Good morning!

Q1 2021 hedge fund letters, conferences and more

In this week’s Dirty Dozen [CHART PACK] we look at the largest drawdown on cash since June 18’, the easiest financial conditions since January 18’, a large global credit impulse that’s rolled over, resilient market breadth, a breakout in risk-assets, and a breakdown in safe ones. Another long USD pair and more…

Let’s dive in.

- Investors decided that now is a good time to start running down their cash balances and dramatically up their risk. BofAML points out that cash just saw its largest 2-week outflow since June 18’. Smart, smart, smart…

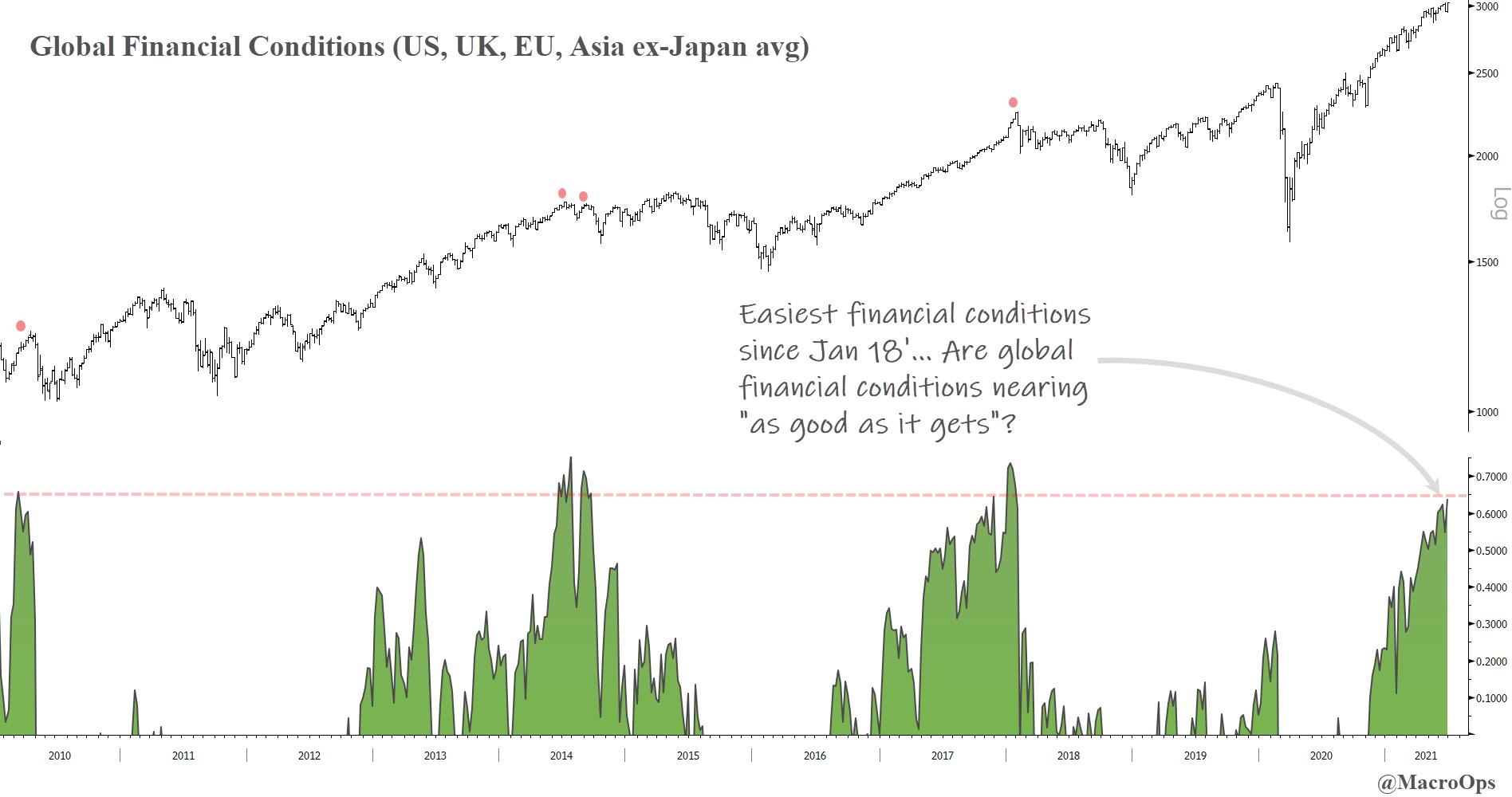

- Global financial conditions haven’t been this loose since Jan 18’. 2018 is starting to pop up a lot in my research. Plenty of similarities to back then… Collective members know what I’m talking about. Anywho, you think we’re nearing the “as good as it gets” point?

- These conditions have been eased by an incredibly large global credit impulse. An impulse that peaked at the start of the year. The economy and market tend to reap the benefits of a large credit impulse for 12-18 months after the impulse has peaked.

- Our long-term US Market Breadth Oscillator shows how well breadth continues to hold up.

- This strong breadth and easy financial conditions make it odds on the SPX’s upside breakout from its 2-months of sideways ranging action will see further bullish follow-through.

The measured move target is an Elon Musk approved 4,420 or roughly 3%+ above current prices.

- In another sign we’re shifting into full-on risk-on we saw bonds breakdown below their 2-month bearish wedge. Expect bonds to fall (yields up) until they hit the equity market’s uncle point.

- Precious metals are likely to trade sideways to lower until that uncle point is reached and this period of risk-on is over. Our CoT oscillator shows that small specs bought the recent dip, which isn’t a great look. Further pain will help wring out this excess positioning.

On a positive note, PMs soon enter their strongest period of seasonality over the next 2-months.

- MS shared some great charts last week that seems to confirm the “controversial” take that giving people bundles of free money actually makes them reluctant to work… A total head-scratcher, I know…

- While a number of transitory components of CPI are rolling over (used cars being an example), more sustainable components are just starting to rise.

MS writes: “Rents have continued to firm across recent CPI prints alongside an improving labor market picture, a relationship that resonates well with our shelter model. As the labor market continues to heal in line with our economists’ expectations, a V-shaped recovery for rents remains our base case.”

- While the FOMC surprised many with their more hawkish (than expected) bent and obstreperous dot drawings. The ECB errored on the opposite side, seemingly wanting to foei gras some Dove livers…

- 11. We pointed out the long US dollar call on the button (link here) but now may be an opportune time to add to one’s EURUSD short.

EURUSD long positioning is still in the 90th percentile. It’s entering a period of weak seasonality. It’s in a Bear Quiet regime. Yields differentials are turning against it. Momentum is as weak as it gets. And Citi’s FX Euro Pain Index shows there are a LOT of trapped longs.

- The pair is trading in the middle of a longer-term sideways range. It’s currently in a minor bear wedge. A break below would offer a good spot to enter or add to your short.

If you enjoy reading these Dirty Dozens each week then please feel free to share them on the Twitters, forward them to a friend, or translate them via smoke signal, etc… Every bit helps us get our name out there.

Thank you for reading!

Stay safe out there and keep your head on a swivel.

Article by Alex Barrow, Macro Ops