Portfolio Manager Chuck Royce and Co-CIO Francis Gannon recap 3Q18 and discuss why they’re confident in the long-term prospects for small-cap cyclical stocks.

Q3 hedge fund letters, conference, scoops etc

- What is your take on the Russell 2000 Index making a new all-time high in 3Q18?

- What was most interesting to you about the third quarter?

- Did large-cap’s outperformance in 3Q18 look like a catch-up period or the start of a more lasting trend?

- What risks do you see that other investors may be overlooking?

- Why should investors be concerned about low volatility?

- What are your expectations for small-cap returns going forward?

- What’s your view of the health of the U.S. economy?

- Are you confident in the prospects for active management in the current environment?

- Why are you more cautious about growth stocks and defensive industries?

- What is the current case for cyclical small-caps?

- In this light, what factors do you think spurred the strong showing for industrial companies in 3Q18?

- Are you concerned that small-cap materials stocks did not recover the way that so many industrial stocks did?

- How are you positioning your portfolios at a time when small-cap valuations are so high?

What is your take on the Russell 2000 Index making a new all-time high in 3Q18?

Chuck Royce We’re certainly pleased with the pace of returns. It’s impossible not to be for any small-cap specialist like ourselves. It’s also interesting—and, I should add, anomalous—that performance has been so consistent over most of the last three years. The last correction of 10% or more occurred between June 2015 and February 2016. In fact, in the last 21 calendar years, only three didn’t have a small-cap correction of at least 10%—and two of them were 2017 and, so far, 2018.

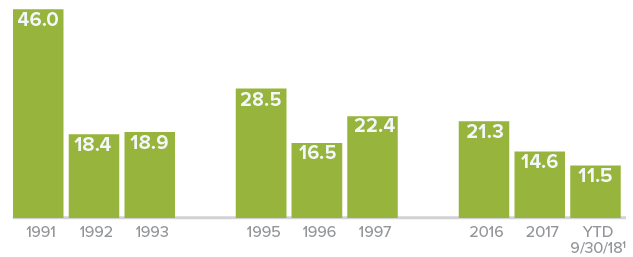

Francis Gannon And with the Russell 2000 up 11.5% year-to-date through the end of September, we could see three consecutive years of double-digit small-cap returns, something that hasn’t happened in more than 20 years—and has only happened twice before since the inception of the small-cap index. Interestingly, both of those instances were in the 1990s, from 1991-1993 and from 1995-1997.

3-Year Periods of Consecutive Double-Digit Small-Cap Returns

Russell 2000 Index Returns (%)

1 Not Annualized

What was most interesting to you about the third quarter?

CR I think there were two very interesting and important developments. The first was the rise in the 10-year Treasury rate. I’m really surprised that we didn’t see more attention paid to the fact that it hit 3% in mid-September and stayed at or above that rate through the end of the month. We’d all been waiting for it to reach that level for so long, and when it finally happened, it seemed that very few people noticed. I do think it’s significant, though. In fact, we talked about two obstacle on the road to normalization at the end of the first half—first was the disconnect between the terrific business results for many cyclical industries versus their relatively underwhelming stock price performance and second was the sluggish pace of increase for the 10-year bond. So we were very pleased that the shares of many cyclical businesses began to gain ground in the third quarter and that the 10-year remained above 3%—even if it didn’t attract a ton of attention.

FG I think it was also notable that investors once again shook off the headlines about the potential dangers of tariffs, trade wars, inflation, and rising rates to keep equity performance humming. This was in line with our own expectations—a lot of the pessimism around the market has looked exaggerated to us. It definitely seems as though investors were more influenced by the current tide of positive news, such as ongoing growth, strong earnings, and high employment, than by the risks just mentioned. These risks have not yet been fully realized—or realized at all.

Did large-cap’s outperformance in 3Q18 look like a catch-up period or the start of a more lasting trend?

FG It’s true that large-caps have led historically when investors become wary of continued growth. But we wouldn’t go so far as to say that their relative edge in the third quarter means that economic growth is nearing its last stage. We see enough signs of ongoing growth—including what the companies we hold are telling us—to underscore our confidence that growth will remain healthy, even as it’s possible that the pace could slacken. So the third quarter’s outperformance for large-cap, which may have been driven, at least in part, by diminishing fears of the negative effects of tariffs, looks more like a catch-up after those stocks lagged significantly in the first half. More important, we believe that cyclical companies will continue to emerge as leaders, which will allow small-cap stocks to stay ahead of their large-cap siblings.

What risks do you see that other investors may be overlooking?

CR I think the lack of volatility is something that a lot of investors are overlooking, and not being prepared for more volatile markets is a genuine risk. Of course, most people tend to forget about volatility until it hits, especially when returns are as high as they’ve been. A growing economy doesn’t rule out the potential for a short-term correction because the market and the economy occasionally diverge. I also think investors aren’t paying enough attention to the possibility that contracting financial liquidity, created by a decline in money supply growth in an accelerating economy, could trigger a correction.

Why should investors be concerned about low volatility?

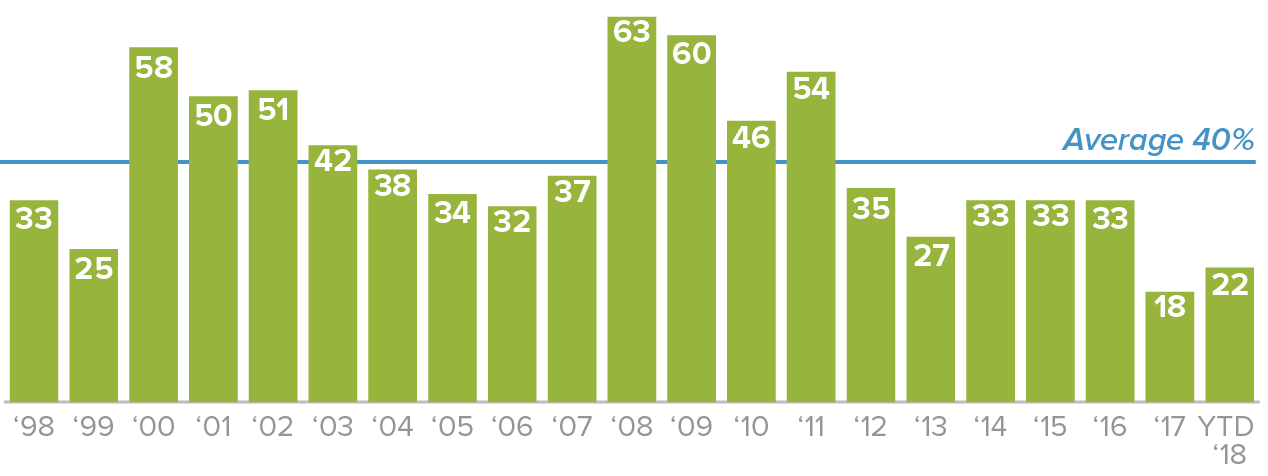

FG What concerns me most is that volatility has been largely absent during a period when small-caps are on course for a third straight year of double-digit performance. Markets have been unusually, eerily calm, reaching cruising altitude with almost no turbulence for an extended period. We recently looked at the historical average of trading days with moves of 1% or more for the Russell 2000—which is 40%. But since the beginning of 2017, only about 20% of small-cap trading sessions have met or exceeded that threshold. However pleasant, these conditions are unsustainable. This is why we feel so sure that volatility will increase—we just don’t know when or to what degree.

Percentage of Trading Days with Moves of 1% or More in the Russell 2000 through 9/30/18 (%)

The average percentage does not include YTD data.

What are your expectations for small-cap returns going forward?

CR They haven’t changed much. We’re still anticipating lower overall returns, higher volatility, and cyclical leadership. I’d describe our perspective as confident but somewhat leery about near-term small-cap performance prospects. There’s an interesting tension in the market right now. Valuations are high, which puts considerable pressure on multiples, particularly when rates are rising. At a time when multiple expansion is harder and harder to come by, the companies that execute best, particularly with regard to earnings growth, stand poised to benefit most.

So I feel good about the longer-term prospects for small-caps, but I think we could see some corrective phases over the next several months. These may not be correlated corrections, however. Instead, we may see more of the rolling sector and industry corrections that we’ve experienced over the last few years. For example, Health Care soared in 2015, corrected sharply in 2016 and has been strong since 2017; Energy has been highly volatile over this same period, as have most Consumer Discretionary stocks. So that pattern could remain in place.

What’s your view of the health of the U.S. economy?

CR I think it’s essentially healthy. Rates, inflation, and wages are each moving up at a manageable pace. We’re encouraged by current earnings and future EBIT growth expectations. The major macroeconomic measures—Leading Economic Indicators and Institute for Supply Management new orders, etc.—are all still robust. I’m also struck by the different views about where we are in the economic cycle. There’s a consensus among many economists that we’re close to end while others—some of whom we respect a great deal—estimate that we’re closer to the middle of the cycle. In other words, no one really knows for sure—but that’s not new.

Are you confident in the prospects for active management in the current environment?

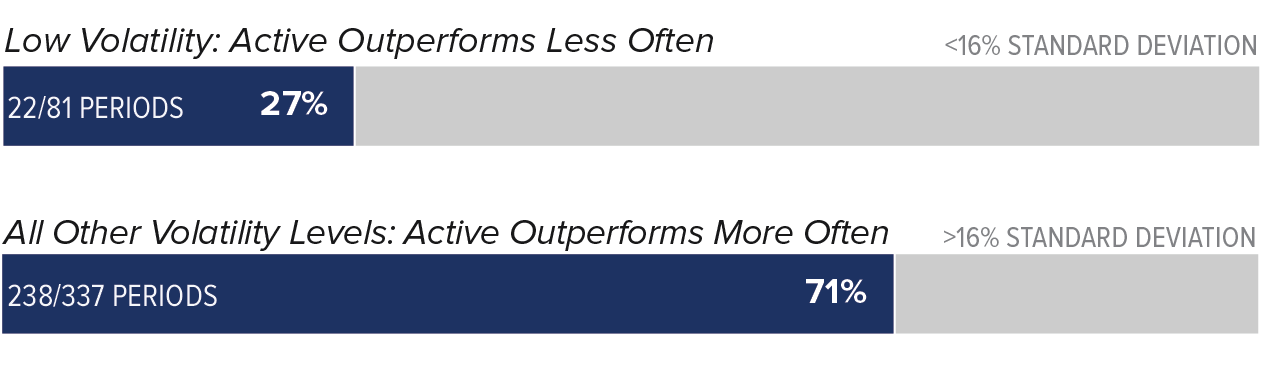

CR We are, especially for the kind of lower-return, higher volatility market that we’re expecting. We’ve done some research that demonstrates what we’ve always suspected was true—that markets with higher volatility tend to be better for active management. This always made sense to us because volatility creates dislocations between a company’s intrinsic value and its stock price. Identifying and taking advantage of these gaps is in many ways the essence of active management.

Percentage Active1 Beat Russell 2000 Within Volatility Levels

Monthly Rolling 5-Year Average Annual Return Periods 12/31/78 through 9/30/18

1 “Active” is represented by Morningstar’s U.S. Small Blend Fund category. There were 539 U.S. Small Blend Funds tracked by Morningstar with at least 5 years of performance history as of 9/30/18.

Standard deviation is a statistical measure within which a fund’s total returns have varied over time. The greater the standard deviation, the greater a fund’s volatility.

FG You can’t invest for the long run simply by loading up on yesterday’s winners. That sounds obvious, but we’re always struck by how many people look at what’s successful right now and just follow along. As active managers with a long-term focus, we have a different task. Our job is to find companies that look capable of surviving difficult or volatile periods so they can thrive when things turn around. Needless to say, you usually can’t accomplish that by stocking a portfolio with whatever’s got the best current results. In fact, we see that as an easy way to lose a great deal of money.

Why are you more cautious about growth stocks and defensive industries?

FG In large part, I think it’s been a function of psychology, as Chuck suggested earlier when he discussed what investors may be overlooking. Investors are often resistant, or at least hesitant, to change when an investment is working, even as the risk of it continuing to work keeps mounting. We think investors are far too comfortable right now, lulled into complacency by historically low volatility and high returns as they stick with the stocks, styles, and/or strategies that have worked through much of the post-Financial Crisis period—the small-cap bio-pharma complex and software, growth stocks, and passive investments.

But as we’ve been arguing, the backdrop has shifted dramatically to one that’s less favorable for defensives and more favorable to cyclicals. We’ve moved past the era of QE, near-zero interest rates, and tepid economic growth. Each of these macro factors has reversed—and reversed decidedly. When we look at the small-cap asset class as a whole, we see many growth stocks and defensive industries carrying both higher valuations and less attractive earnings profiles. This puts them is an especially precarious condition during a period of economic expansion and rising interest rates.

What is the current case for cyclical small-caps?

CR I think the case for cyclicals remains in part what it’s always been—historically they’ve worked best when the economy is expanding because their revenues and earnings tend to grow faster as the economy heats up. As for the current case, we still believe that earnings ultimately drive returns, notwithstanding the oddities we’ve seen so far in the current cycle, such as leadership for growth stocks. Additionally, based on earnings and cash flow quality, we see superior fundamentals in select cyclical areas that other investors have been avoiding or only recently seem to be noticing.

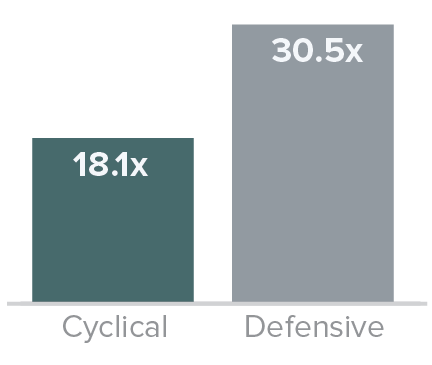

Cyclical Opportunity

Median LTM EV/EBIT¹ Ex. Negative EBIT for Russell 2000 as of 9/30/18

¹ Last Twelve Months Enterprise Value/Earnings Before Interest and Taxes

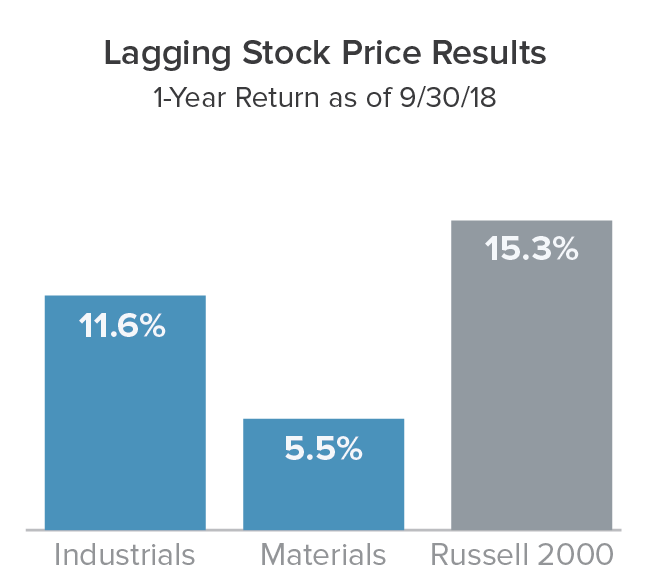

In this light, what factors do you think spurred the strong showing for industrial companies in 3Q18?

FG I think the most significant factor was an emerging recognition of the earnings strength in many of these companies, coupled with their relatively more attractive valuations. This helped industrial stocks make up some ground in the third quarter after they trailed the Russell 2000 in the first half of 2018. Along with Information Technology and Health Care, which have both been very strong this year, the Industrials sector made one of the three largest contributions to return within the Russell 2000 in the third quarter. But they’re just starting to make a move—a sizable valuation gap still exists between small-cap industrials and the rest of the market.

CR In terms of our own holdings in the sector, we feel very good in general about their recent operating and financial results, including some of the areas that gained momentum in the third quarter such as machinery, electrical equipment, and aerospace & defense. As Frank indicated, many industrial companies have been posting strong earnings that seem to be ahead of their respective stock prices, so even in a high-priced market they should still have room to run.

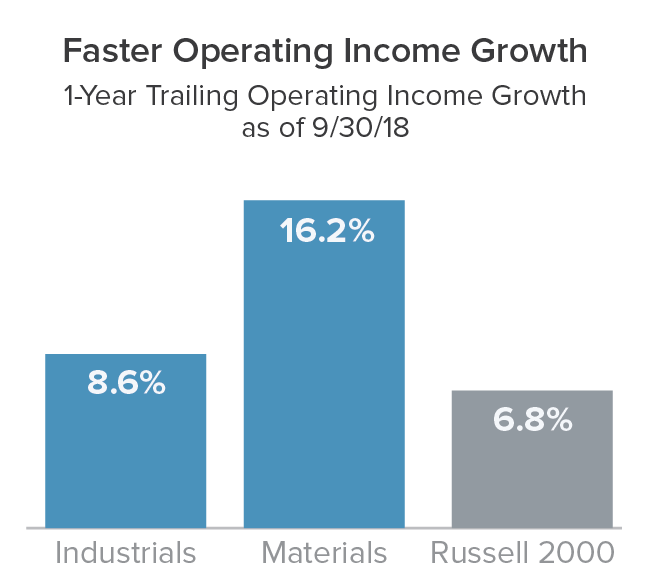

Are you concerned that small-cap materials stocks did not recover the way that so many industrial stocks did?

CR We’re more disappointed than concerned. First, third-quarter results were hurt by a very tough period for the sector’s construction materials industry, which was adversely affected by higher input costs and the lack of any major infrastructure spending. Additionally, the two largest industries within the sector—chemicals and metals & mining—both trailed the index as a whole. Within materials, the bulk of our firm’s investments are in the chemical industry.

As is the case with industrials, we’re confident looking forward. Looking at the Materials sector’s one-year trailing operating income growth shows a similarly vibrant picture to that of Industrials—even more so when you see the interplay between that number and the sector’s one-year return. The combination suggests that investors are missing out on some terrific opportunities to capture the benefits of earnings growth. We anticipate that this will change in the coming months.

How are you positioning your portfolios at a time when small-cap valuations are so high?

CR Buying opportunities are admittedly somewhat scarce—which you can see in the higher-than-usual cash positions in many of our portfolios. But we’re happy to be holding a roster of what we think are great small-cap businesses. In general, we’ve been trimming high valuation holdings and tilting portfolios even more toward select cyclicals. This is a pretty diverse group. It includes alternative asset managers and M&A boutiques, productivity boosting software companies—very timely when labor is scarce, financial intermediaries that look poised to benefit from eventually higher volatility, and contrarian positions in the media and recreational vehicles industries where excess pessimism about future prospects has depressed valuations to what think are attractive levels. So we’re very pleased with how the environment is taking shape.

Article by The Royce Funds