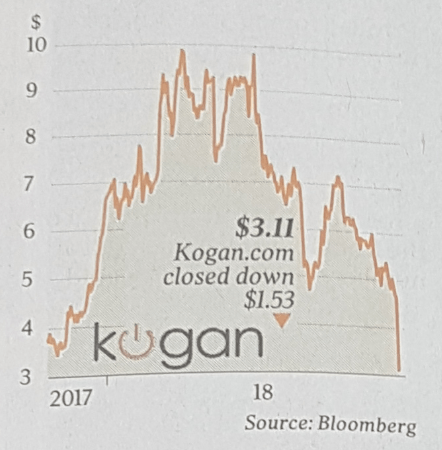

The media are reporting the 33 per cent fall in Kogan’s share price today (30Oct18), saying that since the introduction of new Australian taxation laws requiring online retailers to add the Goods & Services Tax (GST) on imported items below 1000 dollars, came into effect 1st of July 2018 (source).

Q3 hedge fund letters, conference, scoops etc

For non-Australians, GST is a Value-added Tax (VAT), where the business collects the 10 per cent tax added onto goods and services, and pays the tax collected to the Australian Tax Office on a (to my knowledge) quarterly basis.

Before this loophole was eliminated, Kogan enjoyed the supply cost advantage of selling items below $1000 without tax, by directly imported goods into Australia from overseas.

Kogan’s influence was limited, as it was at the mercy of politicians and lobbyists wanting to close the tax loophole. Harvey Norman founder and chief executive Gerry Harvey, went on the warpath to have this new law introduced.

Kogan’s dependence on outside factors to maintain this advantage is well outside their circle of influence.

This supply cost advantage is a weak form of competitive advantage. When a company enjoys a competitive advantage, we need to, as investors, identify what type of competitive advantage it is, and determine its relative strength.

Supply advantages are generally characterised as weak forms of advantage, as the business enjoying the advantaged is not in direct control of the advantage.

A competitive advantage will generally fall into two categories;

- Within their circle of influence, or;

- Outside their circle of influence.

Coca-Cola has enjoyed competitive advantages in the form of demand advantages. Demand advantages arise because of customer captivity that is based on habit, on the costs of switching, or on difficulties and expenses of searching for a substitute provider.

Additionally, a competitive advantage that doesn’t earn higher rates of return on invested capital compared to its competitors cannot be considered a competitive advantage. But I should add that a competitive advantage may take time to play out financially, which makes it that bit more difficult to recognise.

The market recognised that closing the tax loophole will erode Kogan’s ability to earn higher rates of return on invested capital, hence the 33 per cent fall in the share price and a fall of 70% since the June peak of $10.80.

But has the market overreacted?

How will this loss of supply cost advantage affect Kogan’s ability to grow cash flows?

As reported by the media, Kogan’s direct import sales accounted for 18 per cent of its business last year, and 37.4 per cent of sales had fallen in the first three months of the financial year (July to September) compared with a year ago.

Let’s put this into perspective.

So, 6.73 per cent of the 18 per cent in imported sales lost in the first three months of the financial year. And 18 per cent of revenue was $17,216,231 ($412,312,395 X 0.18) and 6.73 per cent works out to be $5 million (rounded up).

Let’s assume that across all four financial quarters that the loss of revenue is the same, for calculation sake.

So, a loss of $20 million in revenue.

As 3.40 per cent of revenue is converted into reported net earnings (net margin), we’ll deduct $680,000 ($20m X 0.034) from last full year’s reported earnings to arrive at $13,430,993.

Unless I’ve screwed up any of the calculations, the impact is wholly insufficient to the bottom line.

Let’s do some [arse]sumptions

Net earnings grew four times in size from 2017 ($3,739,865) to 2018 ($14,110,993). Ideally, we use a 5 to 10-year average growth rate, but purposes here we’ll assume that net earnings will grow at 25 per cent.

Then, you would expect approximate net earnings of $16,788,741.

Assume we brought at $3 per share today, which at the time was earning a 5 per cent earnings yield (EY) and a free cash flow yield (FCFY) of 7 per cent. If Kogan produces our expected goods, then our yields will increase to 6 per cent for earnings and 8.75 per cent for free cash flow (assuming all else being equal).

Just as supply cost advantages generally fall outside the businesses circle of influence, so does the movement in share prices for us investors, therefore, instead of trying to anticipate what the market will do from here, focus on what is in our circle of influence. That is our ability to read, question news reports, and gain a deeper understanding of the fundamental economics of the business, to take advantage of favourable circumstances.

Unless there is more news that would warrant the 70+ per cent share price fall, then I’d assume that the market is overreacting.

The important question I haven’t yet asked is; do current returns (EY or FCFY) compensate you for the risks?

I leave the rest in your capable hands.

Until next Time Take Care

- Adam Parris

(I don’t own shares in Kogan.com)

P.S. If you’re interested in attending the Value Investing program here in Australia, check out the info here.

Article by Searching For Value