Bought into Just retirement group at about 92p a week or so ago. Again, a small position due to volatility, this is 2.5% of my portfolio. I delayed posting this as I wanted to avoid moving the price up and wanted to try and pick some more up at a lower price – but as it is now 100p that isn’t happening any time soon.

Q3 hedge fund letters, conference, scoops etc

This is a life assurer with a 911m market cap trading at a price to book of around 0.5. It has a yield of about 3.4% and a forecast PE of around 5.4. In summary, it is cheap.

I bought into a predecessor firm of this back in 2014 I got out more or less even. Just bought out Partnership Assurance in mid-2016.

The firm may well need additional capital. This doesn’t worry me excessively. Much of this appears to be down to new business strain. Every time they write a new policy they need to allocate some of their capital to do it. They are being successful at writing new policies. Each time they do this a profit is booked. This obviously creates incentives to fiddle numbers / write economically unprofitable business to get at an accounting profit. As a non-actuary / non-insider it is impossible for me to tell whether they are doing this. Self-delusion and the innate complexity of this sort of business being what it is I am not entirely sure if insiders know whether they are doing this. Lots of banking executives bought shares all the way down – the complexity of their own business, and their understanding of it was their undoing.

Having said this, the board is has a few actuaries and a few other more well-rounded business types. It is also heavily regulated so I would hope the books are accurate and there won’t be any unpleasant news in the future. That there is always a level of opacity to banks / insurers which I think means they should always be a bit of a discount. They are the difference between two large numbers, neither of which are ever entirely known until they are wound up.

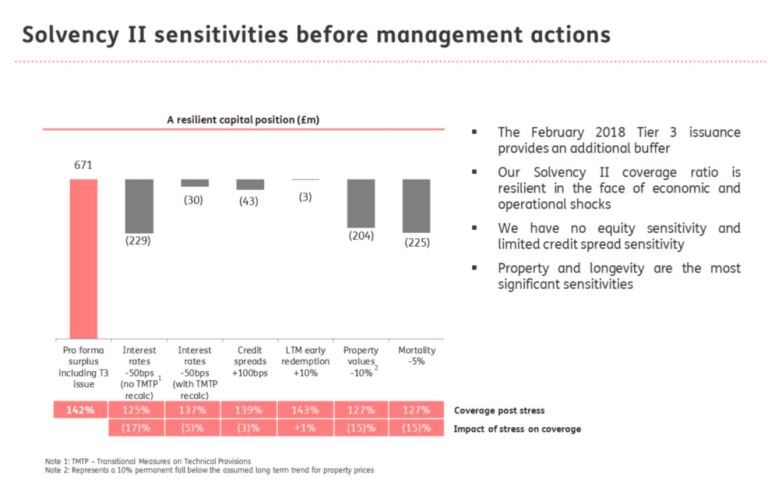

Back to their capital position, it is a bit precarious but is not terminal as is illustrated by this slide (P38).

They are planning to issue convertible bonds which will shore up the capital position, but which will dilute shareholders by c50% if tier 1 capital is below 75% of requirements. If we assume I am diluted by 50% straight away it puts us on a price to book of c70% or a PE of c7.2. Not excessive.

I should also note that Fitch upgraded their credit rating to stable, gave them a financial strength rating of A+ and an issuer default rating of A. We all are aware of the limitations of ratings agencies – but it at least suggests the business is being sensibly run / is stable. They also commissioned a report – which I don’t think is worth the digital paper it isn’t written on – which is here.

A major uncertainty surrounding the stock – how PRA/ PS 31/18 was going to be handled has been resolved. As I understand it they (and others in the industry) had written a bunch of policies in a way the regulator didn’t like and suggested they needed more capital for. The regulator has now backtracked so the risk of needing additional capital due to this has decreased. The share price jumped 20% when this was announced on 10th December, before falling back to almost where it was before due to December market falls.

I think managed carefully there is the potential for growth in this stock. They work in 3 areas, defined benefit derisking, individual annuities and lifetime mortgages.

When an insurer sells an annuity they get a pot of money, that they need to invest. Lots of this goes to government bonds – as they are ‘risk free’. (Co-incidentally the government also has lots of bonds to sell and controls the regulator, practically mandating that bonds are bought). However, some capital can go to fund lifetime mortgages – paying some guy say £50k on his £100k house. This will then grow at a given interest until he dies / moves out – ideally earning a decent rate. As long as the portfolio is structured correctly so liabilities can be met having some of this in there can boost returns, everything works. I believe Just has some of the biggest exposure to lifetime mortgages out there.

This can be coupled with Just Retirement Group’s knowledge / work on impaired annuities (people who are going to die sooner) and you can see how this can start to work very nicely over years to come.

There are risks to this – apparently from the conference call if property prices are flat it costs them £50m of solvency capital, I dont know how this squares with the chart showing a 10% fall in property prices causes a £204m cost. Probable they assume a c2.5% rise each year. They have a negative equity guarantee (imposed by regulation) so the lifetime mortgage can’t eat into the rest of the estate.

I don’t like the defined benefit de-risking business much – commoditised with lots of competition – might be useful to them for reasons I don’t understand however / be less competitive than I assume. This is important as they are doing lots of business here.

With an ageing population / high house prices there is structural growth in the marketplace for this sort of product if it can be done correctly.

My hope on this is everyone does their job properly, there are no blowups and the market eventually regains faith that things are going to work out returning it to a price similar to Aviva / LGEN, ie book value or an 8/10 PE. This will more or less double the existing share price. I think the current discount is excessive and unwarranted. The entire insurance sector seems cheap to me so it might be an area I explore further. There is absolutely no incentive for anyone to establish an insurer right now. Also, many of them trade near / under book – every pound of shareholders funds invested gets you less than a pound of additional market cap – not a sustainable state of affairs.

As ever, comments are welcome.

Article by Rob Mahan, Deep Value Investments Blog