Preqin is proud to have partnered with the Australian Investment Council to produce the 2019 Yearbook Report on Australian Private Equity & Venture Capital Activity.

Q1 hedge fund letters, conference, scoops etc

The report covers activity data on funds, deals and exits across the private equity & venture capital industry in Australia, based on data contained in the Preqin data platform, Pro, as well as on-the-ground information collected by both Preqin and the Australian Investment Council.

As wider global economic and political tensions combine with testing circumstances closer to home, Australia faces another interesting and somewhat challenging year in 2019. Despite this, unemployment remains low and the domestic economy continues to grow, fostering a positive environment for the private equity & venture capital market – fundraising hit a record high in 2018, and total investment activity increased significantly from 2017. Now standing at just over AUD 30bn in size, the Australian private equity & venture capital industry is a force to be reckoned with.

Foreword

We are very pleased to present the latest Yearbook Report, jointly produced and published by the Australian Investment Council and Preqin. The report covers activity data on funds, investments and exits across the private equity & venture capital industry in Australia. This continues the partnership that Preqin and the Australian Investment Council have developed in tracking, recording and disseminating industry data to market participants and the business community in Australia.

Australia faces another interesting and somewhat challenging year in 2019. Domestically, a federal election has just been held, and the repercussions of the royal commission into banking and financial services are working their way through the financial system and wider economy. Meanwhile, risks of a global slowdown – and how central banks respond – weigh on equity markets, Brexit remains unresolved, and trade tensions between the world’s two largest economies are high.

Amid these testing circumstances, Australian unemployment remains low and the domestic economy continues to grow. This backdrop provides a strong set of fundamentals for investors, including those that are actively looking for opportunities in private capital markets.

The industry figures for the full 2018 calendar year presented in this report show strong levels of activity in private equity & venture capital in Australia. Firstly, fundraising hit a record high of $6.6bn. This has helped to boost the dry powder available for investment to over $11bn. Secondly, investment activity also experienced a significant increase across both the private equity and venture capital sectors compared to the 2017 annual period.

These positive trends point to a confident investor outlook, as both fund managers and institutional investors deploy increasing amounts of capital into funds and, importantly, businesses that employ thousands of people across every sector of the economy.

Lastly, the scale of assets managed by our industry, now standing at just over $30bn, is a testament to solid institutional support for private capital investing. We expect that support to continue to grow as the industry in Australia develops and matures further.

We would like to thank all industry participants who have contributed their data to the report – your support ensures that we can report on the industry as comprehensively as possible. Private equity and venture capital play a vital role not only in delivering returns to super funds and other major investors, but also in furthering the development of the wider economy in Australia and globally. Preqin and the Australian Investment Council are both very pleased to play an important role in the industry with the publication of this report.

Yasser El-Ansary

Chief Executive, AIC

Mark O’Hare

CEO, Preqin

Executive Summary

Activity in the private equity (PE) & venture capital (VC) industry in Australia in the 2018 calendar year has seen higher levels of fundraising and investment compared to 2017. This points to a confident outlook for the private capital market, as both fund managers and institutional investors deploy increasing amounts of capital into funds and businesses.

The industry’s assets under management (AUM) stand at just over $30bn as at June 2018, an all-time record. Australia-based buyout funds account for the highest amount of AUM at $20bn. Industry-wide dry powder stands at a healthy $11bn.

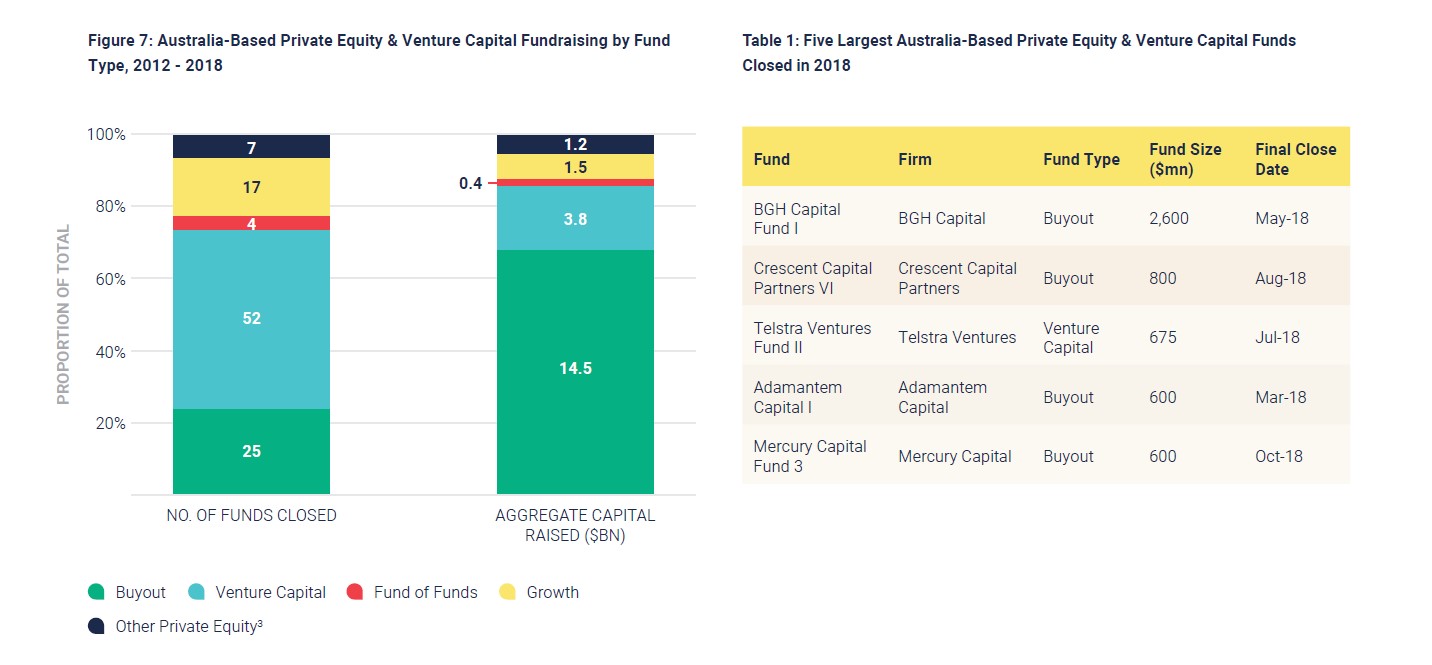

In the 2018 calendar year, the fundraising activity of Australia-based PE and VC fund managers hit a record high in terms of capital raised, with $6.6bn in aggregate capital secured by 17 PE and VC funds. PE funds raised a total of $5.3bn across eight funds, while VC funds raised $1.3bn across nine funds. Buyout funds have been the dominant segment for fundraising since 2012, having secured $14.5bn, more than double the amount of capital raised by all other fund strategies combined throughout these years ($6.9bn).

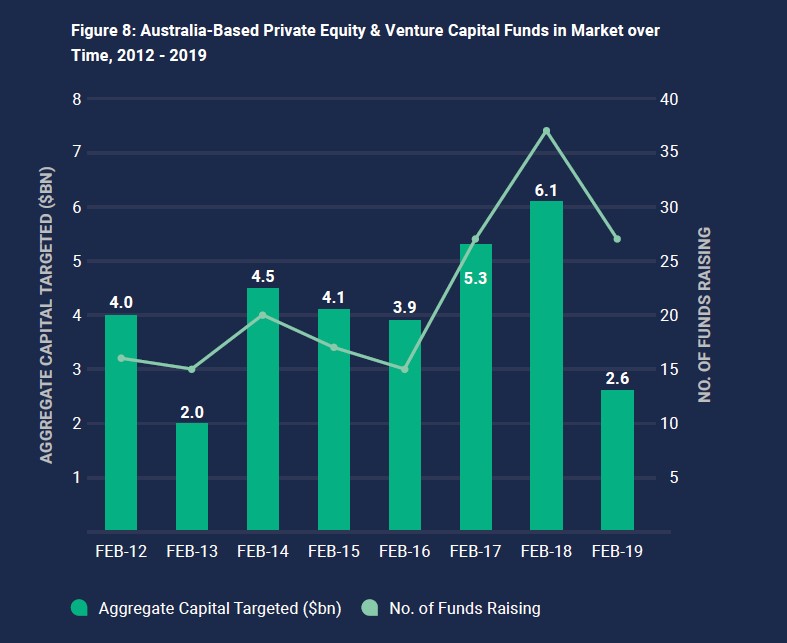

Following several years of strong fundraising, the aggregate capital targeted by PE and VC funds in market is lower as at February 2019 compared to the same point in both 2017 and 2018.

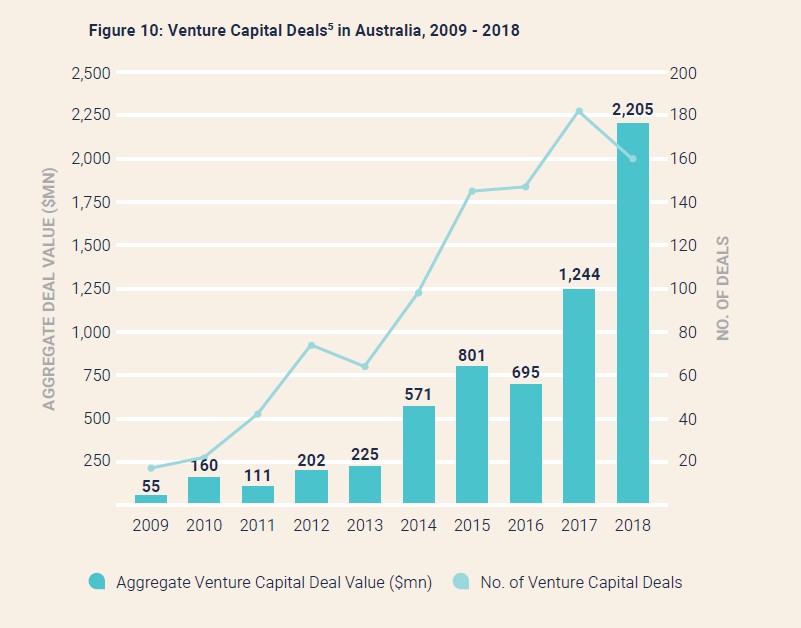

Investment activity across Australia’s private capital sector in 2018 experienced a significant increase in both the PE and VC markets. This marks a new turn from the declining trend seen in the market since 2016. This positive trend in investment activity has been driven by sufficient dry powder levels, the low-risk environment and the attractive fundamentals of many privately backed companies in Australia for both domestic and foreign investors. The VC sector had an especially strong year in 2018 as total deal value more than doubled from 2017 to a record $2.2bn.

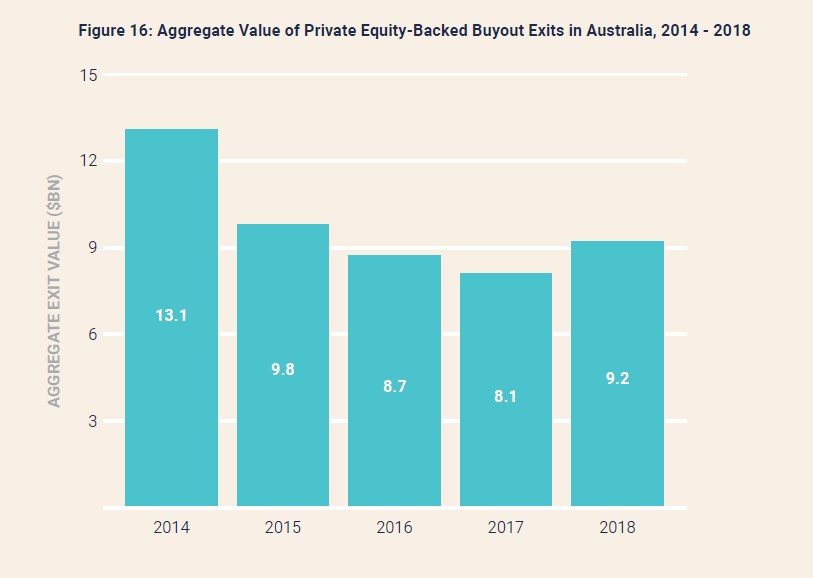

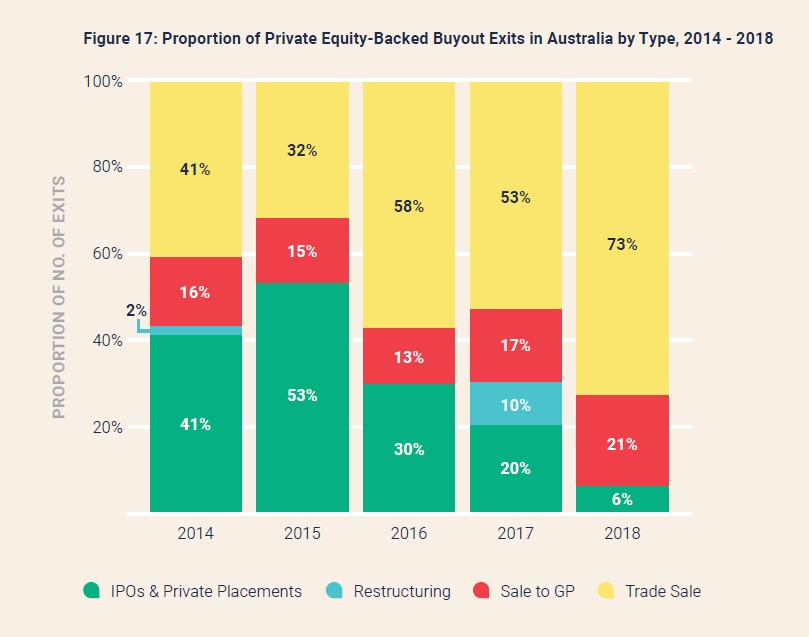

Looking at divestment activity, aggregate buyout exit value made a modest recovery in 2018 to $9.2bn, from a low of $8.1bn in 2017, stemming the consecutive drop in aggregate exit value since 2014. Trade sales were the favoured exit pathway, and represented a record 73% of total buyout exits in Australia in 2018.

- Assets Under Management: Assets By Fund Type

- Assets Under Management: Australia’s Regional Ranking

- Fundraising PE & VC Fundraising Gains Traction

- Buyout Funds Continue To Dominate

- Fundraising Funds In Market: New Age For VC?

- Deals & Exits Overview

- Deals & Exits Buyout Deal Activity

- Deals & Exits VC Deal Activity

- Deals & Exits VC Deal Activity

- Deals & Exits Exit Activity

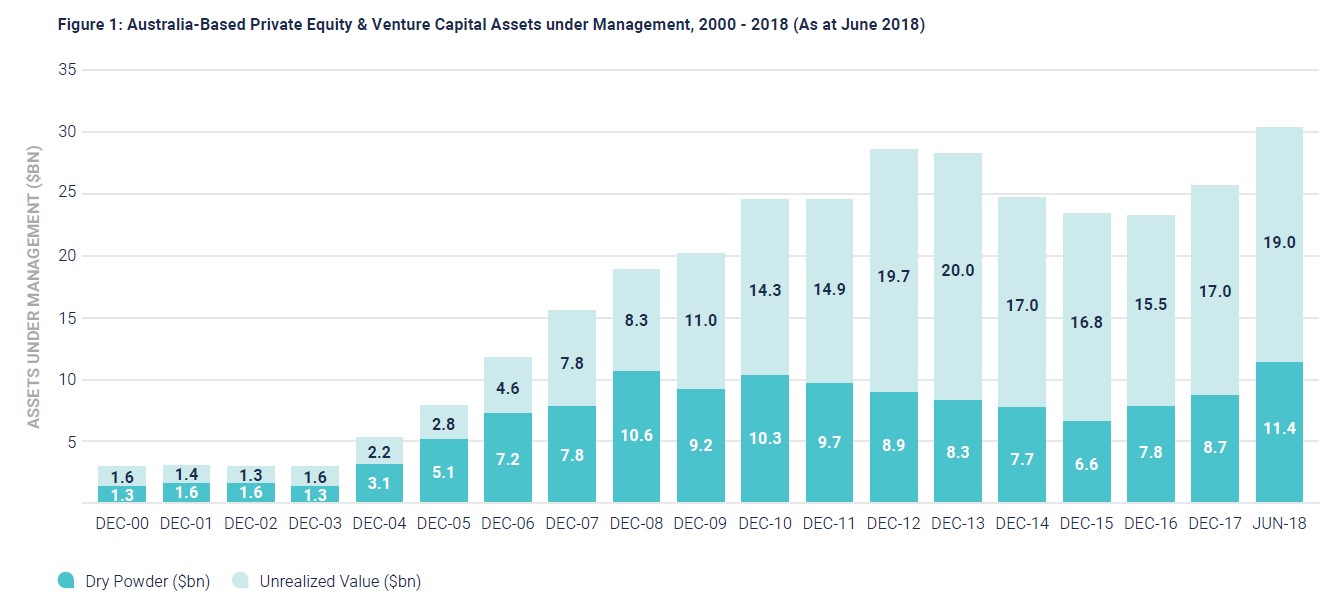

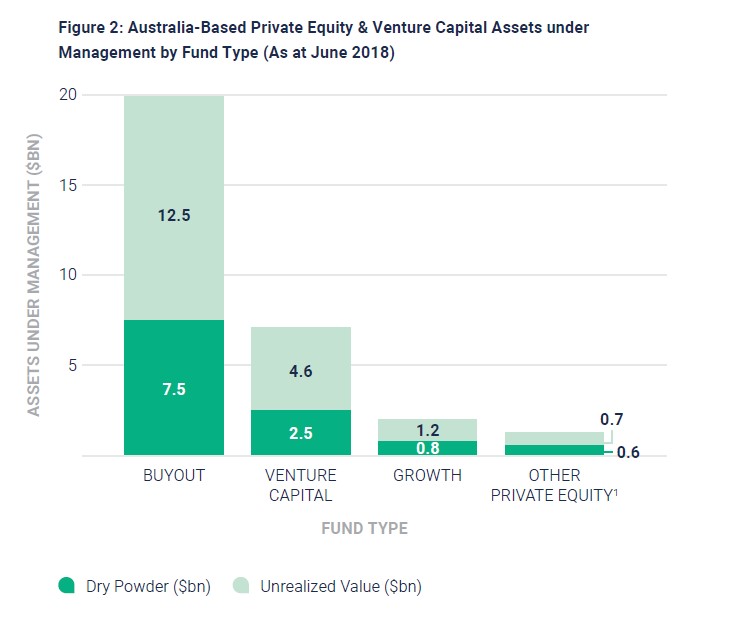

Assets Under Management: Assets By Fund Type

AUM held by PE and VC fund managers based in Australia has been rising at an increasing rate since December 2016, reaching an all-time high of $30bn as at June 2018. The 18% increase in AUM from December 2017 to June 2018 is greater than any annual change observed since 2011. The majority ($19bn) of this total is held in unrealized value, indicating that there is a significant amount of capital yet to be distributed back to investors. Furthermore, fundraising was clearly strong over 2018, as industry dry powder has similarly increased by 31% since December 2017 to stand at a healthy $11bn as at June 2018.

Australia-based buyout funds hold the greatest AUM ($20bn) as at June 2018, more than VC ($7.1bn), growth ($2.0bn) and other PE1 fund types ($1.3bn) combined. VC funds have recorded the highest AUM growth in recent years across the different fund types, with total assets more than doubling from $3.5bn in December 2016 to $7.1bn.

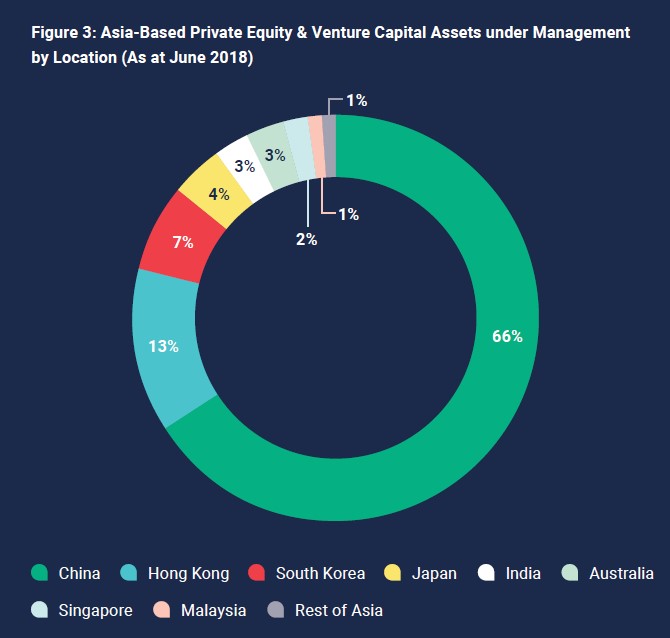

Assets Under Management: Australia’s Regional Ranking

Australia-based GPs collectively hold 2.8% of total PE & VC AUM for the Asia-Pacific region as at June 2018, down from 3.0% in December 2017. This was largely a result of China’s share increasing from 63% to 66% over the same period. Nevertheless, Australia maintains the sixth largest PE & VC industry in the Asia-Pacific region.

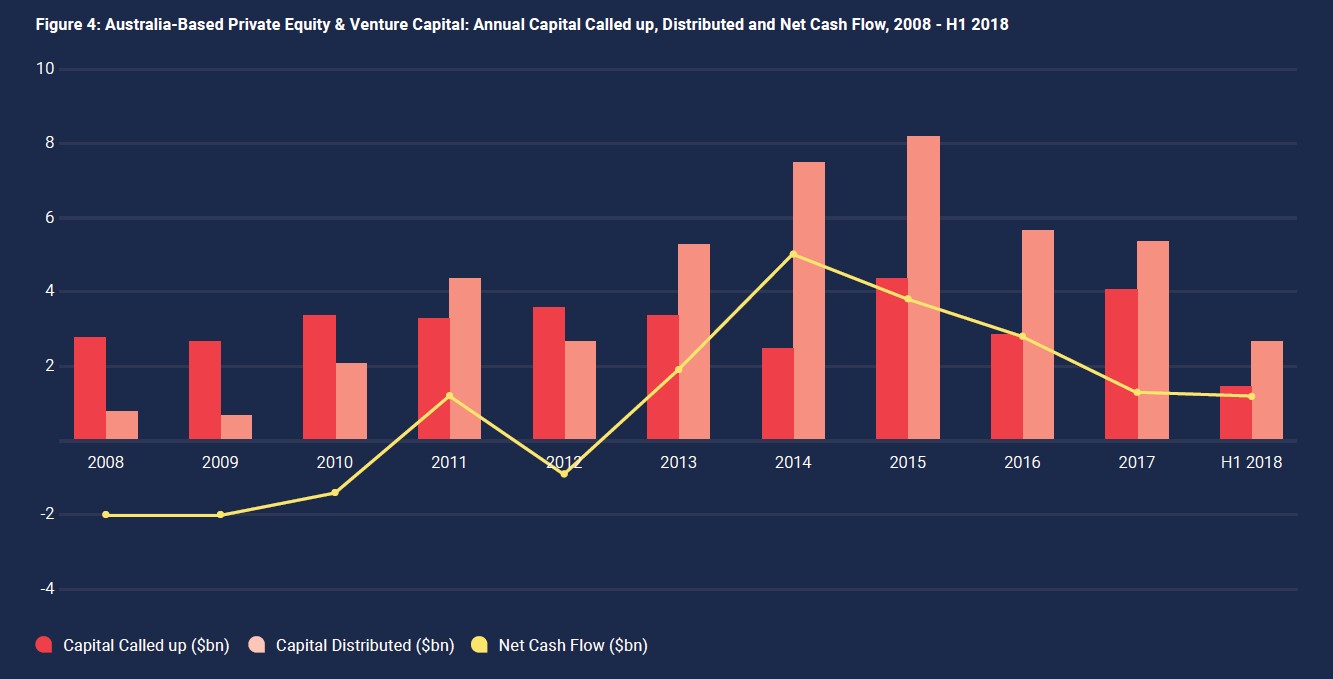

Although net distributions have been positive for Australia-based GPs since 2013, momentum has slowed. Since 2014, net distributions have decreased each year, falling from a high of $5.0bn in 2014 to $1.3bn in 2017. A net total of $1.2bn has been distributed to investors in H1 2018, however, which means distributions for full-year 2018 are likely to be higher compared to 2017.

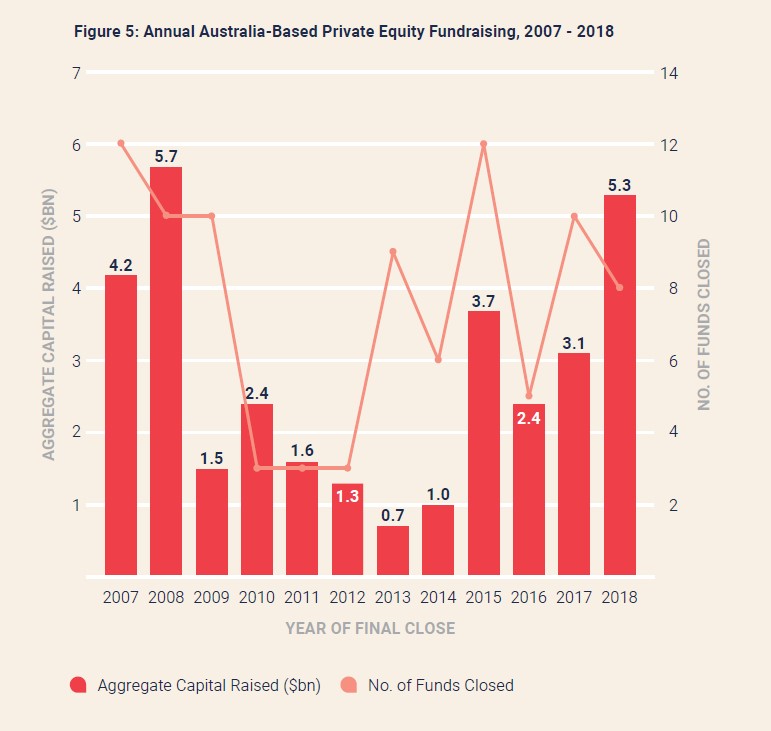

Fundraising PE & VC Fundraising Gains Traction

Australia-based PE & VC fundraising achieved record highs in 2018, with managers securing an aggregate $6.6bn in capital via 17 funds. The average size of PE funds closed was noticeably up by 117% compared to the previous year, suggesting that fund managers are raising larger vehicles to capitalize on the healthy deal pipeline in Australia.

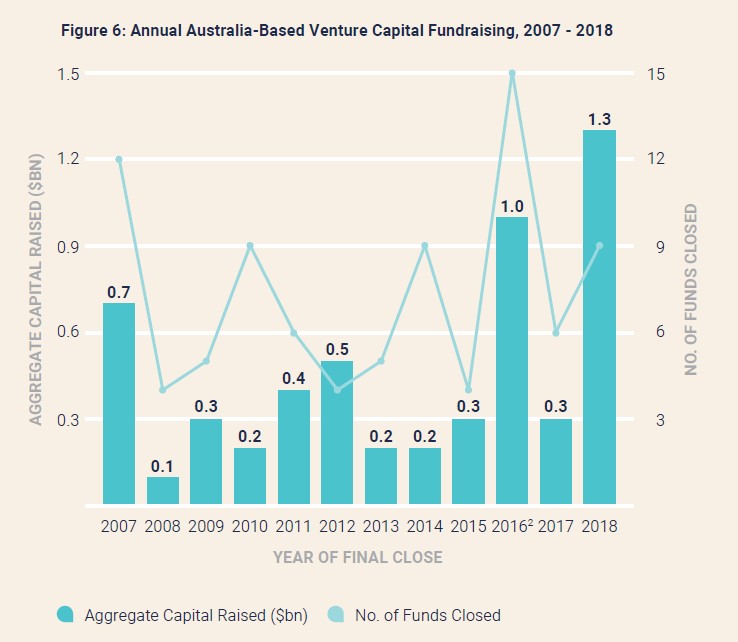

The VC fundraising market also showed signs of improvement in 2018, closing the year with $1.3bn in capital raised. This is the highest amount on record, and it is the first year where aggregate capital raised exceeded $1bn. Over recent years, growth in the start-up ecosystem and innovation policy reforms have helped to stimulate the Australian VC sector and attracted significant capital commitments from both domestic and foreign sources.

According to Preqin’s report on Australian Superannuation Funds in Alternatives, historically, institutional investors in the country have steered clear of the VC market in view of the many challenges associated with a VC allocation. However, this approach has changed in recent years, and LPs are steadily becoming more receptive towards the asset class.

Phil Morle, Partner at Main Sequence Ventures, has observed positive changes in the Australian VC landscape: average fund sizes are growing, LPs are co-investing with larger cheque sizes in earlier rounds, funds are now more focused on specific opportunities/themes and firms are building a unique capability to find growth in their respective markets.

“[As the industry expands,] funds and investors are learning how to understand each other and get aligned on the opportunity. More social proof among institutional investors and evidence that VC can provide healthy returns are helping to grow the sector.” – Phil Morle, Partner at Main Sequence Ventures

Buyout Funds Continue To Dominate

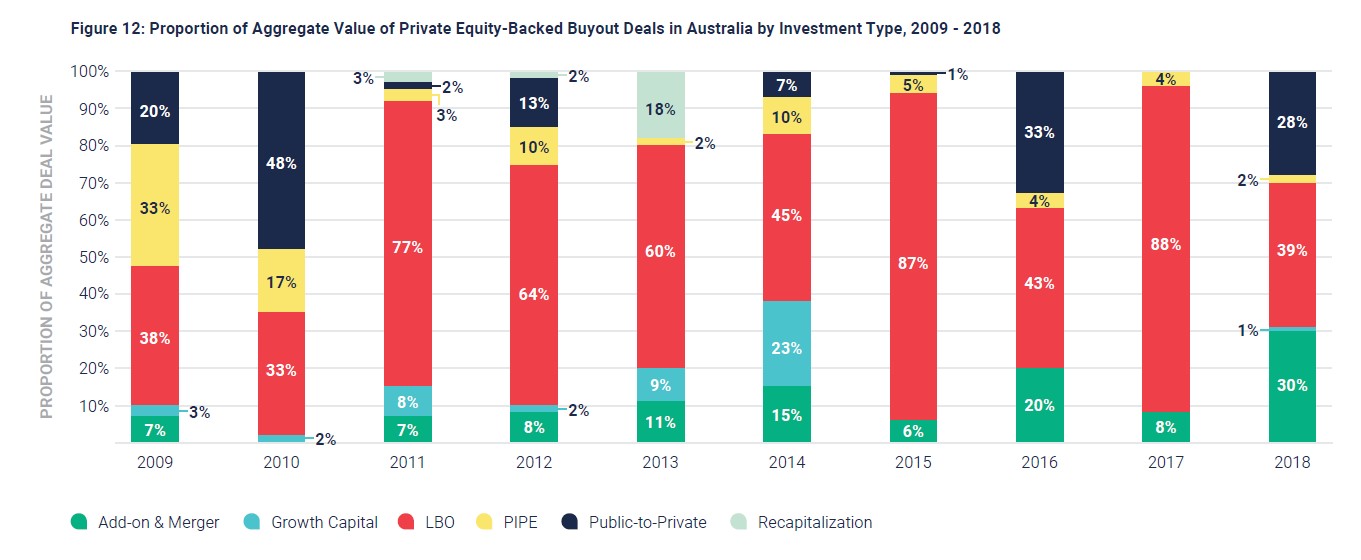

Since 2012, buyout funds have consistently emerged as the preferred strategy among PE & VC investors, and have attracted the greatest amount of cumulative capital. Even though half of Australia-based funds closed between 2012 and 2018 are focused on VC opportunities, at $14.5bn buyout funds have secured more than double the amount of capital raised by all other fund strategies combined throughout the years. Specifically, buyout funds secured approximately 79% of the total PE & VC capital raised in 2018.

The largest fund closed in 2018 was also a buyout fund, BGH Capital Fund I. The fund targets opportunities in Australia and New Zealand to support growth or operational improvement, looking at both mid-market transactions as well as larger buyout deals.

The Australian PE industry has registered ongoing interest in the ‘buy and build’ strategy, based on a recently published report by MinterEllison.4 Some PE funds are seeking businesses that are below their usual ‘equity cheque’ size but are nonetheless suitable for their thematic investment in fragmented sectors, such as childcare, travel & tourism and food & agribusiness.

Fundraising Funds In Market: New Age For VC?

There are 27 Australia-based PE & VC funds currently in market, looking to raise a total of $2.6bn, which is the lowest combined target at this point in a year since 2013. Although aggregate capital targeted was up by 15% from February 2017 to February 2018, funds in market are now seeking 57% less in total commitments as compared to this time last year, which is expected given the high levels of fundraising that have been seen across the industry in recent years. This is also the first drop observed in the number of funds in market since 2016, having declined by 27% in comparison to this time last year.

Among PE & VC funds in market in February 2018, 49% had achieved an interim close, while only 33% of those raising capital in February 2019 have at least reached their first close. Notably, the majority (67%) of funds on the road are VC vehicles, which are aiming to raise approximately half of the total capital targeted across the PE and VC sectors. This demonstrates significant growth in VC funds’ share of aggregate PE & VC commitments targeted given that, on average, they have represented approximately 20% of the total over the past seven years.

Deals & Exits Overview

Investment activity across Australia’s private capital sector experienced a significant increase in both the PE and VC markets over 2018, overturning the trend of decline that has been observed since 2016. Despite the questions over asset pricing and political uncertainty since mid-2018, the grounds for market optimism are solid: foreign investors are attracted to the low-risk environment, dry powder is sufficient, and industries are rapidly changing in tandem with developments in technology.

Many private companies, whether small start-ups or more established companies, have looked to private capital sources as opposed to the listed market to fund their next phase of growth. This has helped to keep the deal pipeline strong for both PE and VC in Australia, and in 2018 PE-backed buyouts and VC deals in the country recorded an increase in aggregate deal value of 89% and 77% respectively compared to the previous year.

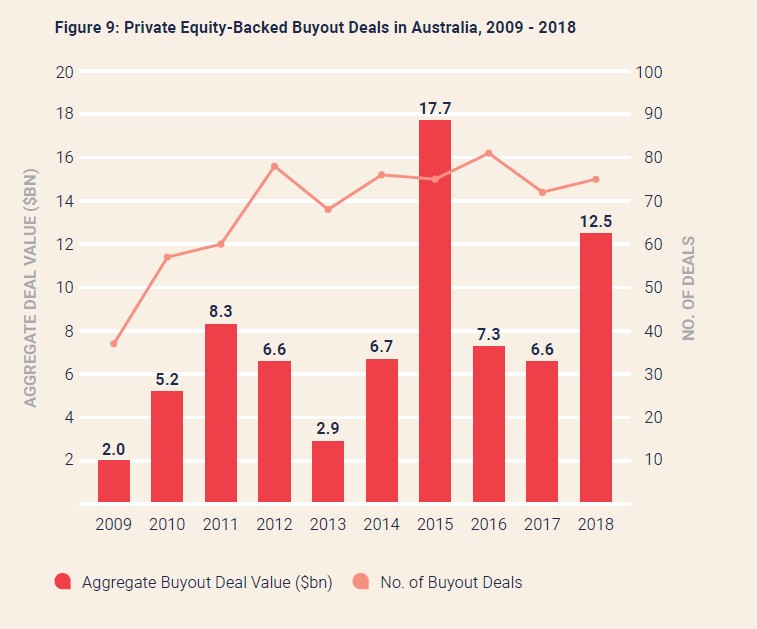

Deals & Exits Buyout Deal Activity

PE-backed buyout deals in Australia have experienced two consecutive years of decline since 2015 (which represented the highest aggregate deal value on record), when 75 deals were valued at $18bn. Since then, deal activity has bounced back to achieve the second highest deal value in 2018, with 75 deals completed for an aggregate $13bn, up 89% when compared to the previous year.

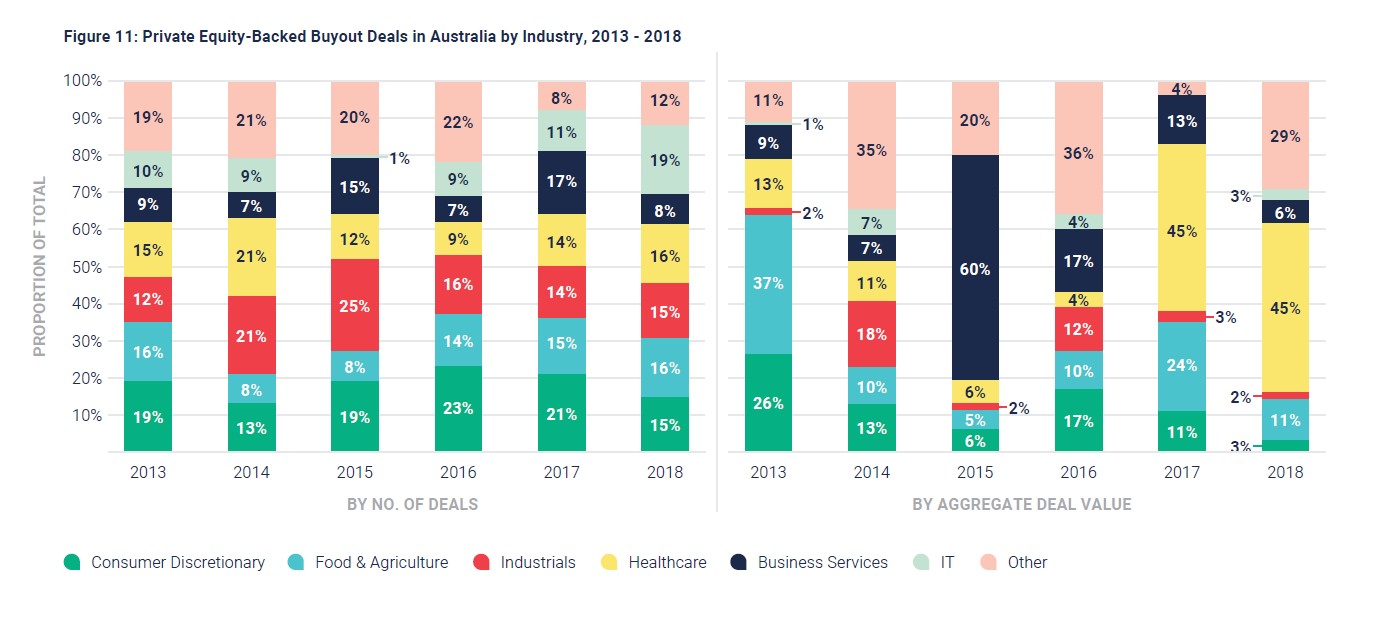

While PE-backed buyout deals were evenly spread across a number of different sectors in 2018, the IT sector appeared a particular area of interest, which marks a departure from the traditional dominance of the consumer discretionary sector (the most active between 2015 and 2017 in terms of deal flow). The IT sector recorded 14 deals in 2018, contributing 19% of the total number of PE-backed buyout deals in Australia.

Notably, the healthcare sector continued to dominate in terms of the aggregate value of buyout deals in Australia, with a 45% market share in both 2017 and 2018. This was mainly on the back of some mega deals, namely investments in Sirtex Medical Limited and I-MED Network Ltd., which fetched a total of $3.1bn and contributed 57% to the total aggregate value of healthcare deals in Australia in 2018. With a growing ageing population, private health insurance coverage in Australia is expanding, creating a favourable environment for healthcare sector investments. The increasing demand for the sector is expected to continue in line with the trend observed over the past two years.

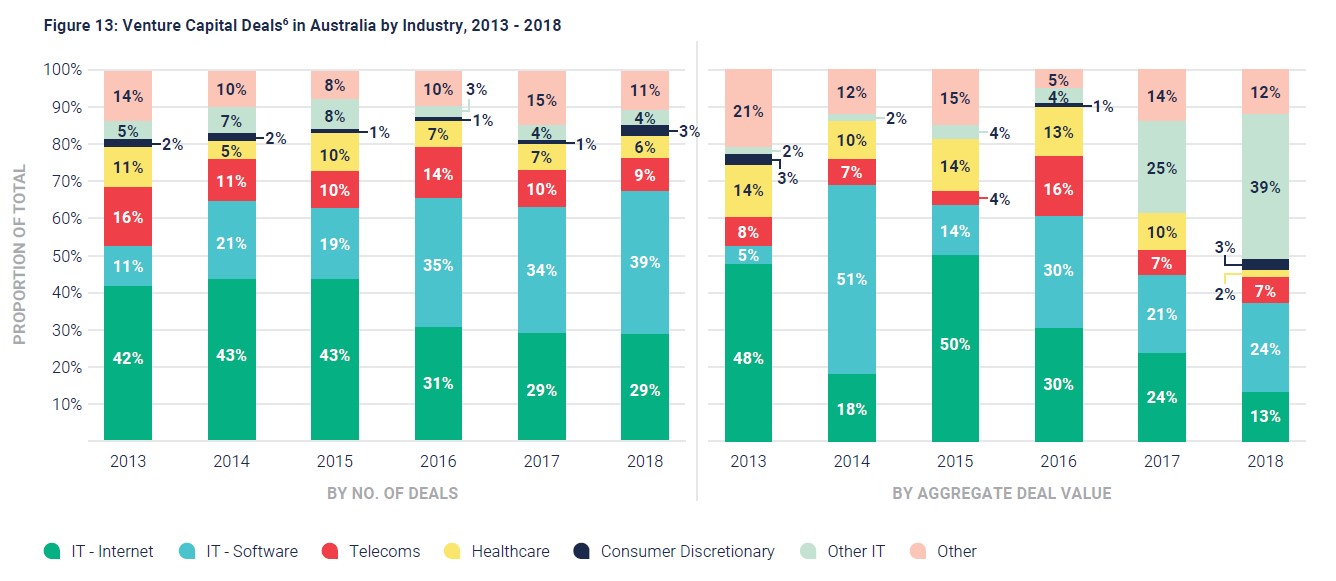

Deals & Exits VC Deal Activity

Since 2013, a total of 796 VC deals have been completed for Australian start-up companies, for an aggregate value of $4.5bn. Historically, the internet sector has been the major investment field in terms of the number of deals completed, followed by the software and telecoms sectors; together these sectors contributed 56% of total deal value since 2013. In contrast, the internet sector contributed only 13% of aggregate VC deal value in 2018, the lowest total as seen in Figure 13. Notably, the software sector recorded a five-percentage-point increment from 2017 in terms of number of deals (from 34% in 2017 to 39% in 2018), and its share of aggregate deal value increased from 21% in 2017 to 24% in 2018.

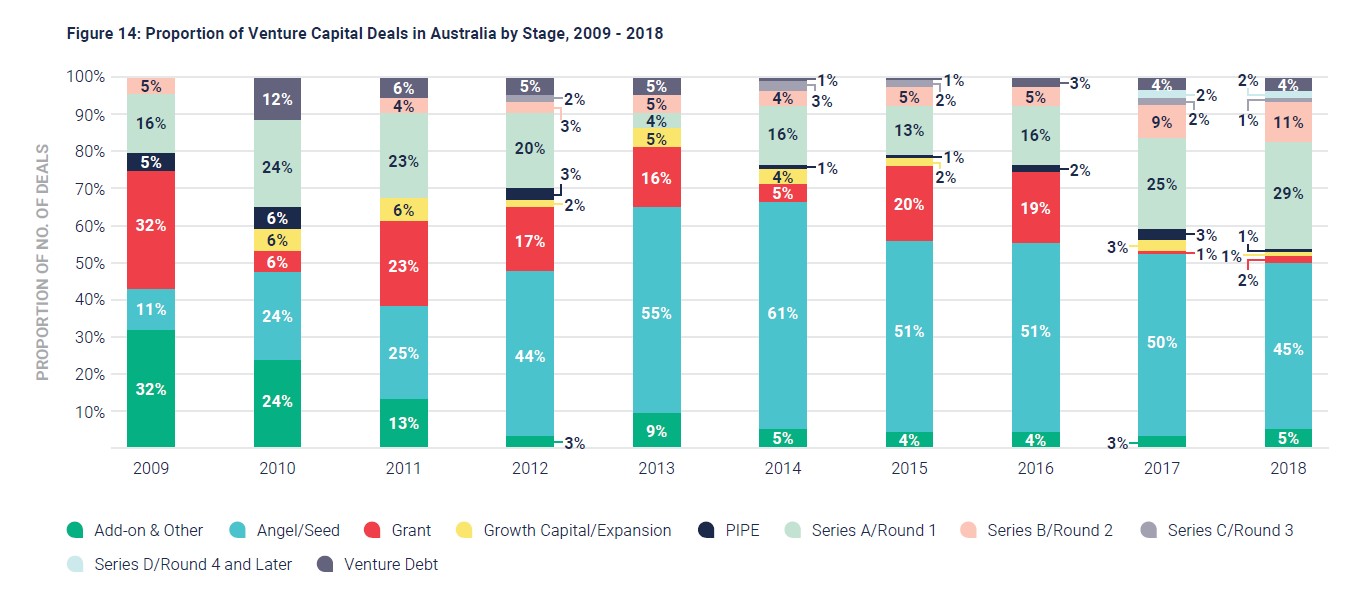

Between 2013 and 2017, deals at the angel/seed stage accounted for more than half of all Australian VC financings. However, this figure decreased to 45% in 2018 as investors looked to invest in later stages; deals at the Series A stage have been on an upwards trend since 2015, with 38 deals completed in 2018 (29% of the total) worth an aggregate $436mn.

One prominent deal in 2018 was Judo Capital’s Series A funding. The financial services firm raised $140mn from Abu Dhabi Capital Group, OPTrust Private Market Group, Credit Suisse and Myer Family Investments.

Deals & Exits VC Deal Activity

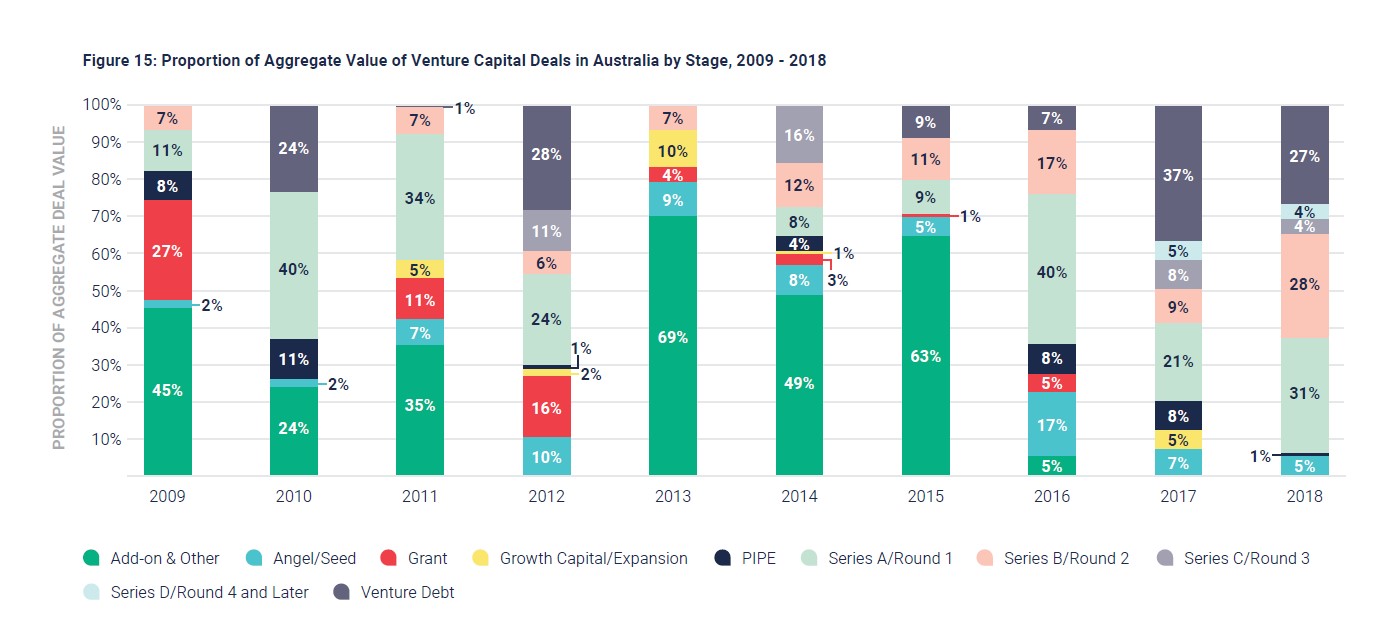

At $287mn, the aggregate value of Series B stage deals was up from $79mn in 2017, representing 28% of the aggregate value of VC deals in Australia in 2018. Notably, early- and expansion-stage deals from Series A onwards accounted for 67% of aggregate deal value in 2018, up 24 percentage points compared to 2017.

Deals & Exits Exit Activity

The aggregate value of PE-backed buyout exits in Australia recovered modestly in 2018 to total $9.2bn from a low of $8.1bn in 2017, stemming the consecutive drop in yearly aggregate exit value since 2014. In terms of exit strategy, trade sales constituted a record 73% of total buyout exits in 2018, the largest proportion observed in Figure 17. On the other hand, the number of IPOs & private placements as a proportion of total buyout exits fell substantially from 20% in 2017 to 6% in 2018; the IPO window remained largely closed due to jittery markets and an uncertain global macroeconomic outlook.

To increase portfolio liquidity, GPs also looked to other exit strategies, which accounts for some of the growth in the number of secondaries exits: exits via secondary transactions as a proportion of total exits have increased steadily from 13% in 2016 to 17% in 2017, reaching 21% in 2018.

Article by Preqin