New research reveals that stock prices revert to a predictable P/E multiple, which is a function of growth and profitability. It also shows why growth stocks, while more profitable than value stocks, earn lower returns.

Q3 2022 hedge fund letters, conferences and more

Over the period July 1926-August 2022, the stocks in the Fama-French U.S. Value Research Index returned 12.7%, outperforming the stocks in the Fama-French U.S. Growth Research Index, which returned 9.8%, by almost 3 percentage points per annum. Perhaps surprising to many investors, the outperformance of value stocks occurred even though growth stocks produced higher rates of return on assets and equity as well as faster rates of earnings growth. In a series of articles (see here, here and here), the research team at Verdad provided the explanations for the outperformance:

- While growth stocks have produced higher growth in earnings, the persistence of abnormal earnings growth was not greater than would be randomly expected, leading to investor disappointment.

- Analysts’ forecasts systematically overshot the actual outcomes; their forecast errors became larger the further down the income statement (earnings available to equity investors) and the further out in time.

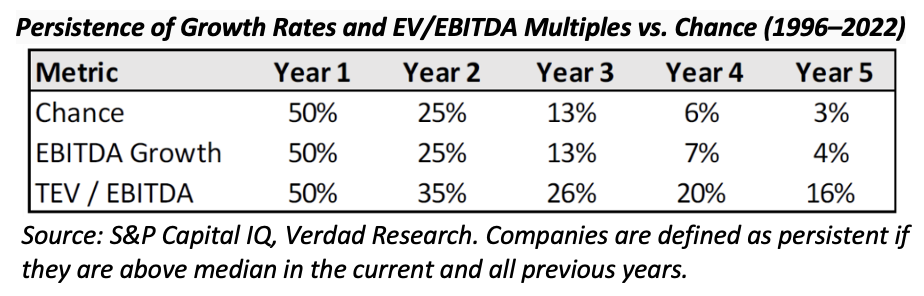

- While analysts have been too optimistic in their growth estimates, they have been able to correctly sort companies into high and low growers. Unfortunately, being able to predict that a company will produce abnormally high earnings growth is a necessary, but not sufficient, condition for generating excess returns (alpha). The reason is that it is not the forecast that matters, but the forecast relative to what is already priced in – not only have analysts been overly optimistic, but abnormal earnings growth shrinks at a rapid pace. As growth rates mean revert downward, so do valuation multiples. The result is that the benefits of strong growth in the short term are often offset by losses from changes in multiples that reflect the mean reversion of growth in the long term. As shown in the table below, valuations have been more persistent than growth:

Because valuations have been more persistent than growth even after multiple contractions, an expensive company can remain expensive relative to the market, and a cheap company can remain cheap or even get cheaper for years (as value investors experienced during the longest and most pronounced drawdown for the value premium in history, from late 2016 through late 2020, before reversing).

Read the full article here by Larry Swedroe, Advisor Perspectives.