“As an investor, you make the most money when you do things that other people aren’t willing to do, like taking risks others shun. Attractive investment opportunities arise when you spot some security or some part of the market being ignored and you come to the conclusion that it’s languishing cheap. But today, I don’t think anything is being ignored. Investors are willing to do almost everything.” – Howard Marks

Q1 hedge fund letters, conference, scoops etc

I attended an advisor summit in Chicago this past week. On stage was a good friend from S&P Dow Jones Indices. He referenced an article S&P published last fall about poor quality in the popular “leveraged loan” segment of the corporate bond market. Dull, I know, but hang in with me for a short few paragraphs, I promise this week’s missive gets better.

Think of the leveraged loan market in a similar way you might have thought about the sub-prime mortgage market in 2007-2008. “No doc” mortgages provided liquidity that accelerated the boom in real estate construction, real estate prices and the economy. That is, until the system was overloaded with supply, borrowers couldn’t pay, defaults mounted and, in the end, sub-prime junk was really just junk after all. All looked swell until the gig was up.

Sub-prime was a boring topic until it became exciting for the few and painful for the many. If you watched “The Big Short” (and I hope you did), today’s piece is preview to “The Big Short, Part II.” Coming in 2022 to a theater near you. And the opportunity it will present will be epic.

Today, we’ll look at what I believe are two of the most important indicators you can follow to help you manage the risk and potentially profit from the defaults that will present in the next recession. Timing, of course, is critical and I’m trusting that what I’ve followed for nearly 27 years can help you and me identify the turning point. To which, I believe the HY price trend holds the key.

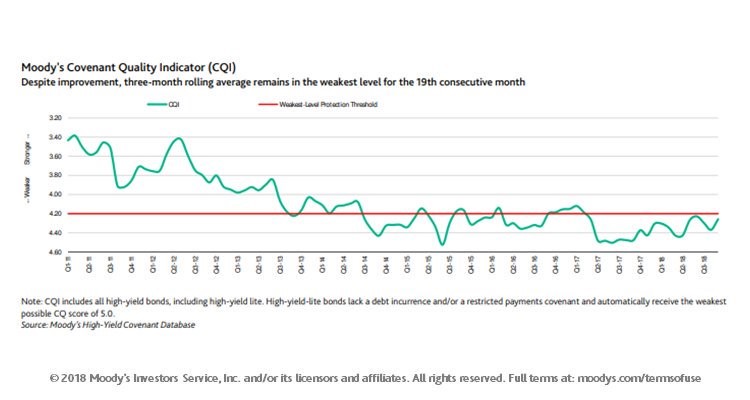

Back to my friend at the conference. So what he and his “high character” team at S&P are signaling in their article is to be aware of the poor level of protection we investors are getting in leveraged loan funds and politely saying risk is off the charts. What I’m impressed with is that S&P wrote the piece despite the fact that they and their client make money when investors buy their client’s ETF that seeks to track the S&P Dow Jones Senior Loan Index. Hat tip to S&P, to my friend, his team and their outstanding character.

First, let me give you some footing that’s important to understand. The leveraged loan market is generally where companies whose credit is so weak they can’t access the high-yield bond market to obtain financing. Read that last line again. This is the sub-prime of the corporate bond market. The popularity of leveraged loan funds and ETFs was enabled by zero interest rate policy. Seeking to improve returns on their savings, investors moved their money into riskier asset classes. That liquidity, like sub-prime in the mid-2000’s, gives borrowers to hold the upper hand. The problem is one of size, scale and poor quality. Let’s take a closer look.

The Big Short, Part II

Think of covenants as the terms of an IOU. If your brother borrows money from you, what do you get if he doesn’t pay you back? If he borrowed from you to buy a house, you may have had him sign a loan agreement requiring him to post his house as collateral. He doesn’t pay, you get his house (and you’ll probably lose your relationship with your brother but that’s another story… so don’t lend him money :-)). A lender (a bank, for example, or investor) wants collateral in case the borrower defaults and does not pay. And there might be other terms (restrictions) written in the agreement, such as, the terms of the loan or debt agreement may restrict a corporation from borrowing more without your permission, or restrict you in terms of what you can use the money for. “Covenant Light” means the lender gets little protection. The borrower dictates the terms. Well, when there is so much liquidity in the system seeking returns, investors are “… willing to do almost everything,” as Howard Marks points out.

Moody’s evaluates and rates covenant protection on a scale of 1 to 5 with 5 being the least protection for lenders and 1 being the best. As you can see next, the news is not good.

When you invest in the corporate bond, leveraged loan or high yield bond fund or ETF, you are buying a large portfolio of loans issued to corporations. “The Big Short, Part II” opportunity is enabled because of the size of the market, the poor quality of the loans and the type of unsophisticated nature of the underlying investor. Like sub-prime before it, when liquidity dries up, defaults will increase and recovery rates will be very low.

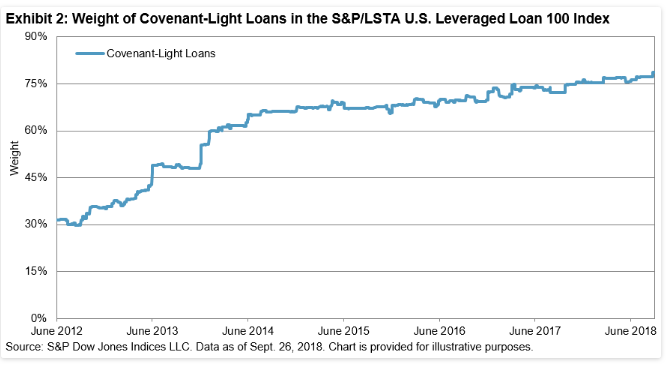

In the S&P report, they said, “With the rapid growth of the loan market, an increasing number of loans are issued with fewer restrictions and protective covenants for the benefit of the lender.” Next is a look showing the percentage of covenant-light loans in the index grew from 31% in June 2012 to 79% in September 2018. It hit 87% in January.

Think about this for a second. Nearly one-third of the companies in the Russell 2000 Index are not making a profit. They are living on debt made available by the trillions that have flowed into leveraged loan, high yield bond and investment grade bond funds and ETFs.

This is sub-prime on steroids. My colleague, John Mauldin, and I thought the potential risk of sub-prime in 2007 to be $400 billion. The most commonly cited estimate of the leveraged loan market uses a figure of around $1.3 trillion. And that’s before we take a look at other debt instruments like high yield and even higher rated corporate bonds are considered. Let’s look at that next.

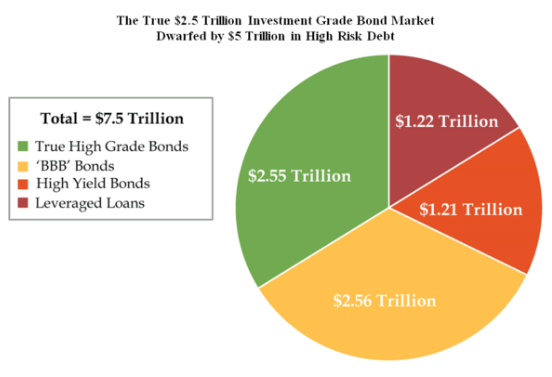

The Size of the Risk is $5 Trillion

BBB-rated bonds are the high-risk sleeve of the investment-grade corporate bond market. BBB-rated bonds sit just one rung from a HY junk bond status. Investment grade bonds are the safer corporate bonds but here too risk has snuck up on us. The overall size of the investment grade segment of the market is $5 trillion. A little more than half of that, or $2.56 trillion are corporate bonds rated BBB, according to Morgan Stanley.

When you consider the $1.22 trillion in leveraged loans, the $1.21 trillion in high yield junk bonds and the $2.56 trillion in BBB-rated corporate bonds, the $2.55 trillion in High Grade/Quality bonds is “dwarfed” by the $5 trillion in high risk debt.

Source: Bloomberg

Moody’s estimated the post-default trading prices for senior unsecured bonds was 53.9% in 2017, up sharply from 31.5% in 2016. The high yield bond market declined 45% in the last crisis. Given the low covenant quality today, I estimate the next recession will see that $5 trillion in debt off 60% from its highs. The sub-prime problem turned out to be an approximately $3 trillion global blow-up that is now defined as the “Great Recession.” I believe the next recession and default wave that concludes by recession-end will match or exceed the sub-prime problem when you factor in the derivatives that are tied to the corporate credit markets.

In the movie “The Big Short,” a few smart people simply opened their eyes and looked. I’m saying we sit at a comparable level of risk or maybe greater since we’ve tripled down on debt since then and central bankers globally are at zero to negative rates.

The game changes when liquidity dries up. Bloomberg concluded their article saying, “The reality is precious few retail investors conceive of the ticking time bombs populating what they believe to be the safest slice of their portfolio pie.” With this said, there is something you can do.

Here is what you can do

Set your sights on and continue to monitor the right indicators. I believe they will help us stay on the correct side of the trade. There are many, but I believe there are two that are most important. (Side bar: I’ll continue to post them in Trade Signals.)

- High Yield Holds the Key

Here is how to read the chart below:

- Plotted is a smoothed 50-day moving average price trend line (green line).

- Uptrend signals occur when the price line (the black/red line) rises above the green line. Downtrend signals occur when the price falls below the green line. In this chart, I am using a large popular high yield bond mutual fund.

- Look closely at the 2008 periods (left side of chart). A move to Treasury bills did two things for you:

- Avoid significant loss.

- Put you in a position to take advantage of the opportunity the recession and default wave created. At the low, due to the 45% crash in HY prices, yields jumped to 22%.

I can take you back to 1999 and even farther back to 1990. I’ve been trading the trends in the high yield space since then. My two cents is that the price trend in the HY market holds the key. The HY market is a good lead indicator for the equity market and both are good lead indicators for the economy. The fireworks will occur in the next recession. Thus, I believe the HY market holds the key. Keep it on your radar.

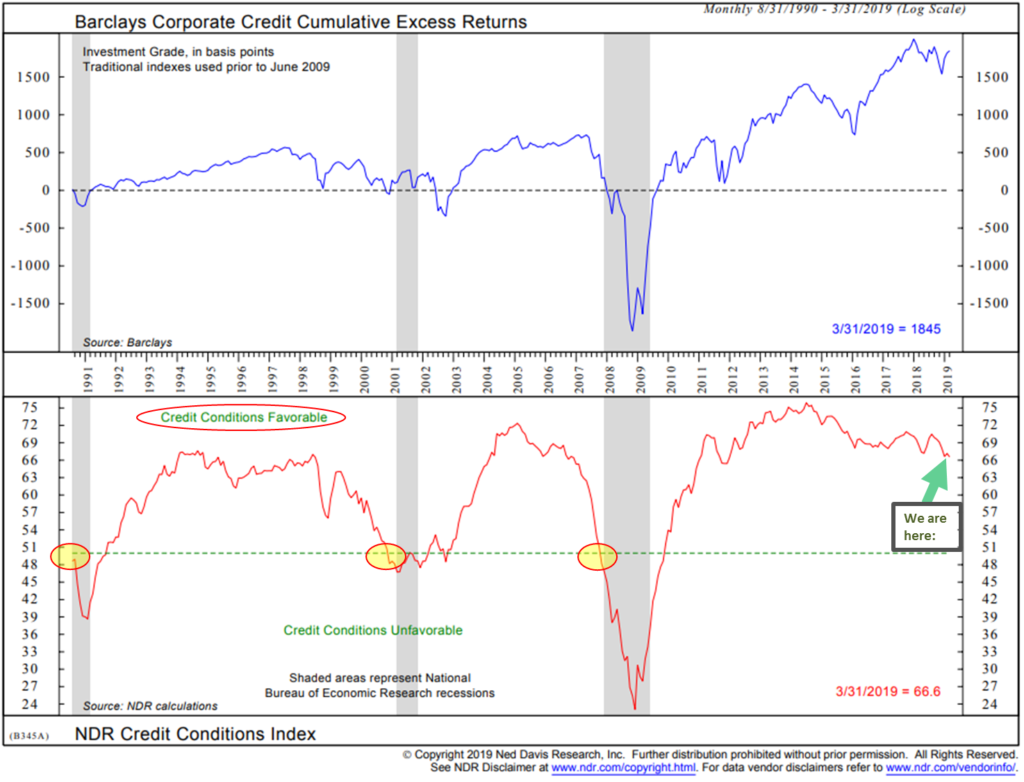

- The Ned Davis Research Credit Conditions Index.

When credit conditions are favorable, borrowers have access to money. When unfavorable, the lending dries up. Note the yellow circles that preceded recession. It is game over in recession. That’s when the companies living on debt can no longer find the funding to survive. That’s when the tide goes out we’ll see who’s swimming naked.

Bottom line: today lending conditions remain favorable. For now, grab a beer and relax.

Source: NDR

I’ll conclude by saying there are a number of other signals for us to follow. At the end of each month, I update my four favorite “Recession Watch” indicators. We’ll do that next week. In the meantime, you can find them in Trade Signals.

Trading strategies can add value and optionality to your portfolio. You may consider shorting a leveraged loan ETF, a high yield ETF and going long when the crisis is in full bloom. Both are tough to execute. The buy is much harder than the sell as fear will be palpable. (Aka 2008/09) Make sure you have a process or hire a seasoned pro how has a few scars on his/her back. Do talk with your financial advisor.

“Today, many investors are what my late father-in-law used to call ‘handcuff volunteers’. They are doing what they have to do, not what they want to do.“ – Howard Marks

I think Marks is right. Price can tell us a great deal. I also believe that price is one of the best indicators we have… so let’s keep an eye on what price is telling us about direction.

Grab that coffee and find your favorite chair. You’ll find a link to a recent Howard Marks interview. It’s worth the quick read. I’m looking forward to his presentation next month in Dallas at the Mauldin Strategic Investment Conference… and I’ll be sharing my post conference notes with you – stay tuned.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Howard Marks Interview

- Mauldin: The Rules Will Change but That’s (Probably) OK

- Trade Signals – Flashing Green

- Personal Note – Coming Home

Howard Marks Interview

Howard Marks was asked: How should investors calibrate their portfolio accordingly?

There are three ways to do it:

- Number one is go to cash. But that’s very extreme and easy to be wrong.

- Number two, you change your asset allocation: bonds rather than stocks, high grade bonds rather than low grade bonds, US rather international markets, developed world rather than emerging markets, large companies rather than small ones, and defensive companies rather than cyclical or growth companies.

- And then, the third way is to be defensive even within your existing asset allocation, just by shifting to safer approaches and safer managers within your asset classes. It’s challenging today to invest in a low-return, highly priced world. But I think a cautious approach can enable you to access returns even while behaving prudently.

You can find the full interview here.

Mauldin: The Rules Will Change but That’s (Probably) OK

I’m highlighting just the beginning of the letter – link to the full letter is below. Do start with the quote as it really sets the stage for the full piece. From John’s April 19, 2019 letter:

“But the emperor has nothing at all on!” said a little child.

“Listen to the voice of innocence!” exclaimed his father; and what the child had said was whispered from one to another.

“But he has nothing at all on!” at last cried out all the people. The emperor was suddenly embarrassed, for he knew that the people were right; but he thought the procession must go on now! And the lords of the bedchamber took greater pains than ever, to appear holding up the robes although, in reality, there were no robes at all.

—“The Emperor’s New Clothes” by Hans Christian Andersen

When you write about controversial topics for hundreds of thousands of readers for 20 years, you develop a thick skin. Virtually anything I say will upset someone.

So, when people say something like, “John Mauldin wakes up sucking lemons and then moves onto something sour,” as happened after last week’s letter, it doesn’t bother me. (It actually made me smile.) I write what I believe is correct. Those opinions change over time as I get new information.

I’m not the only one who changes. Laws and policies that may seem etched in stone are often more flexible than generally thought. In last week’s Japanification letter, I described how no one anticipated the various extreme measures taken in the last crisis, from TARP to QE to NIRP. Yet once those ideas were in play, they happened quickly.

I think the next crisis will bring similarly radical, sudden changes. We will think the unthinkable because we will see no other choices. That means the range of possible scenarios may be wider than you think.

To think this may be so is not necessarily bearish.

Fiscal Insanity

As of now, my best guess is the US will enter recession sometime in 2020. I may be off (early) by a year or two, but it’s coming. We know two things will happen.

Click here for the full letter. It is one of John’s best… I don’t say that lightly.

Trade Signals – Flashing Green

April 24, 2019

S&P 500 Index — 2,934

Notable this week:

Don’t Fight the Tape and the Fed has moved to a +2, the most bullish reading. The equity market trend signals continue to flash green. Investor sentiment is extremely optimistic.

Click here for this week’s Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – Coming Home

My sons, Matt and Kyle, are coming home from college on Monday. Finals are today and they’ll be home Monday afternoon. While I’m not arguing against the relatively low in-state Penn State tuition, I’m not sure why school ends so soon, but they begin internships in June and I sure do miss them. It will be really nice having them home.

Late May brings graduation for Susan’s oldest son Tyler. He’s a finance major and in the ROTC program at Cornell and soon to be commissioned an officer in the Marines and begins serving his military commitment in September. Tyler, his close friend Chase and Matt will be interning in NYC this summer – and sharing an apartment and, I assume, drinking a fair amount of beer. They are covering their own way and figuring out how to budget for the bar scene. Beers are expensive in NYC. Oh boy, do I miss those days. Envious!

I’ll be back and forth between Philadelphia and NYC the next few weeks and then on to the Mauldin conference in Dallas on May 13-16. I present on Tuesday, May 14. The event will be live streamed and you can get video copies of the presentations. There is a cost. Please know I don’t receive a penny. You can learn more here.

Please let me know if you are attending, I would very much enjoy grabbing a coffee with you.

Have a great weekend!

Best regards,

Stephen B. Blumenthal

Executive Chairman & CIO