Merion Road Capital Management commentary for the fourth quarter ended December 31, 2020.

Q4 2020 hedge fund letters, conferences and more

Our portfolios generated strong returns over the past year on both an absolute and relative basis. While it is easy to celebrate a good year, we should remember that it was not always smooth sailing. There were many gut checks as a novel virus, deteriorating economic fundamentals, dissipating liquidity ravaged the stock market. Watching the value of our portfolio drop precipitously is hard to do. It was made easier by having an aligned investor base that is similarly focused on long-term wealth generation. I cannot emphasize enough how grateful I am for your support in this regard.

I find it interesting to compare sentiment today to earlier this year. While there have been many positive developments including the release of multiple vaccines and easing monetary conditions, the market’s collective outlook has shifted from bottomless pessimism to boundless optimism. This euphoria is most evident in the abnormally strong price performance of hot IPOs and SPACs, as well as in key sectors such as electric vehicles and technology. The evolution of no-commission trading services and trendy platforms like Robinhood have magnified the prevalence of gambling in the market. Look no farther than a popular subreddit, wallstreetbets, that has more than 1.8mm subscribers. I began my Q2 2020 letter discussing this topic and it appears to be even more pronounced today. Yet the market is not a single entity. It consists of thousands of companies, each with their own competitive dynamics, financial outlook, and valuation. Many companies are still attractively priced and buying/holding them today should result in a good return over the foreseeable future.

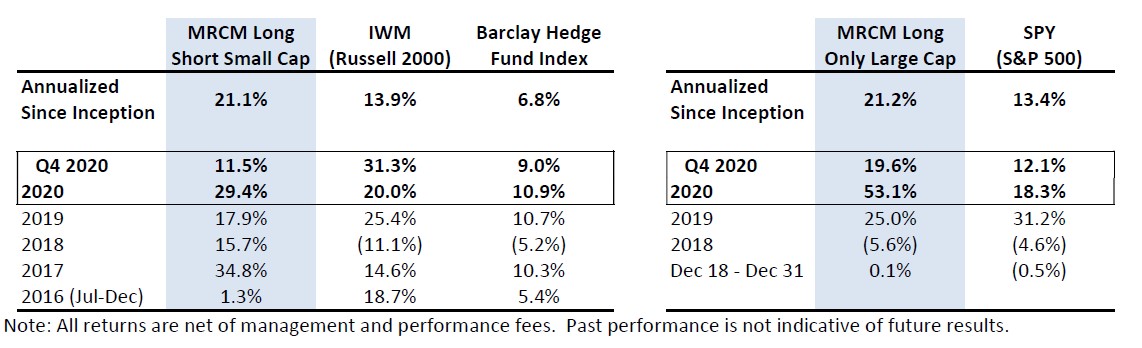

The large cap strategy was up 53% net of fees in 2020. One of our larger contributors for the year was Pinterest (“PINS”). I’ve never discussed PINS before as it is not a major holding. That being said the stock increased about 250% during the year, so even our mid-tier exposure was quite impactful. I initiated our position at the end of last year as the market penalized the company for missing revenue estimates. I added in Q1 as the stock continued to fall based on potential advertising headwinds. The thesis was always a simple one. PINS has a phenomenal product with an engaged, loyal, and growing customer base. They have the ability to increase revenue per user through improved adtech and services (i.e. shopping). There are limited social media properties and advertisers need alternatives to keep the Google / Facebook duopoly in check. And PINS is a trophy asset that should attract retail investors looking to own a name that they know. I have been reducing our exposure as the price has appreciated and the return profile is no longer as attractive.

Four Corners (“FCPT”) was a large detractor for the year as I completely exited our position in March. As a REIT, FCPT operates with relatively high leverage (though within the REIT universe FCPT is conservatively financed). This perceived risk was heightened by their focus on restaurant properties. Retrospectively I should have held or added to our exposure. But part of my job is risk management, and I simply did not feel comfortable holding it given the uncertainties at the time.

Last quarter I discussed our new investment in Ferguson PLC (“FERGY”). I have continued to add to our holdings making it one of our largest positions. In November they announced the tuck-in of an HVAC distributor and in December reported another strong quarter with 3% organic revenue growth and operating margin improvement. On January 4th FERGY announced that they have entered into an agreement to sell their UK subsidiary. This is an important milestone for the company as it is the last holdover from their European business. With this transaction behind them, management can direct their attention to listing on a US exchange. While the US listing does not affect fundamental value, it will likely help bridge the valuation discrepancy versus its peers as it will open the company up to a whole new group of investors and result in index inclusion.

The small cap portfolio was up 29% net of fees in 2020 while averaging a beta adjusted net exposure of 42%. Our largest contributor during the year was our largest contributor last year as well, Mastech Digital (“MHH”). Our position in MHH has fluctuated since I first bought the stock back in 2018. You may recall that I initially acquired the stock upon their acquisition of Infotrellis, a data and analytics company, as I did not believe the market was valuing the combined entity correctly. This year I added as the stock sold off in March and April, and even more ahead of the Russell rebalance as I correctly forecasted their inclusion. With a now delevered balance sheet MHH has recently announced and completed another acquisition of a company called Amberleaf. Amberleaf will serve as a bolt-on to MHH’s data and analytics division addressing the sales, marketing, and customer acquisition vertical. Based on management commentary we can estimate that the transaction was completed at an attractive multiple of just 5.5x EBITDA. So far, the market has not given the company much credit for this latest transaction, but it will be hard to ignore as the company begins to report consolidated figures.

Our largest detractor was Rocky Mountain Chocolate Factory (“RMCF”) which got caught in the cross-hairs of the pandemic. As I discussed in my Q1 letter, my entry was poorly timed though I continued to hold as I thought that the company possessed enough liquidity to manage through the crisis and that there would be tremendous upside should they make it to the other side. While I still believe the latter to be true, I ended up selling the stock in the back half of the year as I became increasingly concerned about the company’s ability to manage costs and their failure to secure additional financing.

During the past quarter initiated a position in Lensar (“LNSR”). LNSR is a micro-cap spin-off from PDL Biopharma that has faced selling pressure from investor rotation as well as tax-loss harvesting. I wrote a longer piece on LNSR that I posted to my website, and for brevity sake I will refer you to www.merionroadcapital.com/letters if you are interested in reading more.

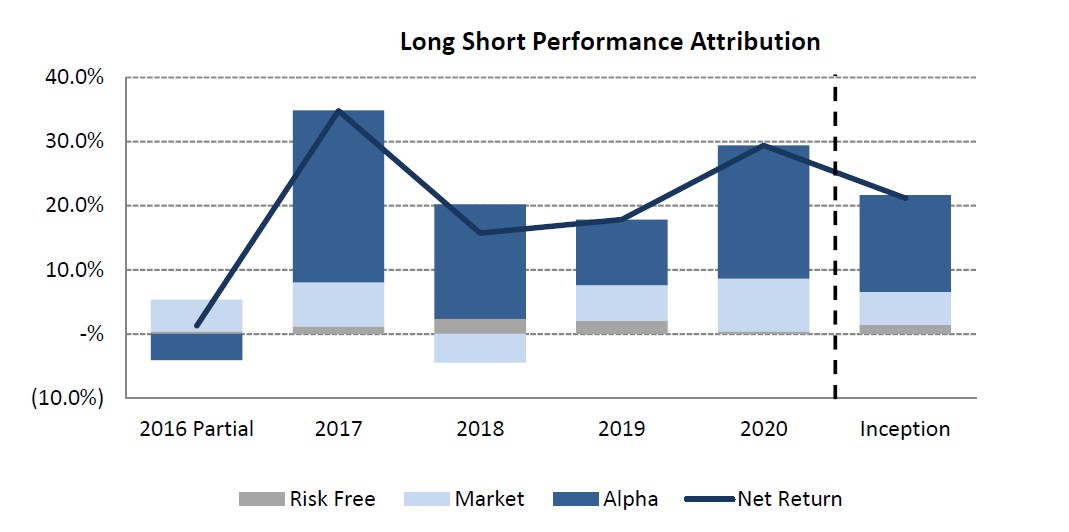

The table below provides the performance attribution of the portfolio. Over the past 4.5 years we have gained 21% a year net of fees. 1% has come from the risk-free rate (i.e. if I had just parked our cash in treasuries), 5% from the market (the market has returned nearly 14% though I have operated with beta adjusted net exposure of just 37%), and 15% from good stock picking. The fact that the bulk of returns have come from stock selection is a point I am proud of.

It is unlikely that 2021 will be anything like 2020, and we should not expect to achieve similar performance.

Nonetheless I will always do my best to find the best opportunities to deploy our capital. I wish everyone much success in the year ahead.

Sincerely,

Aaron Sallen