2018 SEI Preqin Survey of Private Debt Managers and Investors

Q4 hedge fund letters, conference, scoops etc

In collaboration with Preqin, SEI present Private Debt: Preparing for the Unknown, a paper which explores recent activity in the private debt market and the opportunities and challenges associated with its shift from periphery to prominence. Using interviews with more than 200 private debt managers and investors the resulting paper covers:

- Who is investing and why

- What are the drivers of change

- New niches and opportunities

- Preparing for the future

Exploring The Private Debt Frontier

The prodigious growth of private debt in recent years has been extensively documented. Growing competitive pressures and macroeconomic changes are starting to affect the private debt ecosystem, leading to increased discussions of the risks that may accompany this growth. As concerns mount, SEI collaborated with Preqin to survey and interview more than 200 private debt managers and investors in order to discern how GPs might best weather an impending slowdown.

Our research revealed myriad opportunities available to fund managers and investors alike. It also became abundantly clear that these opportunities are accompanied by risks, and the private debt market must be navigated with care. A variety of factors make the business more vulnerable than it was a few short years ago. The scale and competitiveness of the private debt business mean risk has largely been transferred away from banks, but the bountiful supply of credit means fund managers and their investors have been ceding power to borrowers. Covenant-lite loans account for a growing slice of the overall market. While it’s not obvious where the risks ultimately lay, it’s clear that investors and their fund managers may not be protected.

Governments assumed much of the risk in the depths of the last downturn after it proved to be too much for banks and their depositors. With market risk now theoretically borne by a much more global and diverse set of investors, including pension plans, insurance companies, wealth managers, and family offices, it’s difficult to say what will happen when the market is seriously tested again.

In a market full of promise yet fraught with risk, what is the best way forward? Our findings suggest a number of important considerations for managers wishing to take advantage of the opportunities in private debt. These range from niche lending strategies and customized portfolios to the use of advanced data analytics and a greater emphasis on operational efficiency and resilience.

In addition to illuminating some future opportunities, our survey revealed another familiar dynamic: fund managers are considerably more comfortable than investors with the current state of the market and their place in it. This is notable because we observed a similar disconnect between hedge fund managers and investors when we began surveying them a decade ago. Like private debt managers now, hedge fund managers then were largely unconcerned with growing competition, restive investors and looming regulation. That nonchalance gave way in the intervening years to grudging acceptance of the real costs involved. The hedge fund business subsequently evolved and participants became more sophisticated as a result.

Will the evolution of the private debt market mirror these developments? As astute as managers are, it seems fair to point out that it can be difficult to fully grasp the broader market from inside the silos in which many of them operate. This produces a more myopic perspective than the one enjoyed by investors whose exposure to multiple asset classes and strategies allows them to step back and take in the big picture.

Any ambivalence is understandable. Despite slowing growth, the private debt market continues to flourish and is expected to top $1.4 trillion within the next five years.1 Nobody knows when the next restructuring will happen, and we’re not trying to imply or answer the question of whether or not the boom in private debt may pose systemic risk. Individual managers, however, should be asking themselves what they can do—strategically, operationally or technologically—to hedge some of this risk, enhance their competitive positioning, and prepare for the inevitable slowdown or downturn.

Private Debt Goes From Periphery To Prominence

The phenomenal growth of private debt over the past decade can be traced back to the global financial crisis. Financial institutions needed to offload debt and the regulatory response included sharp increases to capital requirements. Both factors caused banks to curtail corporate lending and adopt a much more conservative approach to origination. Fund managers stepped into the breach, effectively replacing banks in the corporate lending landscape. Private equity sponsored deals have driven much of the growth, but nonsponsored loans are a growing part of the picture. In Europe, for example, nonsponsored loans accounted for over a third of overall loan volume in 2017, compared to less than 20% in 2007.2

Meanwhile, investors suffered in the prolonged yield drought driven by easy money policies enacted by central banks to stimulate economic activity. Unable to meet their cash flow requirements with investments in most traditional forms of fixed income, they were increasingly drawn to private credit. Increasingly viewed as a stand-alone asset class, private debt was seen as attractive in part because it was largely protected from interest rate hikes by the use of floating rates. Correlations with other assets were also thought to be relatively low, making private debt an excellent source of risk diversification. Furthermore, risk-reward characteristics looked attractive. Recent research has borne this out, showing that the pooled internal rate of return (IRR) for all vintages from 2004 to 2016 was 8.1%, despite including the negative effect of the financial crisis. Direct lending funds were particularly successful, with a pooled IRR of 11.8%.3 The same study reinforces the fact that “direct lending funds’ low correlation with all benchmark indices indicate they could provide diversification benefits for investor portfolios.” 4

A less-discussed factor is growing investor interest in private debt relative to other asset classes. Passive investments and private debt have been notable beneficiaries of growing discontent with actively managed long-only strategies using publicly traded securities. Private equity and its yield-producing cousin—private infrastructure funds—have also benefited.

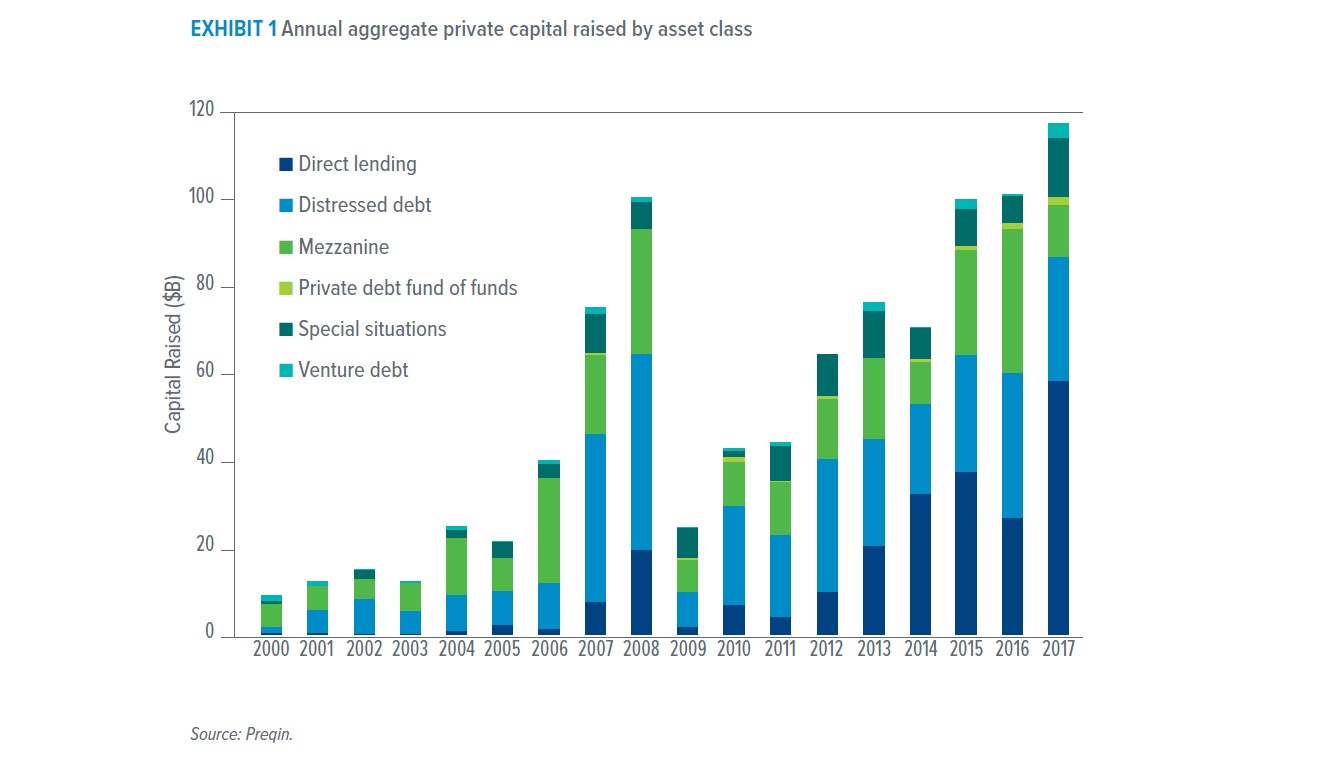

The net result has been a series of banner years for private debt funds. Approximately $100 billion was raised by private debt funds in 2015 and again in 2016, matching the high watermark previously seen in 2008 (Exhibit 1). Interest continued apace in 2017, as investors put almost $120 billion into private debt funds. Assets under management skyrocketed from $245 billion in 2008 to almost $667 billion a decade later. They are projected to double again by 2023.5

How long will this continue? Fundraising has slowed down through the first three quarters of 2018, but has not dropped precipitously. More interesting than the magnitude of current growth, however, is its composition. Investors are seeking the safety of established managers with demonstrable track records with whom they may already have relationships and in some cases seeking to amplify these relationships by establishing “strategic relationships” or SMAs. This trend means assets are increasingly concentrated in fewer hands. In Q2 2018, the five largest private debt funds raised $28 billion—or 66% of total assets raised.6 Investor attention is also being redirected among subcategories. Interest in direct lending and mezzanine credit all but evaporated in Q2 2018 as investors turned instead to special situations.7 These developments suggest that we may not necessarily see more deal volume, but bigger transactions are almost guaranteed.

Read the full article here by Preqin