When it comes to dividend investing, the Dividend Aristocrats are the “cream of the crop.” The Dividend Aristocrats are stocks in the S&P 500 Index, with 25+ consecutive years of dividend increases.

Q3 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

There are thousands of stocks to choose from, many of which pay dividends. But the Aristocrats have profitable businesses, and the ability to grow their profits. This gives them the ability to withstand recessions, and continue increasing their dividends each year.

Franklin Resources (BEN) has increased its dividend for 39 years. The stock has a dividend yield of 3.4% and regularly increases its dividend by 10% or more per year. For example, the company raised its dividend by 13% at the end of 2018.

After a couple of difficult years of declining assets under management, Franklin Resources has returned to growth this year. It could continue to raise its dividend by double-digits each year, which makes it an attractive stock for dividend growth.

Business Overview

Franklin Resources is an investment management company. It was founded in 1947 in New York, by Rupert H. Johnson Sr., who had previously managed a Wall Street brokerage firm.

He named the company after Benjamin Franklin, the founding father who was viewed as a symbol for frugality, saving, and wise investments.

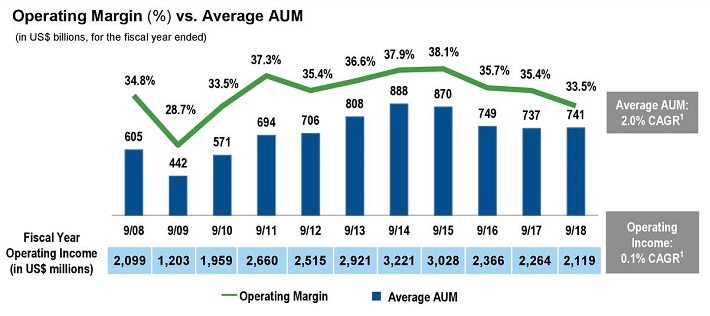

Today, Franklin Resources manages the Franklin and Templeton families of mutual funds. The past few years have been difficult for Franklin Resources. In 2015, revenue and earnings-per-share declined by 6% and 13%, respectively. Things only got worse the following year—in 2016, revenue fell 17%, while earnings-per-share declined 11%.

The declines were due to under-performance across several of the company’s flagship funds. Weak performance is a big problem for an asset manager, because it typically results in lower assets under management.

When funds do poorly, investors take their money elsewhere. This has caused Franklin Resources’ fundamental deterioration Assets under management is the key driver of revenue and earnings.

Source: Earnings Presentation, page 14

Conditions improved moderately in 2017, as Franklin Resources grew AUM by 3% to $753.2 billion. However, its fundamentals have worsened again in 2018. By September 2018, AUM had declined 5% to $717.1 billion. Franklin Resources finished the year with assets under management of $649.9 billion. Much of this decline was due to a sizable reduction in the company’s international equity portfolio.

Franklin Resources’ assets under management exceeded $880 billion at the end of 2014. As a result, the company has a long way to go to regain the ground it has lost.

Growth Prospects

Despite the difficult operating environment, there are reasons to be optimistic about the company’s long-term growth. The U.S. is an aging population. There are thousands of Baby Boomers retiring every day. Combined with rising life expectancies, there is a great need for investment planning.

There should always be a need for the financial services provided by Franklin Resources. The company has seen assets under management increase again in recent periods.

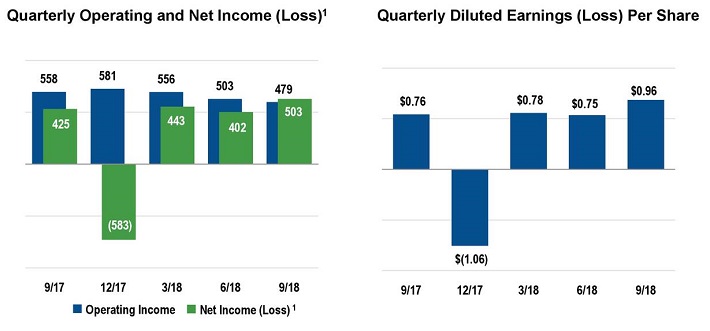

In the short term, the company could see continued difficulty. Franklin Resources saw revenue decline 1% due to lower average assets and lower average fees in the company’s fourth quarter. Earnings-per-share did rise 26% year-over-year, but this was due to lower taxes and a lower share count. For the year, earnings-per-share increased 12% from fiscal year 2017.

Source: Earnings Presentation, page 13

Franklin Resources is attempting to remedy its issues. The company announced that it agreed to acquire alternative credit manager Benefit Street for an undisclosed sum. Benefit Street has $26 billion in assets under management.

Franklin Resources reduced its diluted share count by 6% in fiscal 2018, which helps boost earnings-per-share. We expect the share count to decline another 2% in fiscal 2019.

Accretion to earnings is even stronger when the price of a stock declines. This is an advantage of consistent profitability—the company can use short-term dips in the share price as an opportunity to buy back its own stock.

Competitive Advantages & Recession Performance

Asset management is a highly competitive business, and there are not many competitive advantages in the financial services industry. The ability to retain clients depends largely on performance. If funds perform worse than their benchmarks, clients typically see a need to withdraw their funds.

However, Franklin Resources does have a few advantages going for it. The first, and perhaps most important, is brand recognition. Franklin Resources has been in operation for 70 years. That indicates a certain developed expertise and some innate investment abilities. Franklin Resources also still has huge assets under management, allowing the company to offer a wide range of investment opportunities to clients and generate some economies of scale.

Counterbalancing these advantages, Franklin Resources most recent recession performance was poor:

- 2007 earnings-per-share of $2.37

- 2008 earnings-per-share of $2.24 (5.5% decline)

- 2009 earnings-per-share of $1.30 (42% decline)

- 2010 earnings-per-share of $2.12 (63% increase)

As you can see, earnings-per-share fell steeply in 2009 during the worst part of the Great Recession. This should come as no surprise, since investing is hardly recession-resistant. During recessions, stock markets typically decline. For asset managers, this can lower assets under management and fees. That said, Franklin Resources recovered quickly, and saw earnings jump in 2010 and thereafter.

During recessions, stock markets typically decline. This prompts many investors to sell their stocks out of fear, which causes lower assets under management and fees. That said, Franklin Resources recovered quickly, and saw earnings jump in 2010 and thereafter.

Valuation & Expected Returns

While Franklin Resources’ fundamentals have worsened in recent years The good news is potential investors in Franklin Resources are not paying a high price for the stock.

We expect that Franklin Resources will earn $3.50 per share in fiscal year 2019. Based off the current share price of $30, the stock has a price-to-earnings ratio of 8.6. This is well below the S&P 500, which has an average price-to-earnings ratio of 19.9.

If the company can grow its asset under management either through acquisition or improvement in its core business, the stock could see its price-to-earnings ratio rise to 12 by 2024.

If Franklin Resources can recover and return to earnings growth, the current price could prove to be a good value.

An expanding price-to-earnings ratio could generate significant returns.

Franklin Resources has an attractive dividend yield of 3.4%, and the dividend payout appears to be secure. The following video discusses Franklin Resources’ dividend safety in further detail.

In addition, we forecast 3.8% earnings growth for Franklin Resources through 2024, slightly below the long term average. A potential breakdown of returns is below:

- 3.8% earnings growth

- 3.4% dividend yield

- 6.8% valuation expansion

If Franklin Resources can return to growth investors buying the stock now could see annual returns of 14% over the next five years.

Final Thoughts

Franklin Resources’ assets under management again declined in 2018. It will likely take some time to recover what it has lost, but the company is still growing earnings, thanks to share buybacks. The stock offers a 3.4% dividend yield and the potential for annual dividend increases.

With a low valuation, solid yield and possibility of a higher valuation down the road, Franklin Resources could be a buying opportunity for value and dividend growth investors.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

Article by Nate Parsh, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.