Prescience Point is long shares of MiMedx Group (MDXG), a Georgia-based maker of amniotic tissue grafts that has been the subject of relentless scrutiny and negative headlines for over a year. As frequent publishers of short-biased research, we believe short-selling is vital to the markets and agree with critics that MiMedx has engaged in wrongdoing. But we disagree on the extent of that wrongdoing, and believe that the company will overcome its current challenges and eventually thrive again.

Q3 hedge fund letters, conference, scoops etc

For over five months, we have applied our forensic due diligence process to deepen our understanding of the extent of the company’s misbehavior, the consequences that might result and the future prospects for the business. We have spoken with former employees, large current MiMedx customers, industry and legal experts, competitors, physicians and others.

What we developed is a picture of the company that looks wholly different, and much more positive, than the prevailing public narrative. As such, we believe that MiMedx shares offer one of the most attractive investment opportunities we have ever identified. Based on conservative assumptions, we estimate that the company’s shares are worth ~4x the current share price.

Some highlights from our report:

- Our analysis indicates that the chances of MDXG filing for bankruptcy are remote. MDXG has zero debt, had $33m of cash as of 12/31/2017 and has a highly flexible cost structure which enables it to generate strong FCF at much lower revenue levels. Even in an unlikely scenario where revenue contracts by 50% to around $200m in FY 2019, we project that MDXG will still have >$20m of cash remaining when its restatement process ends.

- Our investigation indicates that the majority of MDXG’s product sales are legitimate and sustainable. While MDXG likely did engage in channel stuffing, it appears to have amounted to just a small portion of revenue carried out at quarter-end. While we acknowledge that certain rogue sales staff may have participated in physician inducements on a one-off basis, we found zero evidence of widespread bribes / kickbacks.

- Despite more than a year of investigation, critics have failed to produce any smoking guns to support their claims of massive fraud. No internal documents or emails, or other direct evidence proving the existence of 1) a widespread inducement scheme, or 2) multiple years-worth of product stuffed in the channel have been produced. Furthermore, no key whistleblowers have alleged that MDXG has committed massive fraud. Instead, their allegations are centered around end-of-quarter channel stuffing.

- According to numerous former employees and physicians with whom we spoke, MDXG’s allograft products are some of, if not the best, in the industry. Given this, along with the fact that competitors Osiris and Organogenesis generate hundreds of $millions of revenue with products of similar or lesser quality, the claim that the vast majority of MDXG’s sales are fraudulent appears quite far-fetched.

- Concerns over the potential loss of the VA as a customer are overblown, in our view. MDXG remains on the Federal Supply Schedule and, according to MDXG’s IR department, continues to sell to the VA. Even if the VA stops purchasing from MDXG, our research indicates that the VA only comprises around 10% of sales.

- The government is highly unlikely to levy a fine that will force MDXG into bankruptcy. According to an expert on government enforcement actions, DOJ and SEC fines have been considerably dialed back under the current, more corporate-friendly, administration. Furthermore, regardless of administration, the government almost never kills companies due to the resulting negative impact on shareholders.

Introduction

Since our founding in 2009, we’ve become known for our deep research into companies committing fraud, inflating financial performance, misleading investors and misappropriating shareholder capital.

Last year, we exposed financial improprieties at trucking company Celadon Group. In the wake of our report, Celadon fired its top executives, rescinded its previously issued financial statements and watched its stock drop over 90%. Celadon’s shares were eventually delisted and both the SEC and federal criminal authorities launched formal investigations.

Activist short-selling serves a vital role in our markets and we are proud to play our part in uncovering wrongdoing. But today we are releasing new research on a company that has been accused of significant wrongdoing, but that we believe has fallen too far. That company is MiMedx Group (“MDXG” or “the company”).

Over the last year, prominent short-sellers and whistleblowers have exposed improper behavior at MDXG, which resulted in an announcement that its previously issued financial statements need to be restated, the firing of executives including the CEO, investigations by the SEC and DOJ, an auditor resignation and a stock delisting.

For over five months, we have applied our forensic due diligence process to deepen our understanding of the extent of MDXG’s misbehavior, the consequences that might result and the future prospects for the business. We have spoken with former employees, large current MDXG customers, industry and legal experts, competitors, physicians and others. What we developed is a picture of the company that looks wholly different, and much more positive, than the prevailing public narrative.

We are confident in our research and can be bold in our predictions. Here is why we own the stock and believe it is worth multiples more than its current share price:

- Our analysis indicates that the chances of MDXG filing for bankruptcy are remote. MDXG has zero debt, had $33m of cash as of 12/31/2017 and has a highly flexible cost structure which enables it to generate strong FCF at much lower revenue levels. Even in a severe downside scenario where revenue contracts by 50% to around $200m in FY 2019, we project that MDXG will still have >$20m of cash remaining when its restatement process ends.

- Our investigation indicates that the majority of MDXG’s product sales are legitimate and sustainable. While MDXG likely did engage in channel stuffing, it appears to have amounted to just a small portion of revenue carried out at quarter-end. While we acknowledge that certain rogue sales staff may have participated in physician inducements on a one-off basis, we found zero evidence of widespread bribes / kickbacks.

- Despite more than a year of investigation, critics have failed to produce any smoking guns to support their claims of massive fraud. No internal documents or emails, or other direct evidence proving the existence of 1) a widespread inducement scheme, or 2) multiple years-worth of product stuffed in the channel have been produced. Furthermore, no key whistleblowers have alleged that MDXG has committed massive fraud. Instead, their allegations are centered around end-of-quarter channel stuffing.

- According to numerous former employees and physicians with whom we spoke, MDXG’s allograft products are some of, if not the best, in the industry. Given this, along with the fact that competitors Osiris and Organogenesis generate hundreds of $millions of revenue with products of similar or lesser quality, the claim that the vast majority of MDXG’s sales are fraudulent appears quite far-fetched.

- Concerns over the potential loss of the VA as a customer are overblown, in our view. MDXG remains on the Federal Supply Schedule and, according to MDXG’s IR department, continues to sell to the VA. Even if the VA stops purchasing from MDXG, our research indicates that the VA only comprises around 10% of sales.

- The government is highly unlikely to levy a fine that will force MDXG into bankruptcy. According to an expert on government enforcement actions, DOJ and SEC fines have been considerably dialed back under the current, more corporate-friendly, administration. Furthermore, regardless of administration, the government almost never kills companies due to the resulting negative impact on shareholders.

To be clear, we are not suggesting that MDXG is an innocent victim. In addition to potential end-of-quarter channel stuffing, we believe prior management was overly aggressive in growing non-core revenue sources, which either were not exempt under Section 361 (i.e. Amniofix Injectable) or were not backed by strong clinical data (i.e. allografts for non-DFUs/VLUs). It appears that MDXG is now paying the price for this aggressive behavior as recent reimbursement cuts have targeted those revenue sources, and resulted in a material contraction in the company’s sales.

That said, although its non-core revenue has recently declined, the company still remains the market leader in its core wound care business. Thus, when the current controversy eventually clears, we believe that the company will still have a sizable and viable business remaining.

In our view, MDXG is one of the largest mispricings we have ever identified. Those who invest now are getting ownership in a business with enough liquidity to survive, that has industry leading products in a sizable, fast growing market and a promising pipeline of late-stage clinical trials – at an extremely low valuation of <1x sales which is far below that of its competitors who are trading in excess of 3.6x sales.

Furthermore, following the latest wave of negative news, we believe the news cycle for MDXG (but not prior management) is about to turn, as there are a number of potentially positive catalysts on the horizon, including:

- The hiring of a new auditor

- The appointment of new Board members

- Completion of the Audit Committee’s investigation

- The release of preliminary audit results

- The hiring of a new CEO

Thus, with its shares seemingly at an inflection point, we believe now is the ideal time to initiate a LONG position in MDXG.

Why Does This Opportunity Exist?

MDXG’s swift rise as a healthcare darling has been followed by an even swifter fall from grace.

Using its proprietary Purion platform technology, MDXG converts donated placental tissue into amniotic membrane products. Over the past few years, the company has grown to become the leading global supplier of allografts (tissue grafts) to the wound care market. MDXG’s flagship allograft products – Amniofix and Epifix

- are used in a variety of applications including the treatment of chronic wounds (e.g. diabetic foot ulcers), burns and surgical wounds.

The company’s troubles began in late 2017 when it became the target of a group of prominent short-sellers. Their reports on the company can be found here, here and here.

Critics believe that MDXG is a massive fraud. Numerous allegations have been levied at MDXG, but central to the bear thesis is the contention that the majority of the company’s sales are fraudulent and have been largely generated via

- massive channel stuffing, and/or

- widespread inducement of doctors via bribery / kickbacks

Developments over the past few months show that the allegations have a degree of merit – In June, MDXG announced that its financial statements going back to 2012 would have to be restated. Former CEO Parker H. Petit, along with other MDXG executives, was subsequently fired for cause, and an interim CEO from the restructuring firm Alvarez & Marsal was hired to run the business. The company also revealed that it was under investigation by multiple regulatory bodies including the SEC and DOJ.

The past two months have proven to be especially painful for MDXG and its shareholders:

- On November 7thMDXG announced that the Nasdaq had decided to immediately delist MDXG shares, reversing its previous decision to grant the company a listing extension until February 25th. This triggered a wave of mandatory institutional selling and resulted in a more than 50% decline in the company’s share price.

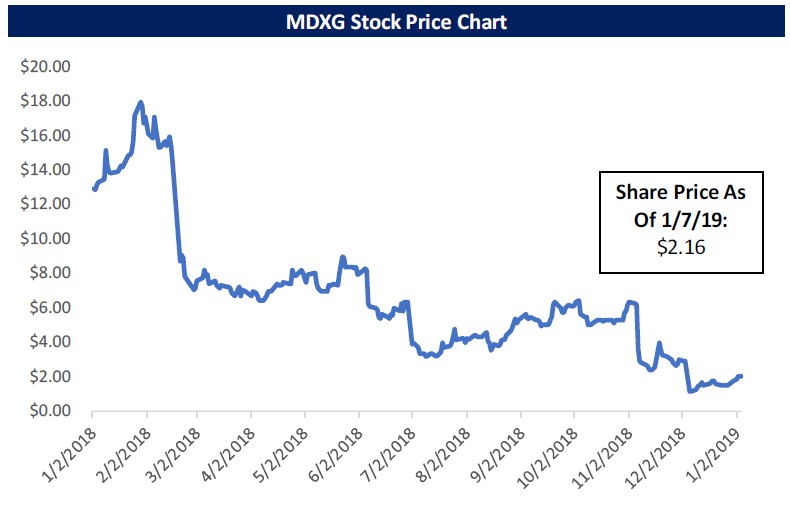

- Then, on December 5th, the company announced its plans to lay off 24% of its workforce in response to a recent, material softening in its revenue, and revealed that its auditor E&Y had abruptly resigned. Following these announcements, MDXG shares cratered to an all-time low of $0.95. As of 1/7/2019, MDXG shares still trade at just $2.16, 88.2% below its all-time high of $18.25.

Claims Of Imminent Bankruptcy Hold No Weight

At the moment, many market participants believe MDXG is simply uninvestable given recent turmoil and negative headlines surrounding its business. At higher valuation levels, we would agree with this sentiment. However, with MDXG shares trading near all-time lows, we believe its equity presents a highly attractive investment opportunity from a risk-reward perspective.

At this depressed valuation, the success of an investment in MDXG now comes down to one simple question: Will MDXG go bankrupt? If the company is able to remain solvent through its current crisis, then its shares should appreciate significantly.

Based on recent developments, critics claim that a bankruptcy filing by MDXG is imminent. They claim that the company will soon be insolvent because its declining sales are not sufficient to sustain its operations and fund its ongoing restatements and investigations.

We, on the other hand, believe that a bankruptcy filing by MDXG is highly unlikely primarily for two reasons:

- MDXG has a strong balance sheet: MDXG has zero debt and had $33m of cash on its balance sheet as of 12/31/2017. With a significant net cash position, the company does not have any other major obligations to fund besides its ongoing investigations and restatements.

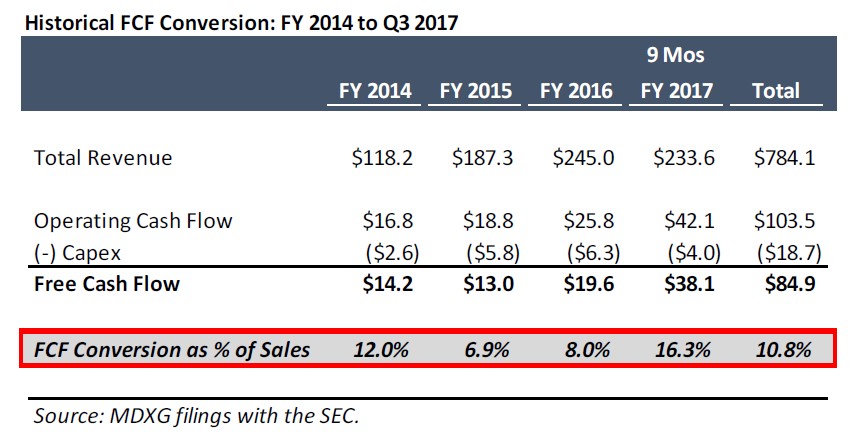

- MDXG has a highly flexible cost structure: With SG&A expenses accounting for around 80% of its total expenses, MDXG has a high proportion of variable costs and can easily scale its operating expenses to match its revenue. This gives the company the ability to generate strong FCF at significantly lower revenue levels, as illustrated by its historical FCF generation:

It is exceedingly rare for a business with such strong financial characteristics to become insolvent. Yet, critics believe that MDXG will somehow be an exception.

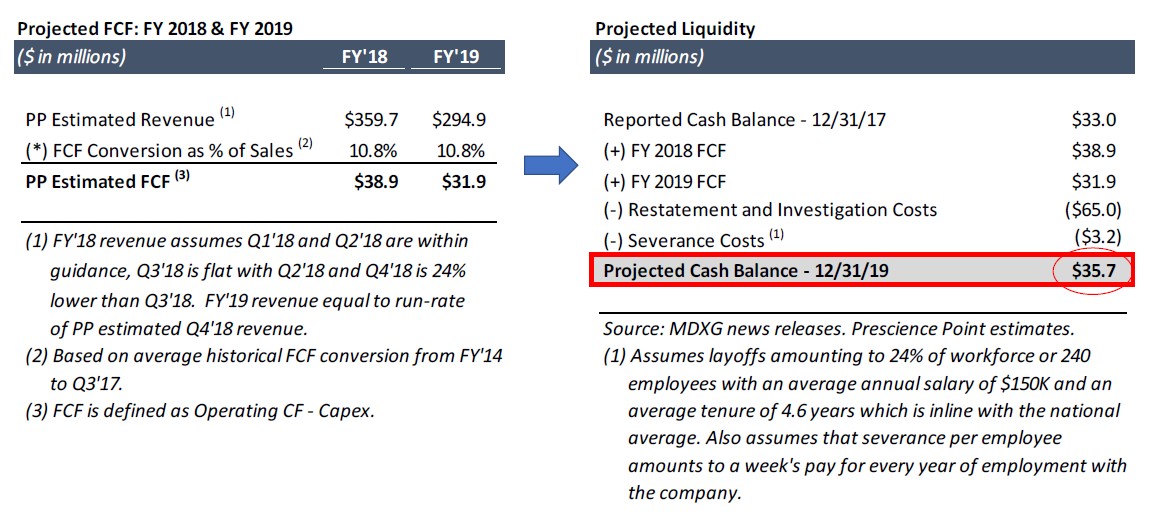

Despite the recent, material contraction in its revenue, the company’s debt-free balance sheet and flexible cost structure should enable it to easily generate enough liquidity to fund itself through its current crisis. To illustrate, we will construct a liquidity analysis with the following assumptions:

- Restatement period concludes at the end of FY 2019

- Restatement and investigation costs total $65m combined in FY 2018 and FY 2019. We believe this is a fair and likely overly conservative assumption given that Arthrocare spent ~$50m over approximately 1.5 years (late 2008 to early 2010) for a restatement process which was similar in scope

- Q1 2018 and Q2 2018 revenue are in-line with guidance at $92m and $97m, respectively, Q3 2018 is flat with Q2 2018, and Q4 2018 is 24% lower than Q3 2018 at $73.7m. Adding it all up, total FY 2018 revenue is an estimated $359.7m. The estimated decline of 24% from Q3 to Q4 is based on the recently announced 24% headcount reduction, which was in response to a recent softening in the company’s revenue

- FY 2019 revenue is equal to run-rate Q4 2018 revenue of $294.9m ($73.7m * 4)

- FCF conversion of 10.8% of sales, which is equal to MDXG’s average FCF conversion from FY 2014 through the first nine months of FY 2017

Using the above assumptions, we project that the company will have a considerable $35.7m of cash remaining on its balance sheet when its restatement process concludes:

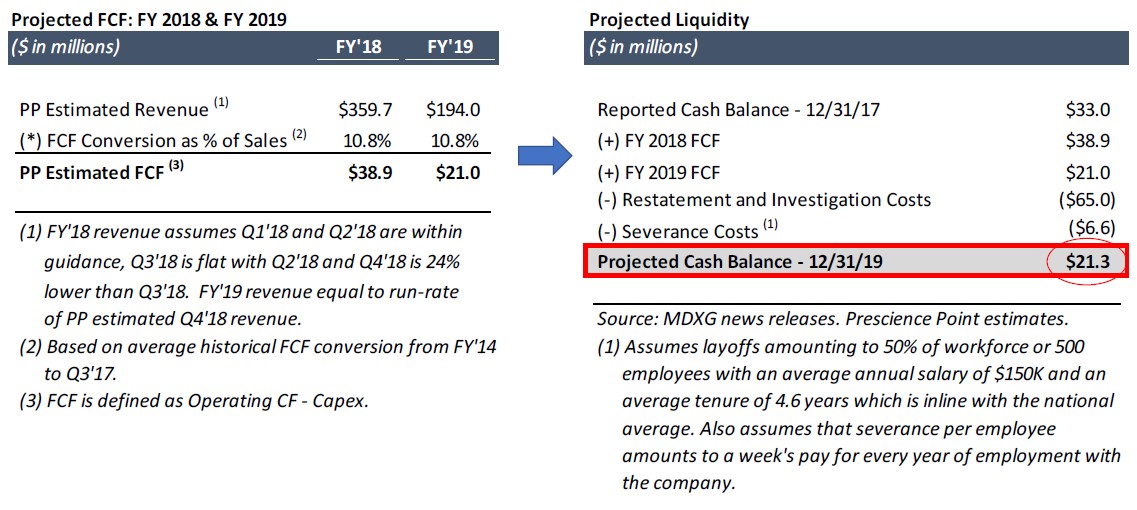

Even in a severe downside scenario where MDXG’s FY 2019 revenue declines to $194.0m, representing a 50% decline from its annualized Q2 2018 guidance, we project that the company will still have $21.3m of cash on its balance sheet when its restatement process concludes:

Read the full article here by Prescience Point