The post was originally published here.

Q1 2022 hedge fund letters, conferences and more

Download the full report as a PDF

On This Page

- The rise and fall of Snapchat’s share price

- Let’s go to the latest annual report

- First, you need to understand the underlying drivers

- What are internal revenue drivers?

- What possibilities does Snapchat have to increase revenue?

- Snapchat was able to rapidly increase its users over time

- North America and Europe start maturing, Asia drives growth

- Internal revenue drivers

- Snapchat has still difficulties monetizing its users

- Though, it makes some progress in the US

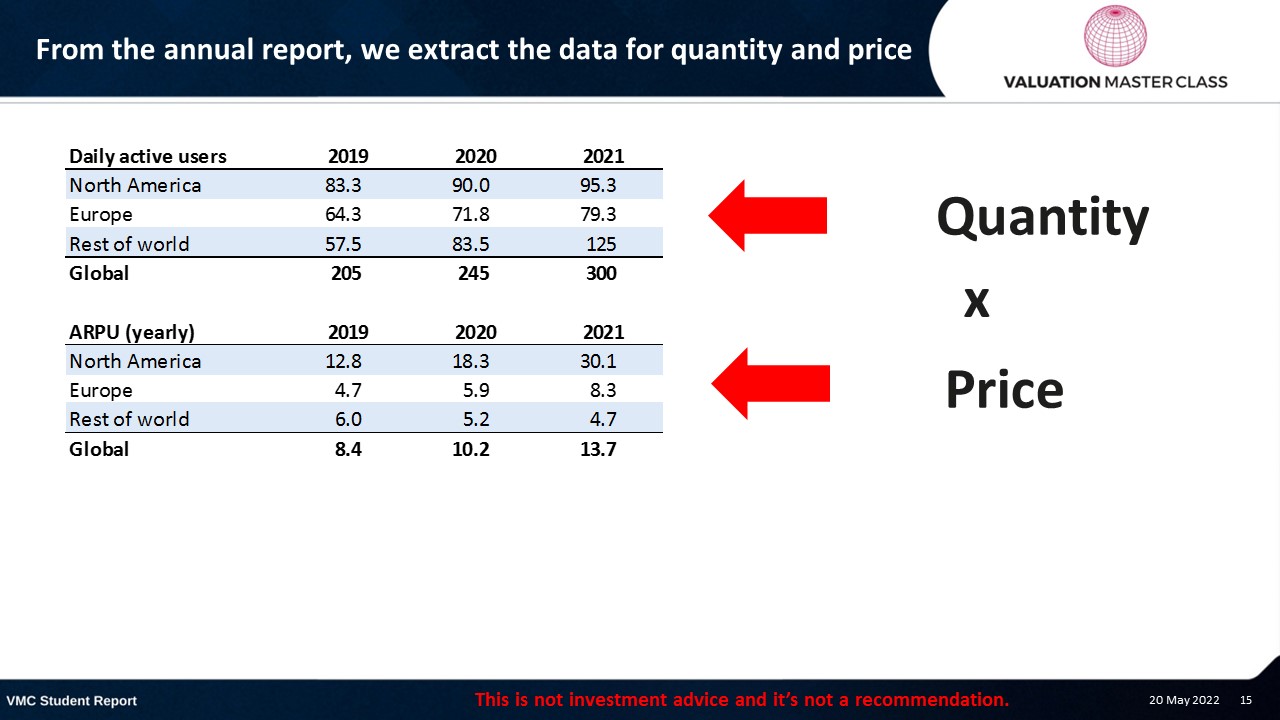

- From the annual report, we extract the data for quantity and price

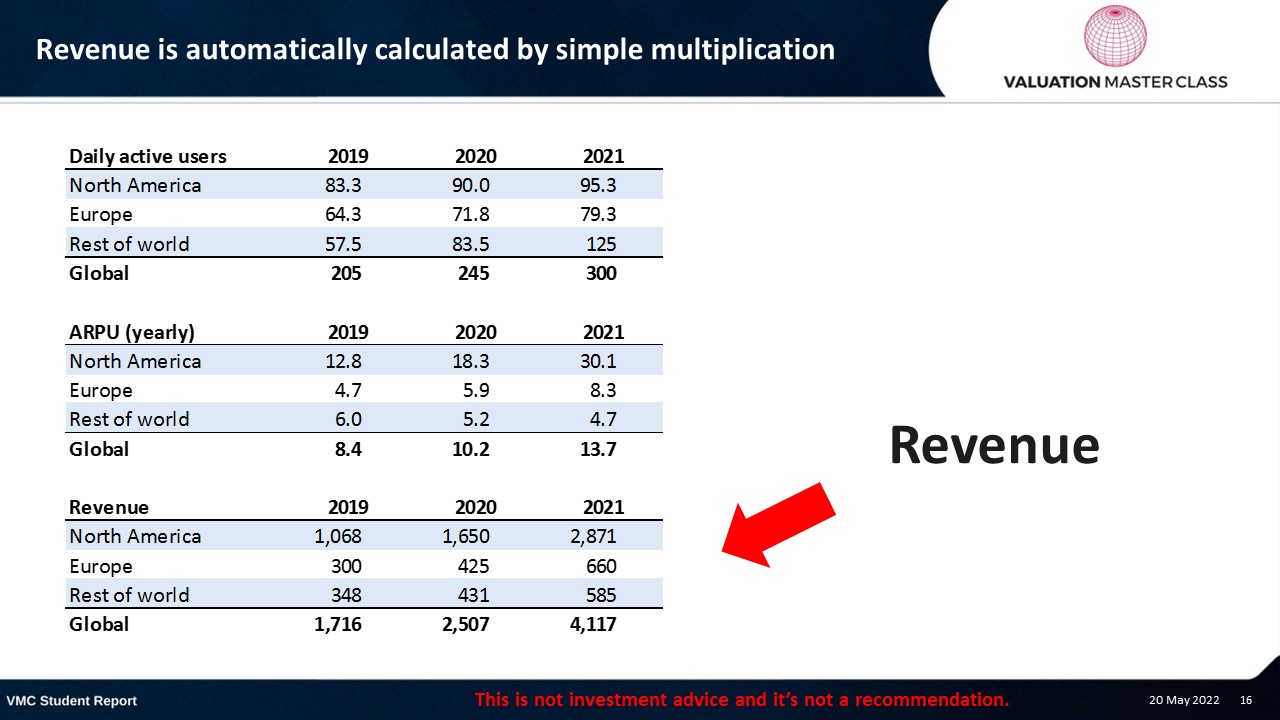

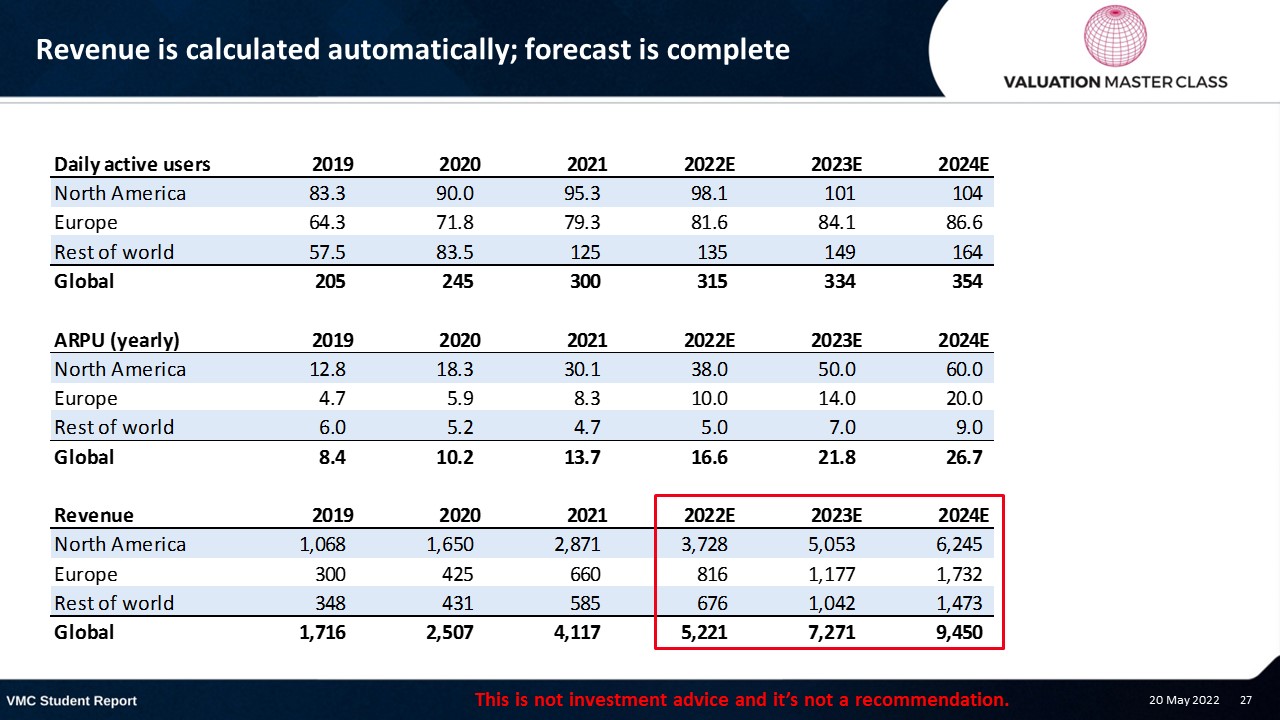

- Revenue is automatically calculated by simple multiplication

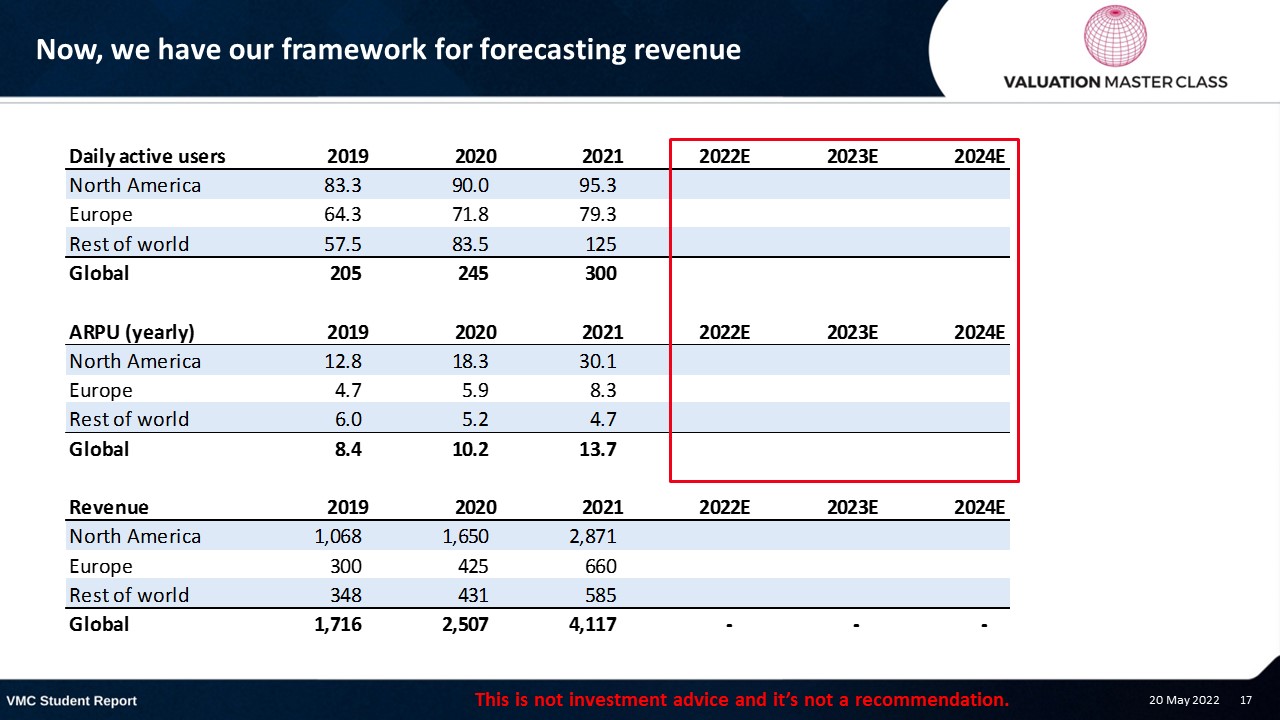

- Now, we have our framework for forecasting revenue

- Next, we want to understand the latest business developments

- Snapchat sees a massive opportunity to expand

- The relevant market is mainly just young generation

- Penetration is already high for the main target group

- Low growth for US and Europe, higher growth for rest of the world

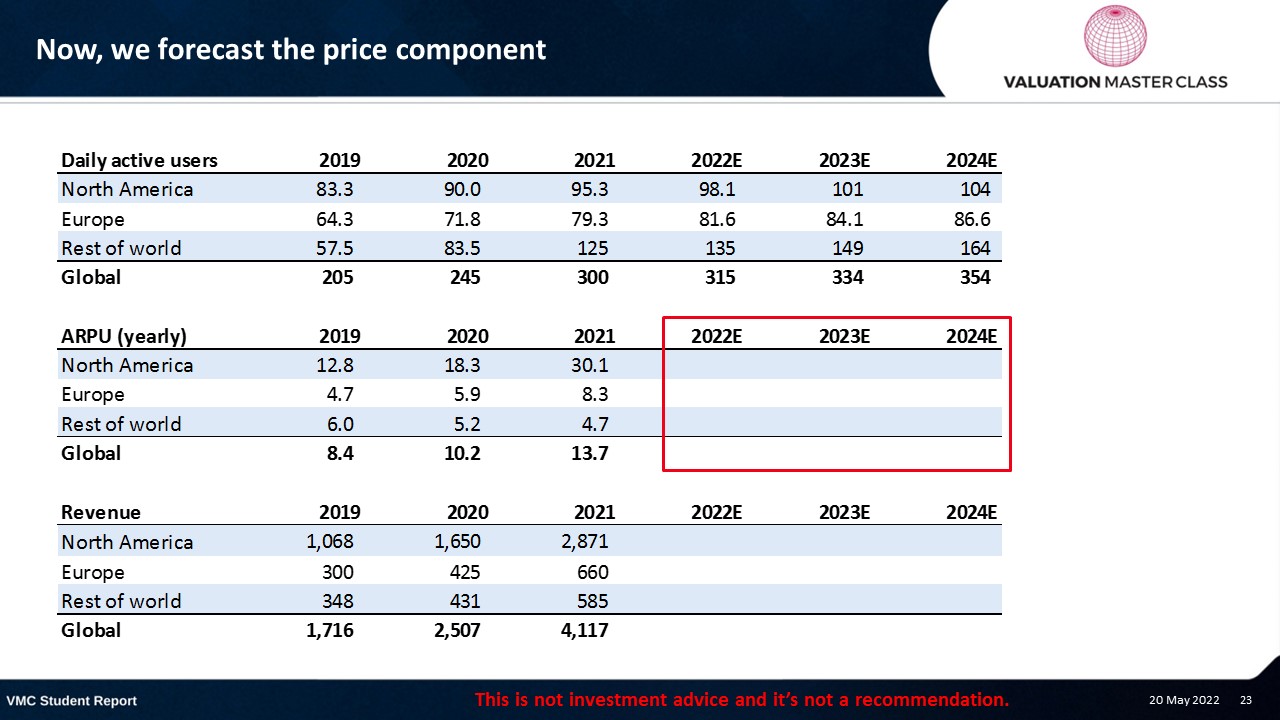

- Now, we forecast the price component

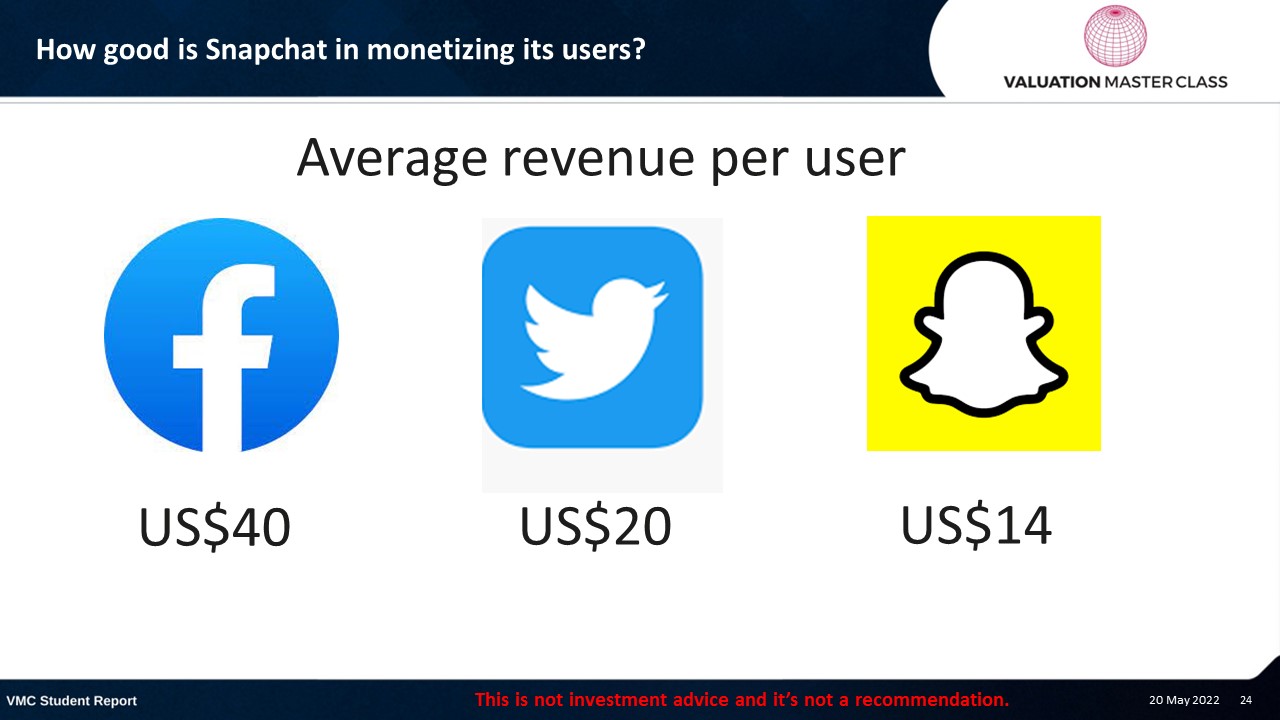

- How good is Snapchat in monetizing its users?

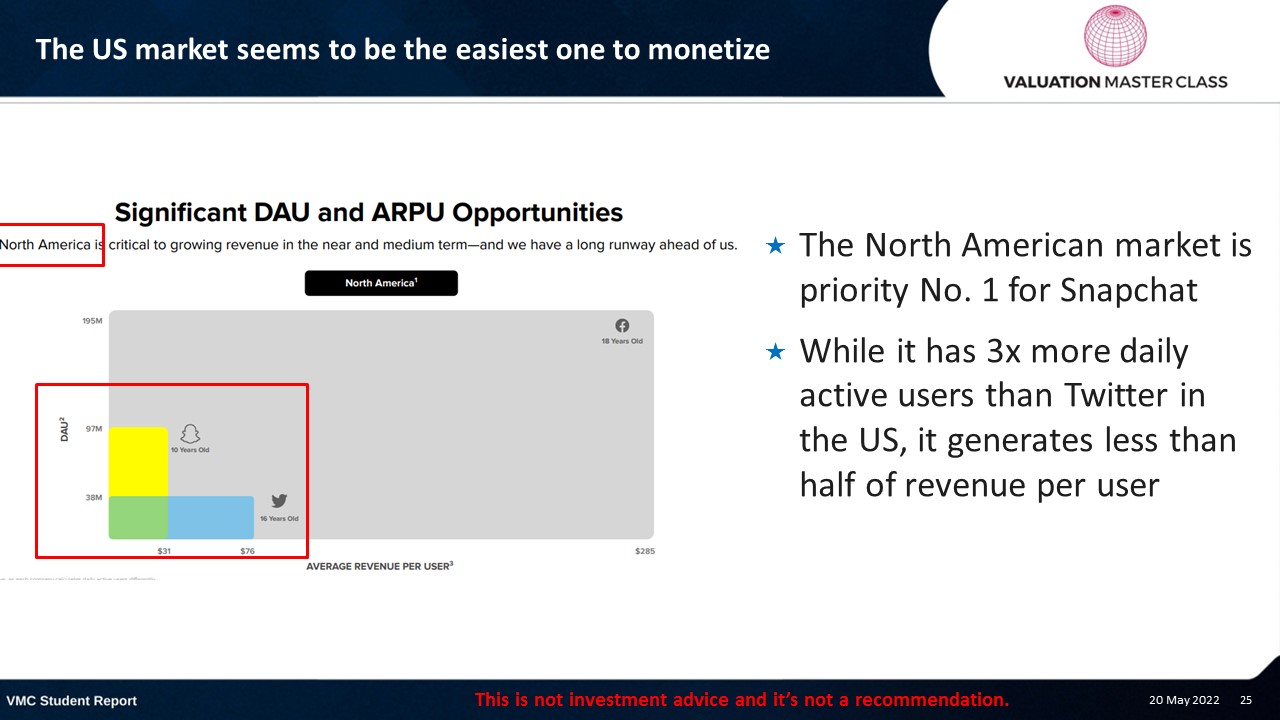

- The US market seems to be the easiest one to monetize

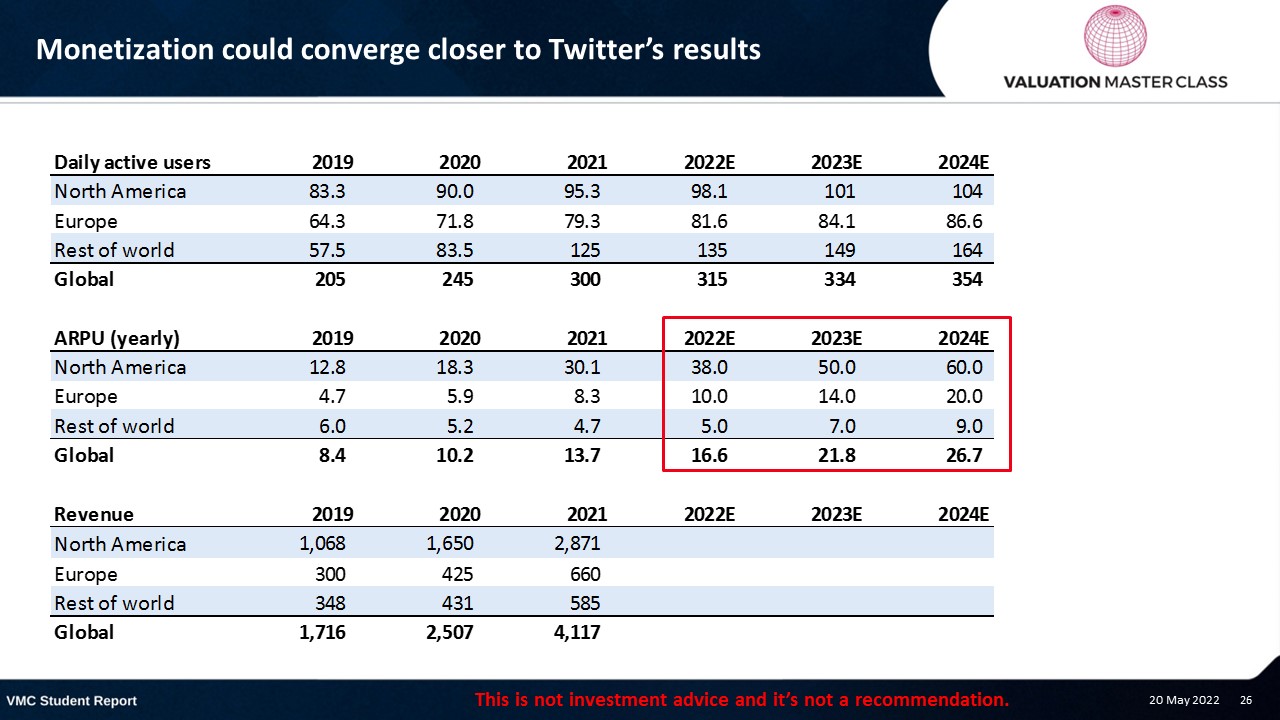

- Monetization could converge closer to Twitter’s results

- Revenue is calculated automatically; forecast is complete

- Let’s take a look at the recent filings

- What is an 8-K filing?

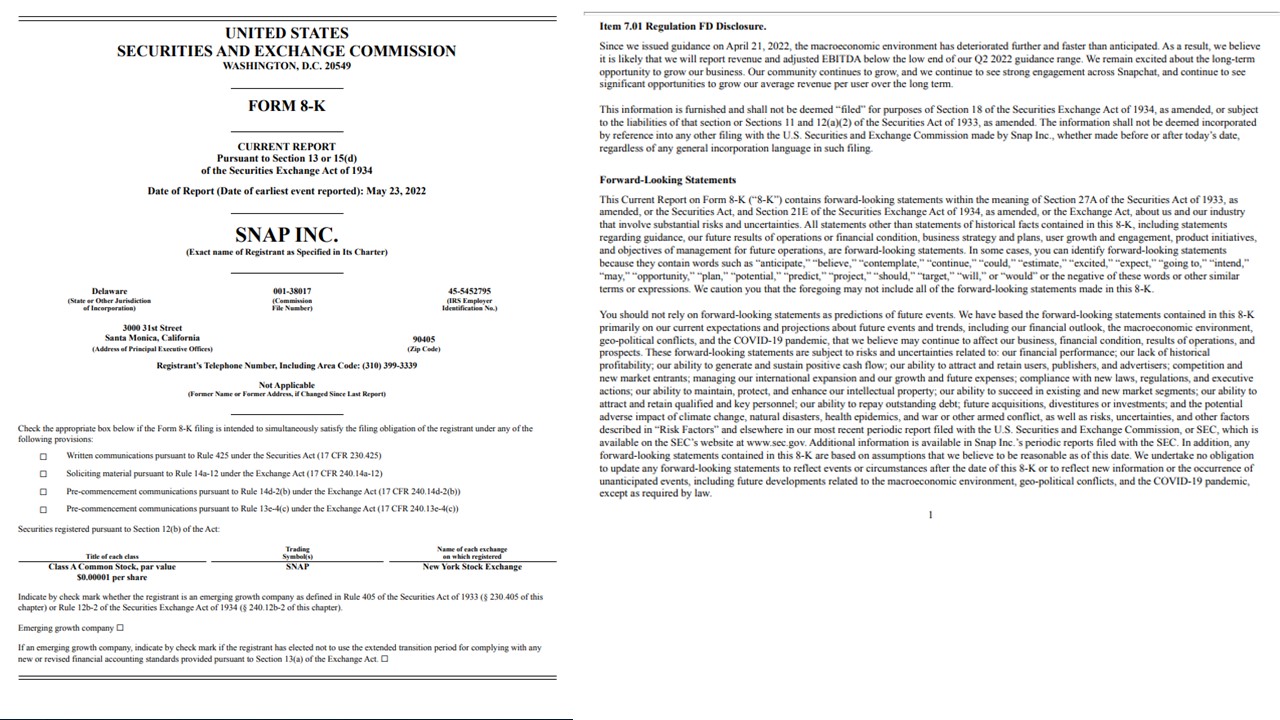

- One sentence has driven stock market sentiment

- In fact, we are not that smarter than before

- Compare fundamentals: Gross profit margin

- Compare fundamentals: EBIT margin

- Compare fundamentals: Net margin

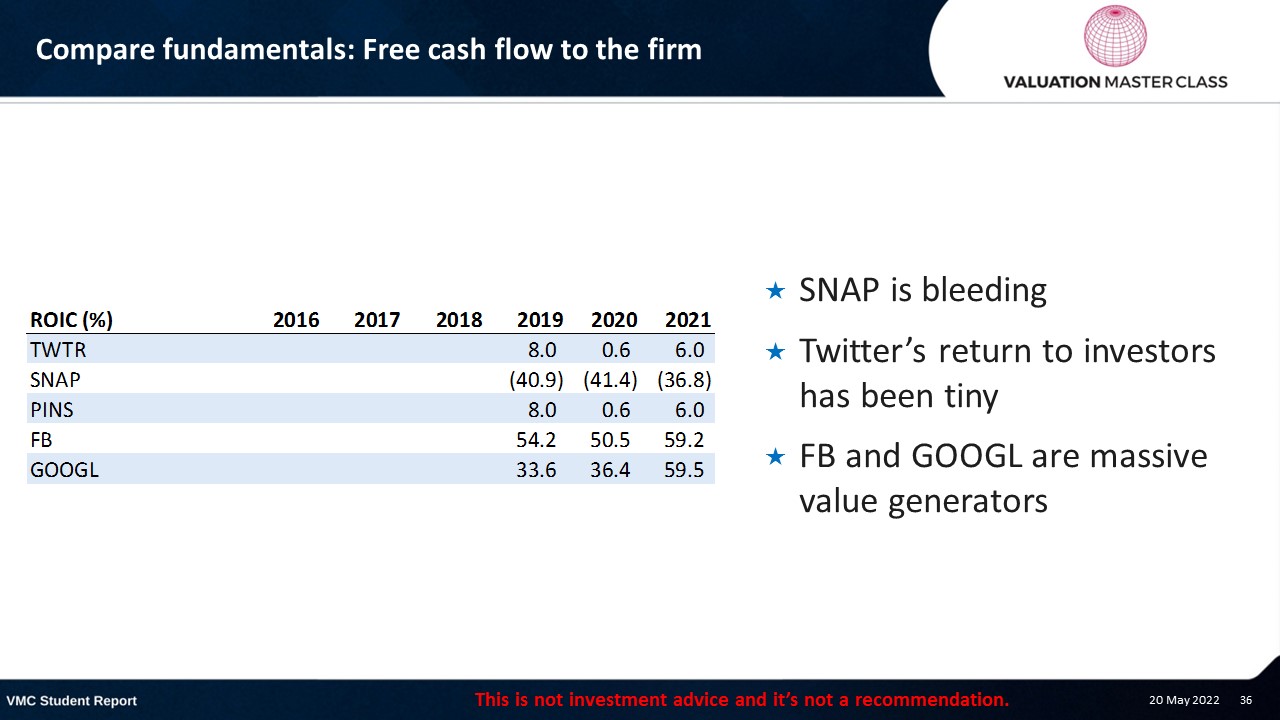

- Compare fundamentals: Free cash flow to the firm

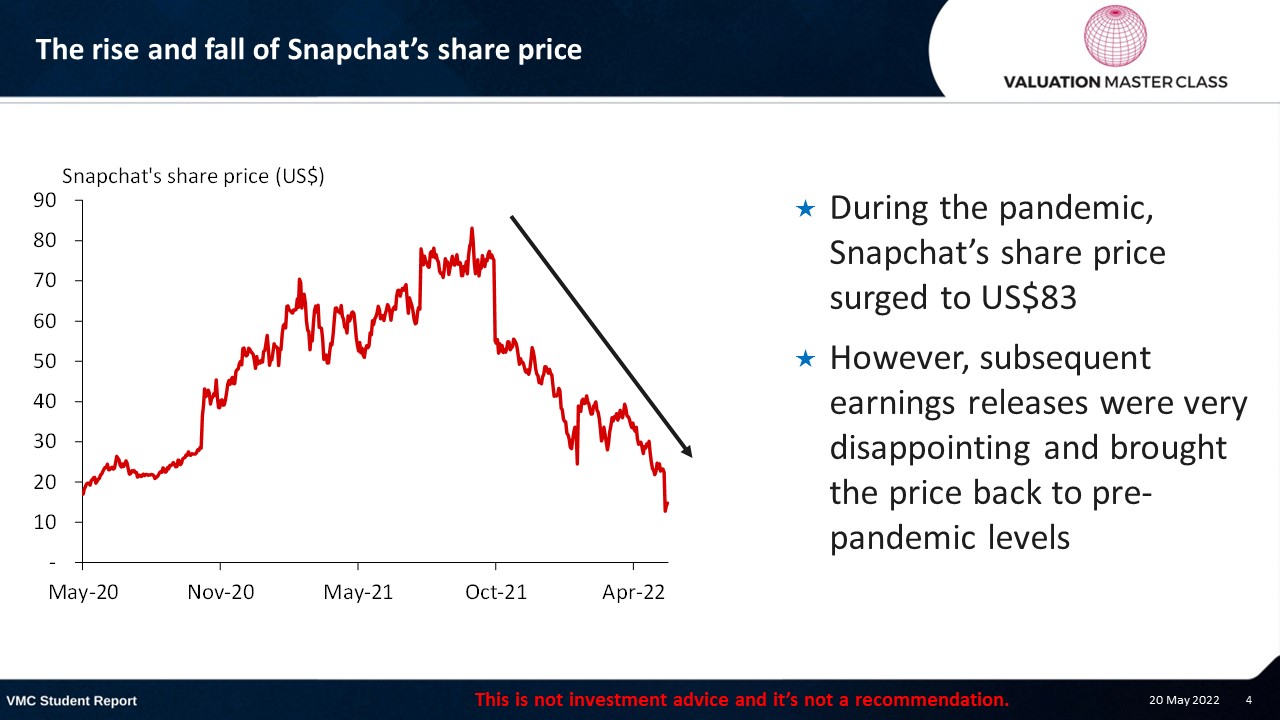

The rise and fall of Snapchat’s share price

- During the pandemic, Snapchat’s share price surged to US$83

- However, subsequent earnings releases were very disappointing and brought the price back to pre-pandemic levels

Let’s go to the latest annual report

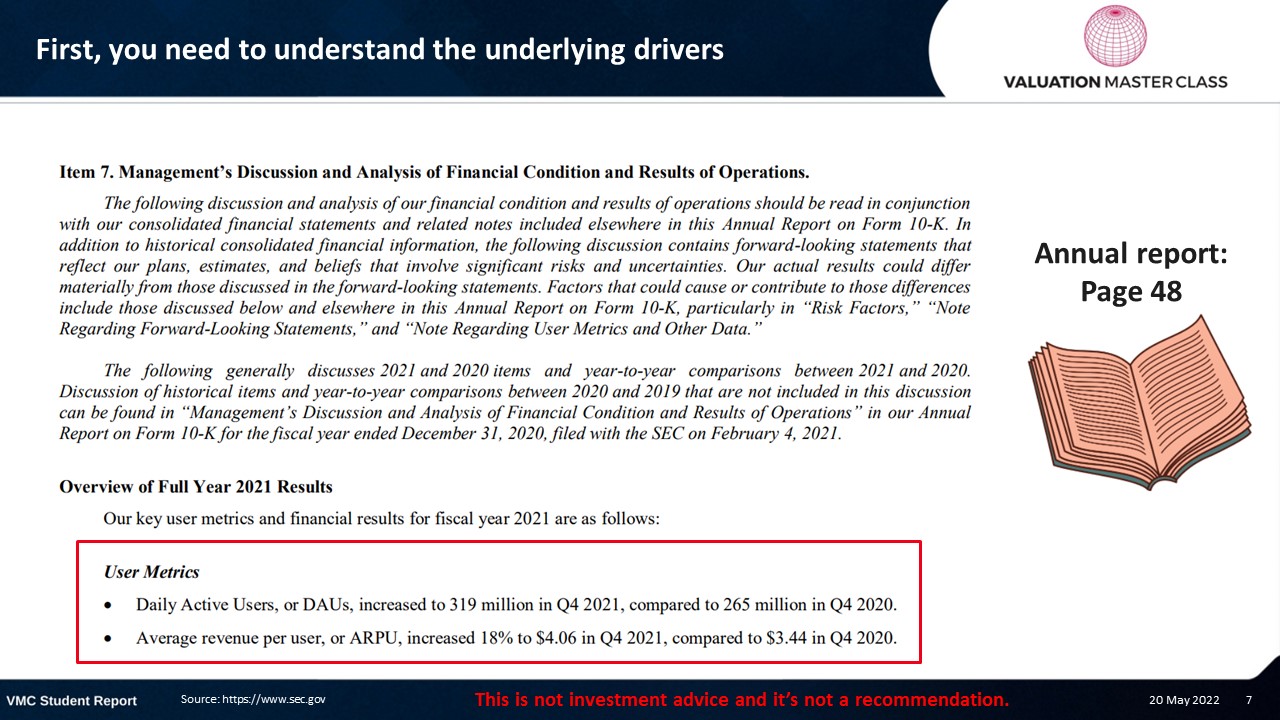

First, you need to understand the underlying drivers

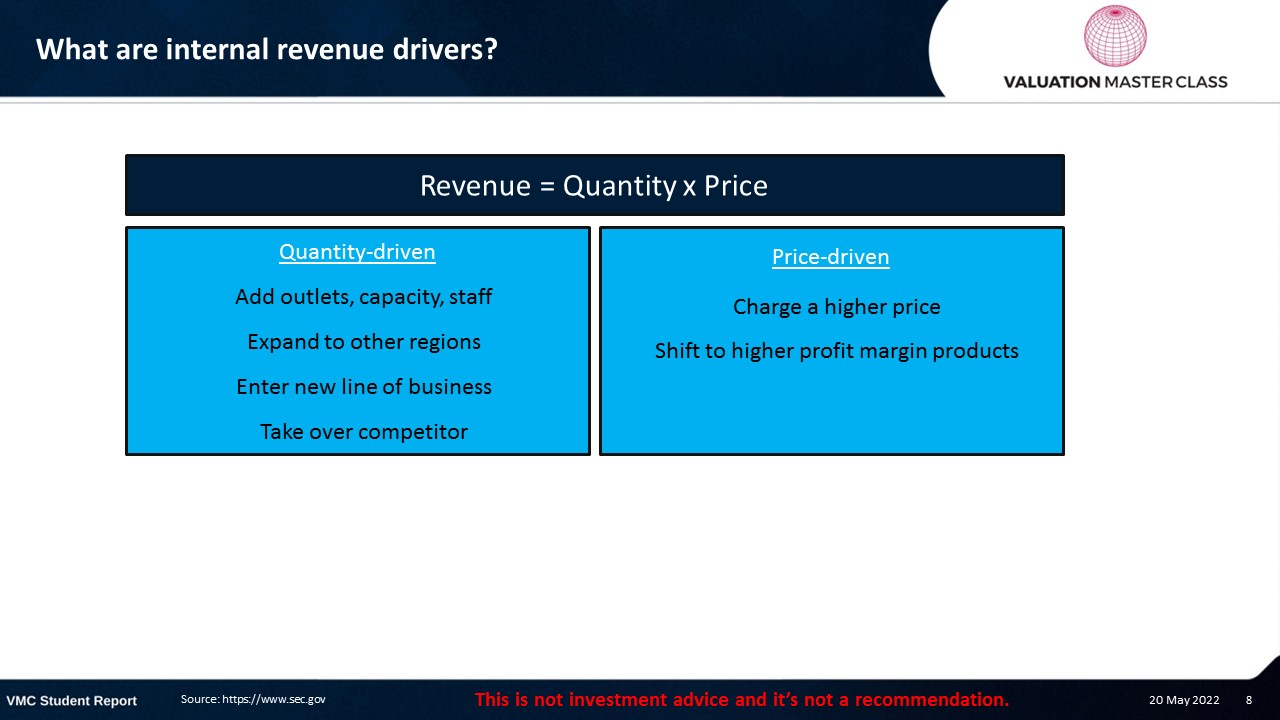

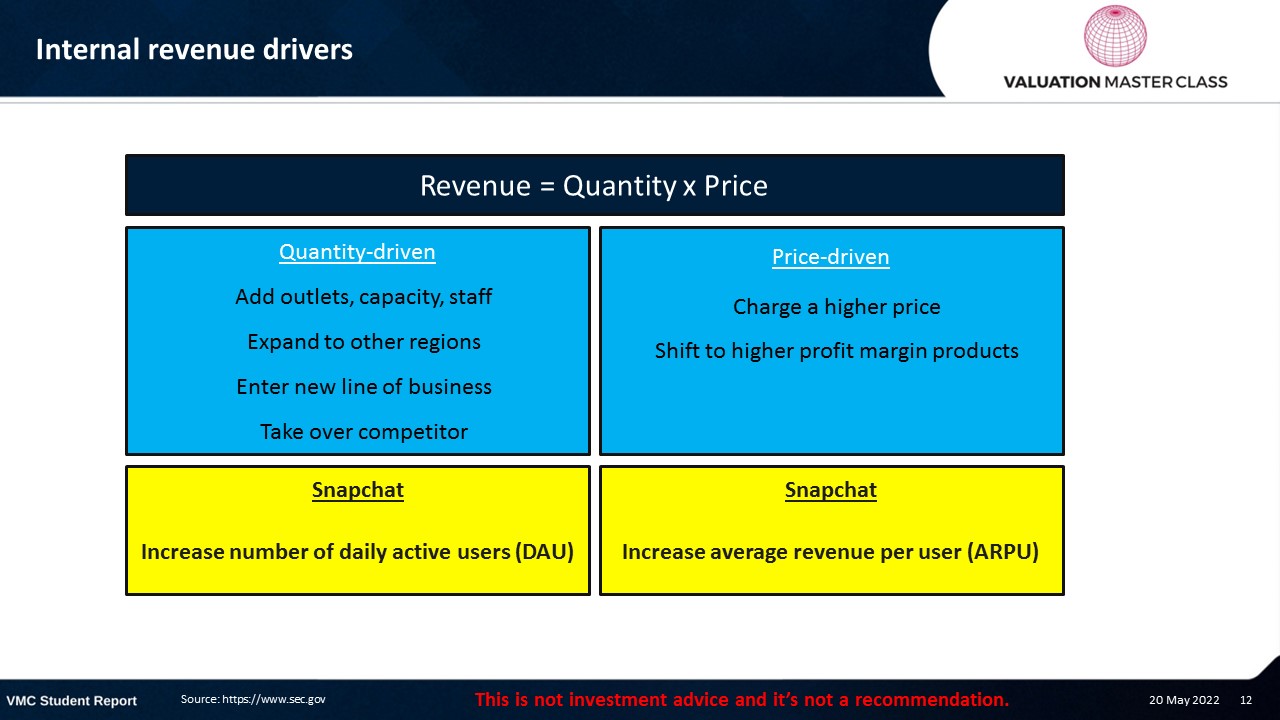

What are internal revenue drivers?

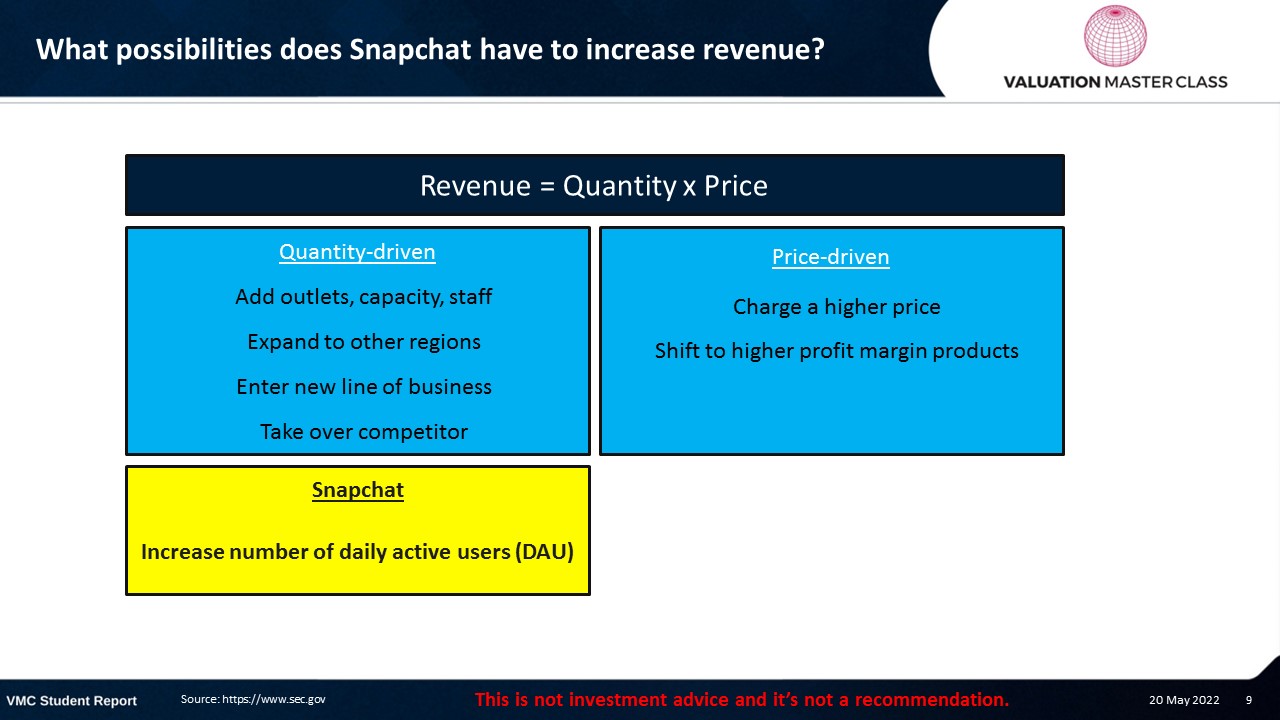

What possibilities does Snapchat have to increase revenue?

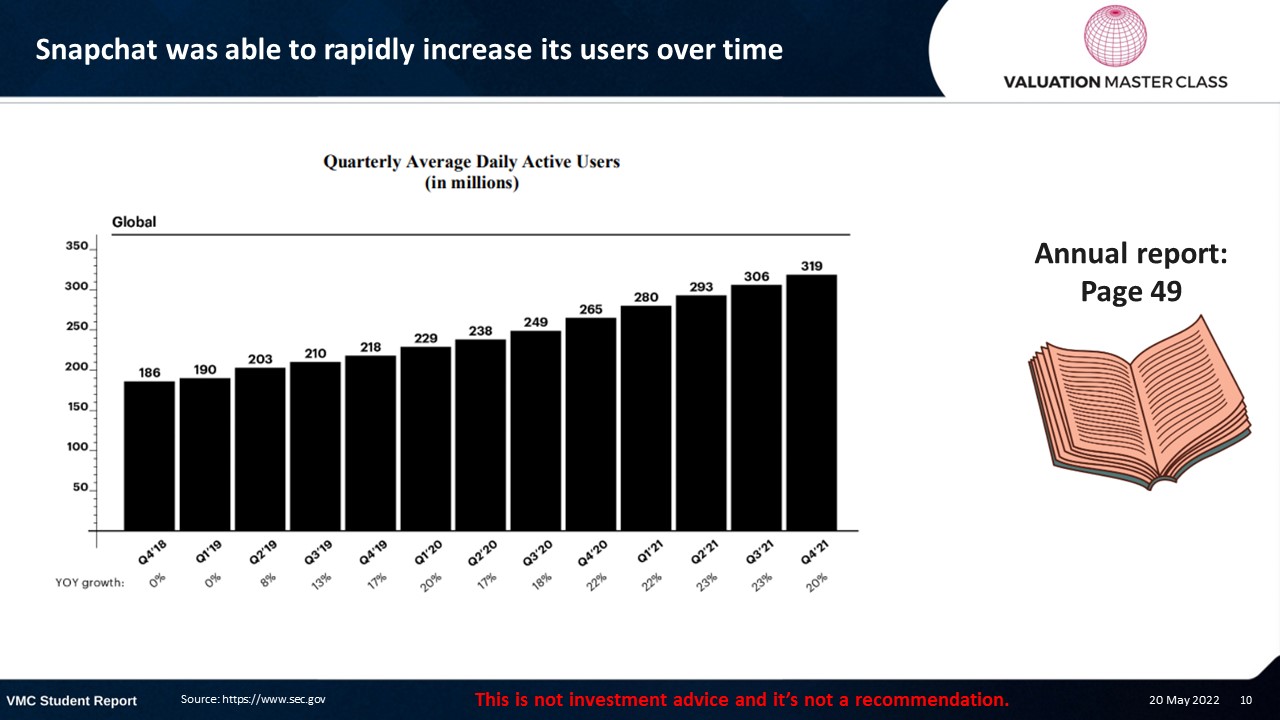

Snapchat was able to rapidly increase its users over time

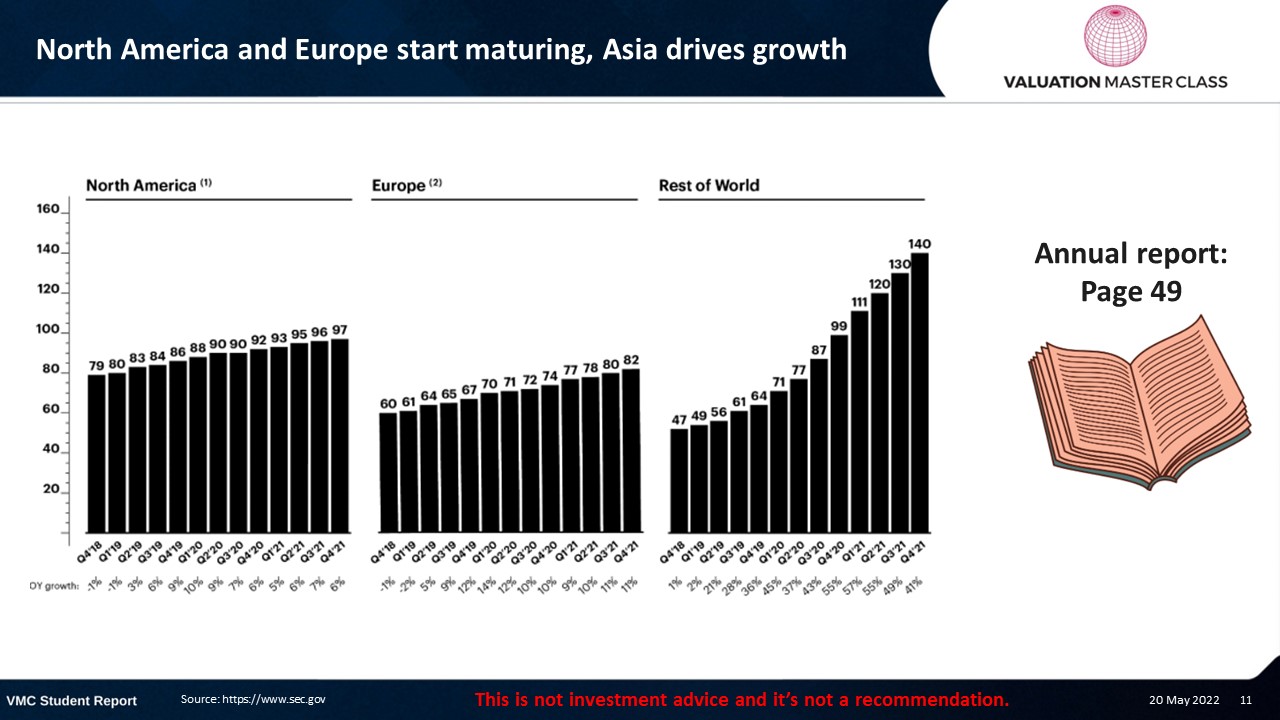

North America and Europe start maturing, Asia drives growth

Internal revenue drivers

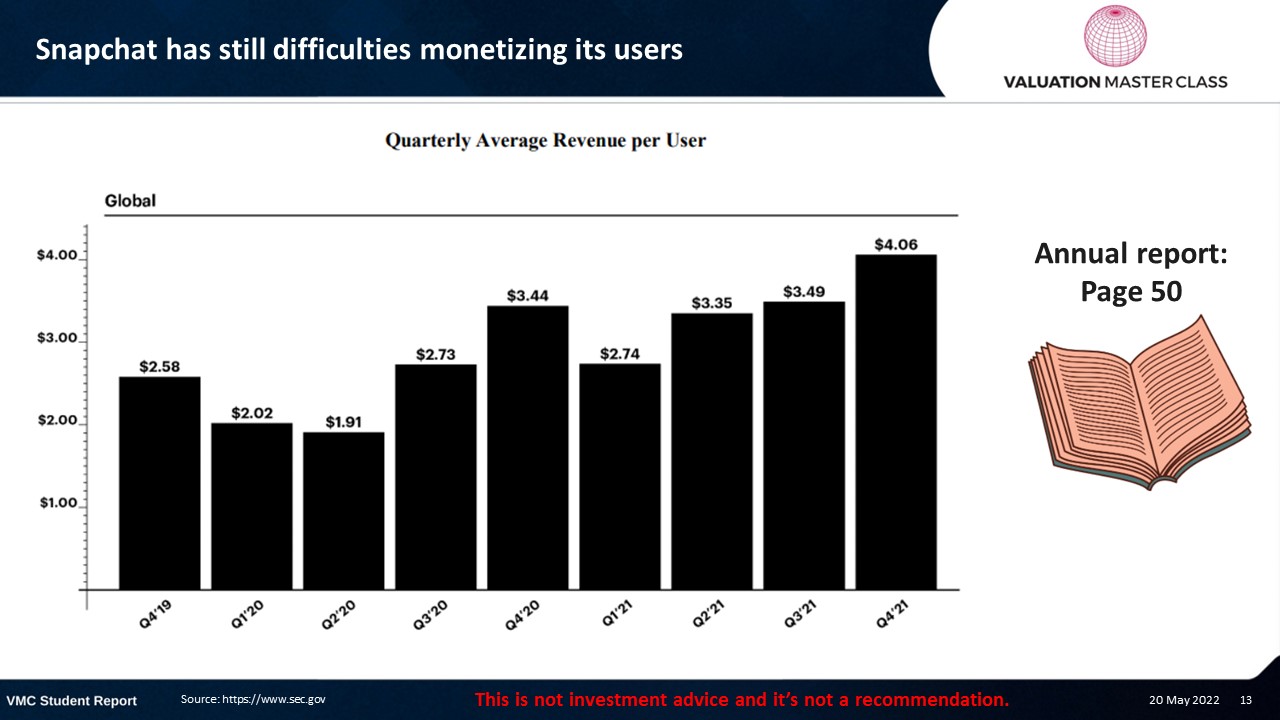

Snapchat has still difficulties monetizing its users

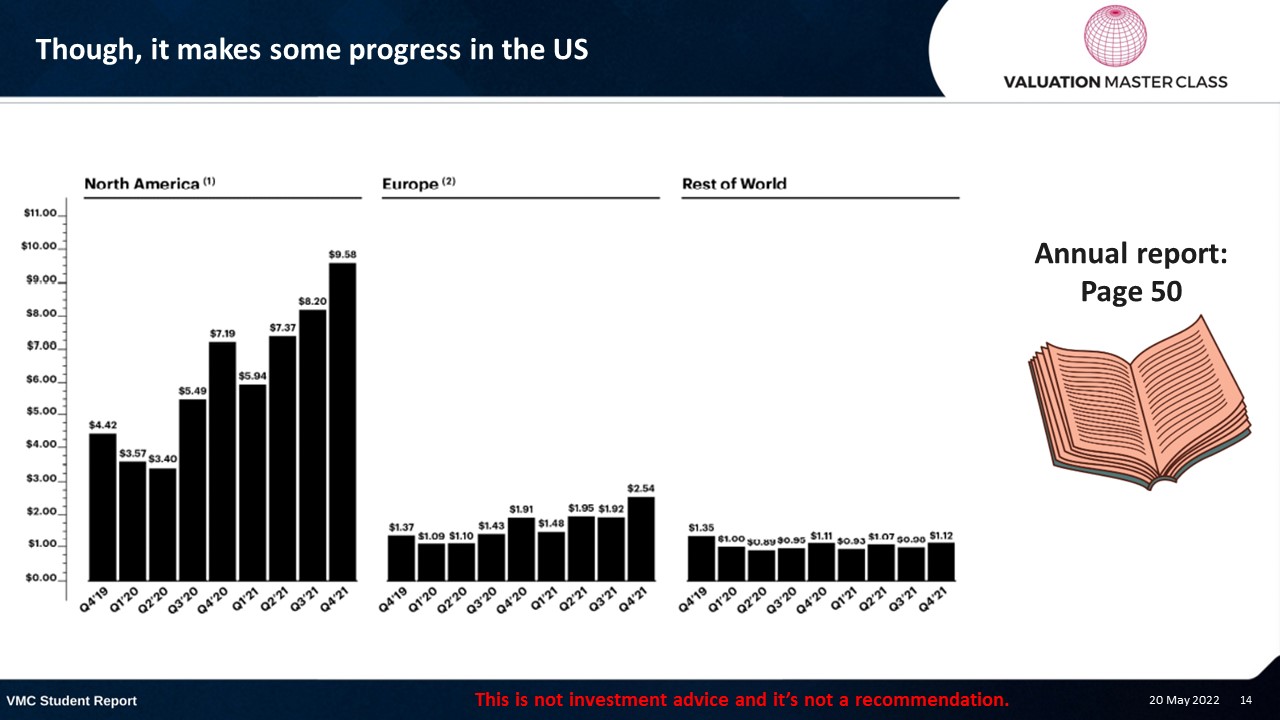

Though, it makes some progress in the US

From the annual report, we extract the data for quantity and price

Revenue is automatically calculated by simple multiplication

Now, we have our framework for forecasting revenue

Next, we want to understand the latest business developments

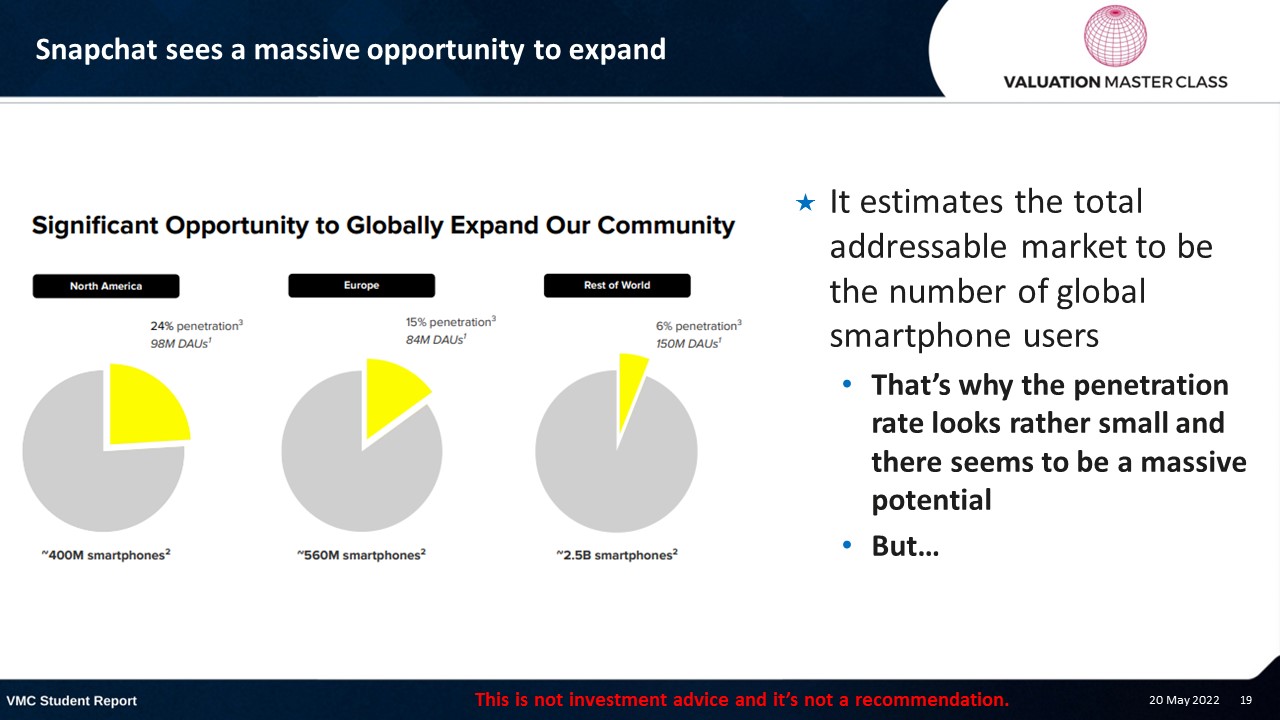

Snapchat sees a massive opportunity to expand

- It estimates the total addressable market to be the number of global smartphone users

- That’s why the penetration rate looks rather small and there seems to be a massive potential

- But…

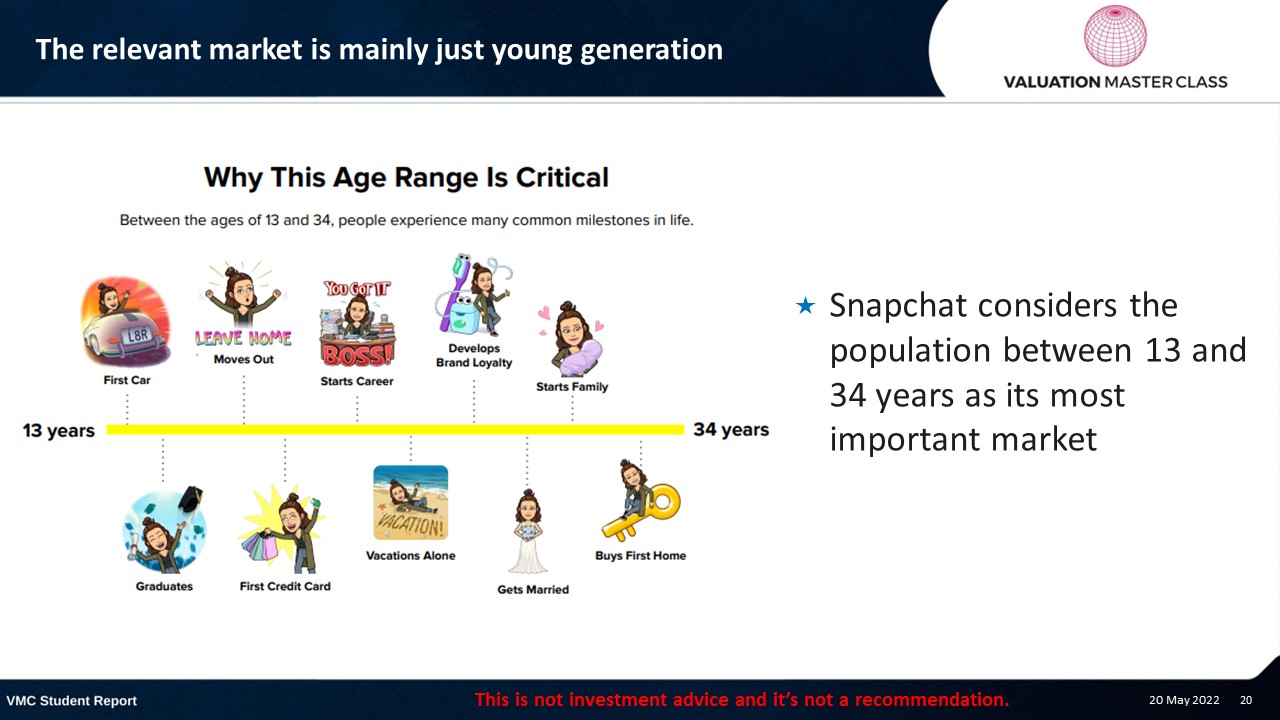

The relevant market is mainly just young generation

- Snapchat considers the population between 13 and 34 years as its most important market

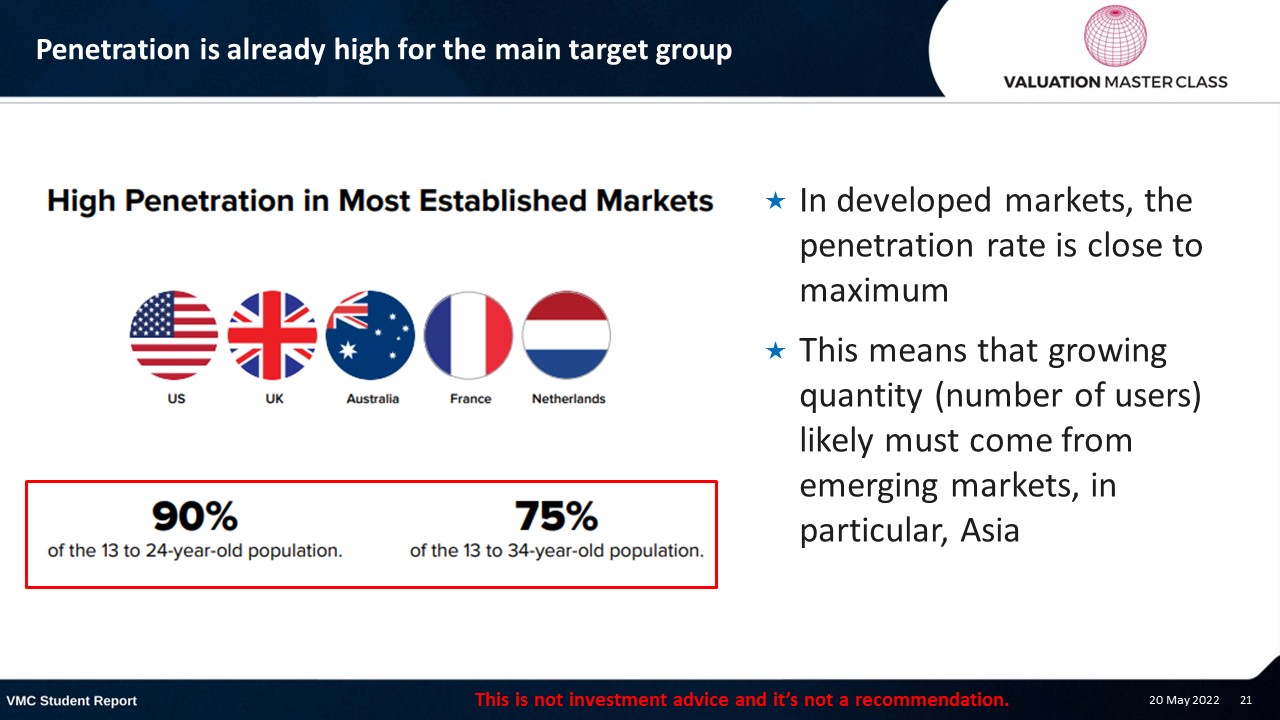

Penetration is already high for the main target group

- In developed markets, the penetration rate is close to maximum

- This means that growing quantity (number of users) likely must come from emerging markets, in particular, Asia

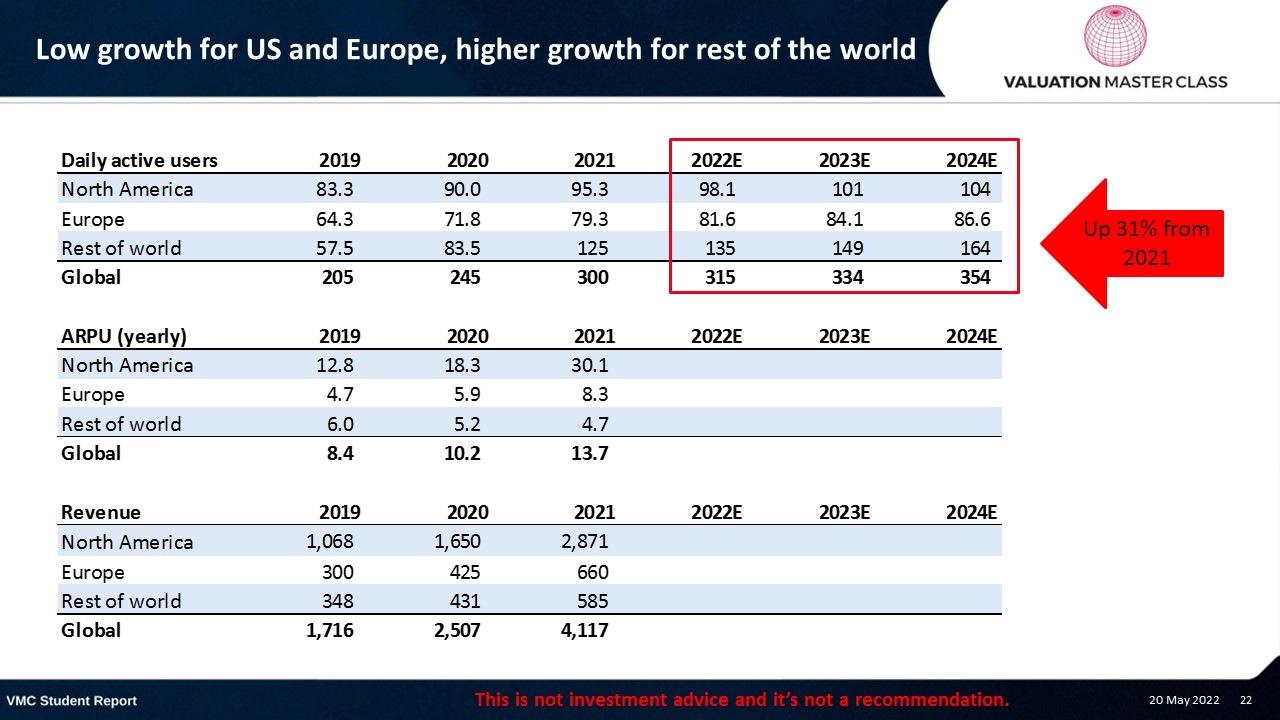

Low growth for US and Europe, higher growth for rest of the world

Now, we forecast the price component

How good is Snapchat in monetizing its users?

The US market seems to be the easiest one to monetize

Monetization could converge closer to Twitter’s results

Revenue is calculated automatically; forecast is complete

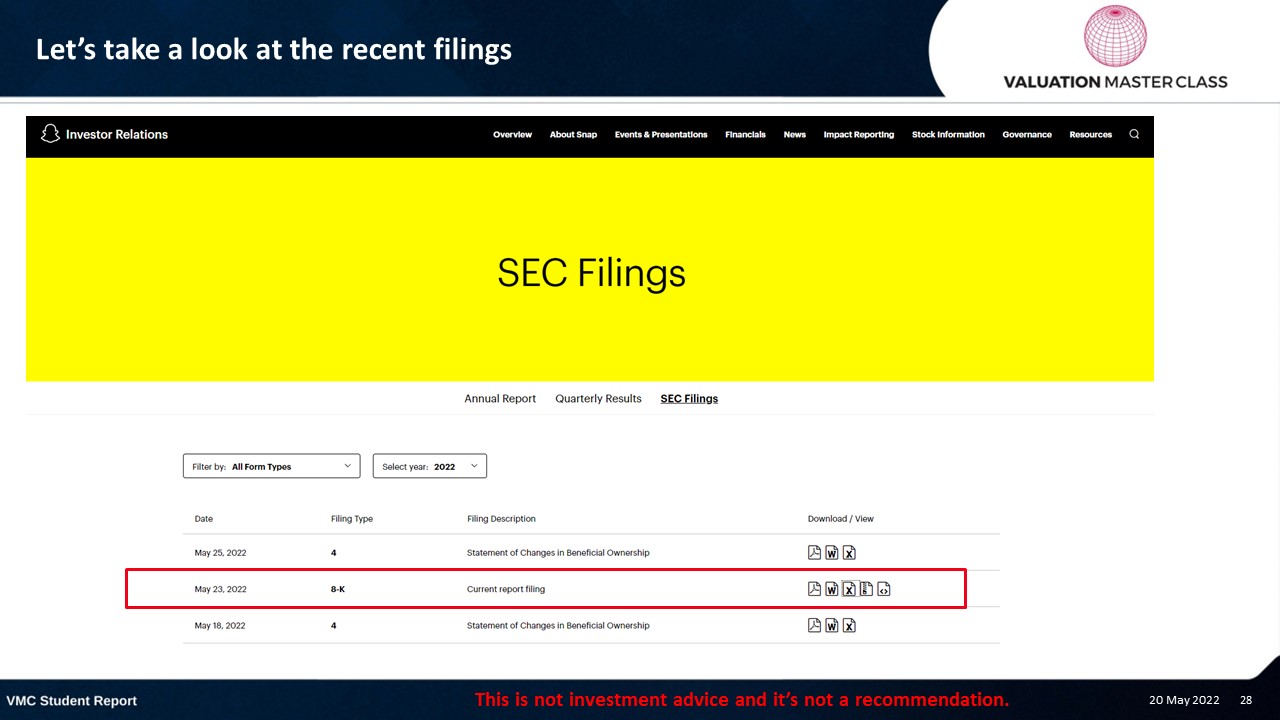

Let’s take a look at the recent filings

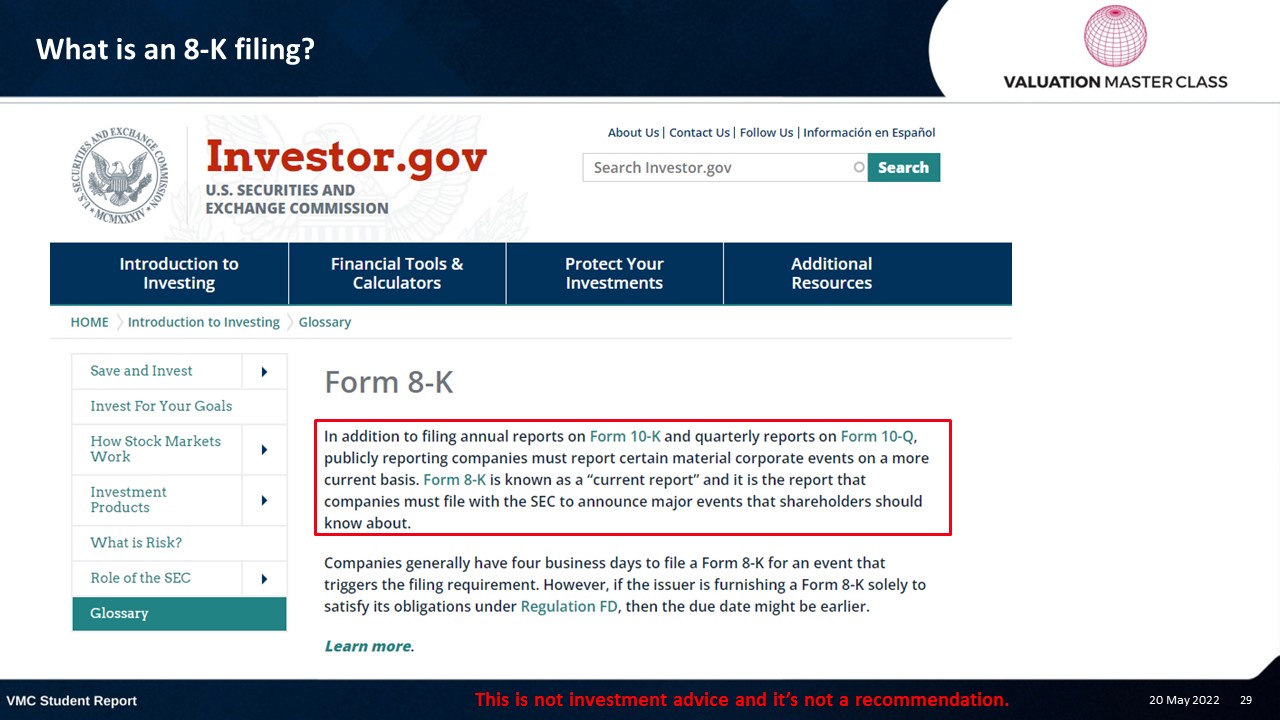

What is an 8-K filing?

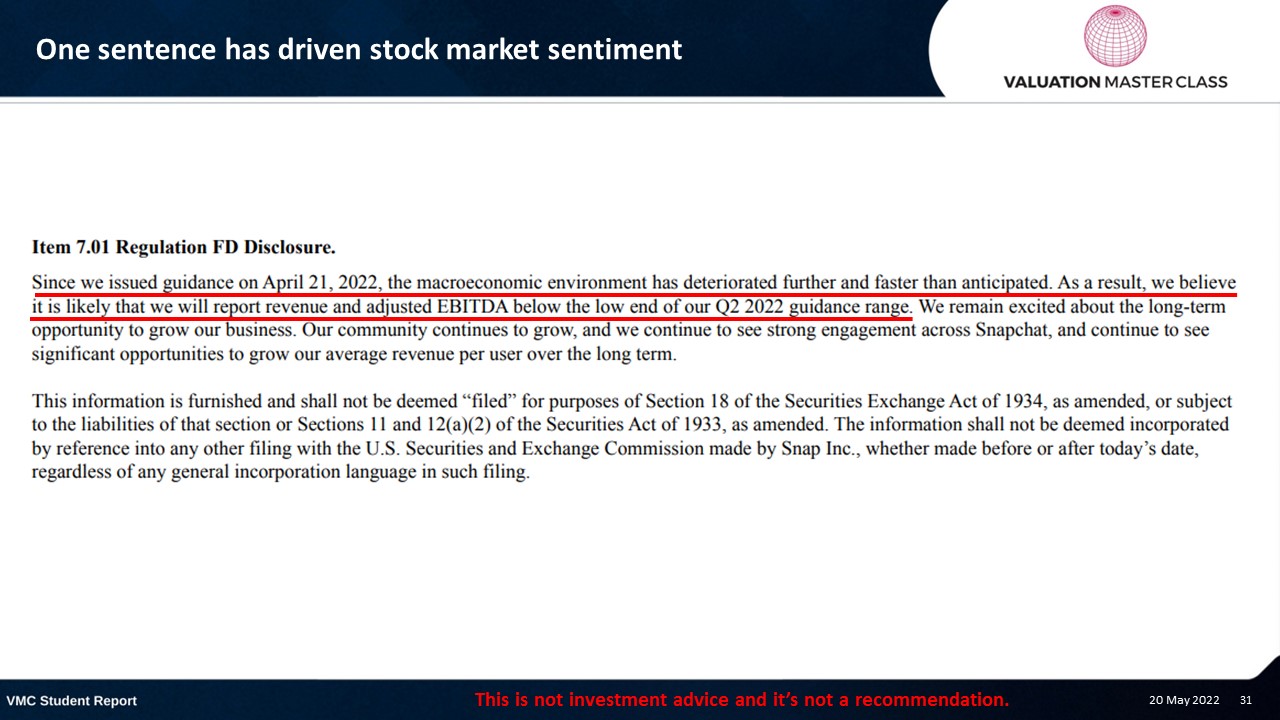

One sentence has driven stock market sentiment

In fact, we are not that smarter than before

- A company always has more information than any investor

- The company did not provide any guidance on how bad the impact actually is

- The only thing we can take away from the company’s statement is to reconsider our revenue drivers

- But if we take a look at Snapchat’s fundamentals, the market correction was just a question of time…

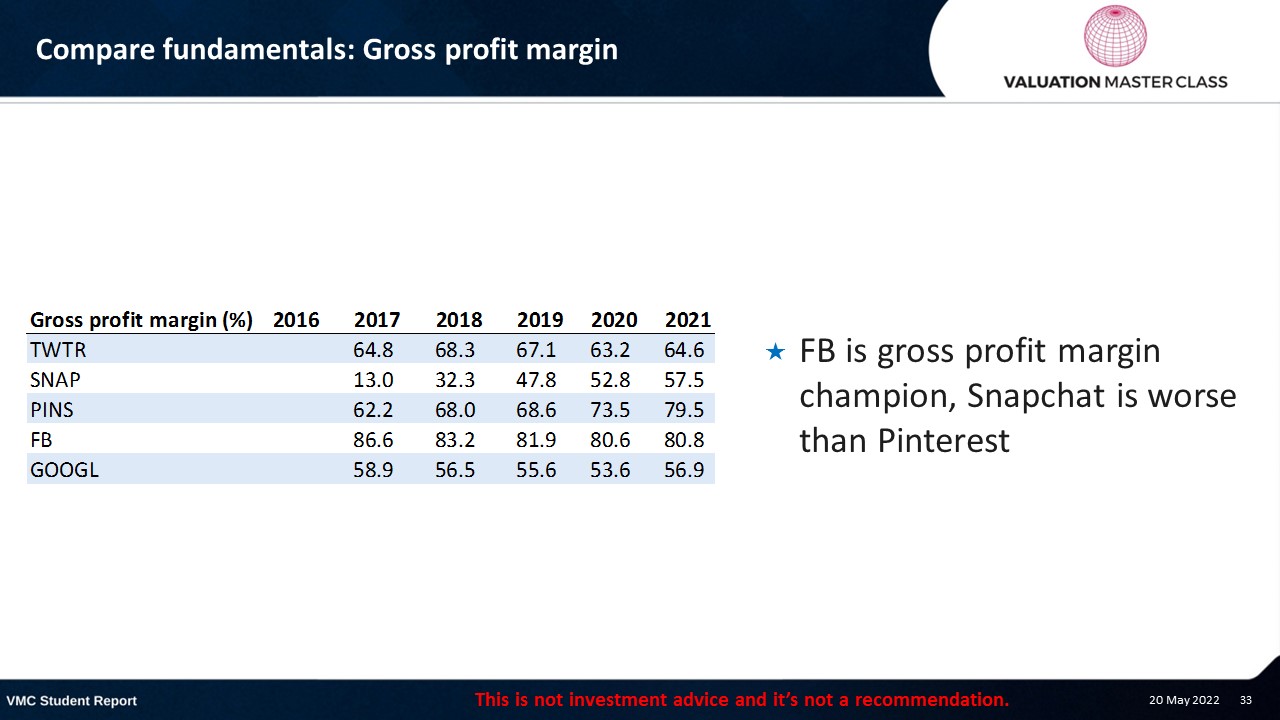

Compare fundamentals: Gross profit margin

- FB is gross profit margin champion, Snapchat is worse than Pinterest

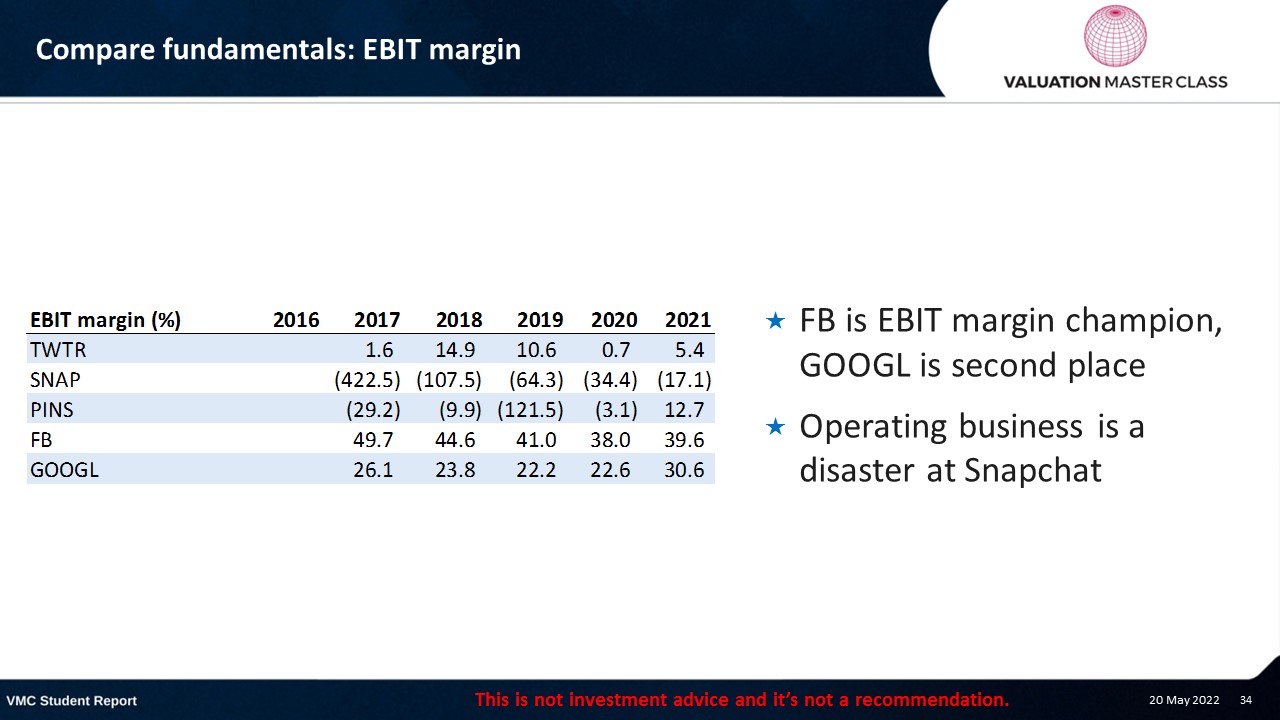

Compare fundamentals: EBIT margin

- FB is EBIT margin champion, GOOGL is second place

- Operating business is a disaster at Snapchat

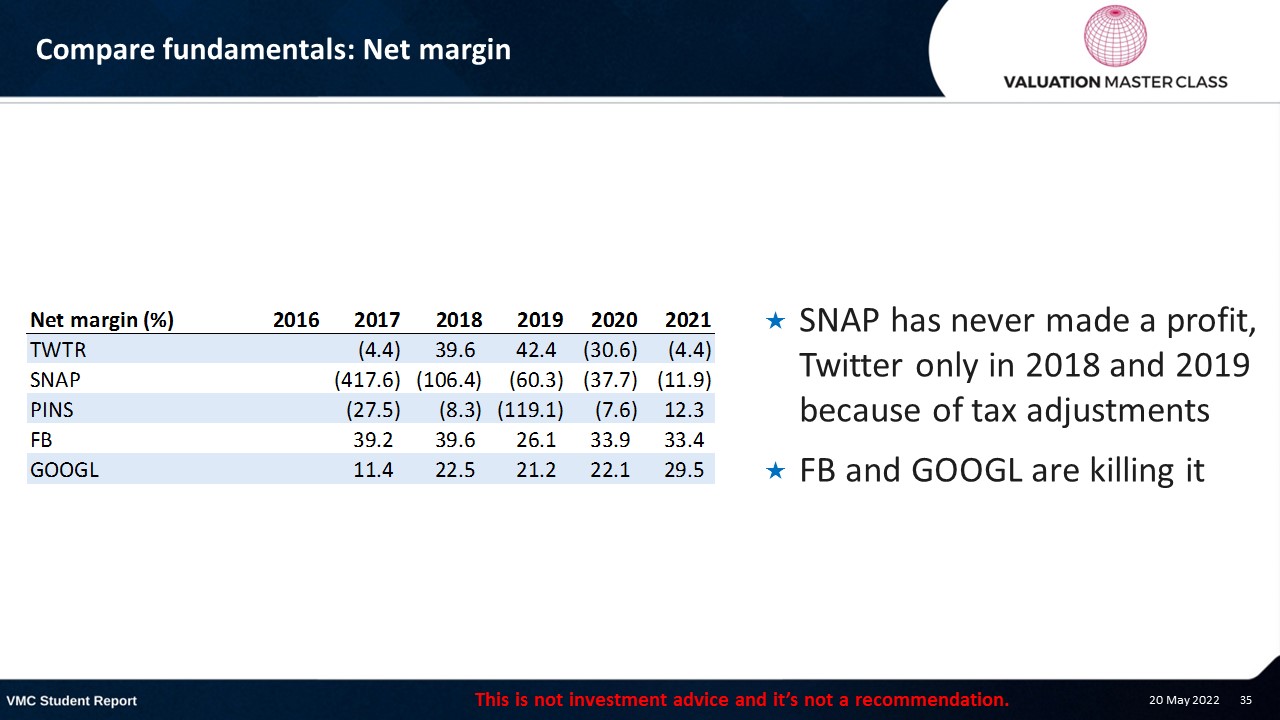

Compare fundamentals: Net margin

- SNAP has never made a profit, Twitter only in 2018 and 2019 because of tax adjustments

- FB and GOOGL are killing it

Compare fundamentals: Free cash flow to the firm

- SNAP is bleeding

- Twitter’s return to investors has been tiny

- FB and GOOGL are massive value generators

Download the full report as a PDF

Aticle by Andrew Stotz, Become a Better Investor.