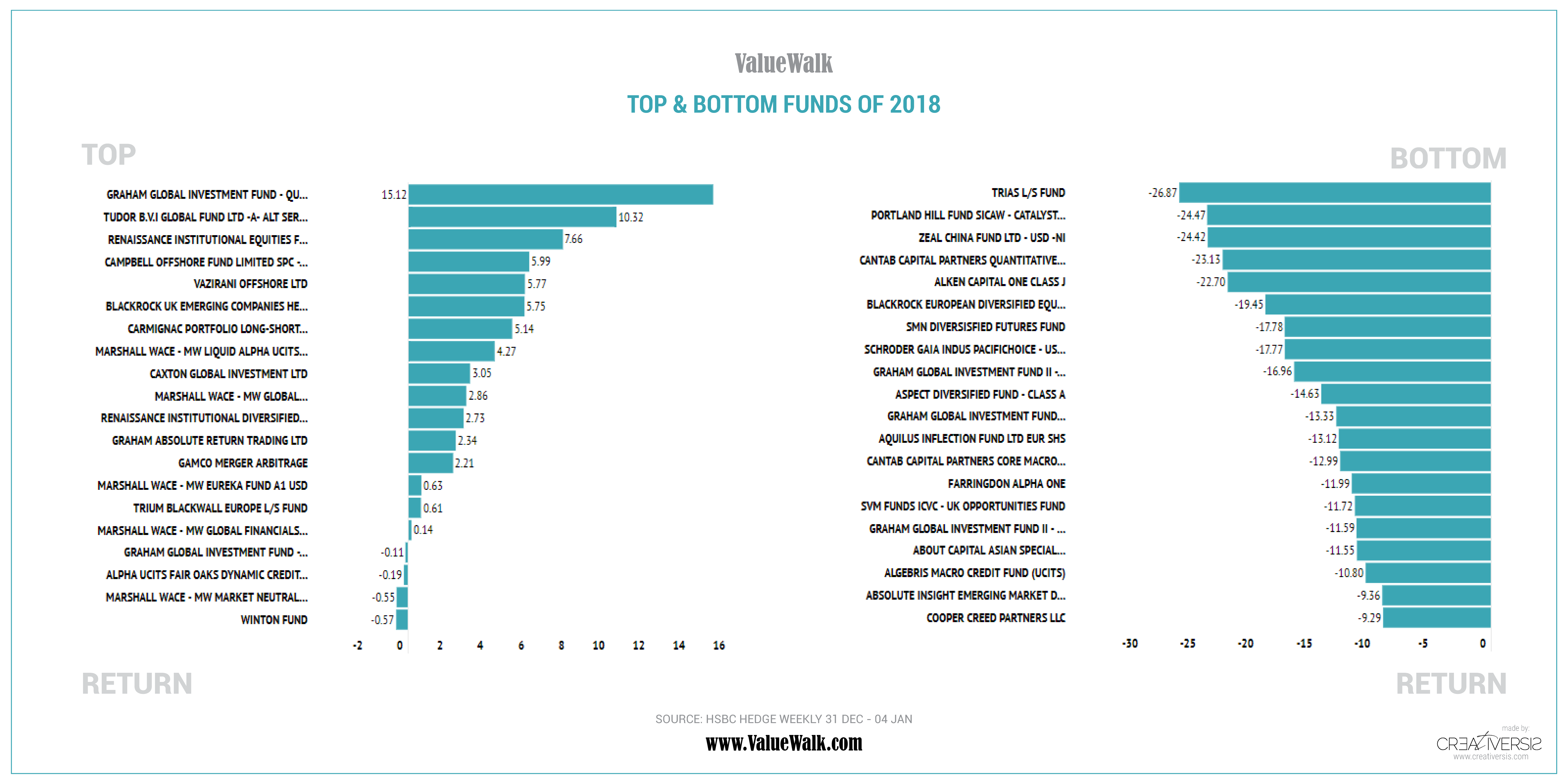

As 2018 officially closes, and year-end returns trickle into HSBC’s Hedge Weekly performance report, an interesting phenomenon is on display. Systematic hedge funds, many of whom have traditionally adhered to a somewhat similar trend following strategy, are posting a returns dispersion. Q3 hedge fund letters, conference, scoops etc Many of the top performing hedge funds in 2018 can be found in the same category as some of the worst performers. Systematic, algorithmic-driven hedge funds are putting on display a wide range of returns during a time of wild beta market price movements. While the overall HSBC category was showing a…

Algo Hedge Funds Among Best But Also Worst 2018 Performers As Volatility Reigns

Mark Melin

Mark Melin is an alternative investment practitioner whose specialty is recognizing the impact of beta market environment on a technical trading strategy. A portfolio and industry consultant, wrote or edited three books including High Performance Managed Futures (Wiley 2010) and The Chicago Board of Trade’s Handbook of Futures and Options (McGraw-Hill 2008) and taught a course at Northwestern University's executive education program.