PM Bill Hench details where he is finding opportunities for our Deep Value Approach and how volatility has affected his portfolios’ weightings.

Q3 2019 hedge fund letters, conferences and more

How did you manage the portfolio during the volatile 3Q19?

Traditionally, this Fund has taken advantage of very volatile times. The liquidity allows us to really dictate more often than not what we want to pay for positions. So when we do get extreme volatility on those down days, we tend to get very good bargains. And quite frankly, you have to have those down days to make money over the long term because you’ve really got to position yourself for that upside. And the best way to do that is to buy during those very ugly times.

If you’re looking for more timely hedge fund insight, ValueWalk’s exclusive newsletter Hidden Value Stocks offers exclusive access to under-the-radar value hedge funds and their ideas. Click here to find out more and signup for a free no-obligation trial today.

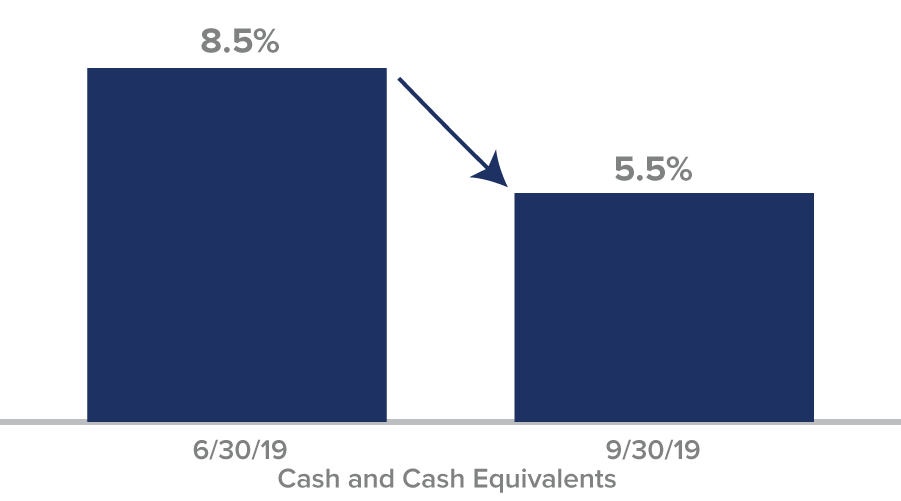

Putting Cash to Work

Opportunity Fund Cash and Cash Equivalent Weighting

How has volatility affected sectors and micro-caps?

During this latest battle with volatility, the industrial sector seems to be taking it a little bit harder than the rest of the market, which makes sense. There are questions about not only U.S. growth but global growth as well. So, a lot of the volatility or downward volatility I guess you’d say is coming on the industrial side.

During times when growth is questioned, the micro-caps usually do the worst. So I think right about now the portfolio is doing what it normally does during periods like this. We’re probably 60 or so percent invested in names that are under $1 billion in market cap and I suspect that that’ll continue to climb a little bit.

How is being later in the economic cycle affecting where you’re finding opportunities?

I think we are late in the cycle. You always get opportunities no matter where you are in the cycle. In this particular cycle, you’ve got very low interest rates, exceptionally low unemployment, and a U.S. economy that’s a little bit stronger than the rest of the world. As we’ve done in the past, we tend to find sectors within the economy during cycles that can do better.

One of the things we do is look for things that are growing maybe in parts of the economy or growing at a given time or a given part of a cycle. One of the things that’s worked really well for us has been housing, so well indeed that we’ve actually pared back some of the investments in there. The recipe for good housing remains the same and those things are really evident in today’s economy.

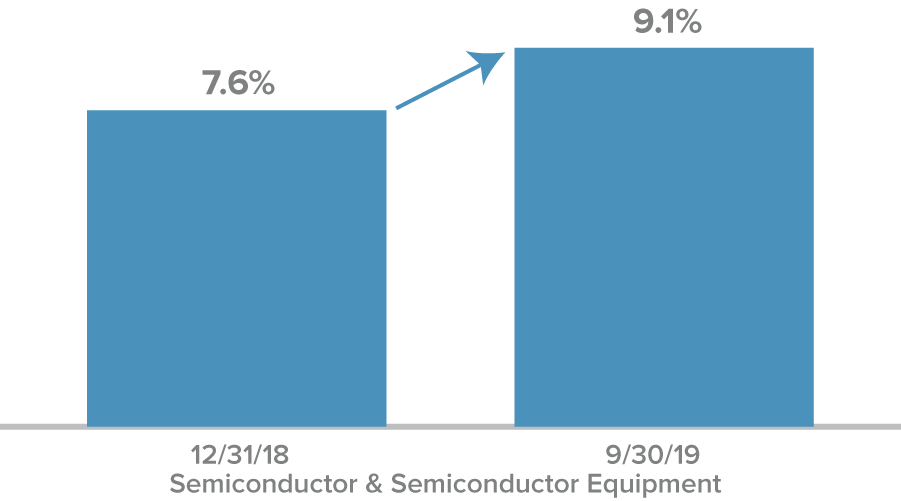

The semiconductor group is one that we’ve traditionally had a lot of success with, and that hasn’t changed. Most of the companies’ customer bases have changed over the last 10 years. It’s much more spread out, much more reliance on the general economy, and less reliance on hit products and sort of tech-only end markets.

Pursuing Semiconductor Opportunities

Opportunity Fund Semiconductor & Semiconductor Equipment Weighting

So this has been very good for the companies. It has taken a lot of the boom/bust mentality out of the sector, therefore for us, we’ve had about a 50/50 I think split between the semiconductor devices and the capital equipment side. Both seem to be doing pretty well, and luckily for investors like ourselves we get to see what the really big players in the industry are doing. And we clearly don’t see any sort of bust coming. Inventories are in good shape. Investment hasn’t been overdone. So it, it should be a pretty good period I think for the semiconductor industry.

This transcript has been edited for clarity.

Article by The Royce Funds