Takeaway versus Home-Cooked Investing

Q1 hedge fund letters, conference, scoops etc

This research note was originally published in the Beyond Beta magazine from ETF Stream. Here is the link.

Summary

- Single factor excess returns are attractive over the long-term, less in the short-term

- Comparing popular asset allocation models does not highlight one superior methodology

- Multi-factor portfolios generated excess returns in two out of three regions since 2008

Introduction

Obesity rates in countries like the US or New Zealand are north of 30%, which increases health issues such as diabetes and effectively reduces life expectancy. The citizens of these countries should do everything within their powers to reduce their daily calorie intake.

Unfortunately, new companies like Uber Eats are making it more convenient to order takeaway food, which tends to be less healthy, more expensive, and contain more calories than when cooking at home.

Factor investors face a similar choice between buying ready-made multi-factors products or creating these themselves. Multi-factor ETFs might be a convenient solution for harvesting returns from various factors, but these are more costly than single factor ETFs and are often challenging to analyze.

Alternatively, investors can directly select single factor products and create custom portfolios, either by allocating on a discretionary or systematic basis. The simplest form of the later might a portfolio that allocates equally across smart beta strategies, but it is questionable if that is an optimal allocation model.

In this research note, we will apply four well-established asset allocation models to smart beta strategies and evaluate if smart beta would have enabled investors to outperform the markets.

Outsmarting The Market

The rise of factor investing is based on the broad effort to make investing more scientific, which has become easier given cheaper, better data and new technologies. Research by academics and finance professionals principally supports five factors namely Value, Size, Momentum, Low Volatility, and Quality. Dividend Yield can be considered a (poor) version of Value while Growth is a widely-followed investment style, but lacks backing from research.

These seven smart beta strategies have become available via smart beta ETFs at affordable prices and gathered approximately $1 trillion in assets.

However, some strategies like Low Volatility were launched as ETFs only in recent years and have a limited price history. We, therefore, create smart beta indices going back to 1990 by selecting the 30% of stocks ranked most favourably by the factor definitions, which are in line with academic and industry standards. When we benchmark these theoretical smart beta strategies with the track records of live smart beta ETFs, they show only minor tracking errors.

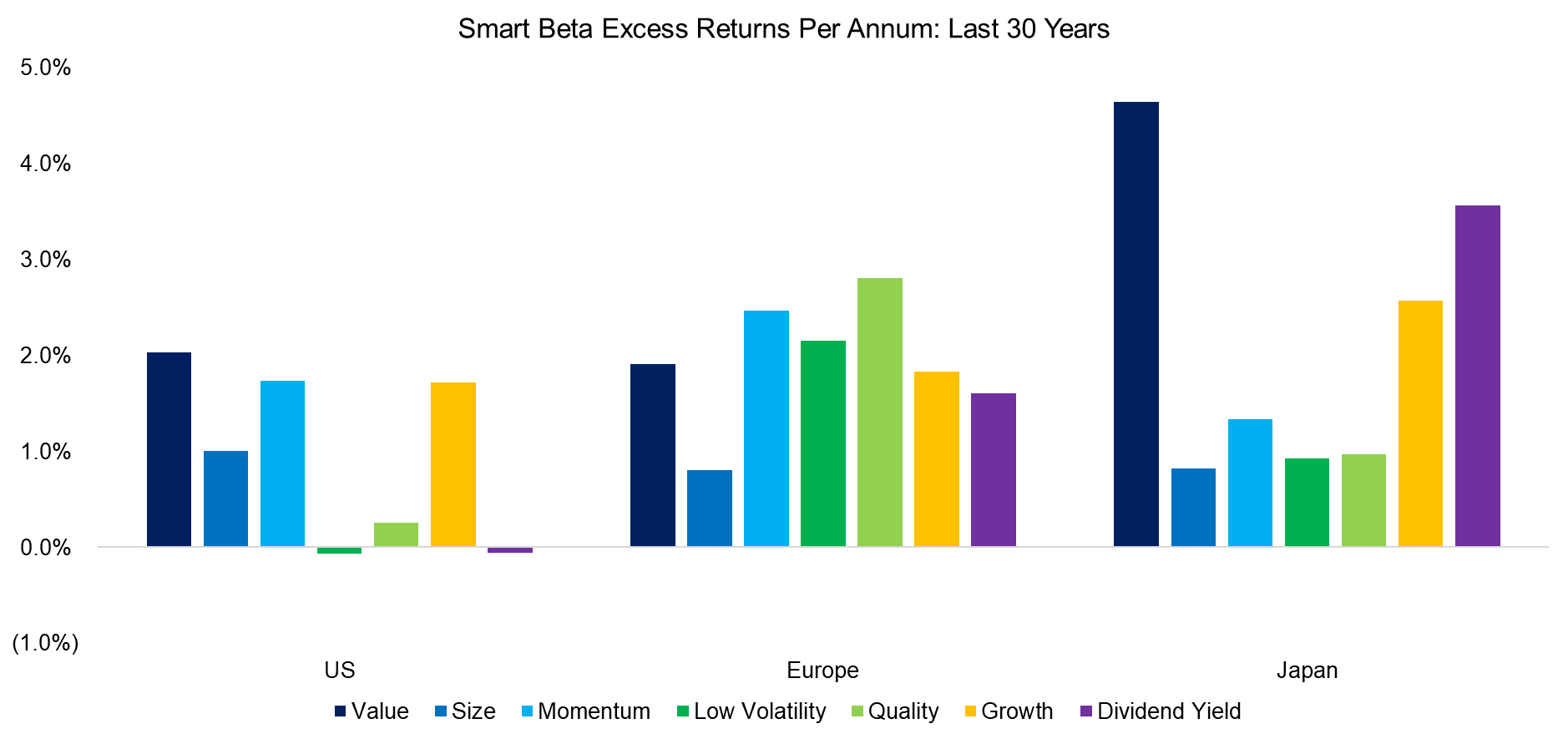

Reviewing the performance of these seven strategies over the last three decades reveals that most generated alluring excess returns that explain the interest in smart beta. Based on these results, an investor might conclude that simply allocating equally to all the strategies might create an attractive portfolio for harvesting factor returns.

However, an astute observer might be perplexed as nearly all strategies outperformed the markets. In Europe and Japan, any of these smart beta strategies would have been better than plain beta. Is it that simple to beat the market?

Source: FactorResearch

Research like the S&P’s SPIVA Scorecards highlights that more than 80% of the fund manager have failed to beat their benchmarks when measured over five years or longer. Perhaps these fund managers have not explicitly followed factor-based strategies, but the lack of performance needs to be reconciled with the high excess returns from the smart beta strategies.

A simple explanation might be cost. Mutual funds have reduced their fees below 1% in recent years, mainly due to the pressure from cheaply-priced ETFs. However, active fund managers like Fidelity have historically charged management fees above 2%, which consumed most excess returns and explains the failure to beat benchmarks. Naturally, smart beta ETFs come to the rescue as they are much more affordable than mutual funds.

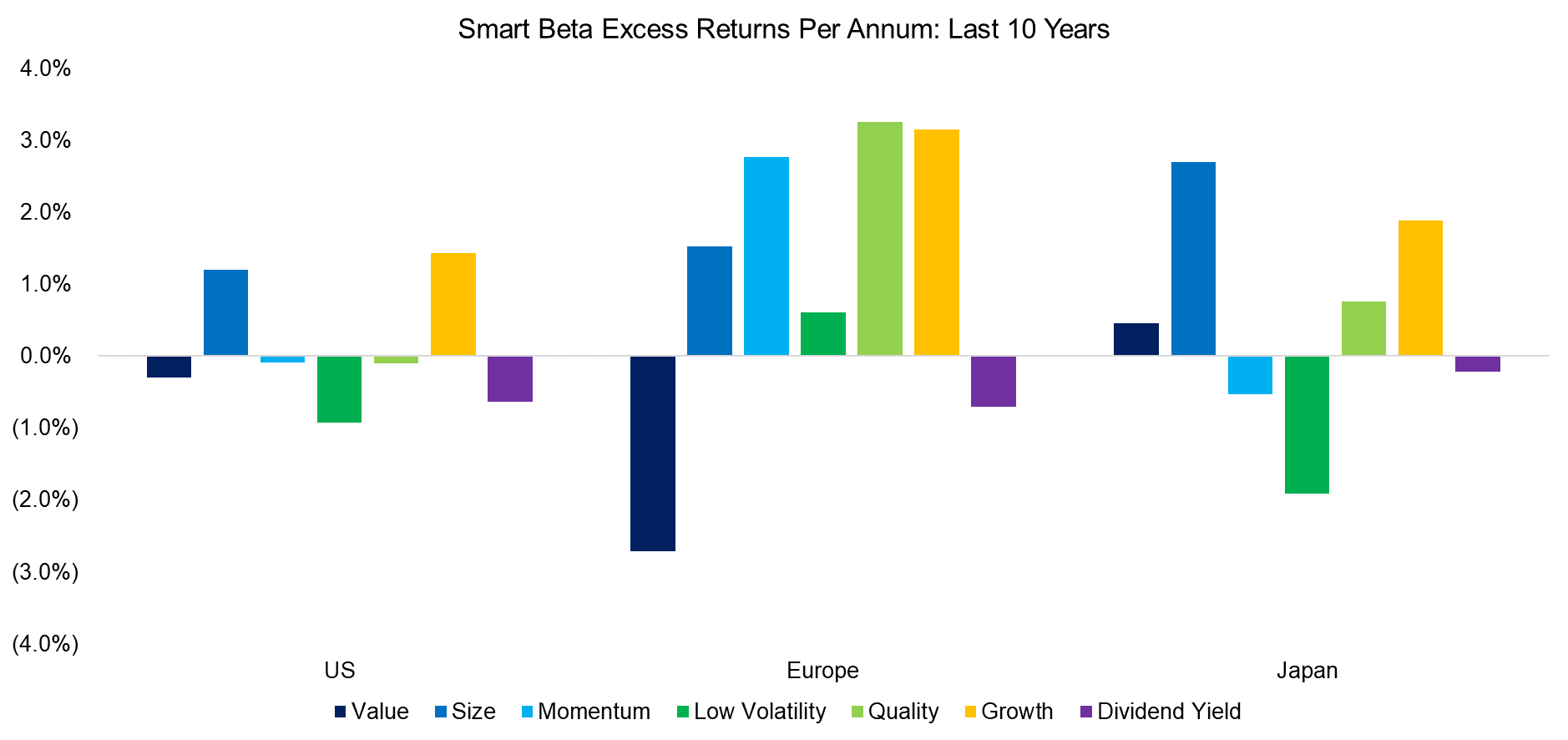

A second reason why the 30-year smart beta excess returns should be regarded with some skepticism is that the observation windows matters. If we rebased the same strategies in 2008 to highlight the excess returns for the last decade, then these look far less attractive.

Source: FactorResearch

The academic research highlights that only a few factors generate abnormal returns across time and even these are highly cyclical with long periods of underperformance. Investors should, therefore, have a long-term view when considering factor investing. Given that smart beta strategies might be less attractive over short periods, it raises the question of how to optimally harvest these returns.

A Horserace Of Asset Allocation Models

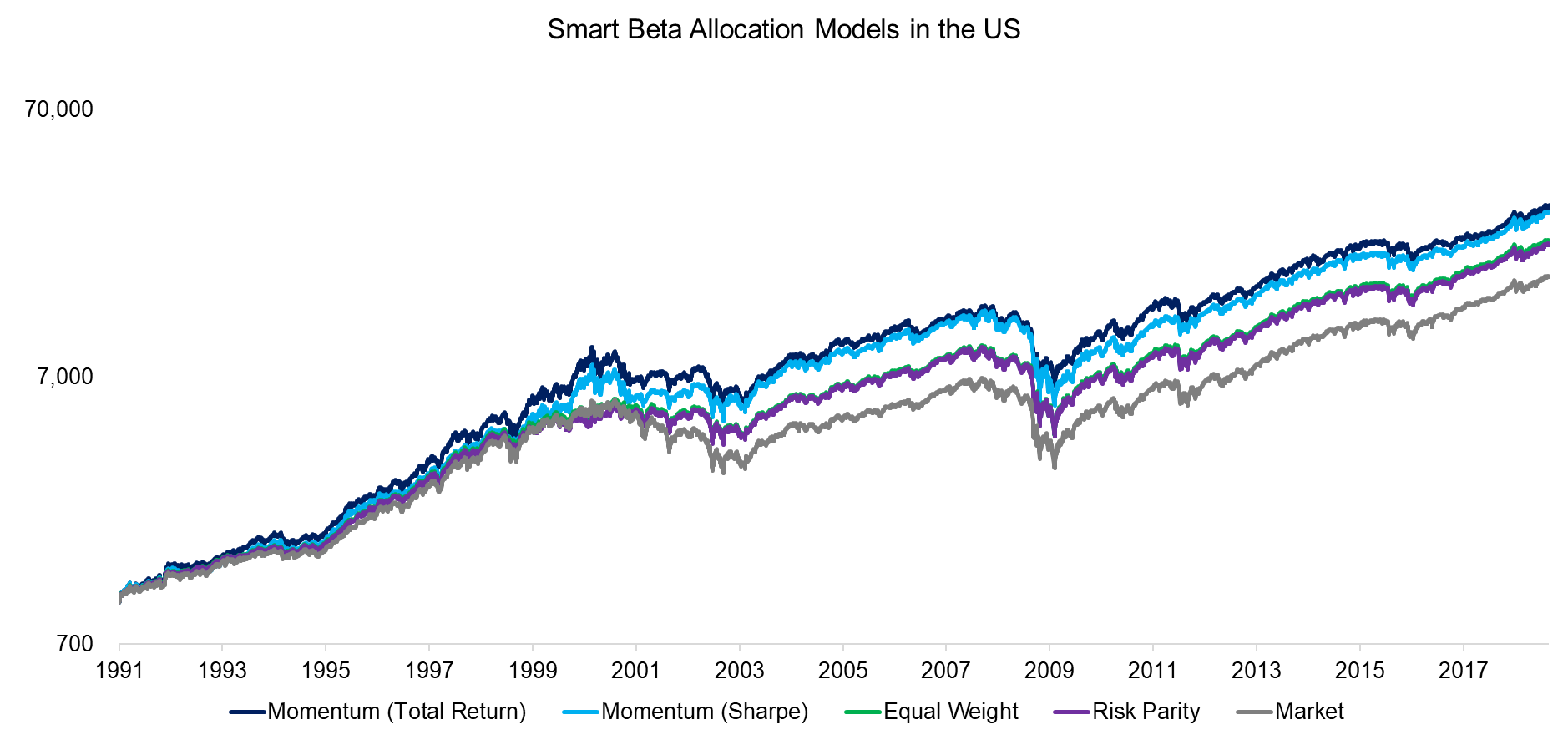

There are many asset allocation models that can be considered for creating a multi-factor portfolio out of smart beta strategies. We will evaluate the following four models, which are well-established frameworks:

- Momentum (Total Return): The total return of each smart beta strategy is measured over the last 12 months and the best three out of seven strategies are selected, receiving equal allocations.

- Momentum (Sharpe): The Sharpe ratio of each smart beta strategy is measured over the last 12 months and the best three out of seven strategies are selected, receiving equal allocations.

- Equal Weight: Each of the seven strategies receives the same allocation.

- Risk Parity: The weight of each strategy is determined in inverse proportion to its volatility, which is measured over the last 12 months.

If we focus on the US, we observe that all multifactor portfolios outperformed the market since 1991, which is expected given that most of the smart beta strategies generated excess returns on a stand-alone basis. The two Momentum-driven portfolios generated the highest returns while the Equal Weight and Risk Parity portfolios show a lower and almost identical performance. The difference between the models was especially large around 2000, where the Momentum-driven portfolios allocated to Tech stocks via exposure to the Momentum, Growth, and Quality factors.

Source: FactorResearch

Allocating to a multi-factor portfolio of smart beta strategies in Europe and Japan also resulted in returns above the market, regardless of which asset allocation model was utilized.

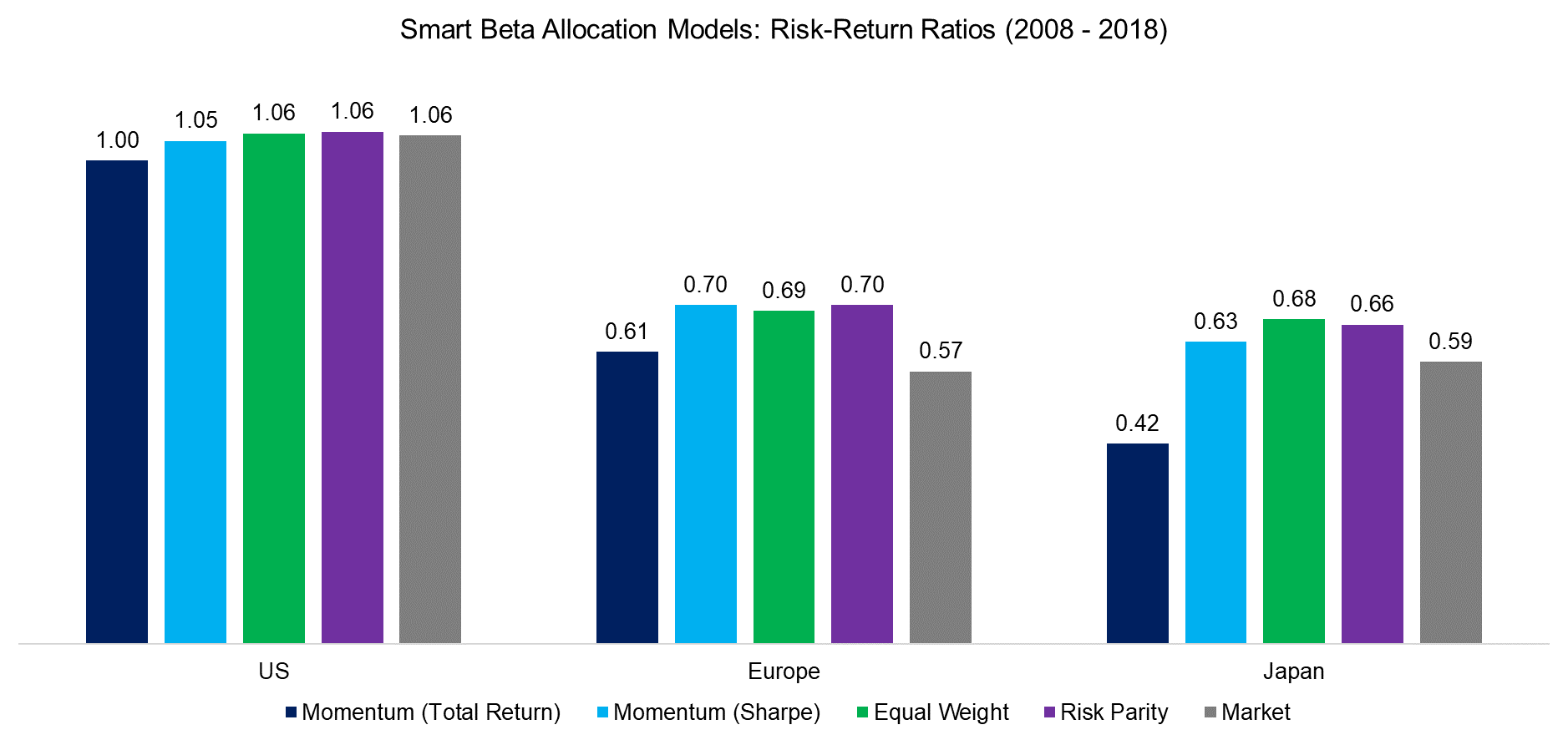

However, as noted earlier, these strategies performed far less attractively in the last decade. We, therefore, compare the four asset allocation models from 2008 to 2018 and change the perspective to risk-adjusted returns.

The results continue to favour allocating to smart beta strategies as the risk-return ratios of the multifactor portfolios were higher than those of the market in two out of three regions. However, none of the asset allocation models can be considered superior, even the simple equal-weight model performed well.

Given the marginal differences between the allocation frameworks, investors should evaluate other characteristics such as the model complexity or transaction costs and tax implications as some like Momentum feature higher turnover.

Source: FactorResearch

Further Thoughts

Some investors have started to turn away from smart beta strategies as performance has been disappointing. The popular Value factor has generated negative returns since 2009 and last year even diversified multi-factor portfolios performed poorly.

However, there are no good alternatives for investors that are mandated to beat their benchmarks. Investors should focus on harvesting factor returns as efficiently as possible, but with the perspective that factors are as cyclical as equity markets and require a long-term view.

RELATED RESEARCH

ABOUT THE AUTHOR

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Connect with me on LinkedIn or Twitter.

Article by Factor Research