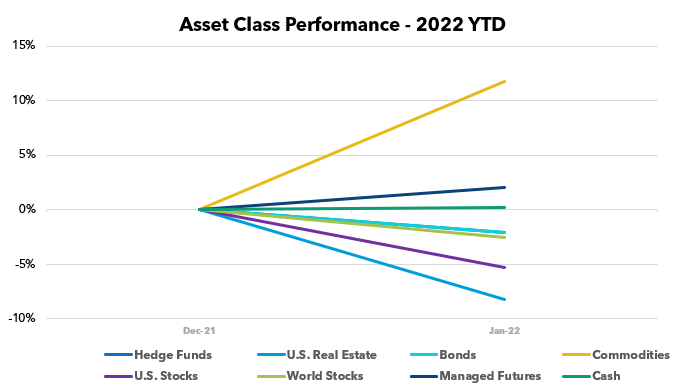

Well… looks like 2022 isn’t going to be the up, up, and away risk on love fest 2021 was. The first month of the year reminded everyone quite quickly that there is real risk in this market. US stocks, world stocks, hedge funds, and real estate all took a turn lower, with the S&P down nearly -10% mid month and Nasdaq having dropped -15%. But in a new twist – so did bonds! Dropping more in January than they typically lose in a full down year. So much for that flight to safety.

Q4 2021 hedge fund letters, conferences and more

Meanwhile, energy and other commodity prices continued their rise – while managed futures were able to capture gains both there and in short bond positions. Some will be hoping the old axiom – as January goes, so goes the year. Others will be fearing that phrase greatly.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

Sources: Managed Futures = SocGen CTA Index,

Cash = US T-Bill 13 week coupon equivalent annual rate/12, with YTD the sum of each month’s value,

Bonds = Vanguard Total Bond Market ETF (NYSEARCA:BND),

Hedge Funds = IQ Hedge Multi-Strategy Tracker ETF (NYSEARCA:QAI)

Commodities = iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG);

Real Estate = iShares U.S. Real Estate ETF (NYSEARCA:IYR);

World Stocks = iShares MSCI ACWI ex-U.S. ETF (NASDAQ:ACWX);

US Stocks = SPDR S&P 500 ETF (NYSEARCA:SPY)

All ETF performance data from Y Charts

Article by RCM Alternatives