FORECASTS & TRENDS E-LETTER

by Gary D. Halbert

March 5, 2019

IN THIS ISSUE:

Q4 hedge fund letters, conference, scoops etc

- 73% of Americans Die With Debt – $62,000 on Average

- What Happens to Your Debt When You Die? Depends

- Student Loan Debt: Some is Forgiven on Death, Some Not

- Private Student Loans Are a Very Different Situation

Overview

Long-time clients and readers know I like to write about topics that interest me, and this week is no exception. I debated whether to write about today’s topic since it deals with death and debt. However, as you’ll read below, almost three out of four Americans die with outstanding debt, and the average debt balance upon death may surprise you.

I will also discuss what generally happens when people with outstanding student loans pass away. It can be very complicated. That’s why I spend considerable space below addressing it. While you may not have any outstanding student loans, I’ll bet you know someone who does – maybe your kids or relatives’ kids or your close friends’ kids. If so, feel free to share this with anyone who might benefit from it.

73% of Americans Die With Debt – $62,000 on Average

I’ve known for many years that some Americans pass away with unpaid debt, and sometimes that debt is greater than the value of their estate. Yet what I didn’t know until a few weeks ago is that 73% of Americans who die have unpaid debt well beyond their funeral expenses. That’s much higher than I would have thought.

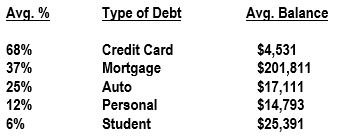

Likewise, I did not know that the average debt balance left behind is almost $62,000. Does that surprise you? It did me. Both figures, the 73% and the $62,000, come from Experian PLC, a leading credit card reporting bureau and Credit.com. As we’ll see below, more Americans die with outstanding credit card debt than any other category of loans.

This is shocking in one sense: Credit.com, an online lender, says half of the people they survey say that they don’t expect to die with a stack of unpaid bills to be dealt with. Only 30% of all Americans surveyed believe they are doomed to be in debt until the day they die. Yet what people will say in a survey and what they do in real life are often very different, as we’ll see below.

I suppose it’s encouraging to see that only 6% of Americans who die still have outstanding student loans, but the average balance is higher than any other category except home mortgages. I’ll explain more about what happens with student loans when people die below.

What Happens to Your Debt When You Die?

For the most part, your debt dies with you, but that doesn’t mean it won’t affect the people you leave behind. If someone has enough assets to cover their debts, the creditors get paid and beneficiaries receive whatever remains.

But if there aren’t enough assets to satisfy debts, creditors lose out; they may get some, but not all, of what they’re owed. Family members do not then become responsible for the debt, as some people worry they might – if they are not co-signers on that debt. In accounts with co-signers or co-applicants, the debt usually falls on that person’s shoulders.

That’s the general idea, but things are not always that straightforward. The type of debt you have, where you live and the value of your estate significantly affects the complexity of the situation. There are lots of ways things can get messy.

Say your only asset is a home that other people rent and live in. If that asset must be used to satisfy your debts, whether it’s the mortgage on that home or a lot of credit card debt – the people who live there may have to take over the mortgage, or your family may need to sell the home in order to pay creditors.

Student Loan Debt: Some is Forgiven on Death, Some Not

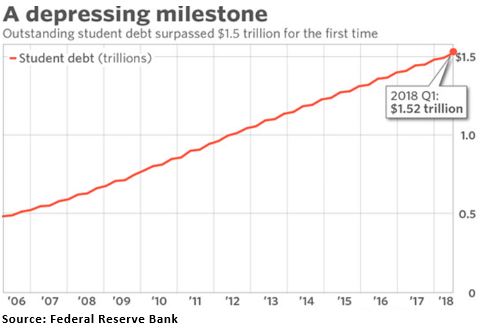

Student loan debt has exploded over the last decade from $600 billion to above $1.5 trillion early last year. It is owed by 44 million borrowers with an average balance of $37,000. Many graduates have student loan balances that exceed their annual income in their first jobs.

Over 9% of student loans were delinquent by 90 days or more in the 3Q of last year, up from 8.6% in the 2Q and the biggest quarterly jump on record. Sadly, the factors that have driven the explosion in student loan debt haven’t changed, and many Millennials now regret that they took on that debt.

The question is, what happens to your student loan debt when you die? That depends on what kind of student loan debt you have – federal loans or private loans.

If the borrower of a federally backed education loan dies, the loan gets canceled, and the government discharges the debt, according to the Federal Student Aid Office of the Department of Education. But be aware that the amount discharged may be taxable as income to the estate of the deceased borrower.

That means if all the student has is federal student loans, their family won’t have to pay the debt.

That goes for Direct Subsidized Loans, Direct Unsubsidized Loans, Direct Consolidation Loans, Federal Family Education Loans and Federal Perkins Loans.

In the case of federal loans, your survivors will have to provide proof of the death to the student’s loan servicer(s). Acceptable forms of proof include an original death certificate, a certified copy of the death certificate or an acceptable photocopy of same.

To pay for their student’s education, their parents may have taken out “Parent PLUS Loans,” which are also federal loans, but in this case the parent is the borrower instead of the student. With these loans, if the student dies, the parents won’t have to repay the loan.

Private Student Loans Are a Very Different Situation

If the student or parents have student loans from a private lender, like a bank, their unpaid balance is more likely to become the family’s problem if the student dies.

Millions of college students are in this boat. The number of private student loans has been increasing, according to the nonprofit Institute for College Access & Success. In recent years, over 1.4 million undergrads took out private loans to help pay for college annually.

Some private lenders will forgive the debt if the student dies, but most won’t be that lenient.

“Some lenders of private (non-federal) student loans offer a death discharge if the borrower dies. These include Sallie Mae, New York’s Higher Education Services Corp., Wells Fargo and Discover,” reports Edvisors, an online resource for paying for college.

That’s not the norm, though. Their lenders, credit card companies and others expect to be paid by the estate. They can file a claim in probate court, which oversees the handling of their estate. Because it may take a while to sort out the finances, creditors may agree to settle with the estate for less than the total debt. Lenders will look for money in a couple of likely places: their estate and any loan co-signers.

Their Estate: Contrary to popular belief, people don’t have to be mega-rich to have an estate. One’s estate includes assets owned such as cars, bank accounts, jewelry, their home (if they own it), etc.

Each state has its own laws governing estates. If the deceased is married, jointly-held property like a home or joint bank account should be safe from creditors.

Their Loans’ Co-signers: If their parents or any other relatives co-signed their college loans, they could be on the hook for the student’s debt if they die before the debt is paid off. And 9 out of 10 private loans have a co-signer, according to Credit.com.

If that’s the case, the survivors should look into the lenders’ “compassionate review process.” On a case-by-case basis, some lenders will waive the co-signer’s legal obligations if the co-signer is on a fixed income and simply isn’t capable of paying off the debt.

If the co-signer is capable of making loan payments, the lender is less likely to forgive the loan.

Making matters worse, the death of the student borrower can trigger default, meaning the entire balance of the loan comes due immediately, warned student loan expert Heather Jarvis.

As you can see, private student loans can be complicated. The above discussion is not intended to be comprehensive, but hopefully it may be just enough to give those you know with student loan debt some things to think about.

Finally, the fact that 73% of Americans die with debt, and quite a lot of it, is just another sign of the times we live in. Young people are encouraged to go to college before they graduate high school – even if that means going into student debt.

Yet not everyone should go to college, in my opinion. I’ll leave it there for today.

Again, feel free to share this with anyone you think could benefit from it.

Best regards,

Gary D. Halbert

SPECIAL ARTICLES

What Happens When People Die With Debt?

Dems/AOC Reintroduce Bill to Tax Securities Transactions

US/China Optimistic Trade Deal Will Finalize Before Month-end

Gary’s Between the Lines blog: Can the US Grow Its Way Out of Debt? The Answer is YES!