The Dividend Aristocrats are a group of stocks in the S&P 500 Index, with 25+ years of consecutive dividend increases.

Q3 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

The list of Dividend Aristocrats is diversified across multiple sectors, including consumer goods, financials, industrials, and healthcare. One group that is surprisingly under-represented, is the utility sector. There is only one utility stock on the list of Dividend Aristocrats: Consolidated Edison (ED).

The fact that there is only one utility on the list may come as a surprise, especially since utilities are widely regarded as being steady dividend stocks.

Consolidated Edison is about as consistent a dividend stock as they come. With over 100+ years of steady dividends and more than 40 years of annual dividend increases, Consolidated Edison makes it onto our list of “blue-chip” stocks. You can see the full list of blue chip stocks here.

This article will discuss what makes Consolidated Edison an appealing stock for income investors.

Business Overview

Consolidated Edison is a large-cap utility. The company generates approximately $12 billion in annual revenue, and has $50 billion in assets.

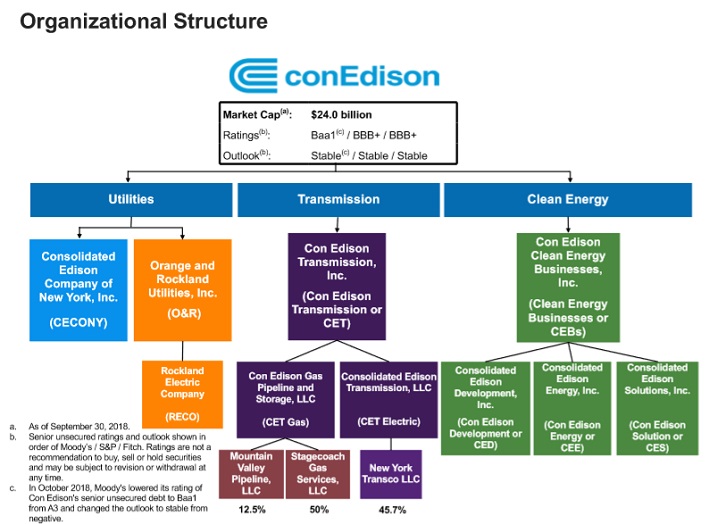

The company serves over 3 million electric customers, and another 1 million gas customers, in New York. It operates electric, gas, steam transmission, and green energy businesses.

Source: Earnings Presentation, page 5

It should come as no surprise that Consolidated Edison generated steady growth over the course of 2018. Adjusted earnings-per-share increased 7% in both the 2018 third quarter, and over the first three quarters of the year combined.

Consolidated Edison should continue to generate modest earnings growth each year, through a combination of new customer acquisitions and rate increases.

Growth Prospects

Earnings growth across the utility industry typically mimics GDP growth. Over the next five years, we expect Consolidated Edison to increase earnings-per-share by 3.5% per year.

The growth drivers for Consolidated Edison are new customers and rate increases. One benefit of operating in a regulated industry is that utilities are permitted to raise rates on a regular basis, which virtually assures a steady level of growth.

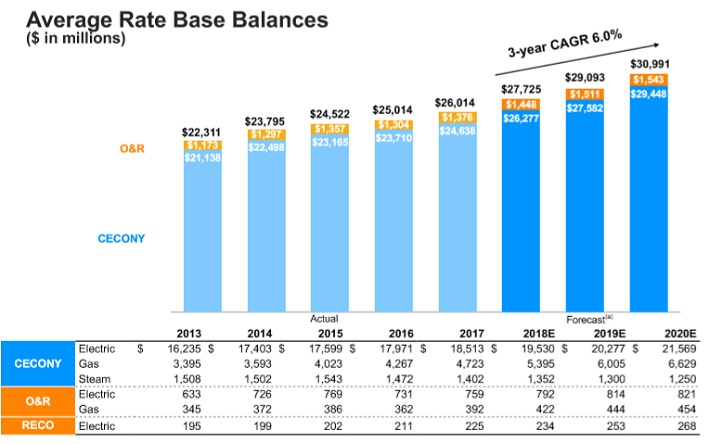

Source: Earnings Presentation, page 23

In 2017, the company received approval for rate base plans over the next three years, in both the electric and gas delivery segments. Consolidated Edison expects to increase its rate base by 6% each year, through 2020.

One potential threat to future growth is rising interest rates, which could increase the cost of capital for companies that utilize debt, such as utilities. Fortunately, Consolidated Edison is in strong financial condition. It has an investment-grade credit rating of BBB+, and a modest capital structure with balanced debt maturities over the next several years.

A healthy balance sheet and strong business model help provide security to Consolidated Edison’s dividends.

Competitive Advantages & Recession Performance

Consolidated Edison’s main competitive advantage is the high regulatory hurdles of the utility industry. Electricity and gas service are necessary and vital to society. As a result, the industry is highly regulated, making it virtually impossible for a new competitor to enter the market. This provides a great deal of certainty to Consolidated Edison.

In addition, the utility business model is highly recession-resistant. While many companies experienced large earnings declines in 2008 and 2009, Consolidated Edison held up relatively well. Earnings-per-share during the Great Recession are shown below:

- 2007 earnings-per-share of $3.48

- 2008 earnings-per-share of $3.36 (3% decline)

- 2009 earnings-per-share of $3.14 (7% decline)

- 2010 earnings-per-share of $3.47 (11% increase)

Consolidated Edison’s earnings fell in 2008 and 2009, but recovered in 2010. The company still generated healthy profits, even during the worst of the economic downturn. This resilience allowed Consolidated Edison to continue increasing its dividend each year.

Valuation & Expected Returns

Consolidated Edison is expected to generate adjusted earnings-per-share of $4.25 in 2018. Based on this, the stock trades for a price-to-earnings ratio of 17.8, which is above our fair value estimate of 15.4. The fair value estimate is equal to the 10-year average price-to-earnings ratio for the stock.

As a result, Consolidated Edison shares appear to be overvalued. If the stock valuation retraces to the fair value estimate, the corresponding multiple contraction would reduce annual returns by 2.9%. This could be a significant headwind for future returns.

Fortunately, the stock could still provide positive returns to shareholders, through earnings growth and dividends. We expect the company to grow earnings by 3.5% per year over the next five years. In addition, the stock has a current dividend yield of 3.8%.

Putting it all together, Consolidated Edison’s total expected returns are 4.4% per year over the next five years. This is a decent expected rate of return for a utility, which are typically bought primarily for their dividends.

Income investors will not be disappointed with Consolidated Edison. It has an attractive 3.8% yield and a highly secure payout. The company has a projected 2018 payout ratio below 70%, which indicates a sustainable dividend.

However, growth investors or those looking for a higher rate of return are likely not attracted to Consolidated Edison stock.

Final Thoughts

Consolidated Edison stock is slightly overvalued currently, making it relatively unattractive for value investors today.

That said, Consolidated Edison can still serve a valuable purpose in an income investor’s portfolio. The stock offers secure dividend income, and its 3.8% dividend yield exceeds the 2% average dividend yield of the S&P 500 Index. Consolidated Edison is also a Dividend Aristocrat, and should raise its dividend each year.

As a result, Consolidated Edison stock is still worth considering for retirees.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

Article by Bob Ciura, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.