My fear of the markets has forced me to hone my timing with great precision. When I am trading properly, it is like a pool player running racks. If my gut feel of market conditions is not right, I don’t trade. ~ Mark Weinstein

In this week’s Dirty Dozen [CHART PACK], we talk fund manager sentiment, bearish USD positioning along with why the dollar is poised for a bounce, western countries out of “equilibrium, record cheap EM stocks, elevated profit margins, and more…

**Note: As you’ve seen in our latest research, the market is transitioning through a “Narrative Crisis” as prices diverge from the dominant consensus.

To help you navigate this regime, we’re opening enrollment to the Macro Ops Collective today.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you want to protect your portfolio against these macro forces, make sure you become a member of the Macro Ops Collective.

Q1 2023 hedge fund letters, conferences and more

Again, Enrollment kicks off TODAY and runs until Sunday, April 30th midnight CST. You can learn more about the Collective and what it can do for your investing, here.

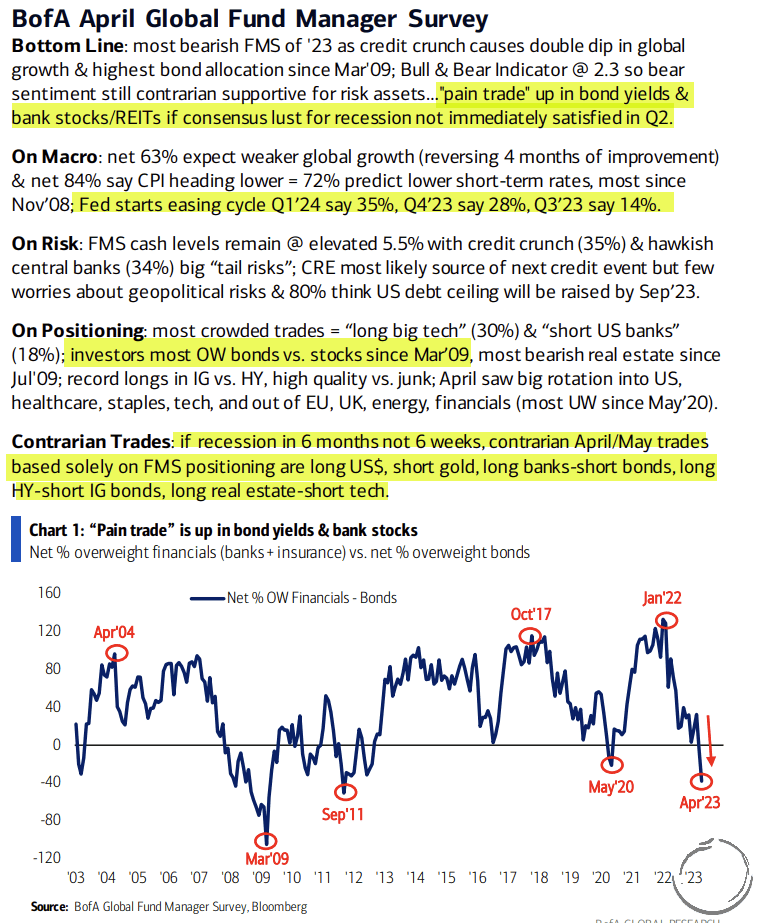

- The latest BofA Global Fund Manager Survey with highlights by me.

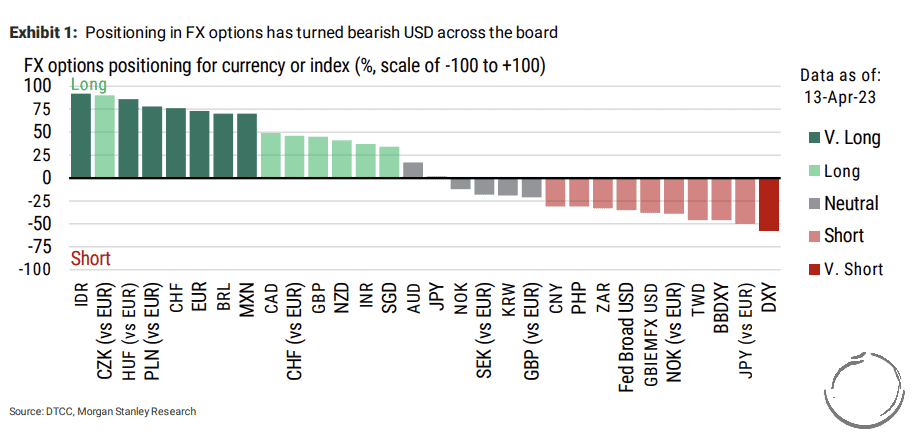

- Last week we talked about a potential intermediate bottoming process in the US dollar due to increasing signs of a bearish consensus forming. MS shared the following in a recent report which shows positioning in FX options is crowded short against USD.

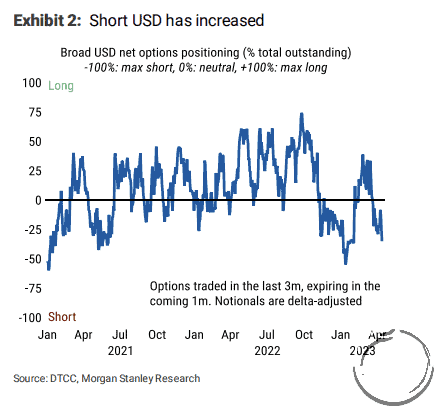

- MS points out that the “short positioning in USD, represented by the broad USD index, has rarely been larger over the past couple of years.”

- They believe (as do we) that growth is going to begin to slow considerably going into the end of the year which makes the USD more susceptible to a risk-off rally.

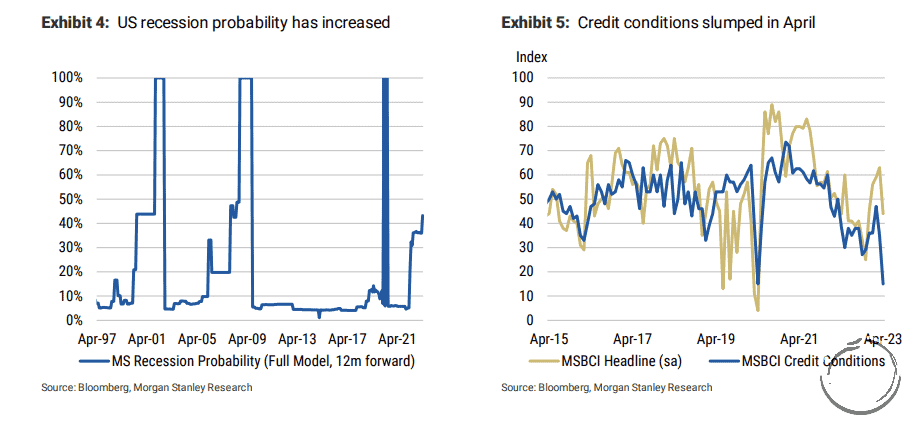

MS notes that they’re “expecting the consumer to come under pressure in part thanks to negative real disposable income growth, while credit conditions are weak thanks to recent events in the banking sector. 2Q has not started well from a growth perspective, with the Morgan Stanley Business Conditions Index dropping sharply in April on the back of credit concerns and driven by the services index.”

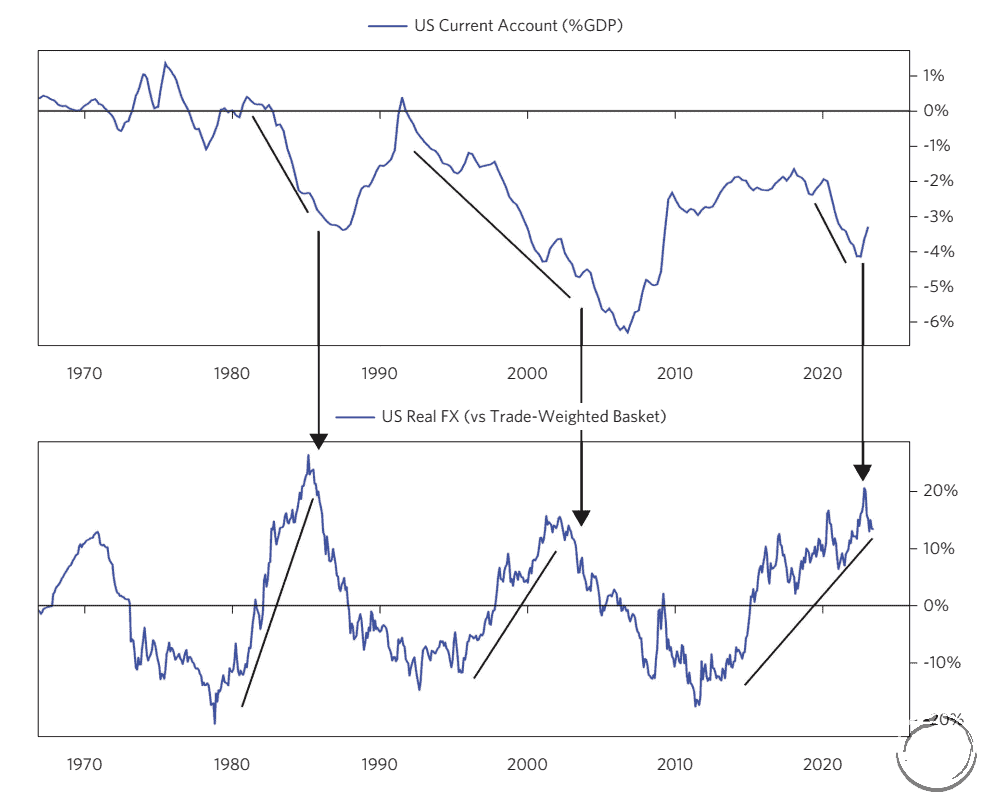

- Bridgewater published a report the other week titled “The Tightening Cycle is Beginning to Bite” and at the end of the report they shared the following chart and commentary:

“The tightening of monetary policy by the Fed was the most aggressive in the world and pulled another round of capital into the dollar, sent the real exchange rate to the top of its 50-year trading range, and pushed the current account into substantial deficit. The current account deficit represents the breakeven capital inflow to hold a currency steady, meaning that a given level of capital inflow is discounted to continue once it impacts the currency and the capital account. The resulting level of the exchange rate can be sustained if conditions are sustained.”

We’re cyclical USD bears for similar reasons which we’ve outlined here. But, as discussed above, we believe there’s an increasing probability that the USD will start an intermediate rally soon.

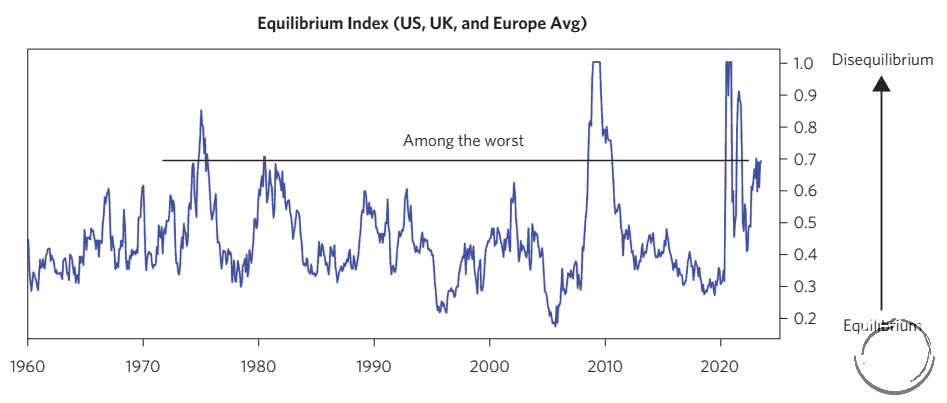

- Another interesting chart from the report is this one showing BW’s “Equilibrium Index”, which is a measure of a country’s debt to income levels, spending versus productive capacity, and risk premium spreads across assets.

BW writes that “the further an economy is from equilibrium, the bigger the policy moves required to fix problems and the higher the market volatility.”

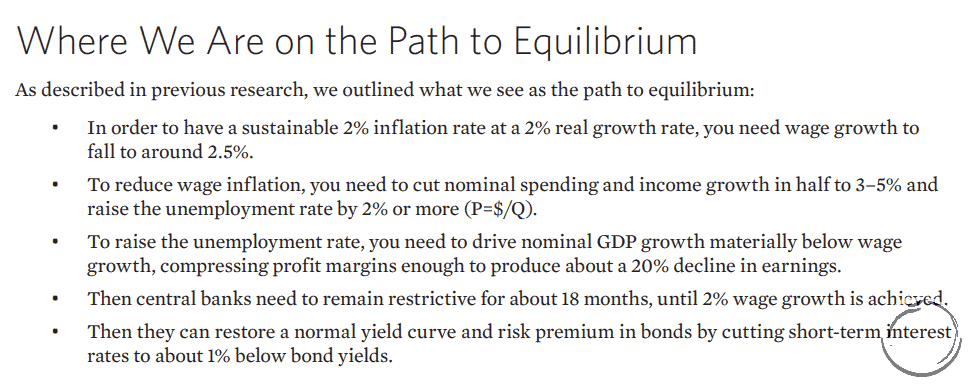

- And here’s our path to equilibrium as BW sees it, which we broadly agree with.

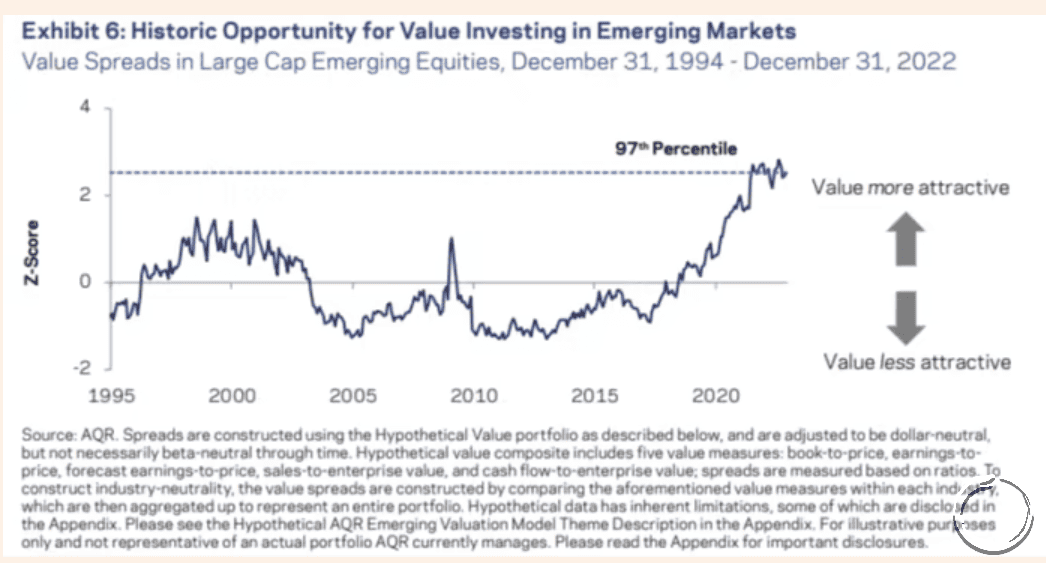

- Once the Fed is able to get the US economy back into equilibrium through the engineering of a recession, there are going to be some great opportunities in emerging markets once the dust settles.

This chart from AQR via the FT shows that value spreads in EM large-cap equities are in the 97th percentile over the last 30 years.

- But, again, we’ll want to wait for this tightening cycle and cyclical bear market to complete first. This chart shows foreign portfolio flows by EM country overlaid against the Chicago Fed Financial Conditions Index. Not surprisingly, investors flee EM assets when conditions get tight (chart via FT).

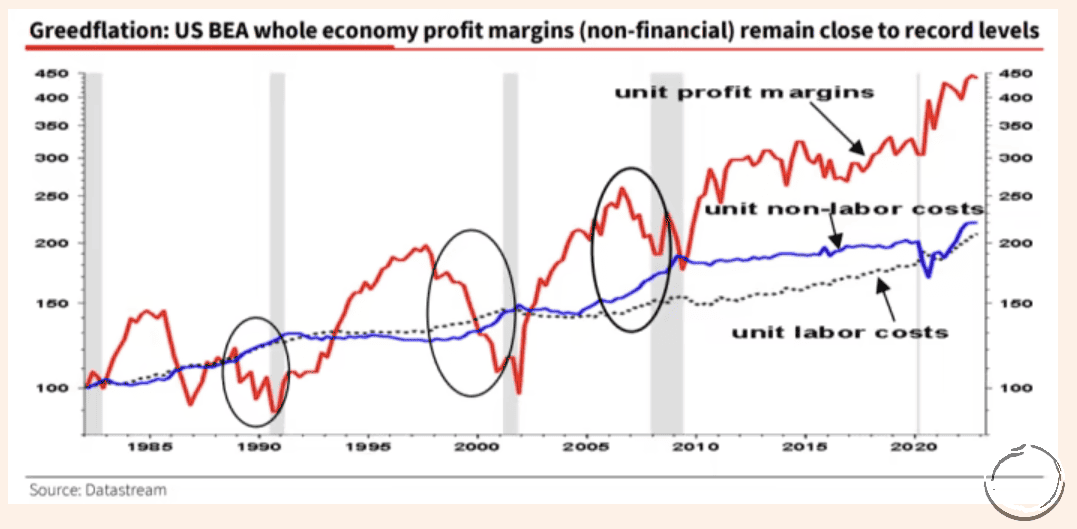

- Albert Edwards of Société Générale published a report on profit margins recently where he discussed the historically elevated profit margins we’ve seen in the US over the past 20 years, a byproduct of what Edwards calls “Greedflatoin” (h/t FT).

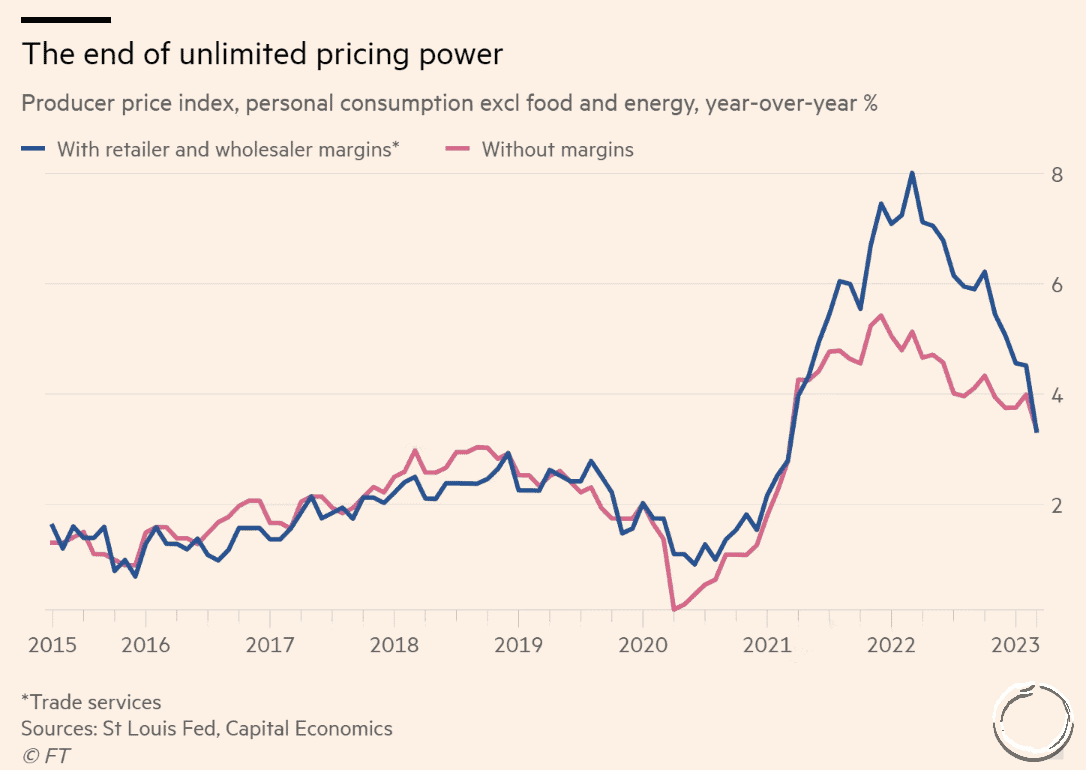

- And indeed this “greedflation” has been particularly egregious over the past two years. This chart from the FT shows the PPI with and without margins, essentially illustrating how companies used the chaos of the post-pandemic environment to collectively ramp up prices well above their rising input costs.

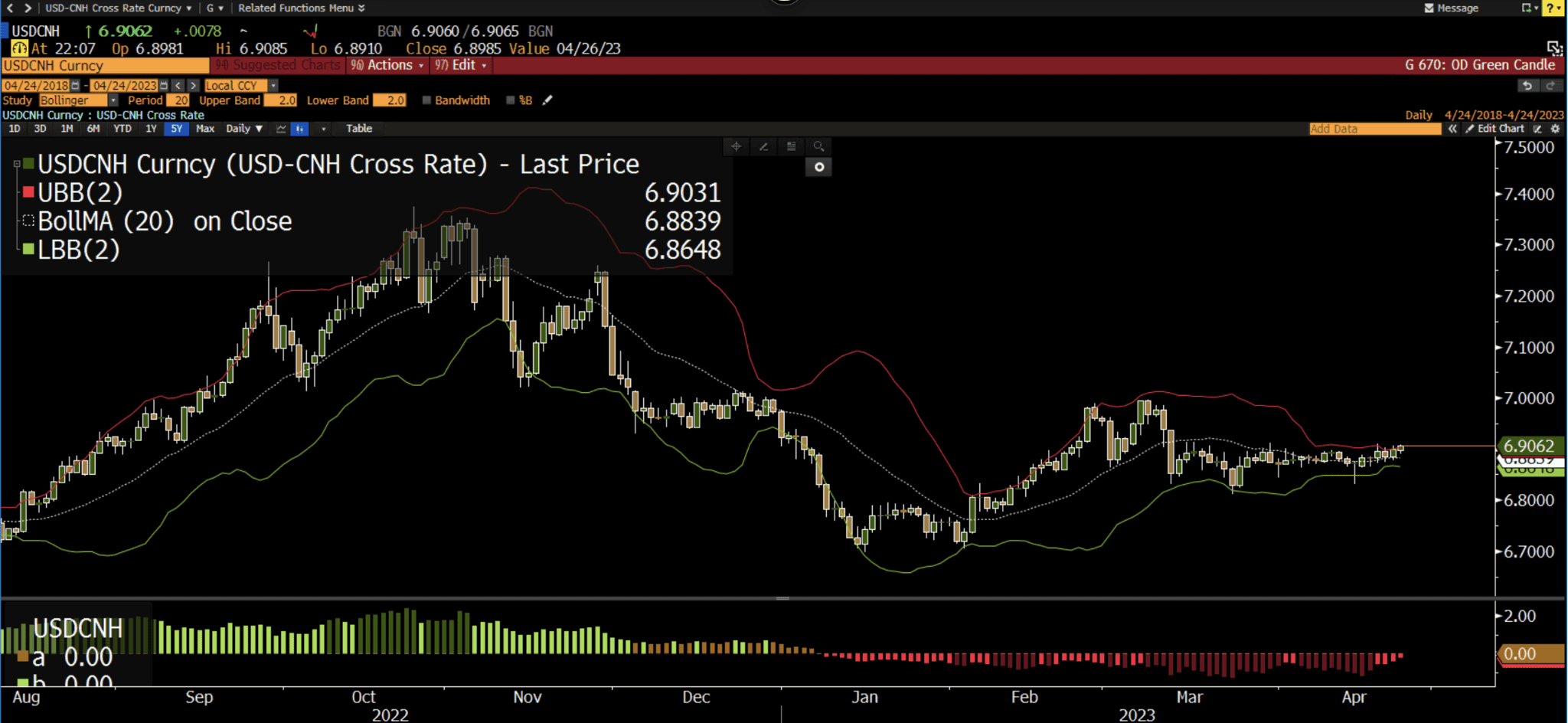

- Getting back to the USD rally trade, one pair that should be on your radar is USDCNH which is in a tight compression regime. Compression regimes lead to expansion regimes (trends). Our bias is this breaks out to the upside.