Its an extreme value opportunity in this overpriced market. Buffet along with most institutions cant. The barriers to entry for institutional investors help create this unique opportunity.

Q1 hedge fund letters, conference, scoops etc

Tandy Leather Factory (TLF) is an illiquid (286 shareholders) micro-cap. A specialty physical store retailer in the dying niche of leather crafting. But, I see a consistently profitable, ignored and oversold opportunity driven by a new CEO with a board of prudent patient strategic capital allocators. TLF sells leather, leather crafts, and related supplies. It’s in 42 states, 7 Canadian provinces, 115 North American stores. Spain is the only remaining location outside North America.

Note the extremely low valuation not just today but over the profitable past + ten years. Price alone would be sufficient due diligence. However, opportunity enhanced with the new CEO discussed below.

Summary comments, why Tandy is Deep Value Cheap:

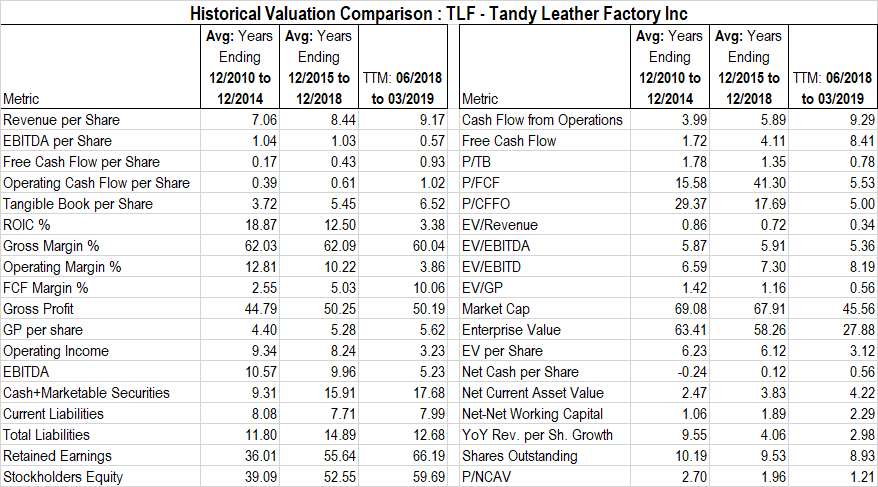

The book value per share increased from 2.83 at the end of 2010 to its recent quarter’s balance of 6.63. Further, retained earnings balance at the end of 2010, 26.42M versus the most recent quarterly balance of 66.189M. These results achieved with consistent positive cash flow,48.436M in cash flow from operations over that same multi year period and 30.43M in free cash flow. Debt reduction, and share buybacks. Yet the stock trades at the current EV per share price of $3.12 versus $4.47 EV per share at the end of 2010.

Undiscovered, ignored, illiquid, with zero analyst coverage. A few conference call questions from individual investors, no institutions.

New CEO Janet Carr after six months develops a logical, strategic value enhancing path with reported tangible progress.

Tandy is the sole retail national brand in their highly fragmented industry. Small enterprises and commercial entities often buy inventory from Tandy.

Amazon resistant as the customer wants to touch, smell, and feel the product. Stores offer a continuous flow of classes, hands-on help with projects/repairs from a skilled staff – endless positive 4.75 average customer reviews on Yelp. “level of service is unheard of these days”, “Never met more kind and helpful employees in retail”, “people are fantastic.”” “Go-Tandy-Go-Tandy!”

Years of compounding intrinsic value versus a falling price/enterprise value.

Management owns 42.20% of the shares outstanding. Board member and value investors Jeff Gramm/ Bandera Partners( 32% at average price of ~ $8.44): Board member James Pappas/ JCP Investments (9.60% at average price of $7.50).

During the most recent reported quarter, the outstanding debt of $9 million paid and bought back $714,000 of outstanding shares. Actions bring cash to $17.68 million at the end of the 2019 first quarter. On June 4, 2019, the Board of Directors expanded the Company’s stock repurchase plan to increase the present size of the plan to 1 million shares.

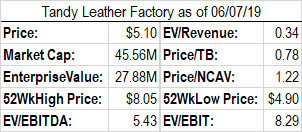

Deep absolute,historical and relative valuation discount. Price/Net Current asset value = 1.22, EV/Revenue = .34, EV/EBIT = 8.29, EV/GP = .56

CEO, Janet Carr’s updates rationale, progress and actions on strategic initiatives to drive longer term earnings growth in the short two months since her first call.

Initially, my investment in TLF solely based on price, discounted absolute,historical and relative valuation. But after six months on the job, CEO Janet Carr’s presented and implemented an impressive strategic plan. I’m persuaded Tandy can transform into an unexpected highly profitable / growth success story.

Commentary taken from the Q1 2019 conference call.

Two different business models now developed for commercial and retail. The infrastructures, processes, talent, data, and systems built. “The how-to” as they are calling it is to make it all happen with an optimal economic return. The strategy will re-establish brand credentials, build a compelling leather crafting retail experience, and create the right proposition to entice business customers back.

The initiatives begin with pricing. They are calling it “Everyday Honest Prices,” phased in globally over the last six weeks. It simplifies earlier complex and confusing price tiers. Pricing is now transparent to customers and makes prices more competitive for every customer.

Competitive benchmarking on every skew proved regular retail pricing complicated and many items too high. For this reason, prices lowered on every skew for both retail and manufacturing customers. A commercial division launched to serve the most significant customers with pricing targeted against Tandy’s wholesale competitors. Further, a reseller license agreement implemented for the resellers that helps maintain brand and price integrity.

The new pricing program launched with a full marketing campaign with in-store, direct mail, digital, social, and even direct personal outreach to the largest customers. Longer term expectation for increased sales, gross margin dollars and positive brand perception. The goal is to increase customer spend and to bring lapsed customers back into the brand.

The second major initiative since the March call is launch of a commercial division. This division is targeting the most significant commercial customers. These customers need products not carried in retail stores but can quickly source. A consistent supply and quality required with tailored shipping options. Consequently, a small team now focused on shifting larger customers from retail store relationship to the commercial account representatives. A dedicated Operations Manager is handling leather choice, order management, and selling support. Customer feedback is especially positive.

Management is appraising the 4-wall cash flow performance of stores as a critical metric in developing the fleet of stores. Bonus target set for inventory turns. But, opportunity with inventory requires merchandise planning capabilities not currently available. They need to evaluate product development, merchandising, merchandise planning, sourcing, and in-house manufacturing capabilities and figure where to invest and divest. When these tools and capabilities in place, inventory managed to the right levels.

Factory workforce reduced by 75% with assigned inventory positions in products produced in the factory. Management is evaluating lower cost outsourced options. Unfortunately, they could not support the factory staff at current levels. Difficult decisions needed on the path to growth and improved profitability. A critical, crucial senior leader is now overseeing the merchandising and commercial functions.

Financial commentary from the first quarter 2019 earnings call provide additional color to current and future value.

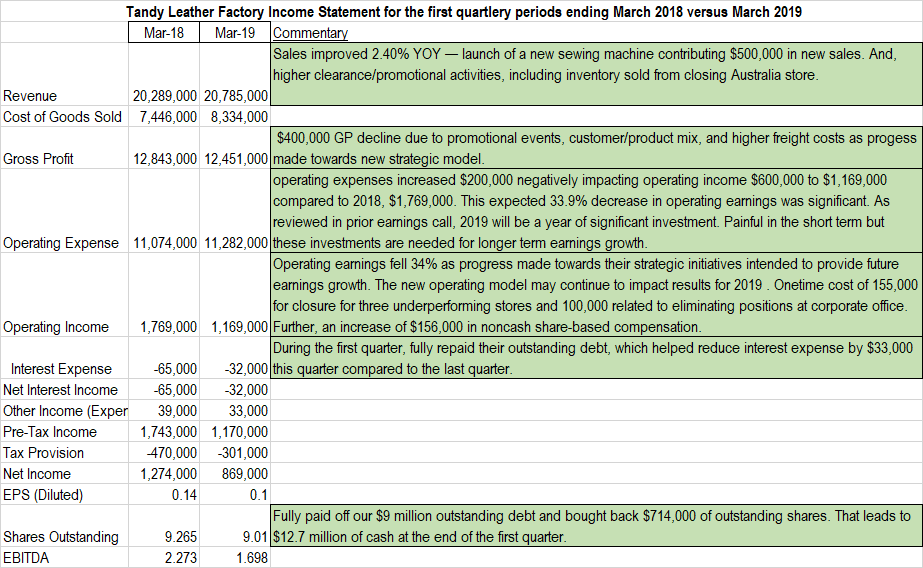

Progress and profits for Q1 2019 include rightsizing the store fleet realized by closing three underperforming stores. Sales improved 2.40% year over year – the launch of a new sewing machine contributing $500,000 in new sales. And, higher clearance and promotional activities, including inventory sold from closing the Australia store. Gross profits declined, and operating earnings fell 34% as progress made towards strategic initiatives intended to provide future earnings growth. The new operating model may continue to impact results for 2019. Promotional activities favorably impacted sales. But, a $400,000 decline to gross profit due to promotional events, customer/product mix, and higher freight costs. Onetime cost of 155,000 for closure for three underperforming stores and 100,000 related to eliminating positions at the corporate office. Further, an increase of $156,000 in noncash share-based compensation.

Gross profit declined $400,000 and operating expenses increased $200,000. This negatively impacted operating income by $600,000 to $1,169,000 compared to 2018, $1,769,000. The expected 33.9% decrease in operating earnings was significant. As reviewed in the prior earnings call, 2019 will be a year of significant investment. Painful in the short term, but these investments needed for long term earnings growth. During the first quarter, fully repaid outstanding debt, which helped reduce interest expense by $33,000 this quarter compared to the last quarter.

Cash flow from operations remains strong, which was $3 million for the quarter driven primarily from the $3.3 million reductions in inventory. This reduction in inventory was the result of 3 store closures this quarter as well as our efforts to clear out damaged/ excess inventory. Outstanding debt of $9 million paid and bought back $714,000 of outstanding shares. These actions bring cash to $12.7 million at the end of the first quarter.

Risk: Sales stagnate as niche continues to shrink. Difficulty in finding skilled labor and higher associated payroll costs, growing retail storefront lease expense.

Opportunity: Corporate action such as going private or sale if profitable growth not realized. Time is on the side of the new CEO as the company has a strong balance sheet and cash flow. Financial strength allows the implementation of corporate strategy. Special dividend, continued share buybacks and slow compounding of intrinsic value. Absolute, relative, and historical valuation is deeply discounted and will not go unnoticed forever. You can’t ask for a better board and CEO in terms of capital allocation.

In conclusion,TLF offers a large margin of safety, deep discounted extreme valuation in this overpriced market. Price alone would be sufficient due diligence. However, opportunity enhanced with the new CEO. Additionally, investors can wait for market recognition, mean reversion, or certain longer-term favorable corporate action.

Long: TLF

Article by Shadow Stocks