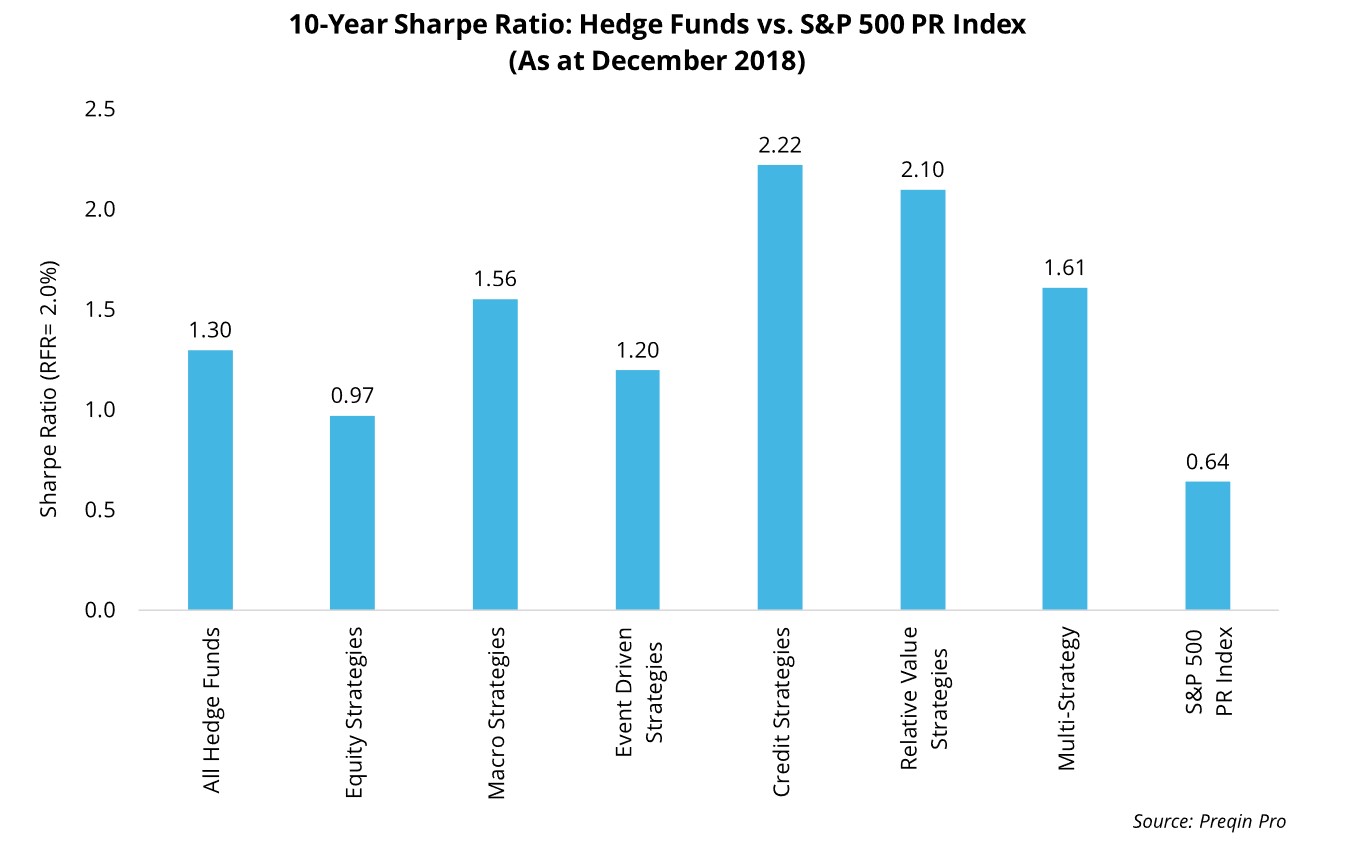

Historically, hedge funds have provided investors with risk-adjusted returns regardless of market conditions. As we approach the 10-year anniversary of the lowest return (676.5) recorded by the S&P 500 PR Index on March 2009, Preqin data captures how various hedge fund strategies have survived the tests of time relative to systematic risk factors. Hedge fund managers that have endured the crisis have produced a 10-year Sharpe ratio of 1.30, more than twice that of the S&P 500 (0.64).

Q4 hedge fund letters, conference, scoops etc

Risk-averse credit and relative value strategies have been consistent, generating the highest Sharpe ratios due to their low and steady positive returns with shallow, dispersed negative months. Over the past decade, credit strategies’ largest drawdown was a mere -3.56%, and relative values strategies’ largest recorded drawdown was -3.00% (as at December 2018).

Macro and multi-strategy hedge funds exhibit slightly higher Sharpe ratios than all hedge funds at the end of the 10-year period to 2018. Due to their dynamic nature, multi-strategy funds can maintain risk and return levels by adapting to varying market conditions. As with multi-strategy funds, macro strategies experience higher Sharpe ratios through portfolios built around global projections of multi-asset, thematic events; although considered the least restrictive strategy due to its ability to trade using virtually any type of security, event risk likely impacted the strategy, leading it to fall short of multi-strategy funds. Event driven strategies, like macro strategies, are also negatively impacted by event risk, suffering large drawdowns when predictions fail to come to fruition; their largest drawdown (-10.49%) was in September 2011, and is the second largest across hedge fund strategies.

With 10-year annualized volatility of 9.55%, equity strategies have the highest risk of all hedge funds, perhaps explaining why equities maintained the lowest Sharpe ratio (0.97). When looking at drawdowns, equity strategies also recorded their lowest in 2011 at -12.28%; however, equity strategies have still displayed downside protection relative to traditional equity markets. Charles Lemonides, Portfolio Manager at ValueWorks, an equity long-biased fundamental value hedge fund manager with a 20-year track record, has observed:

“The key to our long-term returns has been to look past short-term market gyrations and be willing to put money to work when opportunities arise over different economic cycles. ValueWorks believes that we are in the latter stages of a market advance that could last another three to five years, and we could see a double from here. We are more long in the long book than we ever have been, and more short in the short book than we have ever been. We are seeing a lot of discrepancies in valuations.”

In response to a potential crisis, hedge funds and asset allocators have begun positioning themselves more defensively for 2019, with 29% of investors stating they intend to increase exposure to macro strategies, while 28% intend to do so for relative value strategies. Nonetheless, hedge funds have proven to serve their purpose to investors in periods of trial.

With similar market drawdown trends to those experienced a decade ago appearing in today’s markets, the 10-year Sharpe ratio is indicative of the hedge fund industry’s long-standing ability to endure economic distress.

Looking for more hedge fund data and analysis? Sign up to our newsletter to ensure you are notified as soon as the reports are released.

Article by Mark Langan, Preqin