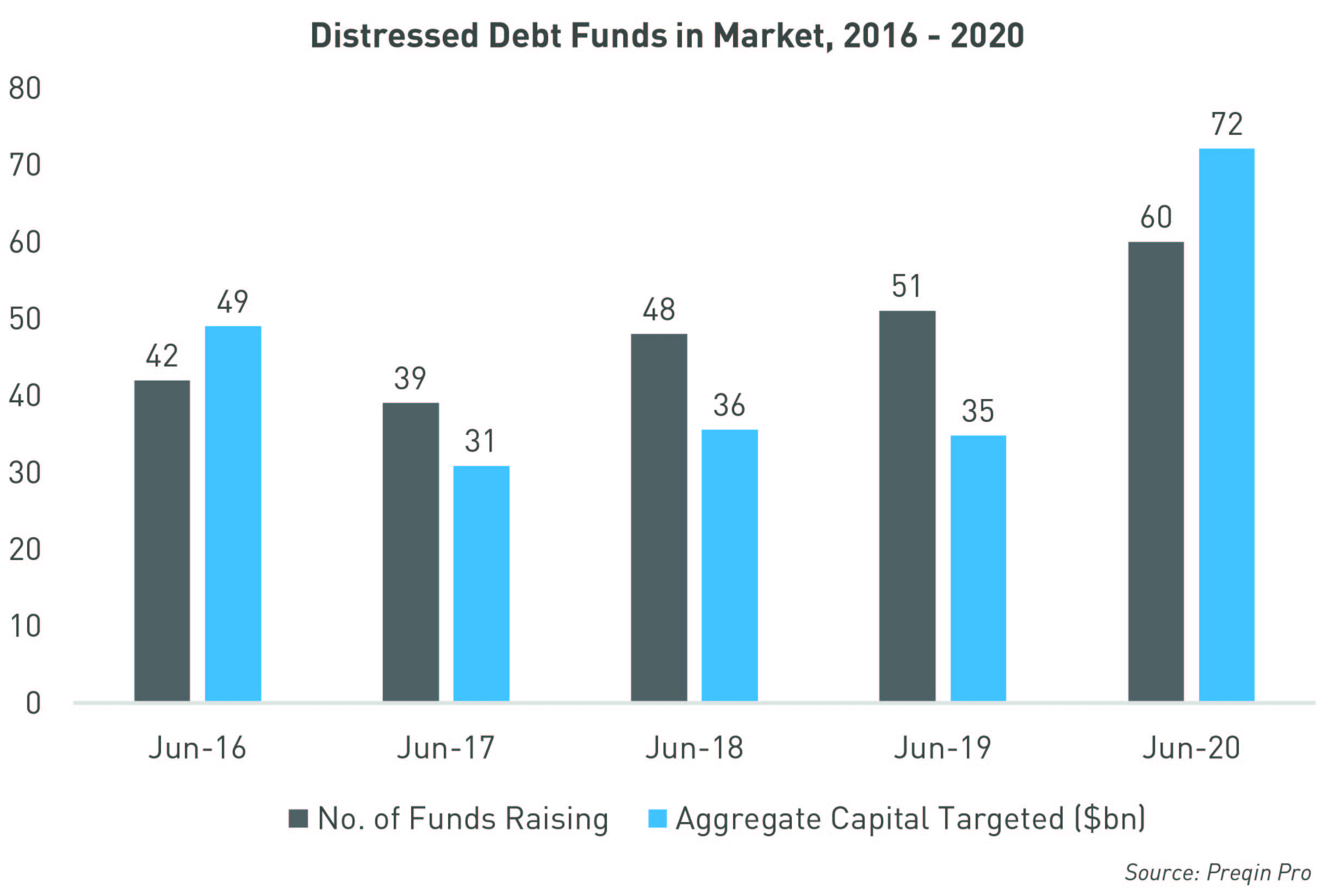

Distressed debt funds on the road number an all-time high of 60 as managers prepare to deploy significant capital in the aftermath of COVID-19

Q1 2020 hedge fund letters, conferences and more

Amid the continued market disruption caused by the COVID-19 pandemic, the number of distressed debt funds looking to raise capital has reached a new record. As the chart shows, these 60 funds in market represent a combined $72bn in capital targeted – this is more than double the amount of capital targeted by distressed debt funds at any point during 2019, and the highest total in the past five years. In anticipation of potential defaults amid the worst downturn since the end of World War II, many large and established private debt managers are seeking significant capital in search of new opportunities.

Preqin data shows that private debt firms have been building up distressed debt funds over several years. There is currently $68bn in dry powder (as of June 2020); this compares with $41bn as of December 2014. These capital reserves are due to be deployed in the coming months given the significant defaulting likely in the aftermath of the COVID-19 crisis. The industries most affected by the economic impact of lockdowns imposed across the globe – such as hospitality, sports, and entertainment – are expected to receive the bulk of this new investment.

Large Firms Are Raising Record Funds

Several established firms have announced new funds in the midst of the pandemic, driving the surge in distressed debt capital targeted. In April, Los Angeles-based distressed asset manager Oaktree Capital Management announced its intention to raise the largest distressed debt fund in history, at a target size of $15bn. Oaktree Opportunities Fund XI will buy up debt in struggling companies, predominantly across North America and Europe, that have been hit the hardest by COVID-19 and will opportunistically seek control of businesses during restructurings.

Other big names in the private debt space have also announced new distressed debt offerings so far this year. These include Apollo Global Management, Carlyle Group, and Goldman Sachs. Meanwhile, major allocators such as Washington State Investment Board have said that they are considering distressed debt investments.

While funds targeting distressed North American companies constitute 74% of capital targeted by distressed debt funds on the road, 20% is aimed at struggling European firms. London-based LCM Partners, for example, is currently targeting $4.4bn for LCM Credit Opportunities Strategy 4, which invests in European performing and non-performing loans. The fund will acquire portfolios spanning secured and unsecured credit portfolios such as credit cards, mortgages, and leasing, with an emphasis on generating investor returns through fair, ethical, and compliant treatment of the underlying borrowers.

But Timing Is Key

Most distressed debt managers are seeking out low-rated bonds, such as triple-B bonds, in anticipation of them being downgraded to junk bonds. While there is opportunity here to take advantage of ‘fallen angels,’ market saturation is a concern. The more crowded the market, the lower the potential for yield.

Ultimately, timing capital deployment is crucial to distressed opportunities: if the investment is made too early, valuations may not be as low as they can be, and if the investment is made too late, the opportunity may disappear altogether.

For more insights and analysis on the impact of the pandemic on alternative assets, take a look at our COVID-19 Knowledge Hub.

Article By Ashish Chauhan, Preqin