In working with clients to develop retirement spending strategies, advisors need to consider worst-case potential outcomes due to poor investment performance. One way involves using historical returns for bonds and stocks and focusing on the particular periods that would have produced the worst outcomes. Another way uses forward-looking estimates of average future returns and Monte Carlo simulations to generate a range of potential outcomes. I’ll develop new measures to compare those two approaches and demonstrate why I strongly favor the forward-looking approach.

[REITs]

Q2 hedge fund letters, conference, scoops etc

Historical returns

The most noteworthy financial planning research study of all time is Bill Bengen’s classic “Determining Withdrawal Rates Using Historical Data,” published in the Journal of Financial Planning in 1994. Bengen demonstrated that, for all historical 30-year periods going back to 1926, a portfolio of at least 50% stocks would have supported withdrawals of 4% of the initial portfolio, increasing with inflation each year – hence the “4% rule.” For the analysis that follows I’ll be assuming withdrawals based on the 4% rule in order to compare downside risk based on historical returns versus forward-looking return estimates. I won’t evaluate the viability of the 4% rule as such, but instead use it as a basis to compare retirement outcomes.

When Bengen published his study 25 years ago, 30 years was a conservative estimate of the potential length of retirement. But longevity has improved, particularly for the upscale individuals typical of advisory clients. I developed an estimate for a 65-year old couple where the life expectancies are 88 for the husband and 90 for the wife. The expected age at death for the last member of the couple is very close to 95. So a 30-year retirement has evolved into more of an average estimate rather than a conservative one, particularly for client couples.

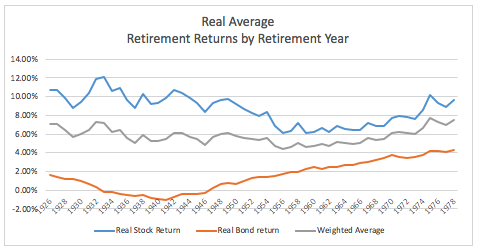

Using these updated longevity estimates, I did a new version of the Bengen analysis based on the Ibbotson data for stock and bond returns (large company stocks and intermediate-term government bonds) and a 60/40 stock/bond portfolio. I did this for cohorts of retiring 65-year-old couples, with each cohort associated with a retirement start year 1926-1978. I stopped at 1978 so that I would have at least 40 years of actual data for all of the cohorts. Instead of using a 30-year retirement duration, I made the longevity variable to reflect what a population of couples might actually experience – some with short lives, others with longer lives – and measured retirement duration based on the last to die for each such couple. A given couple in a particular retirement-year cohort would experience the same year-by-year investment returns as other members of that cohort, but longevity would be variable for the couples in a cohort.

I came up with a new measure for average stock and bond returns – for a given retirement start year, the average returns reflect the forward-looking average arithmetic real returns over retirement for that particular cohort. Because members of the cohort are assumed to die off over time, these returns are effectively survival-weighted – the early retirement years get more weight. The chart below shows the average returns by retirement start year.

Read the full article here by Joe Tomlinson, Advisor Perspectives