“The experience of the Great Recession and its aftermath revealed that a lower bound on interest rates can be a serious obstacle for fighting recessions. However, the zero lower bound is not a law of nature; it is a policy choice. The central message of this paper is that with readily available tools a central bank can enable deep negative rates whenever needed—thus maintaining the power of monetary policy in the future to end recessions within a short time.” – From the IMF Working Papers – Enabling Deep Negative Rates to Fight Recessions: A Guide

“They are insane!” – Steve Blumenthal

Q2 hedge fund letters, conference, scoops etc

It got ugly this week on Wall Street; though we’re ending the week on an up note. Three main factors: the U.S.-China trade fight, uncertainty about the Fed’s interest rate policy and global economic slowing. Many of the biggest troubles sit overseas. Germany contracted in the second quarter and factory output in China came in lower than expected. The markets are signaling that the economic downturn is spreading to the U.S.

Combine an over-extended, over-valued and over-leveraged world with economic growth slowing – risk rises. This week, FactSet, a financial data and analytics firm, reported that earnings for the S&P 500 companies will grow at just 1.5% this year. This is a long way off from the 6% plus growth analysts forecasted back in January. Overall, warning signs are flashing brighter and they are pointing to a deepening global economic slowdown. Risk of recession has ticked higher.

A week ago I attended the annual Camp Kotok (aka “Shadow Fed”) gathering of economists, investment managers, former Fed officials, politicians and journalists. The fishing was fun, the food and wine excellent and the conversations invaluable. David Kotok put it this way:

The 50 person gathering at Leen’s Lodge encompassed diverse political views, financial and economic specialties, and asset classes focused from cannabis to currency trading, real estate to debt of all types, stock markets and ETFs, derivatives and futures, and more. Over $1 trillion in managed assets were represented as we gathered for each informal meal. No lectern, no PowerPoint. The China Panel and the MMT panel are public and in the social media domain and the press and public are free to use the video footage and quote the speakers. Other discussions were conducted under the Chatham House Rule.

Good friend, Dave Nadig, ETF.com’s managing director, wrote this:

Each year I attend an event in the Maine woods called, alternatively, “Camp Kotok” or the “Shadow Fed.” The former sounds frivolous. The latter sounds nefarious. Neither is particularly accurate.

The attendees at Camp Kotok are smart. Like, really, scary smart. While there are strict rules about how and what gets reported—which includes who attends—the combined résumé includes economists from governments and S&P 500 companies, CIOs, portfolio managers, politicians, best-selling authors and a handful of overwhelmed journalists.

It’s also surprisingly diverse for a finance-focused gathering—diverse politically, ethnographically, geographically. Walking into the dining hall on a Friday afternoon creates a near lethal sense of impostor syndrome. The only survival strategy is to ask questions and listen really hard to the answers.

Attendees agree to Chatham House Rule. It is a process that provides a way for speakers to openly discuss their views in private while allowing the topic and nature of the debate to be made public and contribute to a broader conversation. This year’s Camp Kotok gathering occurred at an important time. With trade and currency wars now in play — the macro picture is worsening.

I have two big takeaways from camp to share with you today. First, we need to rethink how we engage with China. I spent an outstanding two hours in the car with new friend, Jonathan Ward, author of China’s Vision of Victory. On the way to Grand Lake Stream after landing in Bangor, Maine, Jonathan took me to school. Yikes – we must wake up. We are playing small ball, they are playing long ball. Second, dare I say, Modern Monetary Theory is coming. Views were shared and stress tested. You’ll find a video of the China panel and a recording of our MMT debate when you click through on the orange On My Radar button below. Grab a coffee and get comfortable. Or, better yet, put your headphones on and get out for a nice walk. I really hope you get a feel for what is was like to be at camp in Maine.

If a friend forwarded this email to you and you’d like to be on the weekly list, you can sign up to receive my free On My Radar letter here.

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Camp Kotok Takeaways: MMT — Modern Monetary Theory and China

- China’s Vision of Victory

- Trade Signals – Keep an Eye on High Yield and Lending Conditions

- Personal Note – Camp Photos

Camp Kotok Takeaways: MMT – Modern Monetary Theory and China

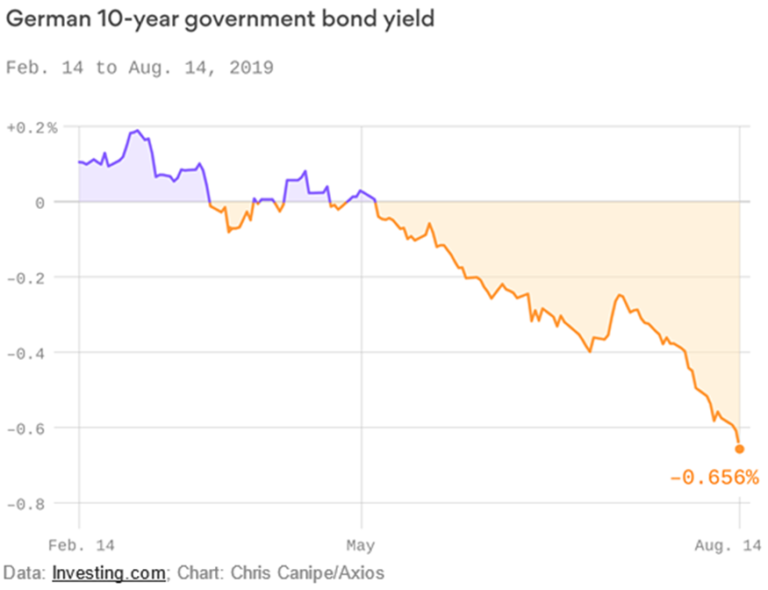

We sit at such an interesting period in time. For several years, we’ve talked about how trade wars will likely turn to currency wars. You’ve likely been hearing much about the “Yield Curve Inverting.” If you want to know more, the Economist did an excellent article explaining exactly what it means in a piece titled, “Yield curves help predict economic growth across the rich world.” In short, it happens infrequently and when it does, recession usually follows. Check – it’s happening. We see other highly unusual things, such as $15 trillion in negative yielding debt. Interestingly, all English speaking countries have debt yielding north of 0%. $15 trillion is mind-blowing. German debt is yielding a negative 0.66%. You invest your money in their government bond and you get to pay them for the privilege. Check – bad.

Yields in the U.S. 10-year Treasury Note dropped below 1.50% and the 30-year dropped below 2%. Just a few months ago I shared with you my view that the 10-year is heading to 1% and the 30-year to 2%. I’m in awe at the pace of the move.

To give you a good feel for what was discussed at this year’s Camp Kotok gathering, I share with you several key takeaways (including links to audio presentations) from David Kotok:

1. Regardless of the attendees’ political views, Peter Navarro’s advice to Trump is seen as a disaster. In a poll, 1 supported Navarro, 3 weren’t sure, and 36 disapproved. When asked more generally about Trump’s trade war policy, the group was divided, with about 3 opposed to Trump for each supporter.

2. The damage incurred by Navarro’s advice and Trump’s policy was cataloged in detail, and it is ugly. It is spreading and appearing in more and more evidence and anecdotes.

3. Border and immigration policies were discussed in detail and with data. The group’s outlook is bleak. Nearly all fault a dysfunctional Congress for its repeated failures. Here the group leaps over partisanship. Democrats and Republicans are guilty.

4. Global debt expansion and central bank credibility is a major concern. I refer readers to the MMT panel for a clear, multidimensional discussion of MMT and the Fed’s dilemma:

David’s personal takeaway is that the Fed needs to step up its game with regard to its communication strategy. More from David, “Most agreed that putting a name with each dot in the dot plot would be an easy improvement to make. If the Fed had a clear policy statement against negative interest rates, that assurance would help to reduce risk premia. The gathering views negative rates as a spreading financial malignancy. The varied forecasts about proliferating negative rates and their global effects are sobering. Kotok noted: adjusted for most recent inflation reports, the U.S. Treasury yield curve is already negative when computing real yields.

5. The China panel packed an extraordinary amount of valuable information into a half hour and is well worth the time you’ll spend to view it (click on the photo to play the video):

Beyond the direct U.S.-China trade war, attendees discussed contagion risk, Hong Kong, Argentina, capital flight and alternative choices for storing value in a world of discredited fiat money, among other issues. Most attendees expressed gratitude for an assembly that allowed for free and open exchanges.

Here are three questions for readers to consider:

- How would you restructure your investment portfolio if you really believed that the global high-grade sovereign debt nominal yield would average 1% or lower for many years? That implies real yields would be negative worldwide for a prolonged period.

- How would you restructure your investment portfolio if you believed that high-grade federal, state and local debt yield would also average 1% or lower for many years? This question implies that the entire yield curve (term structure) is under 1%. What are implications for munis, mortgages, swaps, forwards, etc.

- The third question involves geopolitical risk and personal safety. At Camp Kotok, we had private conversation on this subject. The results are alarming as many of us have altered global travel plans. I’m one of those who has done so. So here’s the question. Think about the world that you see. Then make a list of every place you have visited during your lifetime. This takes a few days for older and well-traveled folks as memories are rekindled. Then look at the list and ask which of these destinations you would visit today and which you would not. Add this consideration: Which would you visit only with ample security and protection?”

Lastly, Dave Nadig drafted an exquisite description of Camp Kotok and has given us permission to share it. Enjoy: https://www.etf.com/sections/blog/camp-kotok-wall-street-woods

We also have permission to share Brent Donnelly’s thoughts on Camp Kotok, 2019: Brent-Donnelly’s-Notes-from-Camp-Kotok-2019.pdf

China’s Vision of Victory

I was fortunate to meet Jonathan Ward at the Bangor, Maine airport. We met and drove two hours northeast to Grand Lake Stream, an isolated and beautiful part of the world. One missed flight and your travel nightmare begins. Mauldin was to meet and drive with us; unfortunately, his flight from JFK was cancelled. The rebooking found him arriving in Augusta, Maine, a much farther drive. He arrived to Camp Kotok around midnight.

My time with Jonathan was outstanding. His message? The United States, and the ideas it represents, are at risk to China’s totalitarian objective: transforming China into the world’s top power by 2049. If successful, this “will mean a world in which China is the world’s leading superpower, capable of extending its military, economic, financial and ideological influence and power into every place on earth not limited by other nations or by coalitions of nations.”

He believes we should engage with China but not enable them economically. If “the Chinese Communist Party’s strategy is intended to deliver the creation of a new world system with China at its center—and the de facto end of an American-led world,” he writes, then: “The United States and other democratic powers must strengthen our connectivity, and economic, military, technological, education, and innovation potential, in ways which enable us to build ourselves and build each other, while closing China off from access to the things that pave its way to power.”

I think he is right. Later today, I’ll be doing a podcast interview with Jonathan and will share it with you next week.

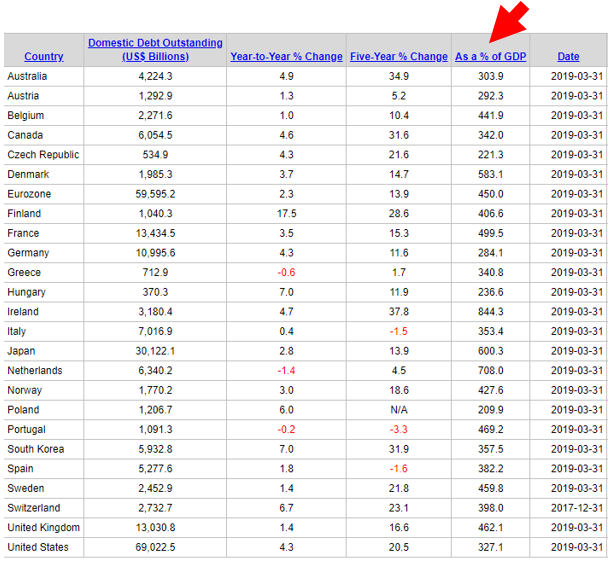

To poo poo subprime in 2007/08 was easy to do. But it sat right there in plain sight. I thought it to be a $400 billion potential problem. Losses were in the trillions. Today, over $9 trillion of debt is foreign debt funded in U.S. dollars. Much of it from China. What happens if the currency peg breaks? The first shot across the bow came last week. European banks are in trouble and -0.66% German bund yields are adding to their woes. U.S. debt-to-GDP is over 327%. Credible academic evidence says economies get in trouble when debt exceeds 90% debt-to-GDP. Look at the column highlighted by the red arrow. Debt is a problem everywhere.

Yield curves inverting tell us the patient has a fever. Perhaps something even more. Something is wrong. We don’t yet know the solution. I believe it will take a crisis to enact laws that will enable something like MMT. Make no mistake — MMT in some form is coming. Buckle up.

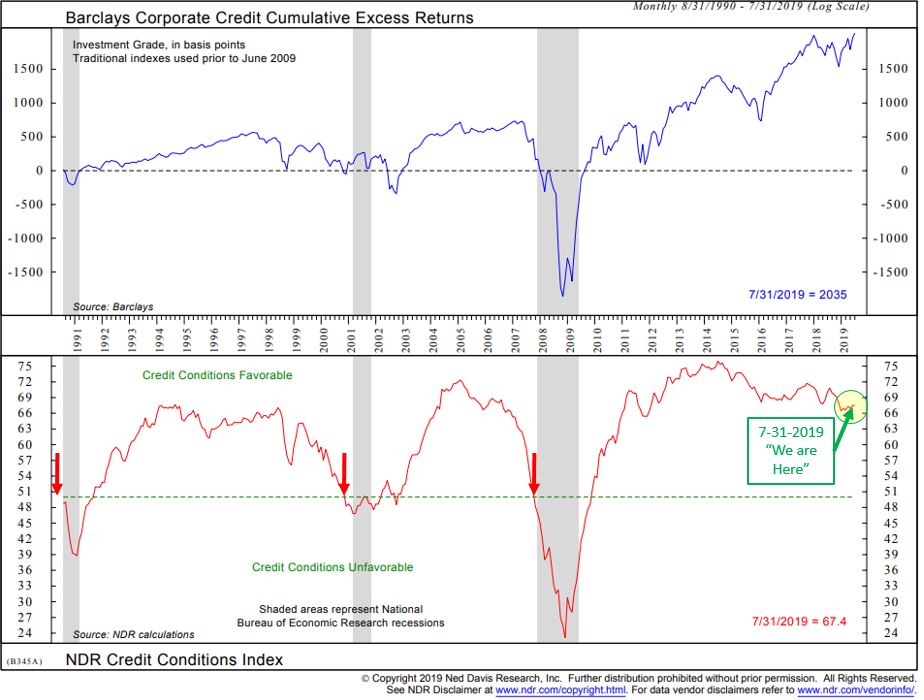

Trade Signals – Keep an Eye on High Yield and Lending Conditions

August 14, 2019

S&P 500 Index — 2,894

Notable this week:

I thought I’d share with you a few charts on high yield (HY) today. Thus, the title of today’s Trade Signals, “Keep an Eye on High Yield.” Following are three important charts (in my view). Think of these as “canary in the coal mine” like indicators.

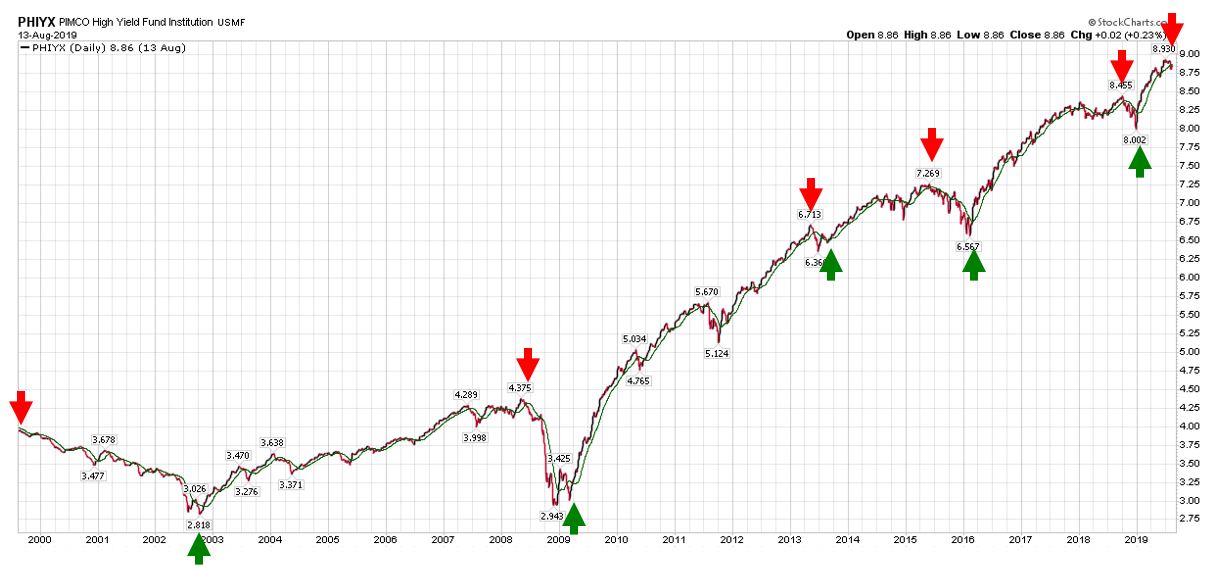

Chart 1 looks at the long-term price trend of the PIMCO High Yield Bond mutual fund. The red arrows indicate select periods in time when the price dropped below its 50-day moving average price trend line. I remember the sell signal in 1999 (red arrow far left). The stock market was racing higher and the big excitement was, of course, in tech. However, the HY market was signaling trouble ahead. Recession followed in 2000/01. Tech stocks declined 75%, the S&P 500 Index declined 50% and HY declined 32%. HY signaled trouble ahead prior to “The Great Financial Crisis” in 2008. The stock market declined more than 50% and bottomed in March 2009. HY lost 32%. The point I’m making is the trend in HY price is an excellent leading indicator. Lights on.

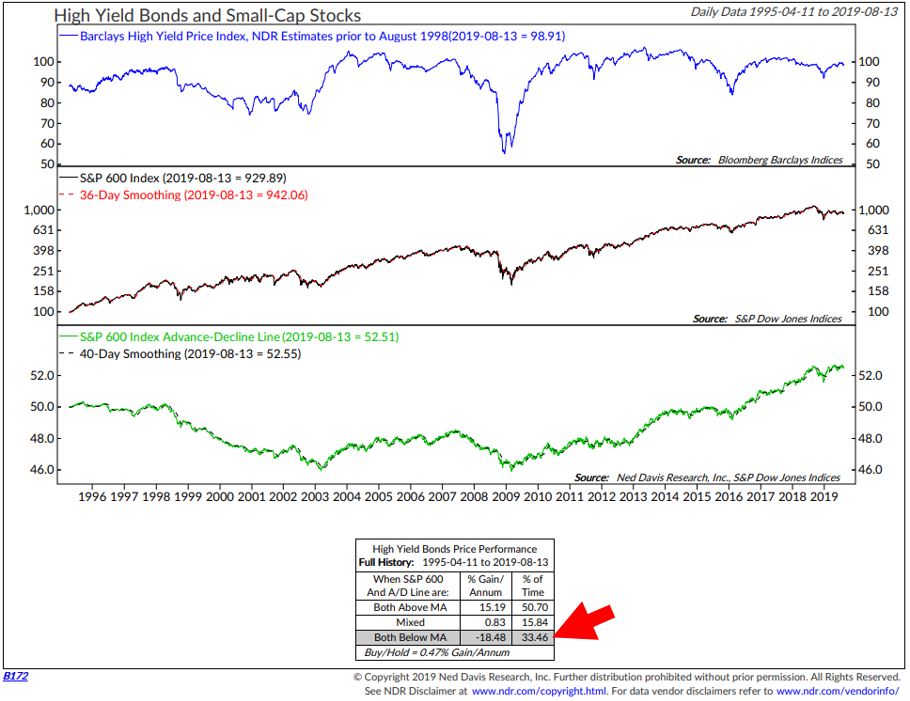

Chart 2 looks at the performance of the HY bond market by analyzing the trend in small-cap stocks. The data is in the bottom box (red arrow). When the trend in the S&P 600 (small cap) Index is up and the S&P 600 advance-decline line is above its 40-day smoothed moving average, HY bonds do best. When both price is in a down trend and the percentage of stocks advancing vs. declining is below its moving average trend line, HY bonds do worst. That is the signal we are in today.

Chart 3 plots the NDR Credit Conditions Index. The red line in the lower section plots the score of the Credit Conditions Index and shows two regimes: “Credit Conditions Favorable” and “Credit Conditions Unfavorable.” Note how the red line dipped to “Unfavorable” prior to the last three recessions. The reason I believe this chart is important is that when lending dries up, all the bad stuff happens. Companies living on debt are unable to gain more financing and defaults happen. Such events are infrequent but given today’s starting conditions (record corporate debt and very poor covenant protections on bonds), I believe the next dislocation will see HY bond prices decline more than 50%. Yields will spike to the mid-20% range. A problem if you get run over. An opportunity if you have a disciplined investment process in place that gets you to safety. The current HY sell signal may or may not mark the top but Credit Conditions are Favorable so that’s good. Stay tuned.

Trade and currency wars are in play. The S&P 500 Index is down over 2% at the time of this writing. The equity market trend signals are weakening but remain in buy signals. The Zweig Bond Model and gold market signals remain bullish. As mentioned, HY is in a sell signal.

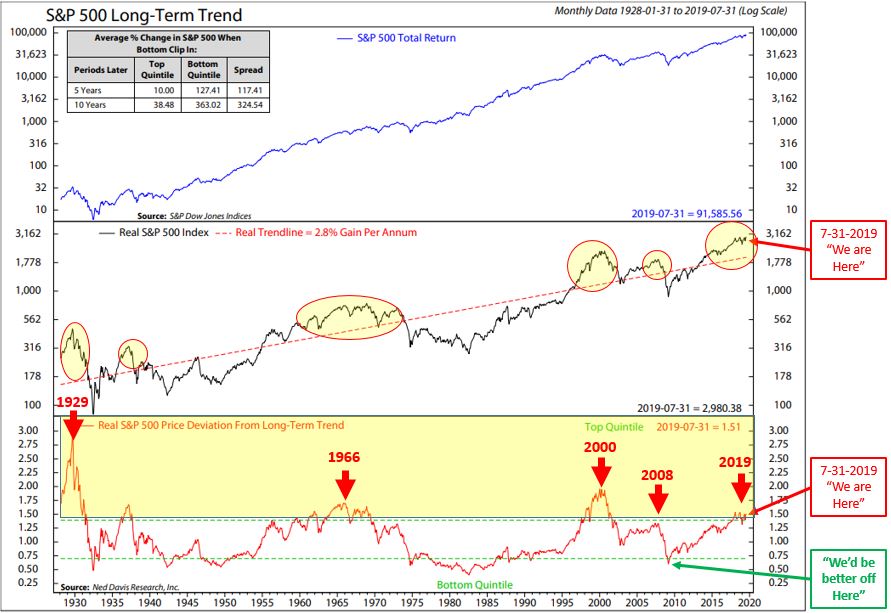

I shared the next S&P 500 Index Long-Term Trend chart with you last week. The S&P 500 Index sits well above its long-term trend line. Bottom line: Expect low returns in the coming five to 10 years. The stock market is richly priced. Here is how to read the next chart:

History presents many data points that can help us measure periods of opportunity and periods of risk. The chart looks at the long-term trend of the S&P 500 Index in relationship to its long-term trend line from 1928 to present.

- Focus in on the middle section of the chart. The black line is the S&P 500 Index price line and the dashed red line is the long-term trend line of the S&P 500 Index. You can see over time the market moves above and below the long-term trend line.

- The lower section measures the deviation from the long-term trend line. The yellow circles in the middle section highlight periods above the trend line (note the red “We are Here” arrow. The bold yellow highlight in the lower section highlights the “Top Quintile” of deviations above the trend. Simply, the periods when the stock market is farthest above its trend. I’ve notated prior periods. Excessive investor speculation bids up prices or investor panic sends prices lower.

- Over time, we should expect to do well with our equity investments and slope upward in line with the trend. This measure is informative in terms of periods of excess. Best to be aggressive buyers when below trend (the bottom quintile: “We’d be better off Here” green arrow). Best to be cautious (risk manage and underweight equities) when in the top quintile such as today (the red “We are Here” arrows).

- Finally, take a look at the data box in the upper left corner. This supports this reasoning. Note the returns five and 10 years later when in the Top Quintile vs. the Bottom Quintile. Top Quintile: five years later, a return of just 10% ($100,000 grows to just $110,000) and 10 years later grows only 38.48% ($100,000 grows to $138,480). That’s an annualized 10-year return of less than 3% per year. Now note the returns in the Bottom Quintile: five years later — a return of 127.41% ($100,000 grows to $227,410) and 10 years later a return of 363.02% ($100,000 grows to $463,020). Clearly, there are times to be more and less aggressive.

Source: NDR

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for this week’s Trade Signals.

Personal Note – Camp Photos

The one-on-one and group discussions are so helpful for me. David and I talked trading strategies at 6:30am with coffee in hand. A great spot for a morning coffee. And I really like what he’s doing… we will talk more. A big thank you to David Kotok and team. Camp Kotok is outstanding. Much appreciated!

Ben’s brilliant. Follow him on Twitter @EpsilonTheory

Thanks for indulging me. I get why people love the lake. A fun time. Wishing you relaxing time at a beach or a lake or a mountain. Somewhere you can decompress, slow down and have fun. I do hope this note finds you with vacation plans. Here’s a toast to you, to life, to joy and to those you love most. Have a great weekend.

Best regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO