We’ve all been rather trained to be very cautious around the VIX, you know – with infographics like this one showing you’ll likely lose all your money and VIXmageddon last February and all. But those who trade the VIX don’t just buy the VIX and hope for the best, or sell it and pray there’s no spike.

Q2 hedge fund letters, conference, scoops etc

No, professional VIX traders are typically doing a relative value type arbitrage trade where they will buy and sell volatility at the same time. How? Well, you can buy the front month contract VIX and sell the next month contract, or buy the VIX and buy the S&P at the same time – where a sell off in the VIX due to an S&P rally would be offset by gains in the long S&P position (assuming you are close on the ratio between the two).

This all sounds great, but a client looking at some Vol Arb strategies last week had the question – is it possible that one side of these hedged trades spikes while the other side does nothing? The quick answer is likely no, as any difference would be arbitraged away. But does a scenario exist where it could happen…. That was a thought experiment worth exploring, and we took to Twitter to question the VIX followers out there.

VIX people….

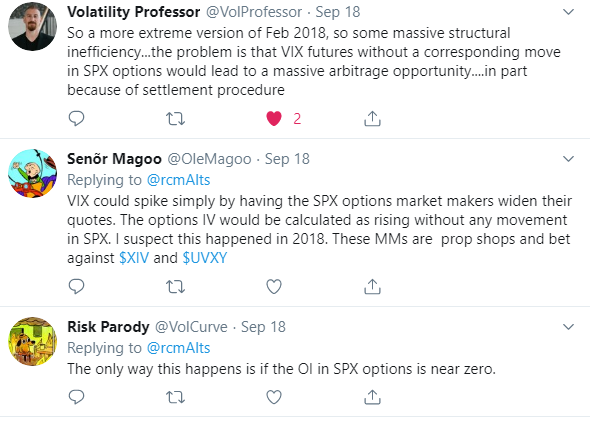

Can you envision a scenario where VIX futures spike meaningfully (>50%) and there is no corresponding move in the S&P?

In theory it can’t happen because it would be arbitraged away, but we’re talking cash settled futures vs an index not directly tradable?

— RCM Alternatives (@rcmAlts) 18 September 2019

And our Twitterverse delivered, via @VolProfessor, @OleMagoo, and @VolCurve to name a few:

So there’s some theoretical possibilities of that happening, but any such difference are almost certainly bound be short lived (hours?) because of arbitrage opportunities. Assume a scenario of VIX up 75% and S&P only down 5% – so VIX futures are at…say 52 and the VIX index at say 40. You would sell the VIX futures and buy the SPX options representing the VIX calculation to arb the difference.

While the futures cash settle, they don’t just settle at the level they’ve reached. They settle to a VIX index value. So, if the difference remained at settlement and the VIX index never rose (because the S&P never fell for one of the many possible scenarios outlined above), the settlement of the VIX futures would be adjusted lower toth the VIX price (40) from e final price of the contact (52). Linking the settlement to the index insures that any such arb (even if taken by nobody) would even itself out at settlement.

Which is all to say, yes, it may be theoretically possible, but as one trader we talked to put it:

“There’s a better chance of an asteroid exploding over the earth and showering down golden babe ruth baseball cards wrapped in seaweed.”

For more on the VIX, download our VIX whitepaper here.

Article by RCM Alternatives