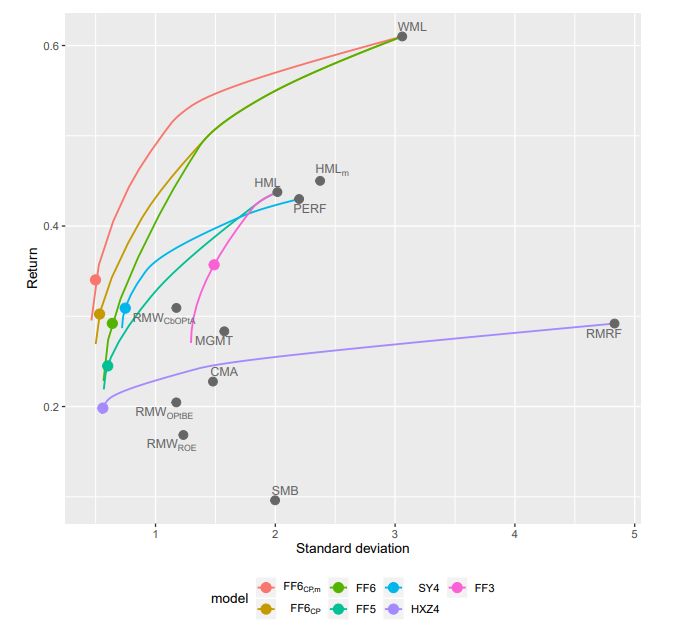

I compare commonly employed factor models across 47 non-U.S. developed and emerging market countries by ranking them based on their maximum Sharpe ratios. Consistent with the U.S. evidence presented in Barillas, Kan, Robotti, and Shanken (2019), I find that the factor models of Fama and French (2015, 2018), Hou, Xue, and Zhang (2015), and Stambaugh and Yuan (2017) are dominated by a six-factor model that includes cash-based profitability and momentum factors, as well as a value factor that is updated monthly. The result is robust in out-of-sample tests, across subperiods, across global regions, and to methodological changes. The main problem for the dominated factors models is that they do not explain the monthly updated value factor. Hence, I conclude that the value factor is not redundant.

Q4 2019 hedge fund letters, conferences and more

Read the full paper here by Matthias X. Hanauer, SSRN