“There isn’t an individual, organization, country, or empire that hasn’t failed when it lost its buying power. To be successful one must earn an amount that is at least equal to the amount one spends. Those who spend modestly and have a surplus are more sustainably successful than those who earn a lot more and have deficits. History shows that when an individual, organization, country, or empire spends more than what they earn, misery and turbulence are ahead.

History also shows that countries that have higher percentages of people who are self-sufficient tend to be more socially, politically, and economically stable. The United States now is spending a lot more money than it’s earning and paying for it by printing money that is being devalued. To improve we have to raise productivity and cooperation. Right now we are on the wrong path.” ― Ray Dalio, Co-Chairman & Co-Chief Investment Officer, Bridgewater Associates, LP

Q3 2021 hedge fund letters, conferences and more

I’ve just pre-ordered Ray Dalio’s new book, Principles for Dealing with the Changing World Order: Why Nations Succeed and Fail. If you are not familiar with Dalio, he is co-chief investment officer and founder of Bridgewater Associates, the world’s largest hedge fund.

Most people probably feel investing is pretty simple. And often it is—until it isn’t. That makes it one of the greatest, most complex games in the world. I view the markets much like the game of chess. It too is a complex game with many moving parts, and one has to respond to those moves as they happen. Some are predictable; some are surprising. Players come to the game with a wide variety of knowledge and abilities. If players are well matched in a particular game, each has a reasonable chance of winning. If a novice faces an advanced player, their odds fade. Up against a chess grandmaster? The odds are near zero. But ultimately, the more one plays, the better one gets.

When it comes to the investment markets, there are many in the game but few grandmasters. Dalio is one of the few: a self-made billionaire on a mission to do good. He’s not perfect, nor is any grandmaster in any space. Dalio attempts to level the playing field, sharing his knowledge on global macro issues, interest rates, valuations, currencies, and capital flows, and how the significant players in the game (legislators, central bankers, etc.) are responding. He covers the moves they are making and what that means in terms of how to think about and position personal wealth.

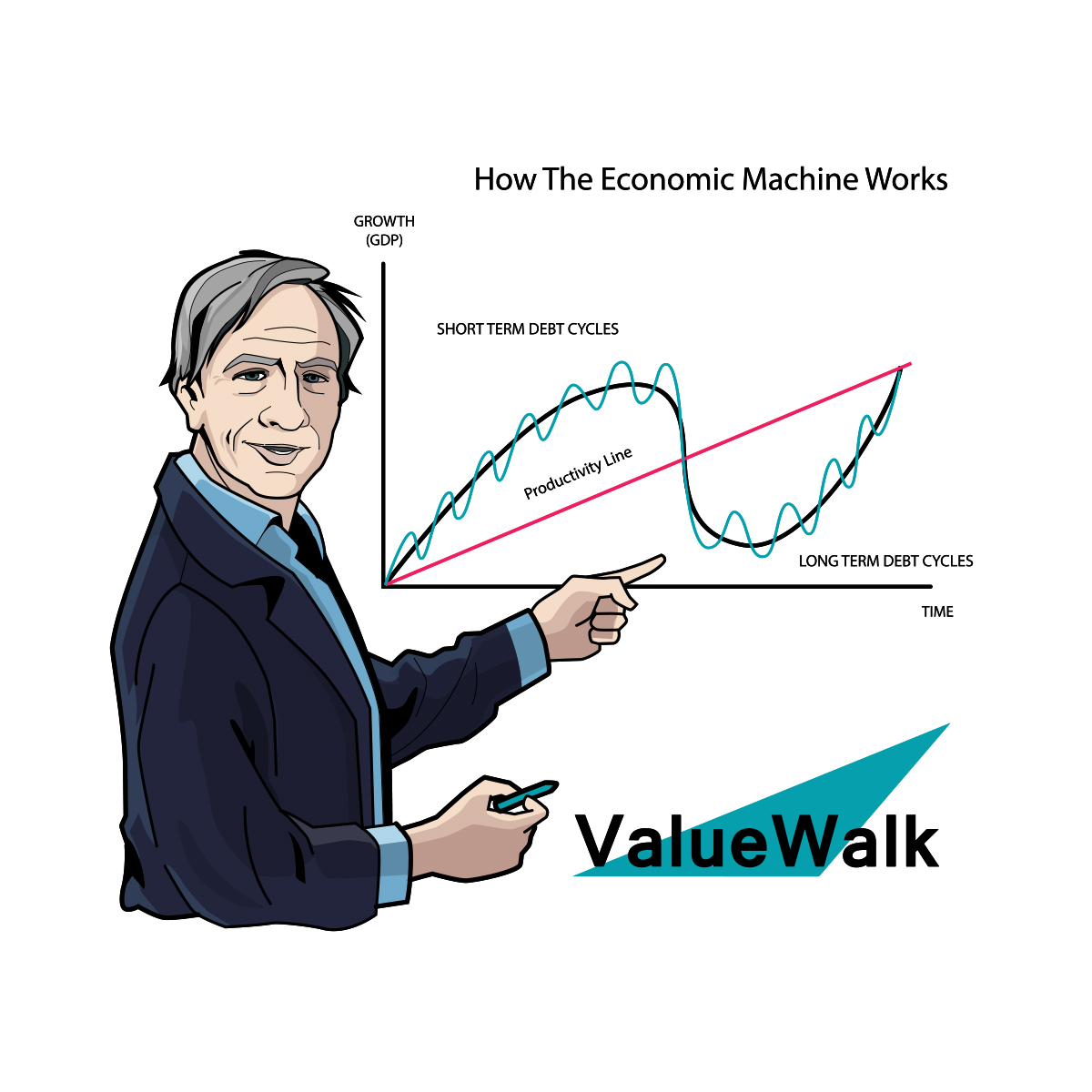

Dalio believes we sit at the end of a long-term debt supercycle. Few of us have experienced one, as the last was in the mid-1930s. Dalio’s grandmaster edge is his ability to see the moves that have been made previously, consider the current state and policy response, and position himself and his clients to profit on what they believe are the probable outcomes.

Here’s what Dalio’s new book covers, courtesy of Amazon’s book preview page:

A few years ago, Ray Dalio noticed a confluence of political and economic conditions he hadn’t encountered before. They included huge debts and zero or near-zero interest rates that led to massive printing of money in the world’s three major reserve currencies; big political and social conflicts within countries, especially the US, due to the largest wealth, political, and values disparities in more than 100 years; and the rising of a world power (China) to challenge the existing world power (US) and the existing world order. The last time that this confluence occurred was between 1930 and 1945. This realization sent Dalio on a search for the repeating patterns and cause/effect relationships underlying all major changes in wealth and power over the last 500 years.

Putting into perspective the “Big Cycle” that has driven the successes and failures of all the world’s major countries throughout history. He reveals the timeless and universal forces behind these shifts and uses them to look into the future, offering practical principles for positioning oneself for what’s ahead.

Watching the end-game of a long-term debt supercycle is about as much fun as watching paint dry. It just takes time for the end to come, and the significant players can push the game into many overtimes. The end-game is painfully slow, then disturbingly fast. We remain in the painfully slow phase. Mauldin calls what’s coming next “The Great Reset”: a reset of the debt and underfunded pension systems. He and I believe it will present this decade—perhaps around 2025 to 2027, but that is a wild guess. It could come sooner or later.

We don’t believe you have to suffer through it. Instead, we see opportunity—just not in the overvalued and overbought cap-weighted indices where most of the money sits today. In the end, we believe the path we are on will lead to inflation. Inflation regimes, from an investment perspective, should be dealt with differently than non-inflation regimes.

Ray Dalio on Inflation

This from Ray:

Yesterday’s [Wednesday, November 10, 2021] inflation report showed inflation raging so you are now seeing inflation erode your wealth. That is no surprise. At this time:

- The government is printing a lot more money,

- People are getting a lot more money, and

- That is producing a lot more buying, which is producing a lot more inflation.

Some people make the mistake of thinking that they are getting richer because they are seeing their assets go up in price without seeing how their buying power is being eroded. The ones most hurt are those who have their money in cash.

Today I am sharing a part of the Determinants chapter of my new book, Principles for Dealing with The Changing World Order, to remind you of key principles that are relevant now. I did this study of the last 500 years to help me and I am passing it along in this book to help you understand and deal with what is happening now. I hope it is of some value for positioning yourself for what is going on. You can pre-order the book. (SB here: I’ve ordered my hardcopy.)

Here are the key principles to keep in mind:

Wealth = Buying Power

Wealth ≠ Financial Wealth

Making Wealth = Being Productive

Wealth = Power

Wealth Decline = Power Decline

For the purpose of understanding the big cycles, it’s worth defining wealth a bit more specifically and looking at its impact on countries that have it or lack it. I believe the following to true and very relevant to what is happening now:

Wealth = Buying Power. Without getting too nuanced, let’s call wealth buying power to distinguish it from money and credit. That distinction is important because the value of money and credit changes. For example, when a lot of money and credit are created, they go down in value, so having more money won’t necessarily give one more wealth or buying power.

Real Wealth ≠ Financial Wealth. Real wealth is what people buy because they want to have and use it, such as a house, car, streaming video service, etc. Real wealth has intrinsic value. Financial wealth consists of financial assets that are held to a) receive an ongoing income in the future and/or b) be sold in the future to get money to buy the real assets people will want. Financial wealth has no intrinsic value. Right now there is far more financial wealth than can ever be converted into real wealth so it has to be devalued. When you are seeing your financial wealth go up as is happening now don’t think you are gaining real wealth when your buying power is going down.

Making Wealth = Being Productive. Over the long run the wealth and buying power you have will be a function of how much you produce. That is because real wealth doesn’t last long and neither do inheritances. That is why being continuously productive is so important. If you look at societies that expropriated the wealth of the rich and tried to live off it and weren’t productive (e.g., Russia after the revolutions of 1917), you will see that it didn’t take them long to become poor. The less productive a society, the less wealthy and hence the less powerful. By the way, spending money on investment and infrastructure rather than on consumption tends to lead to greater productivity, so investment is a good leading indicator of prosperity. On the other hand printing money and distributing it without being productive won’t raise wealth. Keep this in mind when thinking about the implications of policy developments. Printing money and giving it away won’t make us wealthier if the money isn’t directed to raise productivity.

Wealth = Power. That is because if one has enough wealth one can buy most anything—physical property, the work and loyalty of others, education, healthcare, influential powers of all sorts (political, military, etc.), and so on. Through time and across countries, history has shown that there is a symbiotic relationship between those who have wealth and those who have political power, and that the type of deal they have between them determines the ruling order. That ruling order continues until the rulers are overthrown by others who grab wealth and power for themselves. Wealth and power are mutually supportive. For example, in 1717 the British East India Company effectively brought together financial capital, people with commercial capabilities, and people with military capabilities to force India’s Mughal emperor to trade with them, which was the first step toward the British colonization of India, the fall of the Mughal Empire in the 18th century, and then its complete failure in the 19th century, when the British exiled the emperor and executed his children after the 1857 Indian Rebellion. The British did these things because they had the wealth and power to do them in pursuit of more wealth and power. Power changes come from wealth changes so watch who is doing what to create wealth changes.

Wealth Decline = Power Decline. There isn’t an individual, organization, country, or empire that hasn’t failed when it lost its buying power. To be successful one must earn an amount that is at least equal to the amount one spends. Those who spend modestly and have a surplus are more sustainably successful than those who earn a lot more and have deficits. History shows that when an individual, organization, country, or empire spends more than what they earn, misery and turbulence are ahead. History also shows that countries that have higher percentages of people who are self-sufficient tend to be more socially, politically, and economically stable. The United States now is spending a lot more money than it’s earning and paying for it by printing money that is being devalued. To improve we have to raise productivity and cooperation. Right now we are on the wrong path.

SB here again: My hope is that we get back on the right path. I could be wrong, but I just don’t know how we get there without a hard knock on the head. Inflation is the number one issue today; it’s likely to be that hard knock. We sit at the end of a long-term debt supercycle. If inflation sticks, think about the political implications we’ll see, particularly as we enter next year’s mid-term elections. What policy we get remains to be seen. “To improve we have to raise productivity and cooperation.” Will we?

Grab that coffee and find your favorite chair. I share a chart I meant to present last week. It does a great job showing where the S&P 500 Index sits in terms of risk/reward and coming returns. Think of it as a roadmap you can use to recognize when the opportunities for returns are least, average, and best. You’ll also find the latest Trade Signals post and some excitement about soccer in the personal section.

The Stock Market Will Mean Revert

I forgot to include this next chart in last week’s On My Radar: Valuations and Coming Returns post.

While no guarantees can be made and timing things right is a difficult task, a market decline that gets us back to the long-term trend is probable. I’ll explain what I mean by this in the next chart. Here’s how to read it:

- Think of the light blue upward sloping dotted line in the center section as the long-term average of the market, dating back to 1928. Over that long period of time, the S&P 500 has moved above and below the line.

- The bottom section of the chart is important. It shows us just how far above or below the long-term trend line the market was at any given point in time dating back to 1928. That gives us a quantitative way to look at when may be the best time to invest in stocks, when might be an okay time to invest, and when we might want to get defensive (hedge).

- Note the data box in the upper left-hand corner of the chart. A good time to buy is when the orange line corrects back to the blue dotted average long-term trend line. The best time to buy is when it dips well below the line.

- Notice where the blue line in the lower section is relative to 2000, 1966, and 1929 (I’ve inserted an arrow). We sit at the second highest deviation from long-term trend since 1929. It’s why I keep shouting, “hedge!” Admittedly, if the market rockets higher like it did in 1929, I may be shouting awhile longer.

Lastly, Ned Davis Research sorts the data into quintiles. The top quintile comprises the 20% of deviations above the long-term trend, and the bottom quintile comprises the 20% of deviations below long-term trend. The “average % change in S&P 500” is the total return gained five years and 10 years later. In the top quintile, every $100,000 turned into $140,650 10 years later. In the bottom quintile, every $100,000 turned into $459,140 10 years later.

Kind of cool to have this type of data, right? Bottom line: Play more defense than offense.

Trade Signals – Inflation at 6.2%, Highest Since 1990, Keep a Close Eye on Bond Yields

November 11, 2021

Posted each Wednesday, Trade Signals looks at several of my favorite equity market, investor sentiment, fixed income, economic, recession, and gold market indicators.

For new readers – Trade Signals is organized into three sections:

- Market Commentary

- Trade Signals — Dashboard of Indicators

- Charts with Explanations

Market Commentary

Notable this week:

“The best way to destroy the capitalist system is to debauch the currency.

By a continuing process of inflation, governments can confiscate, secretly and unobserved,

an important part of the wealth of their citizens.” – John Maynard Keynes

Inflation climbed 6.2% in October. While Treasury Secretary Janet Yellen and others continue to play down the risk of inflation, Wednesday’s inflation report is the largest year-over-year increase in 30 years. Stocks closed lower, the dollar rallied and gold closed higher. Bond yields rose 15 bps. The 10-year Treasury is at 1.56%. The Zweig Bond Model remains bullish on bonds.

I remain in the global slowdown camp and see a rising risk of recession by mid-2022. That means over the short-term rates may move higher. That’s my fundamental view and I could be wrong. If I’m right, the 10-year to move towards 1% by next summer. The 10-year is too large of a market to be controlled by the Fed. It will be one of our best signals to understand the direction of the economy. Keep a close eye on the bond market.

The Ned Davis Research (NDR) CMG U.S. Large Cap signal remains bullish on U.S. equities.

- It is a market breadth-based indicator that analyzes the overall technical strength of the market across 24 Industry Groups (GICS), as measured by three types of priced-based, industry-level indicators: trend-following, volatility, and mean-reversion.

- Trend-following primary indicators include momentum and moving average measures that evaluate the rate of change in price in each of the 24 Industry Groups (GICS) over short-term, intermediate, and long-term time frames to assess the current direction of the markets.

Click HERE to read to the balance of Wednesday’s Trade Signals post.

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – PKs

If you read last week’s post about my Susan’s high school soccer team, I owe you an update. They won last week’s game to advance to the quarterfinals of the PA Independent School State Championship. This past Tuesday, I left the office early and raced to the next game. Son Matt arrived before me. By the time I got there, the game was about fifteen minutes in.

Matt was faced with a conundrum: Root for his alma mater and former coach, or for his stepmom coaching the visiting team?

“How are the boys doing?” I asked. “Shipley is dominating,” he answered. Then he added, “Malvern Prep is getting good chances.” The score was 0-0 at halftime. Then the shift: MP came out strong and dominated the second half of the game, outplaying and outshooting their opponent. After an exciting 40 minutes, the game ended in a 1-1 tie. The teams and officials huddled, two 5-minute overtimes followed, and after overtime the game remained 1-1.

Do you remember when Brandy Chastain scored the winning penalty kick goal for the US women’s national soccer team in the 1999 World Cup final vs. China? To go back to that moment, click on the photo above. So much pressure on both teams. I remember watching the game with daughter Brianna then just six years old. We went crazy, as did most of America. Every kid wanted to wear the #6 jersey after that Chastain goal.

Back to Tuesday’s game. Five shooters from each team were selected. Malvern Prep shot first. After two rounds of penalty kicks, the teams were tied at 2-2. The 6’8” goalie for MP made a spectacular save in round three. The Shipley’s goalie saved the next two. Leading 3-2, the next Shipley player placed a strong shot past the MP goalie. Game over. A heartbreaker for Susan’s boys.

At 6:45am the next day, a young MP player was out on the soccer pitch alone with a bag of balls. He was practicing penalty kicks. The young man was one of the two players whose PK was blocked the day before. Often what we don’t want becomes our greatest teacher. A starter all season, and only in 10th grade. Come on… who needs a great summer intern? I just love it.

One more regular season game to go. At 10am tomorrow, Susan’s boys play a strong Springside Chestnut Hill team. Sitting with four wins, four losses, and one tie, MP can solidify third place with a win or a tie. Coach Sue wants that W.

Son Tyler is home for a visit, and he too is an MP grad. I, Matt, Tyler and his friend Taylor will be cheering from the sidelines, and we’ll all head to lunch in beautiful downtown Chestnut Hill after the game.

The dinner meetings in NYC this past week were fun. The city is alive and the meetings productive. Dallas is up next where I head to learn more about innovative company that has built a platform to provide investors with access to liquidity from alternative assets. Former Dallas Fed President Richard Fisher is a senior director. I’m hoping he is attending. He’s the most sane (former) central banker in my view.

The trees have mostly turned here in the Philadelphia area, yet the colors remain and they are spectacular. I hope you are enjoying life and injecting some fun into your daily routine. Thanks for reading.

Wishing you a great week!

All the best,

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Consider buying my newly published Forbes Book, described as follows:

With On My Radar, Stephen Blumenthal gives investors a game plan and the advice they need to develop a risk-minded and opportunity-based investment approach. It is about how to grow and defend your wealth.

If you are interested in the book, you can learn more here.