Fairholme Fund commentary for the fourth ended December 31, 2018.

Q4 hedge fund letters, conference, scoops etc

To the Shareholders and Directors of The Fairholme Fund:

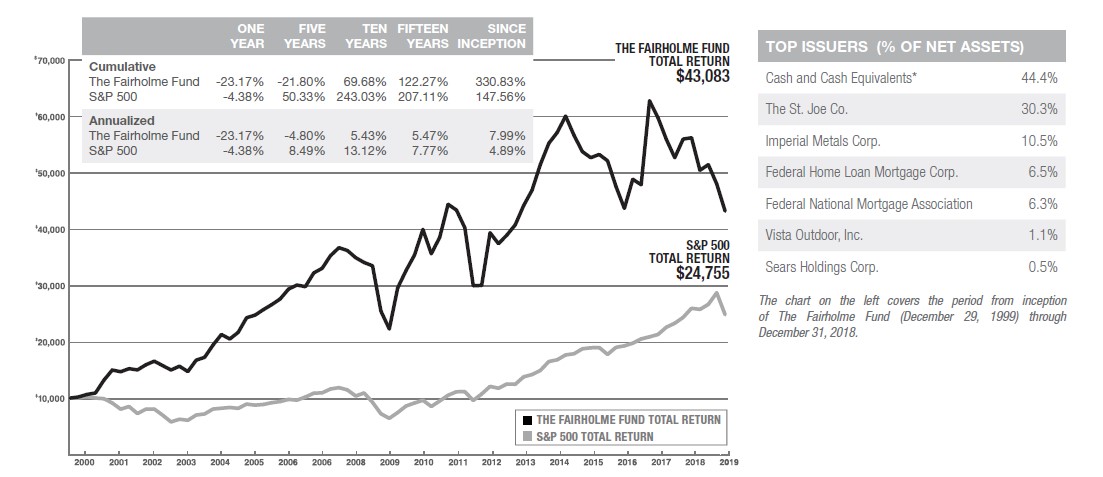

Absolute and relative returns for the Fund were poor last year due to the Chapter 11 filing of Sears Holdings, below plan operating performance at Imperial Metals, and significant investor fatigue with the government’s so-called conservatorship of Fannie Mae and Freddie Mac. Performance since inception tells a more uplifting story, and the new year is off to a great start. The Fund remains focused on long-term outperformance by employing a non-diversified strategy that results in greater than normal volatility.

The Fairholme Fund decreased 23.17% versus a decrease of 4.38% for the S&P 500 in 2018. The above graph and performance table compare The Fairholme Fund’s unaudited performance (after expenses) with that of the S&P 500, with dividends and distributions reinvested, for various periods ending December 31, 2018. The value of a $10,000 investment in The Fairholme Fund at its inception was worth $43,083 (assumes reinvestment of distributions into additional Fairholme Fund shares) compared to $24,755 for the S&P 500 at year-end. Of the $43,083, the value of reinvested distributions was $27,943.

The St. Joe Company (St. Joe) Common Stock

St. Joe is a complex story about unique lands and operations in Northwest Florida. The company has a strong balance sheet, low expenses, and the ability to profit for decades with real estate surrounding the Gulf of Mexico, US Intracoastal Waterways, and Northwest Florida Beaches International Airport.

There is growing demand for houses, apartments, limited and full-service hotels, clubs and resorts, and office space for work, life, and play in what Forbes calls “The Hamptons of The South.1” St. Joe initiated a record number of projects for 4,600 homes and 490 hotel rooms while buying back common stock with excess liquidity last year. Depending on scope, projects may take between eighteen and thirty-six months to show profits.

Fannie Mae and Freddie Mac (Fannie and Freddie) Preferred Stock

Fannie and Freddie’s regulator and conservator, the Federal Housing Finance Agency (FHFA), believes we will soon see administrative resolutions of remaining issues to end, what we believe to be, federal conservatorships of two of the most successful companies in the world.

We have argued for years that had the FHFA’s questionable net worth sweep never been implemented, Fannie and Freddie would have predictably restored statutory capital levels for safety and soundness, housing markets would better meet affordability goals, and Fannie and Freddie preferred shares would be fairly priced. Parts of the judicial system also appear to be moving towards our view with Judge Willett’s belief that the conservator’s “net worth sweep strips the GSEs of their capital reserves, and it is thus antithetical to the FHFA’s statutory command that it ‘preserve and conserve the assets and property’ of the GSEs.2” A conservator cannot “bleed the GSEs profits in perpetuity.3”

Despite the over 35% rise year-to-date, the preferred shares continue to trade at what we believe are large discounts to redemption values and realistic future outcomes.

Imperial Metals Corporation Debt & Common Stock

Imperial Metals is in a robust, ongoing process to assess strategic alternatives, including the establishment of a joint venture to accelerate development of a world class copper and gold mine in British Columbia. We await the results. Trading at less than 70 cents on the dollar and maturing in March of this year, Imperial corporate debt alone has the potential in our view to significantly increase the Fund performance should a joint venture be established with a credible strategic partner.

Outlook

The Federal Reserve increased interest rates by 100 basis points last year. U.S. federal and overall state budget deficits continue to soar in the midst of full employment and economic expansion. Financial markets are volatile, but not cheap. There have been sporadic opportunities to deploy

cash recently, and we believe there will be more going forward. There are positive developments in certain of the issuers constituting our larger holdings and, year-to-date, the Fund is up 10.1%. We believe much more potential exists. The Fund’s net assets stand at $1.1 billion. Cash and cash equivalents represent 37.4% of the Fund and are available for new opportunities. I and other Fairholme-affiliates own 16.9% of total Fund shares.

Respectfully submitted,

Bruce R. Berkowitz

Manager

The Fairholme Fund (“The Fairholme Fund”) commenced operations on December 29, 1999. The chart above presents the performance of a $10,000 investment for up to ten years to the latest annual period ending November 30, 2018.

The following notes pertain to the chart above as well as to the performance table included in the Management Discussion & Analysis Report. Performance information in this report represents past performance and is not a guarantee of future results. The investment return and principal value of an investment in The Fairholme Fund will fluctuate, so that an investor’s shares when redeemed may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted within. The performance information does not reflect the taxes an investor would pay on distributions from The Fairholme Fund or upon redemption of shares of The Fairholme Fund. Most recent month-end performance and answers to any questions you may have can be obtained by calling Shareholder Services at 1-866-202-2263.

Data for both the S&P 500 Index and The Fairholme Fund are presented assuming all dividends and distributions have been reinvested and do not reflect any taxes that might have been incurred by a shareholder as a result of The Fairholme Fund distributions. The S&P 500 Index is a widely recognized, unmanaged index of 500 of the largest companies in the United States as measured by market capitalization and does not reflect any investment management fees or transaction expenses, nor the effects of taxes, fees or other charges.

See the full PDF below.