To create wealth, you need three things: Some cash to start with (though less than you might think!), time and a positive rate of return.

Q1 hedge fund letters, conference, scoops etc

It’s easy to get caught up thinking that, to achieve this, you need your stocks and other investments to power through the roof. (Which is why many investors panic when stock markets correct – however briefly.)

But creating wealth isn’t just about seeing your stocks head higher. There’s another way to create wealth…

I’m talking about saving and compounding. It’s never too late to start – and even if you’re starting late, you could be in better shape than you think.

The magic of compounding

Here’s how compounding works… you invest a sum of money that generates a steady positive return. But instead of taking that return and spending it, you reinvest it by buying more of the original investment. The next year both the original investment and the reinvested interest will earn interest, which you again reinvest.

With compounding, your original investment is growing in size due to repeated reinvestment, and every year you are getting a larger and larger sum of interest. It’s like a snowball rolling downhill, growing bigger in size as it picks up more snow on the way. (We’ve written about this here and here.)

Two hypothetical – and simplified – personas, Jack and Sue, will show how powerful saving and compounding are…

Jack – a small fortune, bit by bit

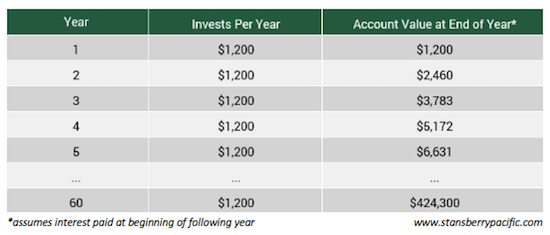

The day Jack is born, his parents start to invest US$100 for him every month in a special investment account that yields 5 percent (during a period when zero and negative interest rates are as foreign as chicken rice on Mars). For 60 years, they make a deposit every month, and interest builds every year.

Jack’s Portfolio (assuming % interest rate)

So at the end of 60 years, Jack’s parents invested a total of US$72,000 (US$1,200/year). Thanks to the magic of compounding, when the interest earned is reinvested and starts earning more interest, Jack’s account balance after 60 years (he never touches it) stands at US$424,300.

During those 60 years, Jack takes the cheap, scenic route through life and as a result, he doesn’t put a penny in the bank. On the day he starts his seventh decade, he’s the proud owner of absolutely nothing. But he also owes nothing. So his net worth is solely the account that his parents started for him when he was born.

This is a (very) simplified version of one of the foundations of personal finance: Start saving early, even if it isn’t very much. Skip the cappuccino, put the kids in cheap castoffs instead of Nikes, and keep your iPhone 6 in a world of iPhone X’s. Take a short flight to Phuket or Orlando (depending on where you are), rather than a luxury cruise to Tierra del Fuego or the Maldives.

But a life of sacrifice doesn’t suit everyone. More importantly, it doesn’t have to be that way. For many people, the structure of lifetime earnings is very different. Compounding works, especially over longer periods of time. But it’s not the only way to build wealth.

Sue starts late – but makes it up

If you know early on that you’re going to take Jack’s path, you’d better start saving early if you don’t want to be sharing food and shelter with your dog when you’re old. But many people are more like Sue.

Sue’s parents didn’t open an account for her at birth. They bring her up and put her through school and let her figure out how to earn a living. So Sue gets a job and rises through the ranks.

Sue isn’t good at keeping her money. She fancies Jimmy Choo and Kate Spade, and shiny cars that roar. She gets a puffy coffee beverage every day, and never cooks at home. She earns a lot… and spends it all. And by middle age, she owns nothing – and owes nothing. Through middle age, she’s like Jack – but without a parental safety net awaiting her.

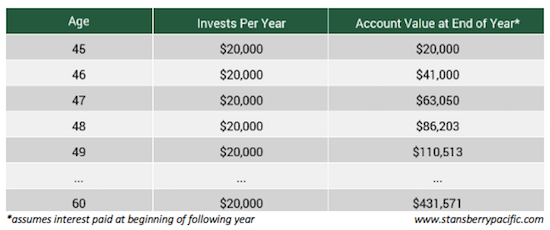

However, unlike Jack, Sue has been building her “personal equity.” She has a career and her earnings are rising every year. On her 45th birthday, she changes course and resolves to put in the bank US$20,000 every year until she’s 60 (totalling 15 years of savings). She also earns a 5 percent return on her capital, compounded annually.

Sue’s Portfolio (assuming 5% interest rate)

she has a net worth of US$431,500, very close to Jack. Sue starts four and a half decades after Jack, so the power of Sue banks a total of US$300,000, and thanks to compounding, by the time she’s 60, compounding has much less time to work for her. And she keeps a lot more of what she earns. And Jack and Sue get to about the same financial place by the time each of them turns 60.

Sue isn’t so unusual

Sue’s scenario happens all the time. Saving when you’re younger is difficult for many people. Eventually, your kids leave home, or finish university, and suddenly you have more money to spend. Or the flat or house is paid off and the monthly mortgage bill vanishes. Or a relative passes and leaves a small bundle. (Seventy percent of people in Hong Kong expect to leave an inheritance and the average amount left behind is US$146,000.)

Or you get a raise at work and decide to put off the five-star holiday or the new car or the bigger house in favour of starting a nest egg. Whether it’s a lump sum or an accelerated savings plan, it can ensure the retirement of the Sues of the world.

In Asia, many entrepreneurs spend decades building up their businesses and paying themselves very little so that they can reinvest in their business. When the business is ready to be sold or passed on, the founders will be older – and will suddenly have a lot of money on their hands.

It’s never too late to start saving. Saving a big chunk of money later in life is a realistic scenario for a lot of people – maybe more realistic than saving a regular amount every month starting from a young age. If the amount you’re able to put away for later on is large enough, it can compensate for less time to compound (and a lower savings rate).

If you’re middle-aged and haven’t really had a chance to keep much money in the bank yet, you can start right away and still retire comfortably. It’s never too late to start creating wealth.

Good investing,

Kim Iskyan

Publisher, Stansberry Pacific Research