Mergermarket, an Acuris company, has released its Global M&A roundup for 2018, including its financial advisors league tables, and with so many market-moving factors fluctuating throughout the year, mergers and acquisitions have understandably had a somewhat ambivalent 2018.

Q3 hedge fund letters, conference, scoops etc

A couple key findings include:

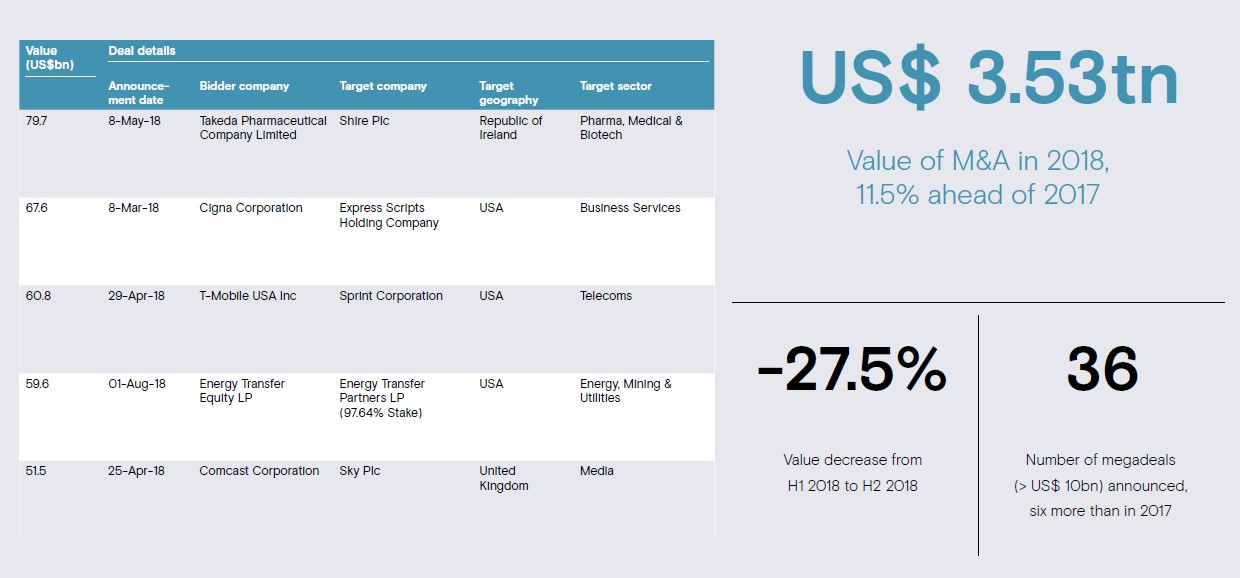

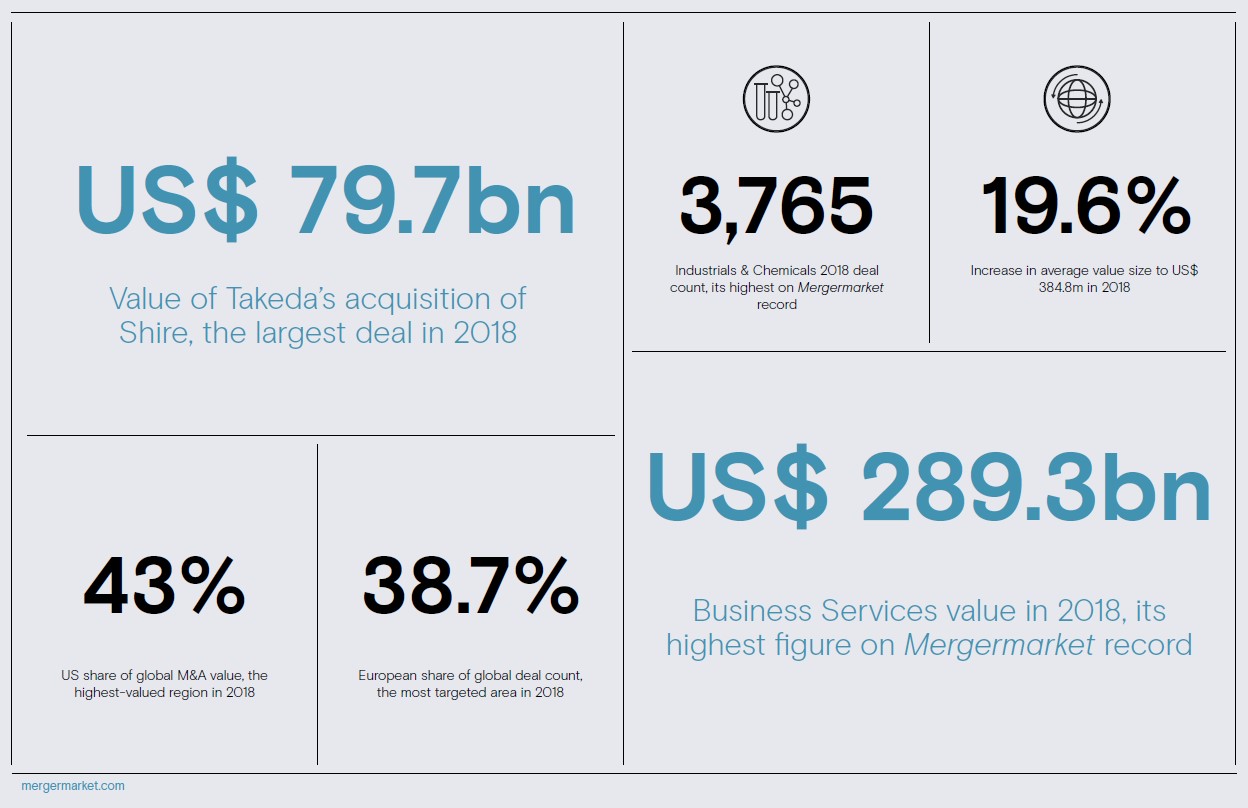

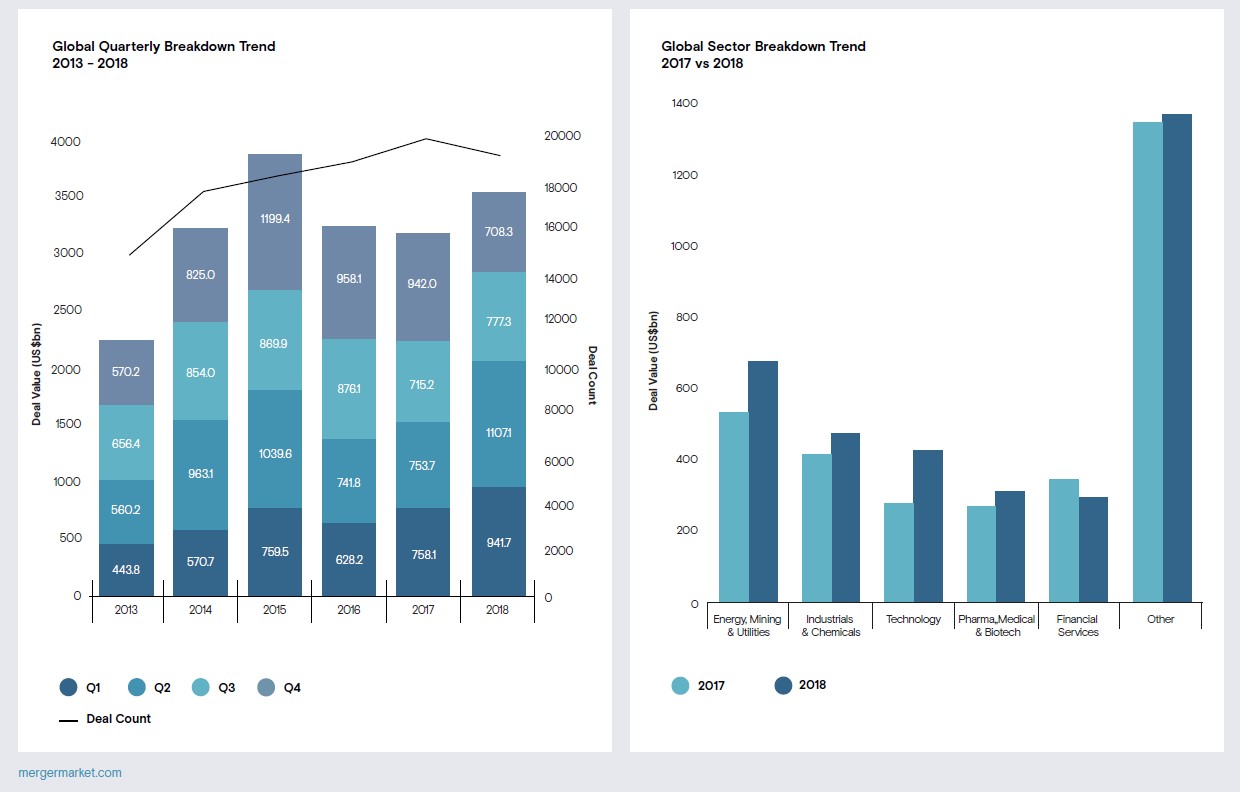

- Intensifying trade tensions, political instability, and increased regulatory scrutiny took their toll on the number of deals struck over the year, which fell for the first time, however slightly, since 2010 to 19,232 after steadily rising for close to a decade. The transactions that did make it to the signing table reached US$ 3.53tn worth of activity, ranking 2018 as the third-largest year on Mergermarket record by value. Average deal size consequently saw its second-highest total value on record with US$ 384.8m, just below the US$ 400.3m peak reached in 2015

- As companies felt the pressure to consolidate, fueled by a need for greater equity value, firms often found themselves competing for the choicest targets, pushing up valuations. Comcast’s eventual US$ 51.5bn Sky takeover was a case in point where the Pennsylvania telecoms giant ended up paying considerably more than its starting offer in an effort to beat rival bidder Twenty-First Century Fox. Further, the continued availability of cheap financing due to historically low interest rates in the post-crisis period aided much of the capital needed to fund bidding wars, particularly in the private equity space. Ahead of expected interest rate rises, global buyout activity reached US$ 556.6bn, its highest total in a decade and 3.7% more than 2017’s US$ 536.7bn. Buyouts also achieved their highest-ever deal count – 3,599 – breaking the previous record of 3,530 set in 2017. Meanwhile, sponsors exited the second-highest number of investments on record, registering 2,450 compared to a peak of 2,592 in 2017. Moreover, 2018 reached the highest total exit value ever of US$ 551.5bn

Global & Regional M&A Report 2018

Global Overview

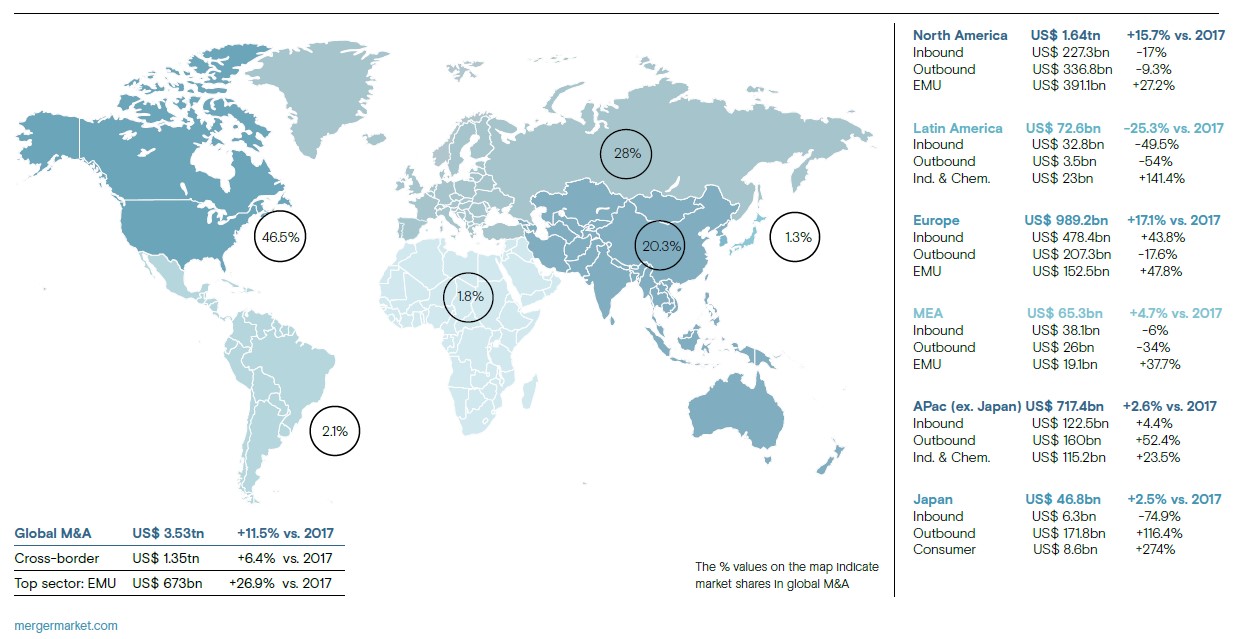

Regional M&A Comparison

Global

- With so many market-moving factors fluctuating throughout the year, mergers and acquisitions have understandably had a somewhat ambivalent 2018. Intensifying trade tensions, political instability, and increased regulatory scrutiny took their toll on the number of deals struck over the year, which fell for the first time, however slightly, since 2010 to 19,232 after steadily rising for close to a decade. The transactions that did make it to the signing table reached US$ 3.53tn worth of activity, ranking 2018 as the third-largest year on Mergermarket record by value. Average deal size consequently saw its second-highest total value on record with US$ 384.8m, just below the US$ 400.3m peak reached in 2015.

- As companies felt the pressure to consolidate, fuelled by a need for greater equity value, firms often found themselves competing for the choicest targets, pushing up valuations. Comcast’s eventual US$ 51.5bn Sky takeover was a case in point where the Pennsylvania telecoms giant ended up paying considerably more than its starting offer in an effort to beat rival bidder Twenty-First Century Fox. Further, the continued availability of cheap financing due to historically low interest rates in the post-crisis period aided much of the capital needed to fund bidding wars, particularly in the private equity space. Ahead of expected interest rate rises, global buyout activity reached US$ 556.6bn, its highest total in a decade and 3.7% more than 2017’s US$ 536.7bn. Buyouts also achieved their highest-ever deal count – 3,599 – breaking the previous record of 3,530 set in 2017. Meanwhile, sponsors exited the second-highest number of investments on record, registering 2,450 compared to a peak of 2,592 in 2017. Moreover, 2018 reached the highest total exit value ever of US$ 551.5bn.

- The year also saw the emergence of a few sectors to watch. While Energy, Mining & Utilities (EMU) ranked first by hitting its second-highest value on record with US$ 673bn, Construction reached a new decade high of US$ 116.5bn, driven by PE plays and infrastructure bids; total value was just under 2007’s record of US$ 116.8bn. Defense also set a new record with US$ 28.8bn as competition for government contracts heated up, according to Mergermarket intelligence. Business Services saw a new high of US$ 289.3bn, bolstered by defensive healthcare services moves in the US and PE interest in information providers. Although deal count fell almost everywhere, Agriculture emerged from the fog of uncertainty to reach a record high with 219 transactions, boosted by the emerging North American cannabis industry.

- Against a backdrop of growing socio-political tensions, dealmaking continued at an encouraging rate. With tariffs, trade wars, the UK’s exit from the European Union, and an underlying sense of general economic uncertainty and unease, it may be surprising that figures have held up as they have. Yet activity did suffer in some corners. Chinese buys of US firms fell 94.6% to US$ 3bn from a record USD 55.3bn in 2016. Meanwhile, China’s bids in Europe rose 81.7% to US$ 60.4bn from US$ 33.2bn last year. Cross-border count fell by 6.6% to 6,405, while valuations inched higher to US$ 1.35tn from US$ 1.27tn the year prior. Domestic count slipped to 12,827 from 13,115, while value increased 15% to US$ 2.18tn from US$ 1.90tn. US consolidations accounted for much of this, with top deals in pharmacy benefit management, telecommunications, energy, software, retail, and real estate, many of which found consolidation necessary for survival as technology disrupts sector after sector – a trend that seems likely to continue causing more structural changes in 2019.

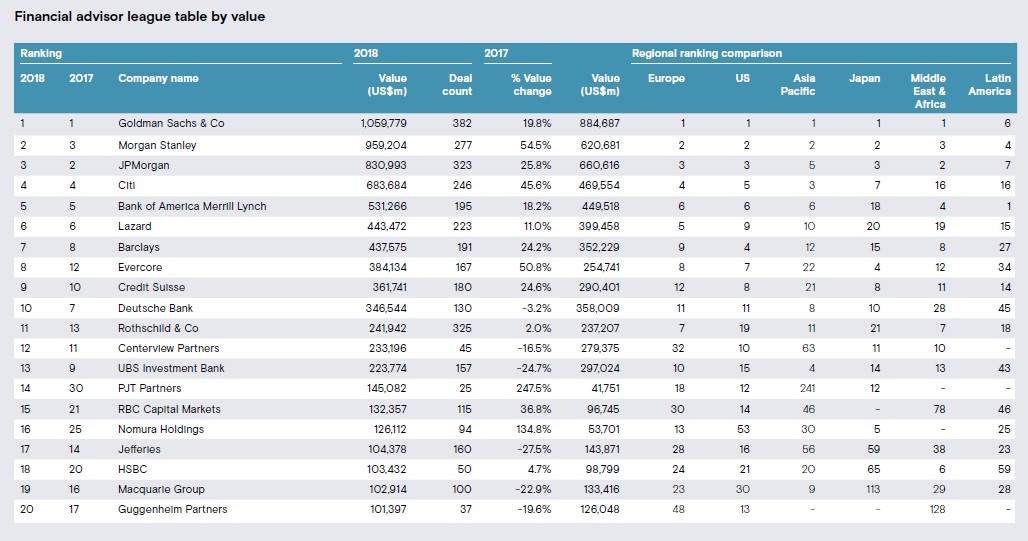

Global League tables

Europe

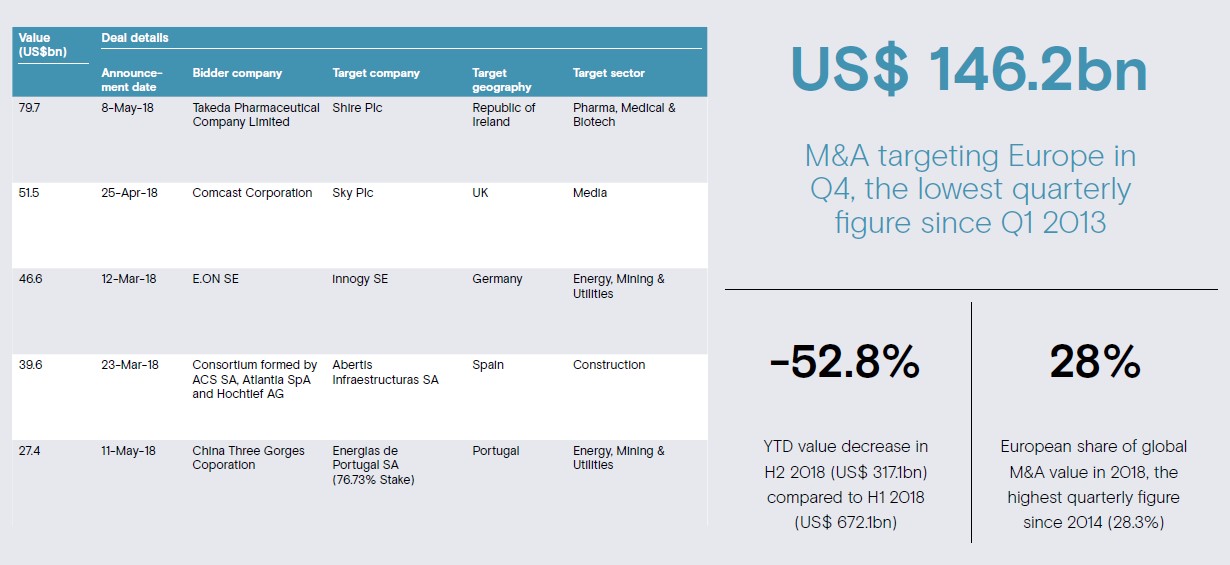

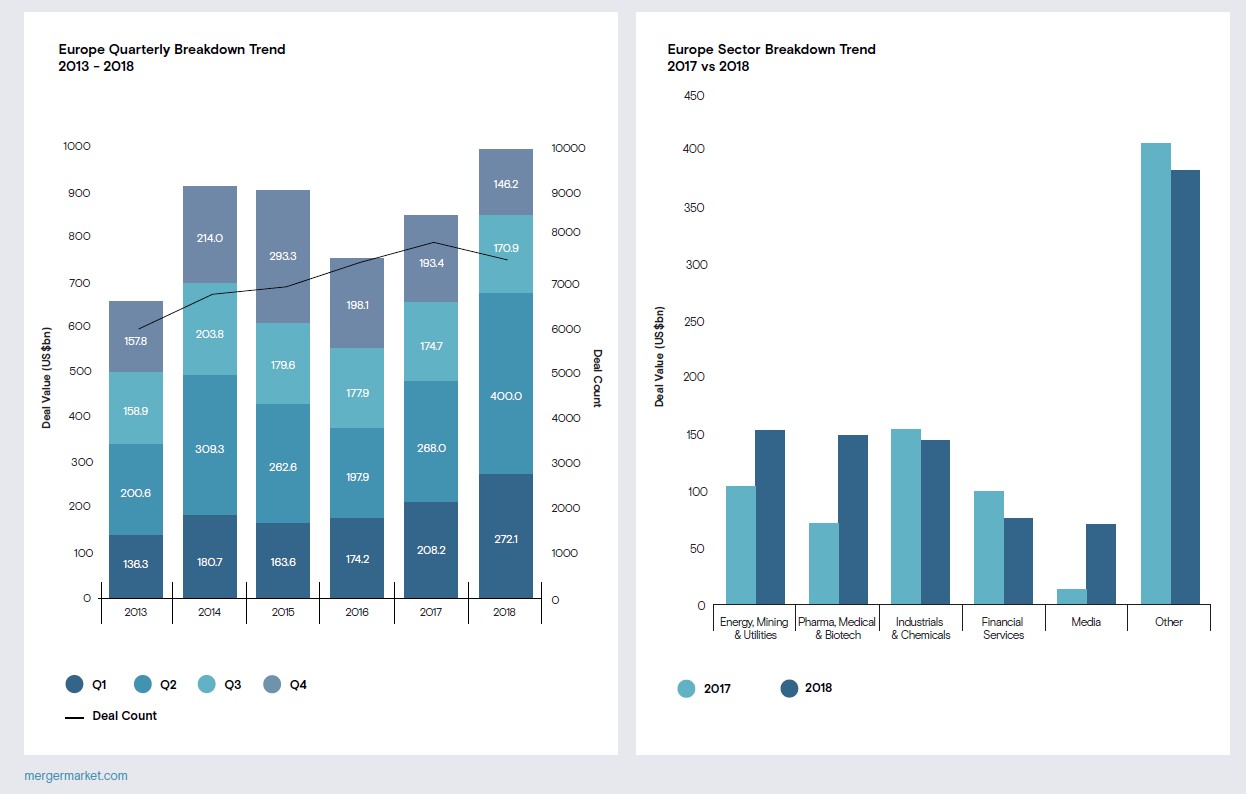

- Politics continues to plague European dealmakers, as M&A experienced a considerable drop during the second half of the year, as Q4 recorded US$ 146.2bn worth of activity, the lowest quarterly value since Q1 2013. While Europe received 11 megadeals (> US$ 10bn) in 2018, four more than the entirety of 2017, all were announced in the first five months. Rising protectionism, government intervention, and continued uncertainty have all undoubtedly caused firms to reconsider high-profile investments. The region saw just ten deals worth over US$ 5bn in H2, including Hitachi’s US$ 9.4bn acquisition of ABB’s power grids business and the US$ 7.1bn Calsonic Kansei/Magneti Marelli deal. Despite the continent reaching its highest post-crisis value (US$ 989.2bn) and highest value share of global M&A (28%) since 2014, dealmakers will be concerned over the slowdown in activity in H2 and whether 2019 will return to the buoyant levels seen in recent years.

- Prolonged uncertainty regarding the future relationship between the UK and the rest of the EU has caused a noticeable slowdown in M&A activity. This has been particularly felt in the final three months of the year as Theresa May battled both sides of parliament once her deal was agreed with the EU. In Q4 the UK recorded its lowest quarterly value and volume since the referendum with just US$ 34.1bn (333 deals) announced. A delay to the final vote in the House of Commons and subsequent confidence vote in the UK Prime Minister will have done little to reassure investors, and the looming threat of a no deal scenario could see continued subdued activity in 2019. M&A targeting the EU27 has seen a similar dip, albeit less pronounced, from the exceptional start to the year. The lack of clarity has resulted in further domestic consolidation in the UK, something which may further increase in 2019, particularly in the retail space, given the ongoing political and economic difficulties.

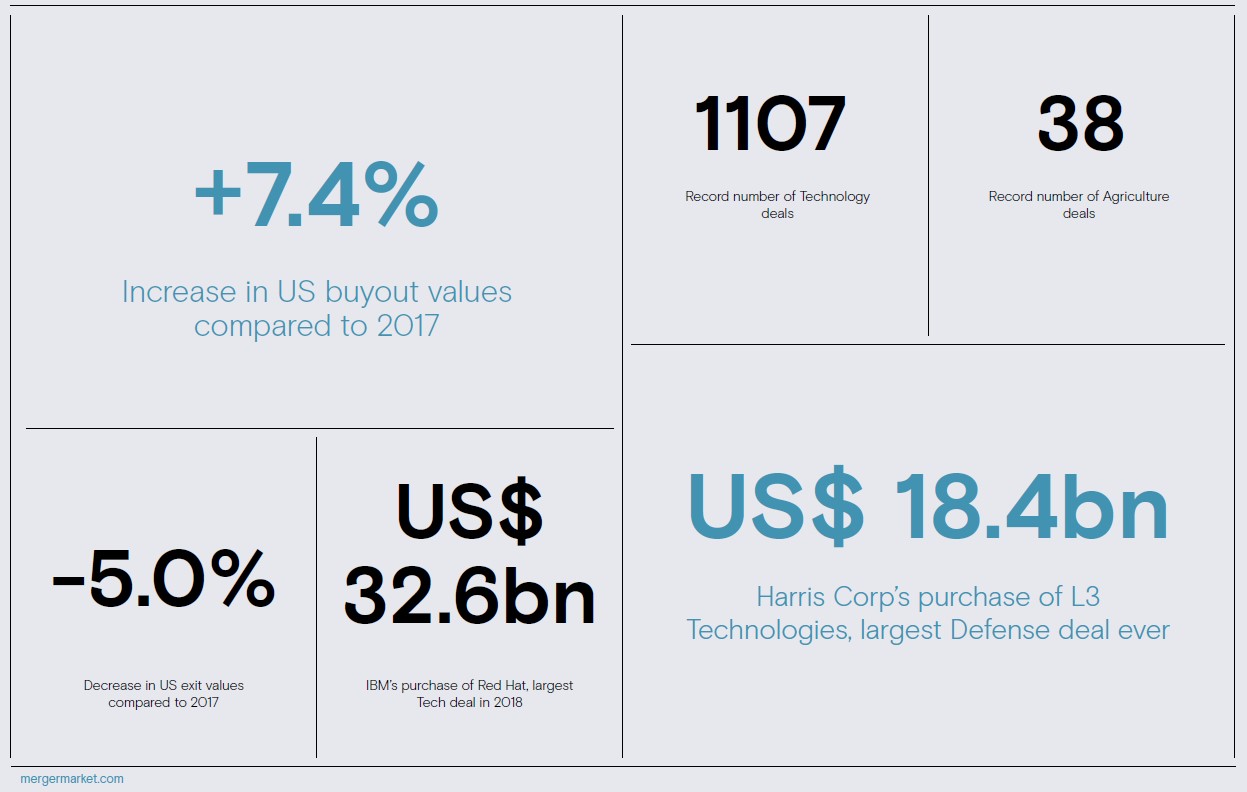

- Private equity was key to M&A levels, with buyout activity hitting US$ 195.5bn (1,458 buyouts), its highest value since the crash. With unprecedented levels of dry-powder readily available, private equity houses have looked towards higher-valued firms, including listed companies. Take-private buyouts have soared in recent years with 64 such deals announced since the start of 2016, including the proposed US$ 4bn takeover of Travelport Worldwide and the US$ 2.9bn acquisition of Testa Residencial, both announced in H2. In 2018, take-private buyouts reached its highest annual value and joint-highest volume since the crisis with US$ 26bn recorded across 22 deals. This accounted for an 13.3% share of the year’s overall buyout value. As the mid-market becomes ever-more saturated, the pressure put on GPs to invest the vast sums available should result in continued high levels of activity in the coming year. For example, there is reported private equity interest in firms such as L’Occitane and Nestle Skin Health, which could result in multi-billion euro deals.

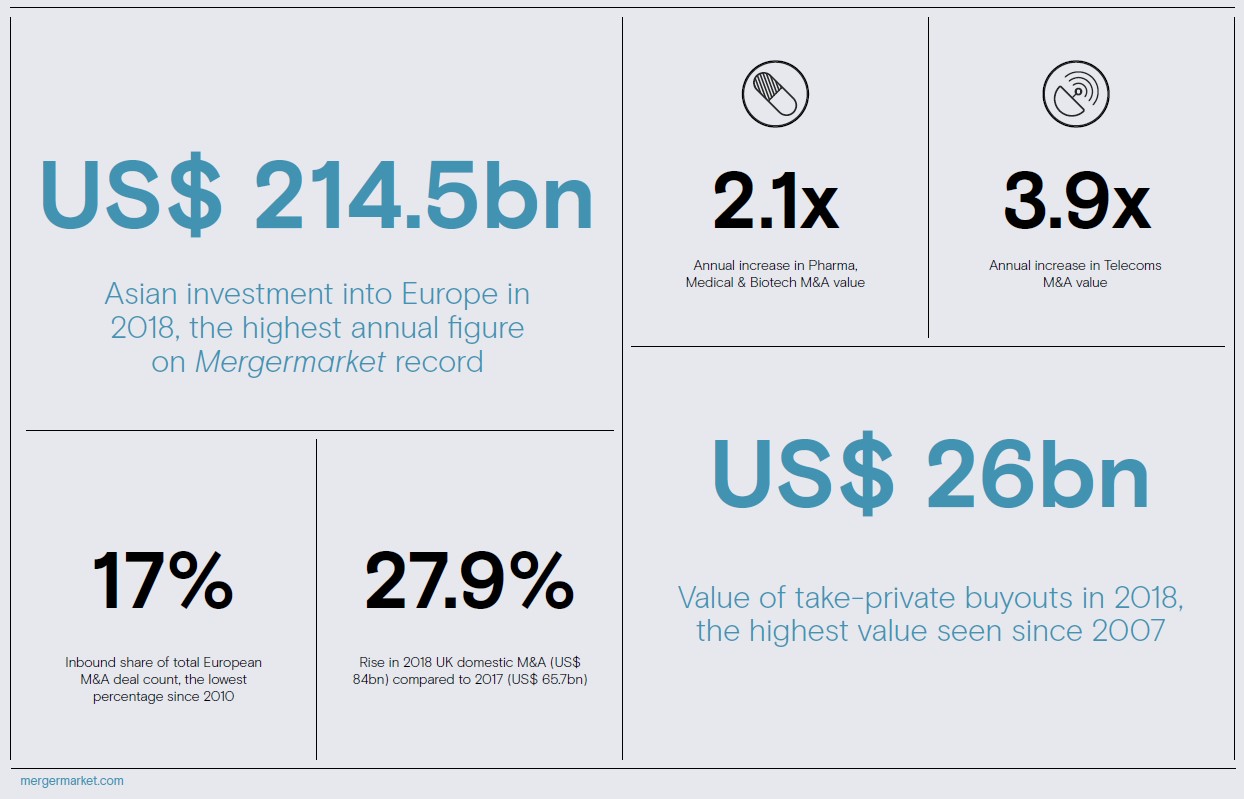

- A series of high-profile transactions resulted in Energy, Mining & Utilities (EMU) becoming the highest-valued sector in Europe, with US$ 152.5bn recorded across 402 deals. Takeovers of innogy and EDP, together with interest in North Sea assets and renewable energy, pushed the sector to its highest annual value in since 2012 (US$ 218.6bn, 430 deals). Europe accounted for 22.7% of global EMU M&A (US$ 673bn), its highest share since 2015. Amid global changes to the way consumers interact with products and services, the Tech, Media, and Telecoms sectors all saw noticeable upticks in activity. Telecoms reached its highest annual value in Europe since 2014 (US$ 94.8bn), registering US$ 69.6bn worth of M&A, which included Vodafone’s US$ 21.8bn acquisition of Liberty Global’s German and CEE operations, and the US$ 10.5bn takeover of TDC.

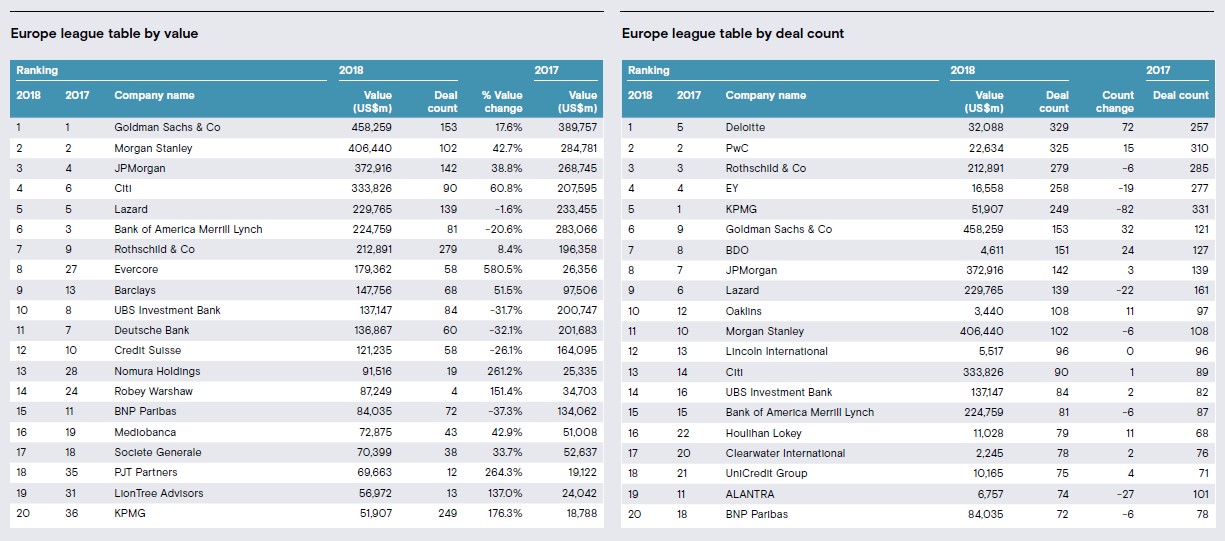

Europe League tables

United States

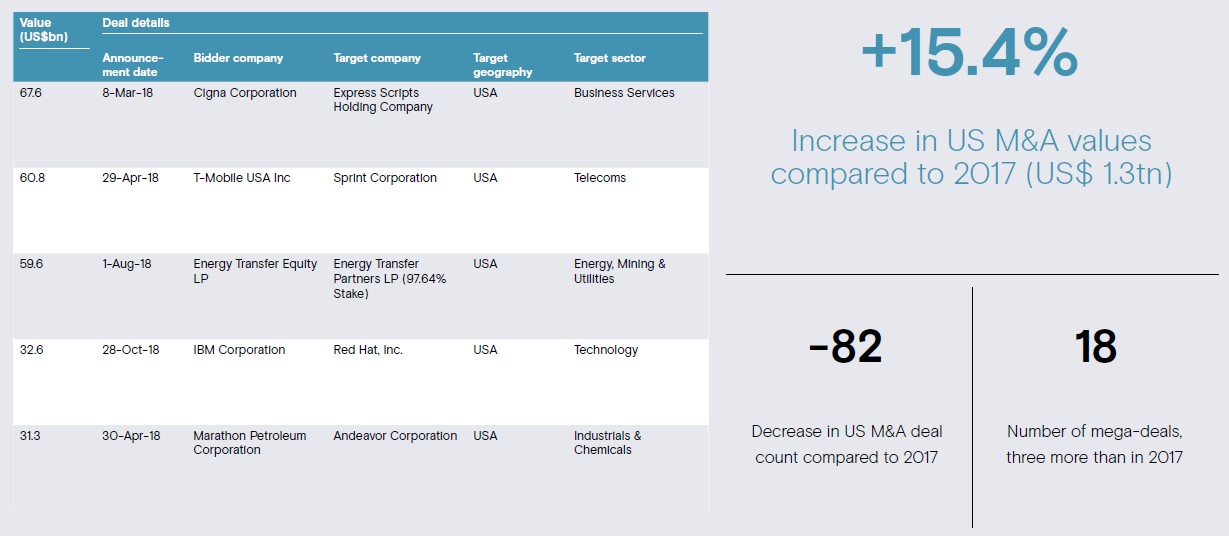

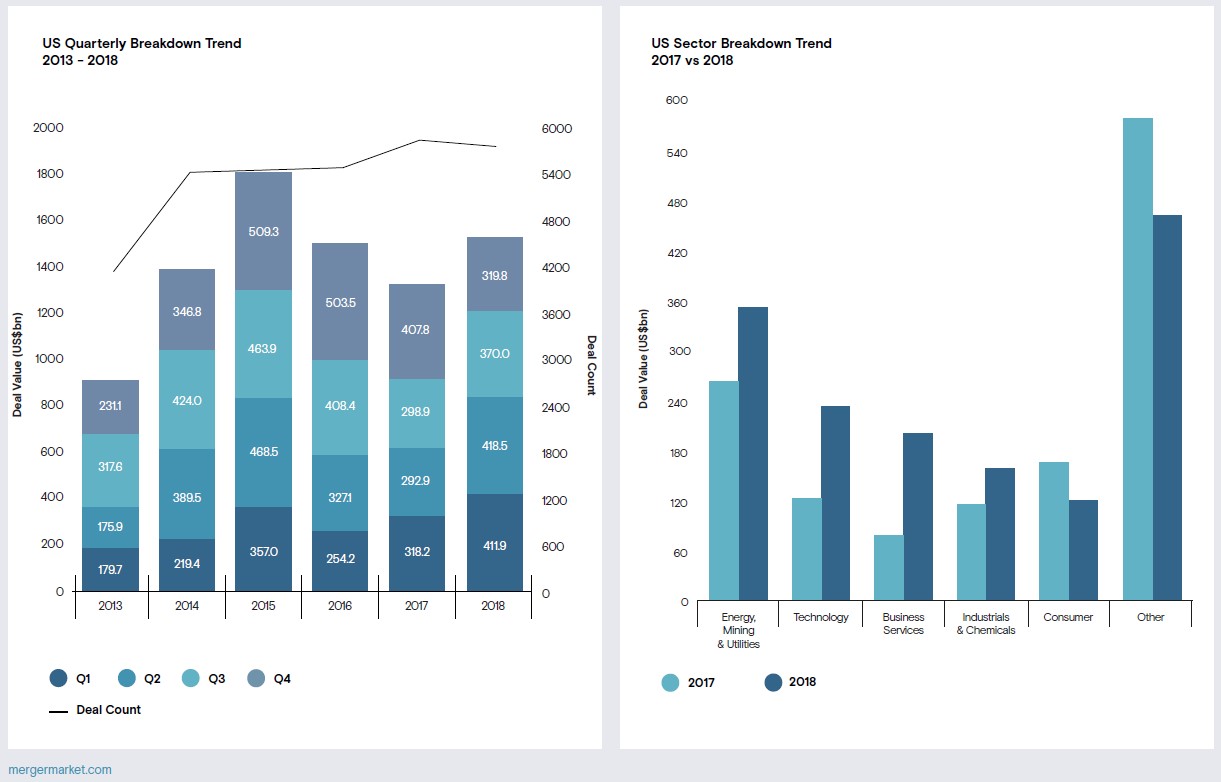

• The final quarter of 2018 brought some resolution to the year’s political uncertainty with the US midterm elections in November, though other concerns have taken their place. With rising interest rates and a new Democratic majority set to take over the House of Representatives in 2019, worries that valuations could see some effect and deals potentially coming under even more scrutiny than over the past couple of years remain. By the end of 2018, nonetheless, US M&A reached US$ 1.5tn, the second-highest total value ever and up 15.4% from 2017’s US$ 1.3tn. Deal count also achieved its second-best figures on record with 5,718 transactions, down slightly from 2017’s record 5,800. Moreover, the US share of global deal value increased to 43% in 2018, up from 41.6% in 2017, while its share of global deal count rose slightly to 29.7%, up from 29% in 2017. However, new uncertainties by year’s end from the global stock market sell-off as well as the government shutdown have dampened some enthusiasm among dealmakers.

• As a whole, 2018 is unlikely to go down in M&A history as one that would put any observer of the business world to sleep. While Q1 saw the White House blocking then Singapore-based (now US-based) Broadcom’s bid for US-based semiconductors firm Qualcomm on the basis of national security concerns, in Q2 the finale of the AT&T/Time Warner antitrust trial saw that transaction finally close after a federal court ruling in its favor, resulting in the Justice Department losing its lawsuit to block the deal. Further, against a backdrop of national security concerns and trade tensions, 2018 saw protectionism gaining more of a foothold, with dealmakers appearing stuck between the need to consolidate in an increasingly technological world fuelled by cheap financing and the uncertainty of making deals in an environment of trade wars and tariffs.

• With global political and economic tensions rising, activity between the US and China, one of its largest trading partners, has seen a sharp decrease in the past year, plunging 94.6% from a record high inbound value of US$ 55.3bn in 2016 to just under US$ 3bn in 2018. From 2017 (US$ 8.7bn), activity fell 65.8% in value. In terms of deal count, this year has seen activity fall from 63 transactions in 2017 to 38 in 2018, and a drop by 35 transactions from a peak of 73 recorded in 2016. In fact, the largest Chinese bid for a US company in 2018 did not even break the billion dollar mark – Bison Capital’s US$ 450m bid for US biopharmaceutical firm Xynomic Pharmaceuticals, whose completion is still pending as of this writing.

• US M&A saw a number of sectors shattering value records, included Business Services, boosted by the aforementioned Cigna/Express Scripts deal, reaching US$ 200bn; Construction, recording US$ 29.5bn; Defense M&A reaching a record US$ 26.6bn; and the year’s top sector Energy, Mining & Utilities (EMU), reaching US$ 350.4bn. Media, following the resolution of the antritust lawsuit against its largest deal ever recorded (AT&T/Time Warner, US$ 105bn) fell 76.5% in value of US$ 26.7bn from US$ 113.6bn in 2017. Though technologies continue to put pressure on sectors such as Media to consolidate, in a time of intense regulatory scrutiny, dealmakers understandably have some cause for concern before engaging in the mega-deals of yesteryear. Further, with interest rates steadily rising and the cost of financing such transactions projected to similarly increase, it is unclear to what degree activity is poised to continue on its upward trend in 2019.

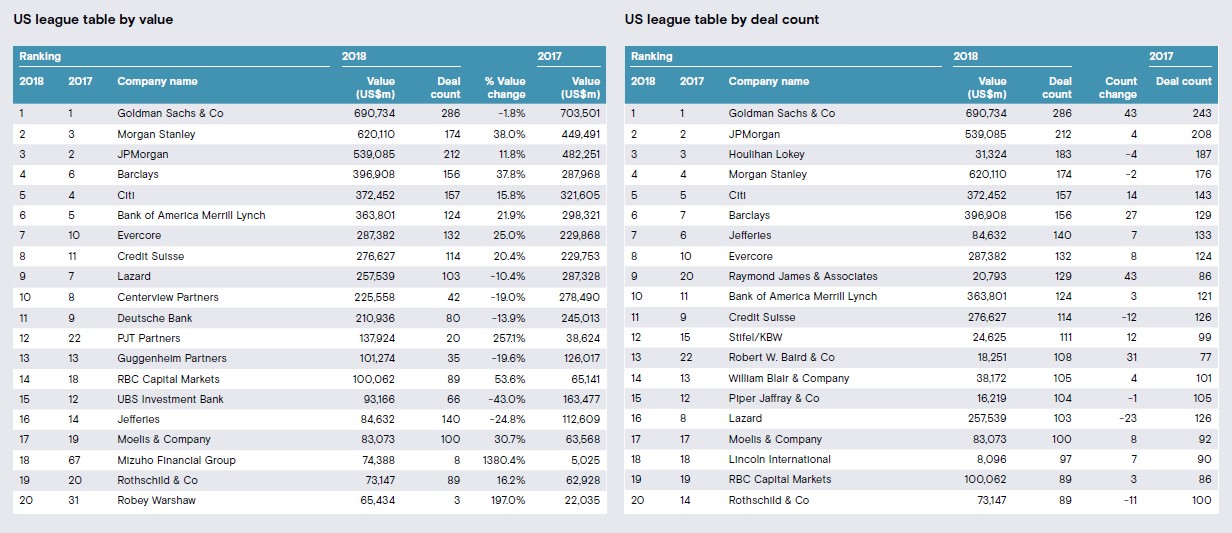

US League tables

See the full report below.