On July 23 2019 Jeffrey Gundlach, Chief Executive Officer of DoubleLine Capital, held an audio webcast discussing the closed end funds Opportunistic Credit Fund (DBL) and Income Solutions Fund (DSL).

Q2 hedge fund letters, conference, scoops etc

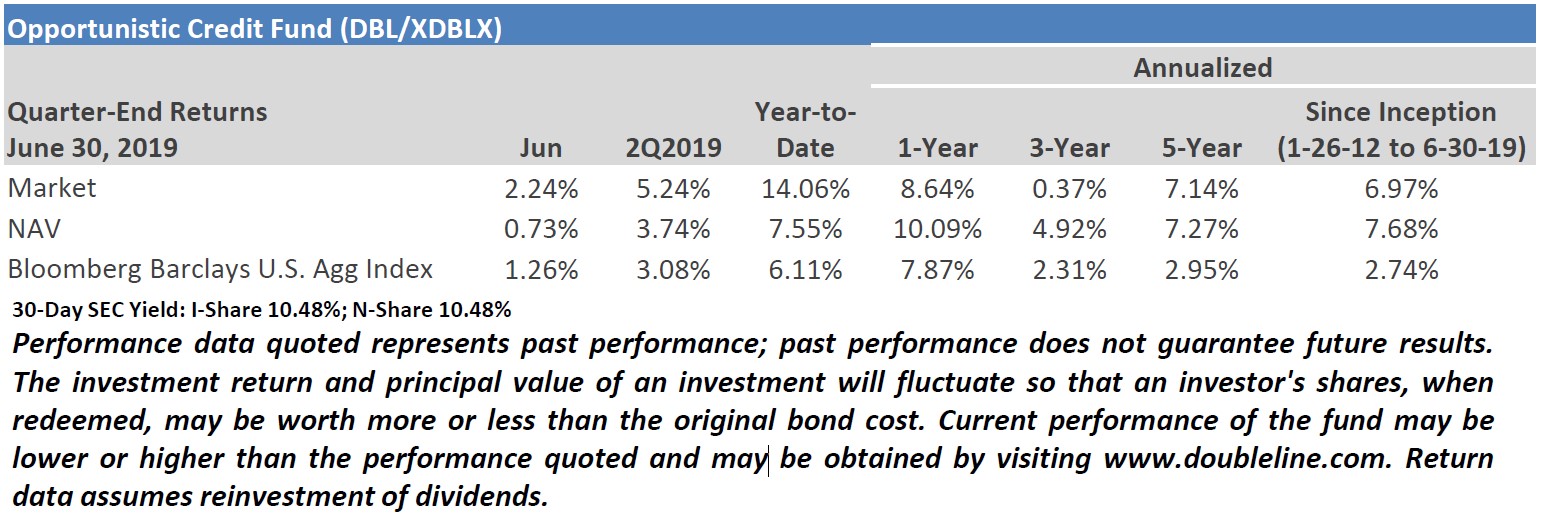

DoubleLine Opportunistic Credit Fund (DBL)

- DBL is a Mortgage Backed Securities (MBS) fund with a mix of credit and government guaranteed securities which aims to provide a high level of income.

- Per prospectus, the Fund must invest at least 50% of its assets in investment grade securities.

- When DBL was started, it was a mix of long duration agency mortgage backed securities and non agency residential mortgage backed securities, many of which were distressed in the aftermath of the Great Recession and the housing problems of 10+ years ago. Since then, the portfolio has evolved into a mix of government guaranteed debit and credit sectors.

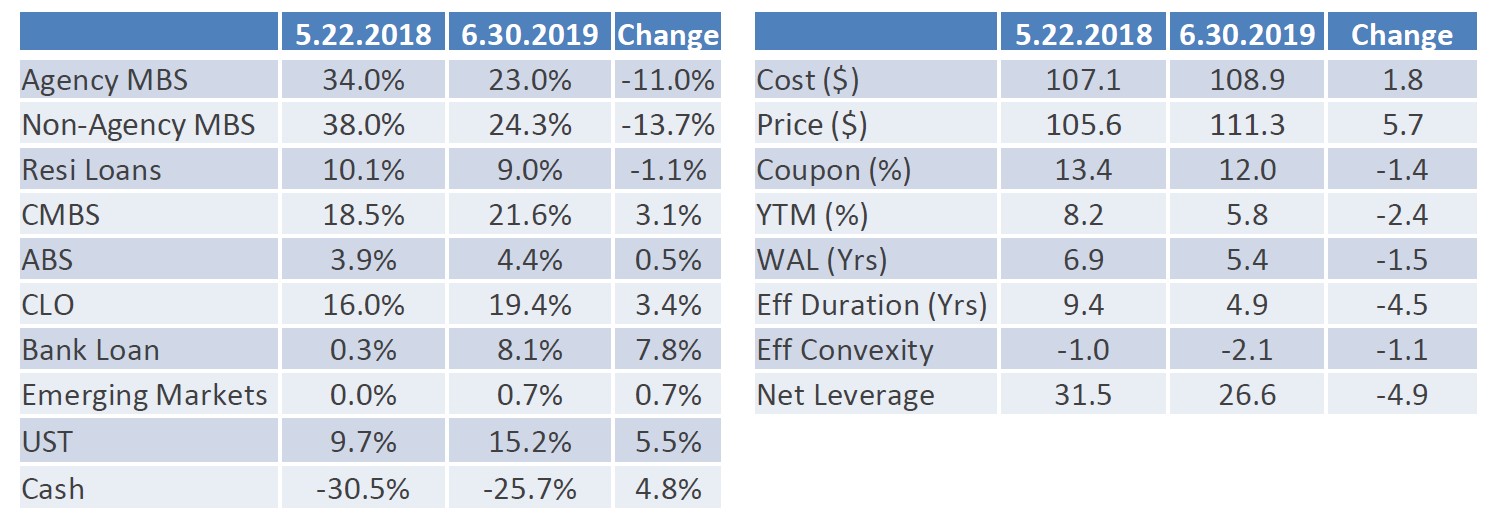

- As of June 30th,

- Agency MBS : 23.0% of the gross assets are in agency mortgage backed securities, with an effective duration of 13.9 years.

- Non Agency MBS : 24.3% of the gross assets are in non agency mortgage backed securities (RMBS), which are primarily below investment grade. Not all of the RMBS are legacy assets as there has been new issuance in recent years.

- Residential Loans : 9.0% of the gross assets are in residential loans, which carry a Not Rated (NR) rating. NR does not necessarily mean below investment grade, but rather the issuers of the loans did not acquire a rating by a third party rating agency.

- CMBS : 21.6% of the gross assets are in commercial mortgage backed securities (CMBS), which is split roughly 50% investment grade and 50% below investment grade.

- CLO : 19.4% of the gross assets are in collateralized loan obligations (CLO), which have become a very significant activity here at DoubleLine. The CLOs in the fund are roughly 50% investment grade and 50% below investment grade. CLO debt tranches exhibit low interest rate duration risk due to their floating rate nature, which can offer protection in a rising rate environment.

- Government : 15.2% of the gross assets are in a 3 year United States Treasury (UST) note, with a yield to maturity (YTM) of 2.05% and an effective duration of 0.46 years. These securities are primarily held to acquire leverage through the repo facility.

- Bank Loans : 8.1% of the gross assets are in bank loans, which the fund holds because they are floating rate in nature and they yield substantially more than the fund’s borrowing cost for leverage.

- ABS: 4.4% of the gross assets are in asset backed securities (ABS), with a majority carrying an investment grade rating and an effective duration of 3.44 years.

- Emerging Market Debt: 0.70% of the gross assets are in an investment grade emerging market bond, which is in the fund as a short term tactical opportunity.

- Leverage: Net leverage is 26.6%.

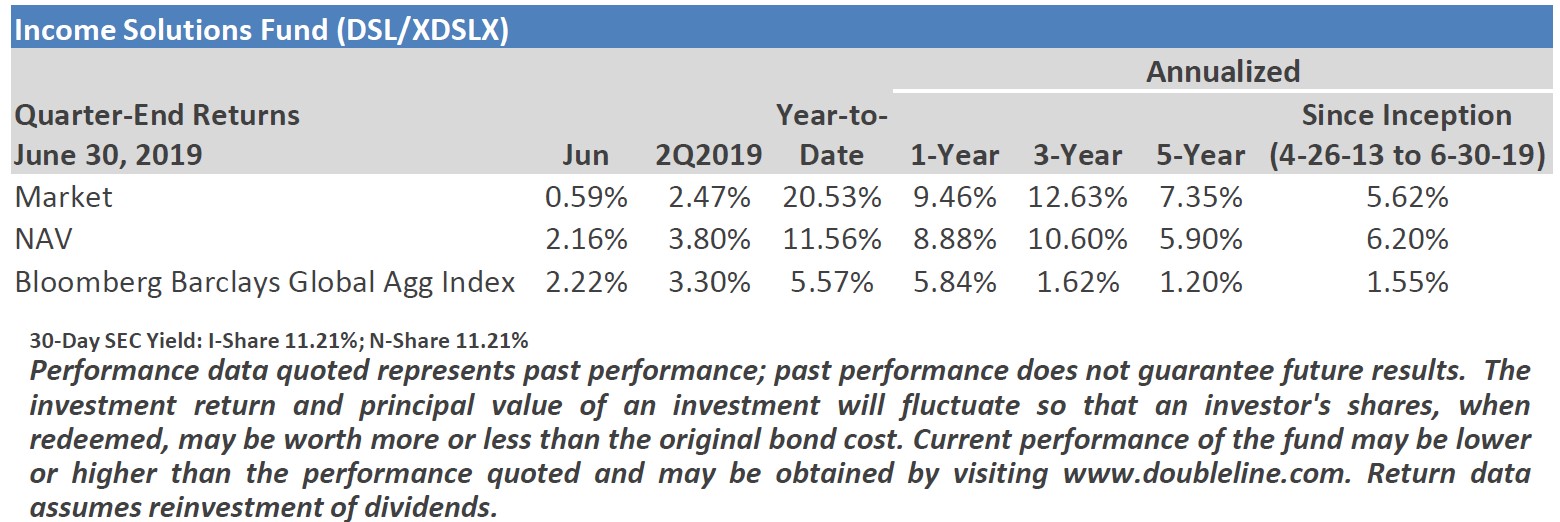

Income Solutions Fund (DSL/XDSLX)

- DSL is a credit centric fund that takes a diversified approach to accessing credit markets by investing in international credit, structured products, and corporate credit markets in an effort to provide a high level of income.

- Per prospectus, the Fund may invest without limit in securities rated below investment grade or unrated securities judged by DoubleLine to be of comparable quality.

- Since inception on April 30 th , 2013 the Fund has averaged less than 20% of its gross assets in investment grade securities.

- Compared to DBL, DSL is:

- Much larger in size, at over $2 billion in market value compared to roughly $300 million of DBL.

- Carries more leverage and is inherently more volatile.

- Benchmarked against the Bloomberg Barclays Global Aggregate Unhedged Bond Index, as roughly 43% of the fund is invested in USD denominated emerging market fixed income, whereas DBL is benchmarked against the Bloomberg Barclays U.S. Aggregate Bond Index.

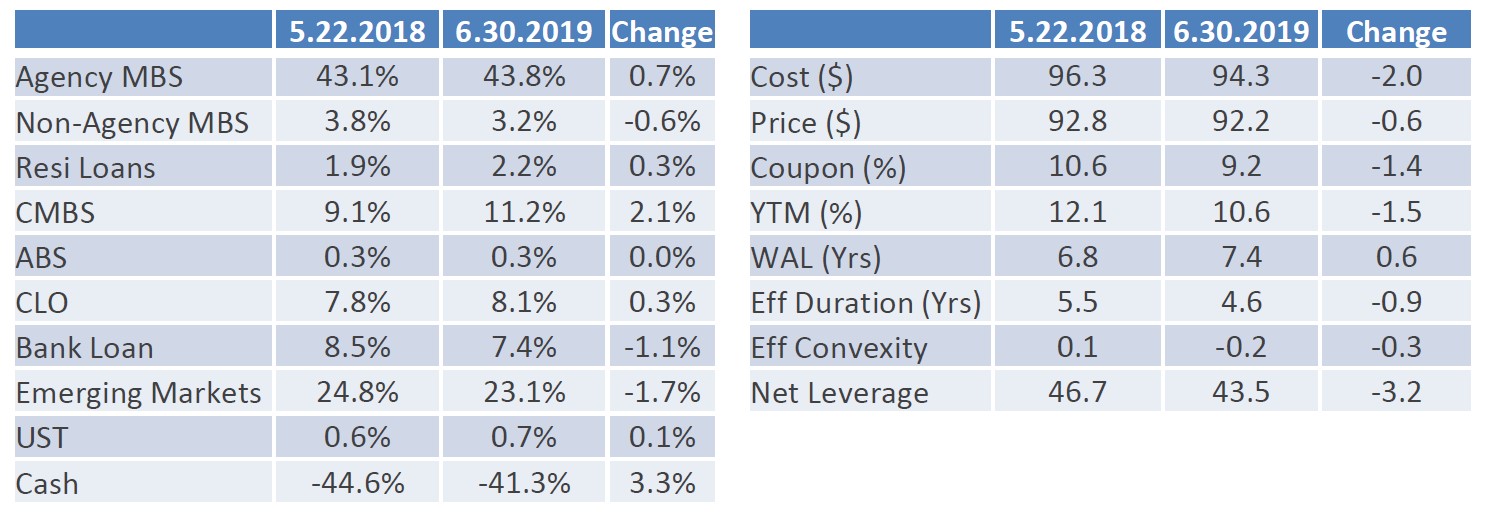

- As of June 30th,

- Emerging Market Debt : 43.8% of the gross assets are in USD denominated emerging market corporate and sovereign bonds, with the majority of the exposure in emerging market corporate bonds, with a YTM of 7.72% and an effective duration of 4.59 years. The majority of this allocation is rated BB (18.5%) and B (19.9%).

- Mr. Gundlach believes the next move for the United States Dollar (USD) is down, which will likely be a tailwind for emerging market debt.

- High Yield : 23.1% of the gross assets are in high yield bonds, with a YTM of 9.55% and an effective duration of 3.06 years. The majority of this allocation is rated B (9.1%) and CCC (10.6%).

- This is an area of the portfolio Mr. Gundlach and the investment team continue to monitor on a day to day basis as the team is keeping a vigilant eye on a potential recession.

- Similar to January 2007, where Mr. Gundlach wrote a white paper on this topic, he advised clients that, “It’s okay to be dancing the risk dance, but you’d better be dancing near the door.” For now, holding this mix of high yield could be a good risk reward trade off at this point, but is something the Fund is monitoring very closely as the economic data and outlook changes.

- CMBS : 11.2% of the gross assets are in commercial mortgage backed securities (CMBS), which is primarily below investment grade or Not Rated (NR). The duration of these assets are very short at 1.78 years, with a YTM of 8.79%.

- CLO : 8.1% of the gross assets are in collateralized loan obligations (CLO), and are attractive for the same reasons held in DBL. The majority of CLOs held in DSL are below investment grade.

- Bank Loans : 7.4% of the gross assets are in bank loans, which the fund holds because they are floating rate in nature and they yield substantially more than the fund’s borrowing cost for leverage. The bank loan portfolio has a duration of 0.25 years.

- Agency MBS : 3.2% of the gross assets are in agency mortgage backed securities, with an effective duration of 16.83 years.

- Non Agency MBS : 2.2% of the gross assets are in non agency mortgage backed securities (RMBS), which is almost all subprime and carry a YTM of 3.64%, with an effective duration of 7.02 years.

- RMBS had been a considerable allocation in DSL several years ago; however after the strong performance of the RMBS sector, the Fund sold the majority of the initial allocation.

- Municipal: 0.7% of the gross assets are in municipal bonds.

- ABS: 0.3% of the gross assets are in asset backed securities (ABS).

- Leverage: Net leverage is 43.5%.

- Emerging Market Debt : 43.8% of the gross assets are in USD denominated emerging market corporate and sovereign bonds, with the majority of the exposure in emerging market corporate bonds, with a YTM of 7.72% and an effective duration of 4.59 years. The majority of this allocation is rated BB (18.5%) and B (19.9%).

- As of this webcast, DSL was trading at a discount to its NAV of 1.13%. Since inception, DSL has traded at an average 5.80% daily discount.

Question & Answer

Q: Is there a reason to hold DSL and DBL or should you pick one or the other?

A: It depends on your risk profile. DBL is a higher quality portfolio and likely to be a better hold in a weaker economy. DSL is a lower quality, more volatile portfolio that could do well in strong risk on environments, such as the one witnessed year to date.

Q: In a recession led by corporate defaults, can active management versus passive management be more nimble, especially with regards to DSL?

A: Mr. Gundlach does not believe we’ll get it perfect every time, but during the last credit crisis of the ‘00s, Mr. Gundlach went to virtually no credit risk in the spectrum of funds managed at the time. In Mr. Gundlach’s Core Fixed Income strategies, the funds held 85% in UST bonds, which could have easily been 15%. That put Mr. Gundlach in a position that when everything crashed, the team was able to rotate from government securities to credit at the bottom in March 2009.

Q: What type of economic environment would be detrimental for DBL and DSL?

A: An imminent credit meltdown would be bad for DSL and likely not as bad for DBL. DBL is a lower risk fund and doesn’t have nearly as much credit risk. DSL is a full on credit fund at its present construct. DBL is less unidirectional when it comes to credit.

Q: What drove the dividend cut in DBL?

A: Mr. Gundlach and team decided to cut the dividend so that we would be able to feel that we could earn it without taking on excessive interest rate and credit risk. Interest rates are down very sharply from where they were back in 2012, when DBL launched. Additionally, credit spreads are extremely narrow at the present time. When interest rates drop and credit spreads tighten, it becomes increasingly more difficult to earn a high dividend. The yield on DBL (5.84%) remains significantly higher than the Barclays Aggregate Index (2.53%).