The AIMA Hedge Fund Confidence Index (HFCI) is a new global index that measures the level of confidence hedge funds have in the economic prospects of their business over the next 12 months. A product of AIMA, Simmons & Simmons and Seward & Kissel, the HFCI is calculated during the final two weeks of each quarter and published at the start of the subsequent quarter.

Selecting the appropriate level of confidence, respondents are asked to choose from a range of -50 to +50, where +50 indicates the highest possible level of economic confidence for the firm over the next 12 months.

Q4 2022 hedge fund letters, conferences and more

When considering how best to measure their level of economic confidence, hedge fund respondents are asked to consider the following factors: their firm’s ability to raise capital, their firm’s ability to generate revenue and manage costs, and the overall performance of their fund(s).

Hedge Fund Confidence Index Q4 2022 Results

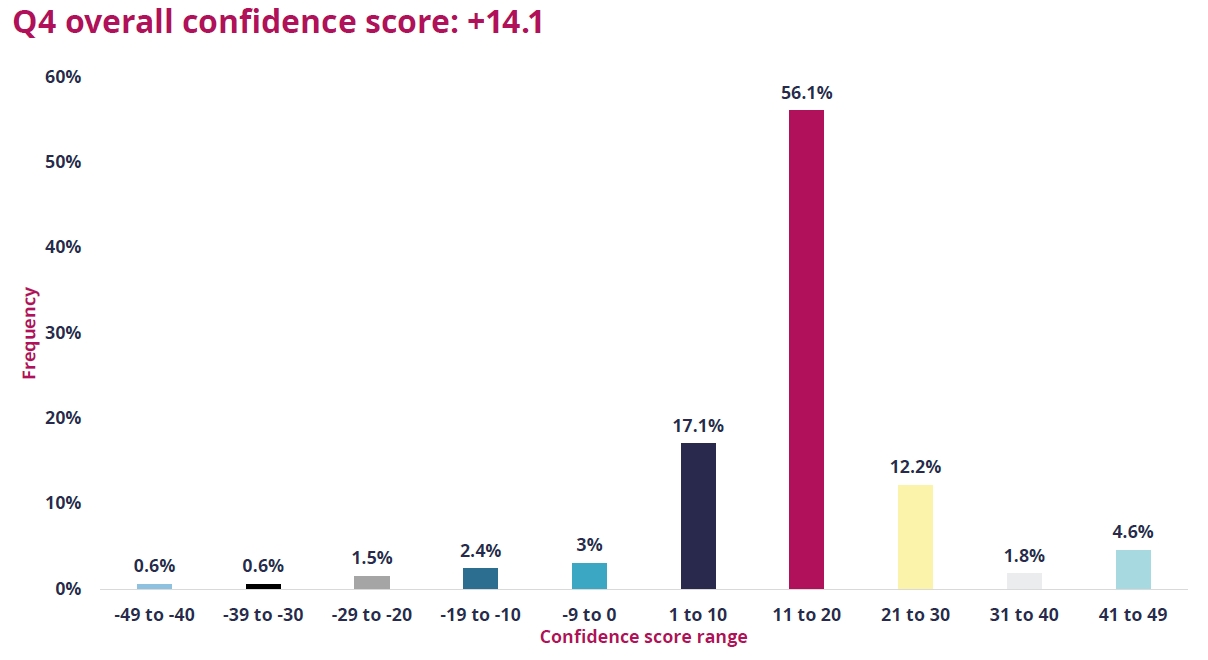

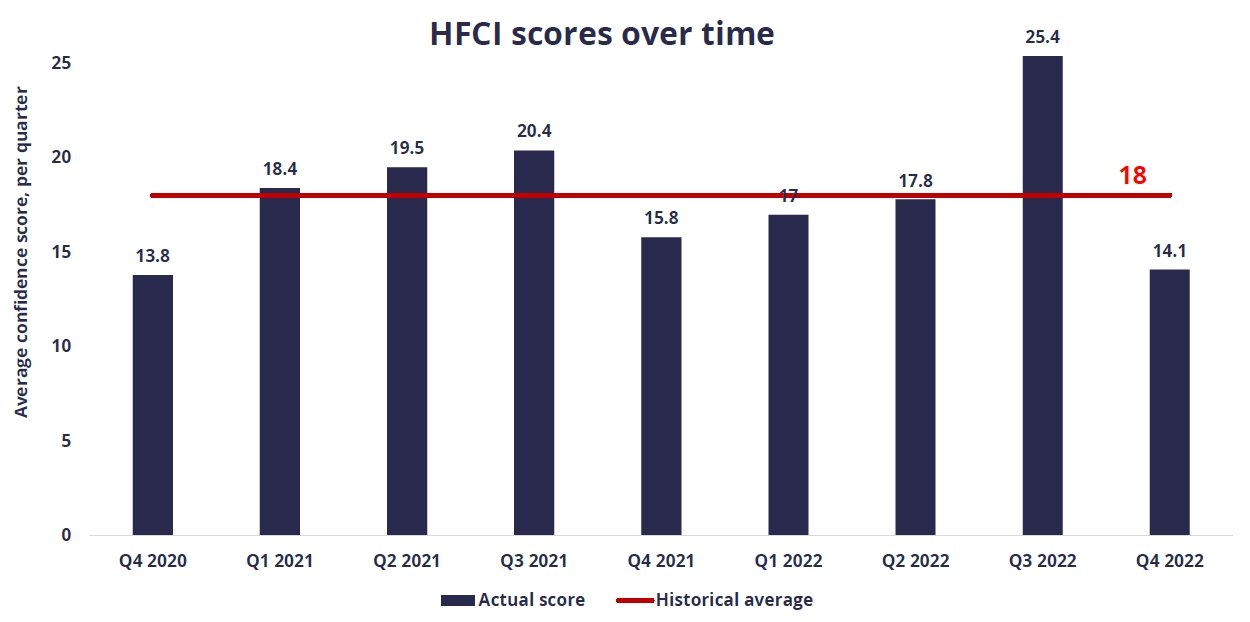

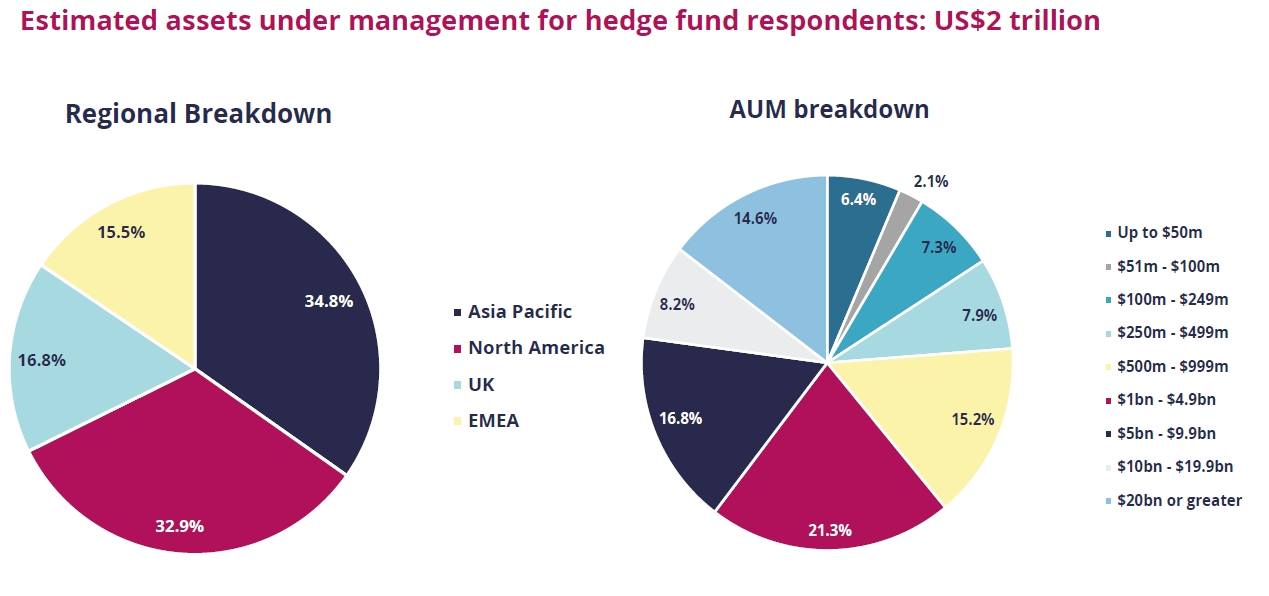

Based on a sample of 328 hedge funds (accounting for approx. US$2 trillion in assets) that participated in the index, the average measure of confidence (in the economic prospects of their business over the coming 12 months) is +14.1, representing a two year low in confidence levels reported by hedge funds, and several points below the historic average (See HFCI confidence score over time).

The downturn in confidence from the previous quarter is ubiquitous across all regions, fund sizes and strategies but upon closer examination of the data the overall score is most influenced by a clear divergence in confidence across strategies that post significantly lower scores related to the prior quarter.

For a full breakdown of confidence scores by region and fund size, see the charts that follow.

Overall, how would you score your confidence in the economic prospects of your business over the next 12 months, compared to the previous 12 months, on a scale of +50 to -50? (Hedge fund managers).

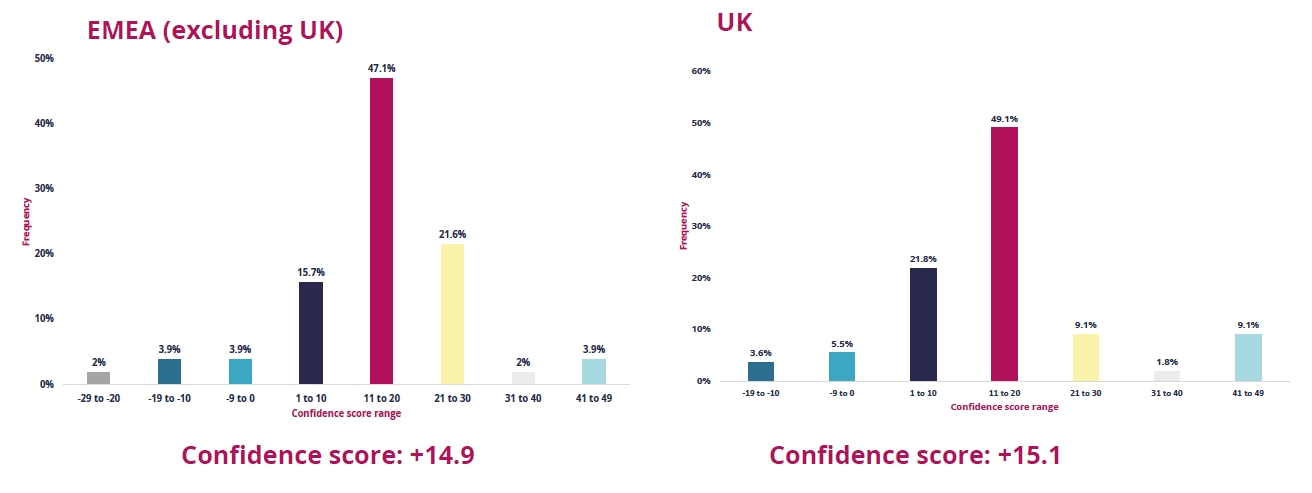

Breakdown By Hedge Fund Location

On a geographic basis, the EMEA confidence score is influenced by Middle Eastern fund managers, who were the most confident of all the regional groups. Beyond the growth of several financial hubs across the Middle East as attractive domiciles for alternative investment funds, the score is driven by a respondent pool dominated by multi-billion-dollar global macro funds who are among the most confident demographics in terms of size and strategy.

Elsewhere, fund managers in the UK remain stubbornly optimistic as they were all year. UK respondents are twice as likely to be larger managers who are historically more confident than their smaller peers. Similar to the Middle East, the UK respondent pool also includes a relatively large percentage of global macro funds. Moreover, the UK has fewer long-short equity funds – among the least confident strategies this quarter – compared to other regions.

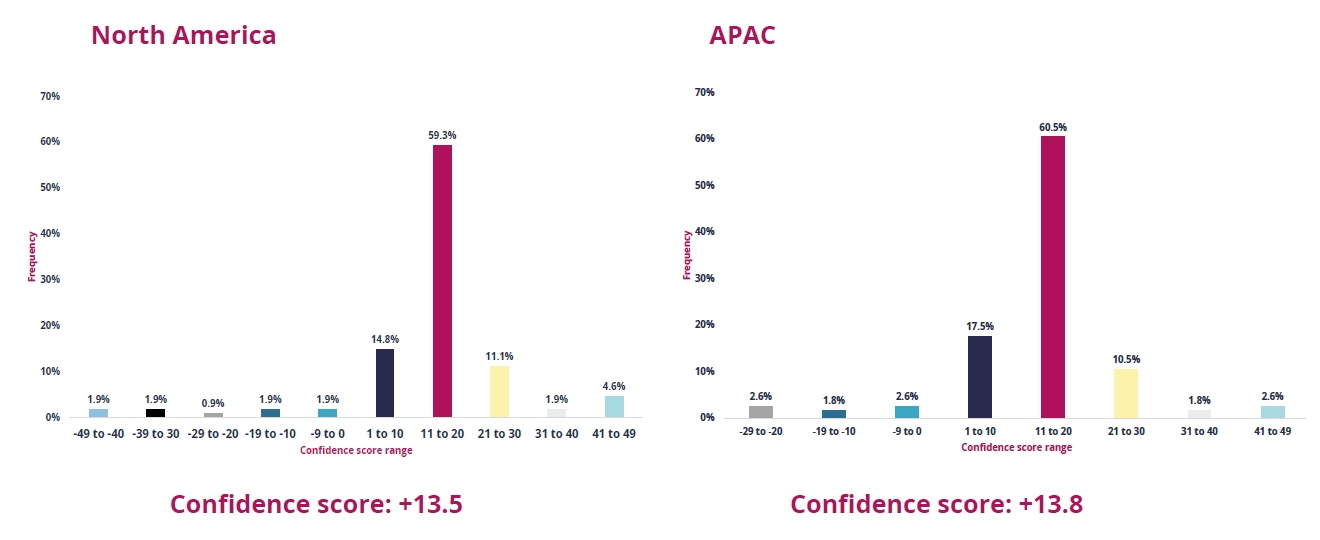

North American managers – the vast majority of which are from the US – maintained modest optimism throughout 2022 and ended the year as the least confident region. Like the previous quarter, the drag on North America’s score can partly be attributed to a handful of digital assets fund managers, who posted record-low confidence.

Additionally, almost half of North American respondents were long-short equity managers, while a further one in five represented fund-of-funds which were even more gloomy, albeit less well represented in the overall demographic breakdown. Although North America had a similar split as the UK between those managing greater than or less than $1 billion, it also had a relatively large pool of those managing up to $50 million who posted a lower-than-average confidence score across the AUM bands.

Turning to APAC, the region remained fairly consistent in its outlook throughout 2022 although the Q4 downturn only narrowly beat its lowest-ever score, recorded in Q4 2020. The region had a slightly greater proportion of smaller managers and also a relatively high percentage of respondents representing the smallest cohort of managers, both of which served to depress the average confidence number.

Commentary: Gloomy Prognosis For The Global Economy Pushes Average Confidence Levels To A Two-Year Low

The cause of the 10-point drop-off in the overall average confidence since Q3 2022 is multifaceted but will undoubtedly be partly due to the combined challenges of the deluge of radical regulatory proposals from the US SEC and a chaotic macroeconomic landscape which shows no signs of settling as we begin the new year.

Rising interest rates, higher inflation levels, the very real threat of recession and broader market uncertainty underpin an increasingly downbeat economic outlook. This comes after a dismal year in which global equities have lost over 20% of their value while bonds have also tumbled.

Subsequently, 60/40 portfolios (for a long time regarded as being the optimum investment strategy for pension plans and other institutional investors) posted one of its biggest annual negative returns, having nursed losses of close to 20%.

By comparison the average hedge fund is expected to end the year down between 4%-6%1 amid a mixed bag of performance with some hedge fund strategies (global macro, CTA/managed futures, and multi-strategy) delivering some very strong returns for their investors while others (long-short equity, long-only to name but two) enduring a very challenging year. Capital outflows are coming under pressure throughout the past quarter across all asset classes including hedge funds.

Confidence levels are further undermined by the increased set of regulatory headwinds that hedge funds must contend with. In the US, not a week seems to go by without another proposal being put forward by the SEC amidst the most serious overhaul of existing market practices for the private funds’ industry.

Elsewhere work is ramping up across Europe, the UK and APAC as policymakers prepare to build on wave of new industry regulations that began in 2022 – all of which will impact how firms manage their business.

That said, the terms of several of the most potentially damaging regulatory proposals, such as the SEC’s draft reforms to the Dealer Rule, are expected to be confirmed in the first half of the year and, regardless of the final terms, this will bring greater certainty to the market landscape.

Moreover, some market signals indicate that inflation is due to peak, with some central banks indicating a lower ceiling to interest rates than might have been predicted in 2022. Greater clarity in these key areas may offer fund managers some reassurance in the ability to map out a future for their businesses even if other macro-headwinds persist.

Breakdown Of Respondents

Hedge Fund Confidence Index Over Time

Tom Kehoe, Global Head of Research and Communications at AIMA, said:

“The past 12 months have been among the most challenging for businesses in many years. Confidence levels among hedge funds are further curtailed by the gloomy prognosis for the global economy as well as additional industry headwinds in the shape of increased regulatory action.

Reasons for hedge funds to be optimistic over the coming year include their ability to best manage risk amid the volatility being witnessed across global markets and an expectation of greater clarity around many of the regulatory proposals unveiled last year.”

Debbie Franzese, Partner Investment Management at Seward & Kissel, said:

“Given the current recessionary environment that we’re in and the headwinds that the economy and private fund industry is facing going into the new year, it’s unsurprising that North American-based hedge fund managers are the least confident they’ve been recently regarding the prospects of their business.

The industry continues to experience increased regulatory focus from the SEC, this coupled with fundraising and performance challenges, increasing interest rates, inflation, and other macroeconomic considerations, can make for a perfect storm.”

Article by AIMA