrowed from the broker/dealer. Futures margin is your money and is there as a buffer against losses to make sure the whole system works, and the person on the other side of the trade is ‘good for it.’

The futures ecosystem is set up where clients post this margin, or bond, to the brokers (technically called FCMs = Futures Commission Merchants). The FCMs, in turn, consolidate it and post the collective margin of their clients the exchanges.

What’s more – the FCMs also need to have their own money at risk – about 10% of the amount of margin their clients need at the exchange in excess capital (in case something goes wrong).

Some FCMs will even require a bit more than the exchange required margin (say 125%) to build in an extra cushion; some of you may have gotten an email like that this week. The margin calculation is typically somewhere around 5%-12% of the nominal value of the futures contract. Compare that with the ability to borrow just 50% “on margin” in securities accounts – and you get why futures come with a heavy set of disclaimers.

So what happens when Nickel causes losses greater than the Chinese tycoon’s account as margin? What happens to the longs on the other side of the trade? Their gains are guaranteed against any counterparty risk by the exchange. How does the exchange guarantee such? Well, the first line of defense is the margin/bond the client has in the account. The second line of defense is the capital of the FCM, both the excess capital they are regularly required to have and the rest of their money.

The third line of defense is the exchange’s ‘Guaranty Fund,’ which is in place if the FCM is unable with customer funds or their own capital to meet the capital calls of the exchange. The CME Group currently has a guaranty fund of $5.9 Billion (you can view more about that here.)

The fourth line of defense is the exchange’s assessment powers on its members, which is essentially the ability to fill the guaranty fund back up. The CME’s assessment powers = $16.2 Billion

So – you have the client, the FCM, the exchange, and then ALL the other FCMs and exchange members as the counterparty to each trade… not just that client. It has to be such – or nobody would enter a futures trade for fear the Chinese tycoon goes bust.

The system is built to be anti-fragile and ensure no one counterparty failure becomes the other counterparty’s failure. And it has worked through some tremendous market dislocations (Lehman, Flash Crash, Vixmageddon, Covid).

But…A late-breaking 5th line of defense (which no market participants actually want to see) emerged today, with the LME canceling some of today’s trades!?!?

Canceling trades between willing transactors well after the fact is NOT ok.

Suspending trading is one thing but @LME_news please explain why people should keep trading with you if you can ex post cancel their transactions for your own mystery reasons? https://t.co/DZntOkLyP9

— Clifford Asness (@CliffordAsness) March 8, 2022

To break that 4th wall – as an exchange whose job it is (per all the above) to guarantee those trades – shows this system (at the LME at least) must be under some strain… Perhaps with the decision bust trades or assess members, they chose to bust trades??

We’ll see how this Nickel/LME story plays out – but one way or the other, it’s worthwhile knowing the futures market plumbing in case of an overflow.

Article by RCM Alternatives