Summary

- FTR is down about 97% in the last 5 years as the company’s massive $17B debt load and out of date infrastructure has turned off potential equity investors.

- We examine the company’s debt maturity schedule and free cash flow estimates to arrive at the conclusion that it may not be the bankruptcy story the equity is pricing in.

- If the company can dodge its bankruptcy risk, which we believe is possible, the equity could stand to have massive upside by 2021.

- We explain our reasoning.

- Looking for more? I update all of my investing ideas and strategies to members of Geo Microcap Insights.

Q4 hedge fund letters, conference, scoops etc

Introduction: A 97% Ride Lower in Three Years

There may not be a more hated stock than Frontier Communications (FTR).

The idea was brought to us by friend and contributor Adam Spittler (email: a_spittler@hotmail.com), and with his help we took a deep dive into the company’s debt maturity schedule and potential to generate cash over the next couple of years. We arrived at the conclusion that the equity should be viewed essentially as a call option at this point, but that there is a favorable enough risk/reward profile for us to consider a small speculative investment in the name.

If you know the story or have seen the stock chart, chances are you probably hate it. If you don’t know the story, after about 2 minutes of reading, you are most likely too scared to dig deeper. Here’s what the stock’s performance has looked like over the last 3 years. The equity is down about 97%.

The History

To better understand what happened to Frontier, one must understand the history and underlying technology of the company. Note that I am not a radio frequency engineer, so this explanation is a bit “lay”.

Frontier is a Telco, or legacy telephone company, cobbled together from a bunch of disparate networks, no different than Verizon or AT&T’s legacy telephone network. Telephone “data” is transmitted via low voltage electrical current through copper wire called twisted pair. Anyone who has cut through a telephone line can see the small strands of copper inside of it. As the signal travels through the twisted pair copper line, there is friction, which reduces the speed at which data can travel. The bigger (or thicker) the copper line, the more data that it can carry.

To oversimplify, think of the smallest wire being the old line you plugged into your land line phone, and the largest, a year 2000 era T1 trunk handling data to a cell site, or to a large business. The twisted pair copper is held within a cardboard sheath, then covered in rubber to keep moisture out. Air (primarily nitrogen) is fed through the copper line to keep moisture at a minimum.

As telephone networks are many decades old and as the rubber outer coating begins to dry rot, moisture permeates the inner copper and causes severe signal leakage. When this happens, the affected span of copper has to be completely replaced, resulting in significant network maintenance fees annually. This is the same regardless of whether the utilities within the municipality are aerial (on telephone poles) or underground (in innerduct).

In the 80’s and 90’s, companies began to overbuild the legacy telco networks with coaxial cable as a means of providing more data at faster speeds. Coaxial cable is similar in makeup to twisted pair, however the copper core is solid. This allows the low voltage electrical cable to reduce friction, thereby increasing speed. This presented a problem to the legacy telcos: not only were they small and segmented, post AT&T breakup, but coax technology wasn’t compatible with telephone, meaning they would have to build a completely separate second network to upgrade to the new technology, which at the time was only marginally faster and more efficient than telephone.

A superior technology wouldn’t be deployed en masse until the early 2000’s, with Verizon building Fios Fiber to the home (FTTH). As a result, the telcos (save for VZ and AT&T who expanded into wireless) did the same thing they always did: focused on long distance subscribers and paying a hefty dividend that their shareholders had grown accustomed to receiving.

As the wireless industry grew and a new generation grew up in the mobile phone era, long distance subscribers began to decline, however many telcos were able to offset revenue contraction with their newly offered DSL service and video packages. In the early 2000’s, all of these legacy telecoms reached a significant dilemma. With fiber technology proving superior to both legacy copper and coax, everyone could see the future, however many of these firms had paid out so much in dividends, their balance sheets were still overloaded with debt, while their primary competitors, the cable companies, had spent their capex on a newer network and were able to focus on ways to compress data and improve speeds with many years of viability on their new networks.

Verizon was the first to build fiber to the home with its Fios product. After spending billions on building out select markets, they experienced something they hadn’t factored into their equation: the cost to keep a legacy copper network running alongside a new fiber network was astronomical, and their legacy franchise agreements with each municipality forbade them from forcing customers off of copper and onto fiber, particularly in rural areas where the losses to keep existing copper active were starting to take their toll.

By the end of the 2000’s it was apparent that legacy telcos offering 12 Mbps DSL, regardless of the price, were never going to be able to complete with a competing Cable or Fiber provider offering speeds in excess of 100 Mbps. While the strategies varied, some began to build fiber over their legacy network as financing afforded, and others went for economies of scale (this is what FTR chose). One thing remained constant: they all continued to pay large dividends with highly levered balance sheets.

This is where Frontier comes into play. Frontier was a small rural telephone company focused on long distance subscribers. Maggie Wilderotter was Frontier CEO from 2004 through 2015 and came from AT&T. Her focus was simply adding long distance subscribers because the legacy network was in place and the return on investment was astronomical, as the cost per incremental subscriber was virtually zero.

The problem with her strategy was that while focusing on a dying business, her strategy was to neglect developing fiber and new technologies to better complete with Coax and Fiber, and to make it up with scale.

The first significant acquisition was in 2009 when Frontier announced it was going to acquire 4.8m landline subscribers from Verizon for $8.6 billion. This was after two other firms who acquired legacy copper network pieces from Verizon had gone bankrupt. Verizon knew what they were doing and understood the technology was on its last legs, but Frontier needed the scale, and regardless of the price, they may not have had a choice. After leveraging the company, Wilderotter insisted on continuing the dividend. Frontier was forced to reduce their dividend in Q3 2010 and again in Q1 2012, before a large cut in Q1 2017 followed by complete elimination by year end 2017.

The second large acquisition occurred in October of 2014 when she acquired AT&T’s DSL and U-verse business in Connecticut. U-verse was AT&T’s attempt to build fiber closer to the house in order to improve DSL speeds. Think of it as fiber ¾ of the way from the head end to your house and legacy copper the remaining ¼ of the way. You have massive data flowing through the fiber and when it converts to copper there is a rapid slowdown of the RF signal, however this methodology does improve end user network speed and performance.

The final shoe to drop was announced in February of 2015 when Frontier announced an agreement to buy Verizon’s legacy copper and FIOS networks in California, Texas, and Florida. This acquisition included 3.7m telephone, 2.2m broadband and 1.2m FIOS video subscribers for the bargain basement price of $10.54 billion. Of note, only an estimated 54% of homes acquired (total potential customers) were FIOS enabled. Frontier used that as a sales pitch, but it was really a capital expense liability and provides opportunity today, which we will touch on later. In addition, Frontier had to spend ~$350m in integration capex to allow the networks to talk to each other.

After 11 years with the company, Maggie had managed to encumber the balance sheet, while cutting the dividend in an environment of contracting long distance and basic telephone package subscribers. For that we say bravo, however other investors may use a different adjective.

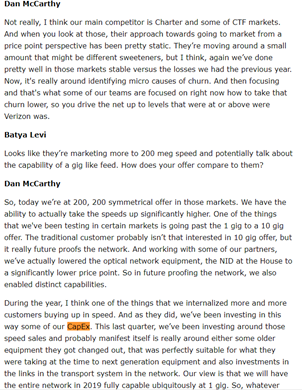

Dan McCarthy was promoted in early 2015 and took over in earnest in early 2016 after Maggie left as Executive Chairman. Dan’s background as COO included a significant amount of time in field operations, which is vital to Frontier’s go forward strategy and execution. Since Dan has taken over, Frontier had to execute integration of the CTF (California, Texas, Florida) acquisition and address the network competitive mismatch as years of neglect and lack of upgrade saddled many customers with a 12 or 24 Mbps DSL option, while Charter, for example, was offering 100 Mbps service in the same markets.

While we appreciate the criticism of the current management team, the task at hand takes time – a lot of it, as Frontier is forced to overbuild fiber closer to the home in order to reach the 100 Mbps competitive speed offering.

The Opportunity

Frontier Communications is an over-levered legacy telecom with $252m of equity value and ~$17b in debt. No one would dispute that Frontier is priced for bankruptcy. The fasted way to BK is to over lever and have revenue contract on you, and that’s precisely what has happened to FTR over the past three years. Everyone hates Frontier for various reasons, and we’re here to explain why we think everyone is wrong.

For Frontier, free cash flow is the key to the equation. While 2018 has been disappointing from a FCF perspective, their Q3 full year guidance is $625m after capital expense and interest expense. While many debate that their capital expense isn’t sustainable while covering debt maturity, I argue otherwise.

Churn rates have improved and revenue contraction QoQ has declined significantly to under 2% in Q3 2018. The most important part of growth execution is to push fiber closer to the premise to offer a competitive 100 Mbps option to challenge Charter and other cable companies. I anticipate that the large overspend on capex in Q3 2018, in tandem with the company’s rebranding, was an effort to push 100 Mbps service to as many customers as possible and reverse the trend of declining revenue and EBITDA.

Another area of revenue growth is due to many of the legacy CTF “sweetheart” Verizon teaser deals expiring. In 2015, Verizon was offering a 3 year introductory discount price, and all of those will convert to full price subscribers by ~April 1, 2019. While this may drive some churn, its already in the historic numbers as these contracts run off, which should provide tail winds to improved churn rates.

In October of 2018, Frontier changed their pricing structure similarly to a change made in Q4 of 2017.

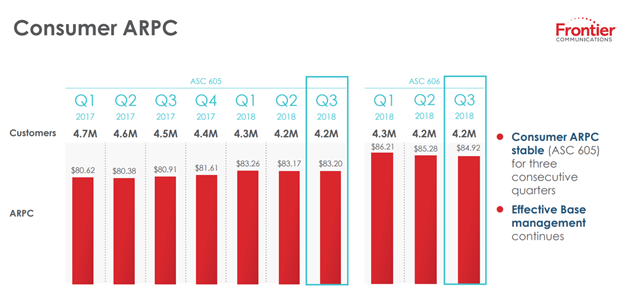

In Q4 2017, Frontier added a $1.99 network service fee, which increased their ARPC from 81.61 to 83.26. While this may not seem like much, $2 per month on $4.2m subs adds up very quickly and falls straight to the bottom line. In October 2018, Frontier announced this network service fee was increasing from $1.99 to $3.99. They have also transitioned away from allowing customers to buy their own modem and charge $10 a month. While this may seem annoying to customers, it is happening across the board to allow networks to be upgraded.

Lastly, as Frontier upgrades service regions from legacy DSL to 100 Mbps service, ARPC will increase due to the price of the upsell.

On the cost side there is one very important opportunity that most, if not all, non-industry folks fail to factor in. Historically franchise agreements between the telco and municipality have been inflexible and forced migration (from copper to fiber) initiatives have been nonstarters. Since 2015, many of the legacy telcos have made inroads with negotiating improved service for the right to transition subscribers off of legacy copper to fiber, and if the ROI doesn’t make sense, outright refuse service once the legacy contract expires (Termed as fire the customer).

While this process will extend another 5 years, once the copper network losses are eliminated, FCF will increase dramatically as legacy network maintenance and capex cost decline significantly. While there is no way to quantify what these savings may be, it’s fair to assume that at least 50% of capex is tied to the legacy copper network. While that figure may never be zero, it’s easy to see a few hundred million coming out of that in the CTF markets alone. This is referred to as a network transformation plan.

Yet another tailwind is the merger of Charter with Time Warner’s cable assets and Brighthouse Networks. While this seems counterintuitive, this is a massive integration and all three companies are trying to understand what the future go-to-market looks like. They have also reduced marketing expense until they figure things out. This should provide at least another 6 months of benefit to FTR provided they are offering a comparable product speed.

Lastly, many of you have heard about people “cutting the cord”. There is a certain stigma that cord cutters will approach 100% of former subscribers for all providers, but this is a fallacy. Cord cutting really refers to folks cancelling their existing video package and substituting something like HULU or Netflix. While it is true revenue per customer declines, that customer still needs a broadband connection, and reduction on the legacy telephone business has slowed dramatically as many folks transitioning from land line to mobile have done so.

Most providers have transitioned to broadband service that allows for certain data usage. Even if a customer is streaming content not being sold by Frontier, they still have to pay for the right to have that content delivered and that will always be (at least for the next 10 years) via wireline network. 5G “wireless” technology is years away, and every device will require a wireline input feed to power the “wireless” network.

The Capital Expense Wild Card

Forward capital expense is vital to the overall conversation with Frontier. During Frontier’s December 4th UBS conference, Dan McCarthy specifically mentioned their initiative to upgrade legacy copper to compete with cable companies.

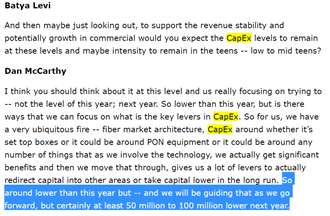

This is specific to our prior point that in order to fuel growth, their network has to be transformed to at least a 100 Mbps service offering. What this means is that they are well positioned going into Q4 and 2019 to compete with the Charters and Comcasts of the world. In addition, this most likely will yield reduced capital expense in the forward periods. At the same conference, Dan provided high level 2019 Capex guidance of $50m to $100m lower YoY, or a 7% reduction over 2018.

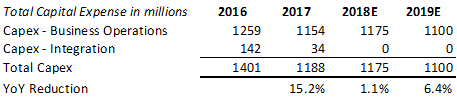

For comparison sake, we have broken out capital expense by year:

As reflected in this table, capital expense has been trending in the company’s favor and improving cash flow, resulting in an incremental $50 to $100m without factoring in potential subscriber growth from the benefit of upgraded service offerings. This is a point that management did an extremely poor job explaining on the Q3 conference call. However, they did explain the situation on the December 4th conference call, after the stock had taken a hit.

Cash Flow Trend

Simply put, the cash flow trend at Frontier has continued to increase year over year.

![]()

Note that 2019 assumes flat EBITDA and management has unofficially guided for a target of $800m for 2019. While I don’t believe $800m is reasonable, an increase to $700m is quite reasonable.

But What About the Debt?

One common point of contention is the massive debt load that Frontier currently holds – it is a very valid point. There is, however, one item of clarification that many folks do not understand. All of Frontier’s unsecured debt is fixed rate. So if rates go up, there is no incremental interest expense to Frontier at the time of interest payments. Their secured debt is all pegged to LIBOR so that debt will float.

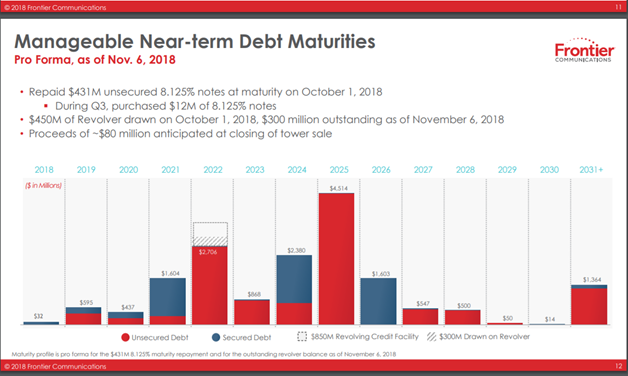

We’ve seen the argument being made interest rates going up could be a death blow to Frontier, and that’s simply not true. In fact one could make the argument that as market rates go up, and the pricing of their unsecured debt declines, excess free cash flow can redeem the debt at a larger discount. This is putting the cart before the horse to some extent, so let’s look at the current debt maturity structure:

While this charge may look bad, it certainly doesn’t paint the picture of imminent bankruptcy that the market appears to be pricing in. 2019 and 2020 debt redemption is not an issue. 2021, while it appears to be tight from a cash flow perspective, is primarily secured debt, which should be generally straightforward to roll out. Note that there are various approvals required by the unsecured tranches in order to roll secured debt, but as long as the cash flow levels stay at or above ~700m annually, this shouldn’t be a show stopper. The elephant in the room is the $2.7b of 2022 unsecured debt (currently priced ~70). The table below shows all debt maturities through the end of 2023.

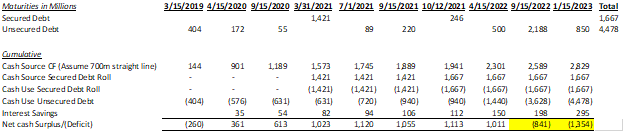

For simplicity purposes, we ignored their standing line of credit and straight lined an estimated $700m of cash flow per year to determine where the real stress comes. We’ve also assumed that all secured debt is rolled, and only unsecured debt is redeemed at par. We’ve also assumed an 8% interest rate on the unsecured debt. The max pain point comes in January of 2023 where they have to solve a ~1.354b problem.

There are two simplistic solutions to this problem: the first of which is to buy September 2022 debt at the current 30% discount with their free cash flow generation (Note that this doesn’t solve the entire problem as the debt would have to trade down and be redeemed for ~60). One cannot forget, however, that the continued spend of $1.1b per year will allow for incremental secured borrowings on Frontier’s network assets, the current secured debt allows for 20% security on network assets (for every $100 spent on network they can borrow $20 in secured debt. This is how Frontier must navigate their mountain of debt, and it isn’t close to being as insurmountable as the market currently thinks. This also will yield $3.5 to $4.5b of reduced unsecured debt at ~8% coupon or an incremental ~$300m of free cash flow.

Another solution that Frontier could consider, although in our opinion it is too early for this, is an unsecured debt swap to extend maturity dates and reduce overall debt load. While this is generally not great for the unsecured debt holders, it is good for both secured debt and equity.

From what we understand, there may have been rumors in the summer of 2018 that an ad hoc bondholder group had begun discussions with Frontier on a restructuring plan, and those may still be ongoing. While we have no insight as to whether this is true, or what the structure or discussions would have been, we believe they would most likely push out maturity of the “problem” tranches in return for a bump in value. For example, in return for exchanging 2022 unsecured currently trading at ~70, they would agree to push maturity out a number of years in return for a par value of ~85, with perhaps a warrant kicker. This would help Frontier’s liquidity while reducing their overall debt – and the bondholders would receive 15 on the current market value and reduced risk of being impaired in the future.

The Case Against Bankruptcy

While many folks believe that bankruptcy is a foregone conclusion, one must think of the benefit/detriment to the creditors. Bankruptcy would render the equity worthless; however, it would only provide $200m of relief on a $17b debt stack. The other detriment is that given the multitude of debt issuances, the legal battle to sort out whom receives what would be extremely complicated and cost prohibitive. Frontier also has ample free cash flow to run its day to day operations while covering interest expense. As such, creditors most likely prefer to grant relief versus blowing the current financial situation up. On the other hand, if Frontier were to get into a situation where it had difficulty covering interest expense, a judge would be the only way to sort out the go-forward, if creditors started to butt heads.

Caveats and Primary Risk

The primary risk to the thesis presented in this piece is that the massive spend to improve network speeds do not result in a return to subscriber and revenue growth. In this situation, free cash flow continues to erode and bankruptcy is guaranteed. Another potential pitfall is significant dilution if a bondholder group were to voluntarily convert part of their debt to equity. In my opinion, this is highly unlikely based on the current debt/equity ratio and the belief that bondholders simply want their coupon and return of principal at the maturity of the tranche.

Summary/Conclusion

Frontier common equity has gotten absolutely destroyed over the past few years. Many “experts” believe they are ripe for imminent bankruptcy. This is under the assumption that revenue and EBITDA contraction trends continue to decline. Many also believe that upcoming 2022 debt maturity will be the penultimate death blow to Frontier.

While there is a chance that Frontier Management will fail, we believe the market is wrong. Frontier currently has $250m of equity value and $17b of total enterprise value, or 4.8x EBITDA. CenturyLink, by comparison, has an enterprise value of ~$53.25b on EBITDA of 8.32b or 6.4x EBITDA. Let’s assume that Frontier executes as I have laid out in this article and the market no longer prices them for bankruptcy, and the multiple moves 50% of the way toward what CenturyLink currently is valued at. Given current EBITDA levels, a 5.6x valuation would yield a total enterprise value of $19.86b.

By the end of 2020, once there is a clearer picture of the Frontier turnaround, net debt levels could be an estimated ~14.776B for a total equity value of $5.084b or just under $50 per share, a return of almost 25x. This level of potential return rarely exists in the market today and often only comes from severely depressed stock prices.

Looking at the risk/return profile of such a potential investment, and keeping in mind the serious caveat of a significant debt load, we believe Frontier equity could be severely underpriced and for us, is worthy of a speculative investment.

Disclosure: No Position in FTR at time of article, but may establish position within 72 hours of publication

Article by Geo Investing