Robo-advisors faced their first big challenge with the bear market in the first quarter of 2020. They lost, and that is an ominous sign for the future of automated advice.

Q1 2020 hedge fund letters, conferences and more

All robos employ a degree of active management. They deviate from the cap-weighted market portfolio through fund selection or sector allocation. As active managers, robo performance can be fairly viewed only through a full market cycle. Nobody needs an active manager in a bull market; index returns are adequate. Active management shows its value in its ability to protect against adverse market conditions. The market downturn in the first quarter gave us that opportunity.

Thanks to the excellent work by New Jersey-based Backend Benchmarking (BEB), the robo’s performance results are readily available. I wrote about BEB’s work last year and noted that the performance of the robos was alarmingly dismal even before they had faced a full market cycle.

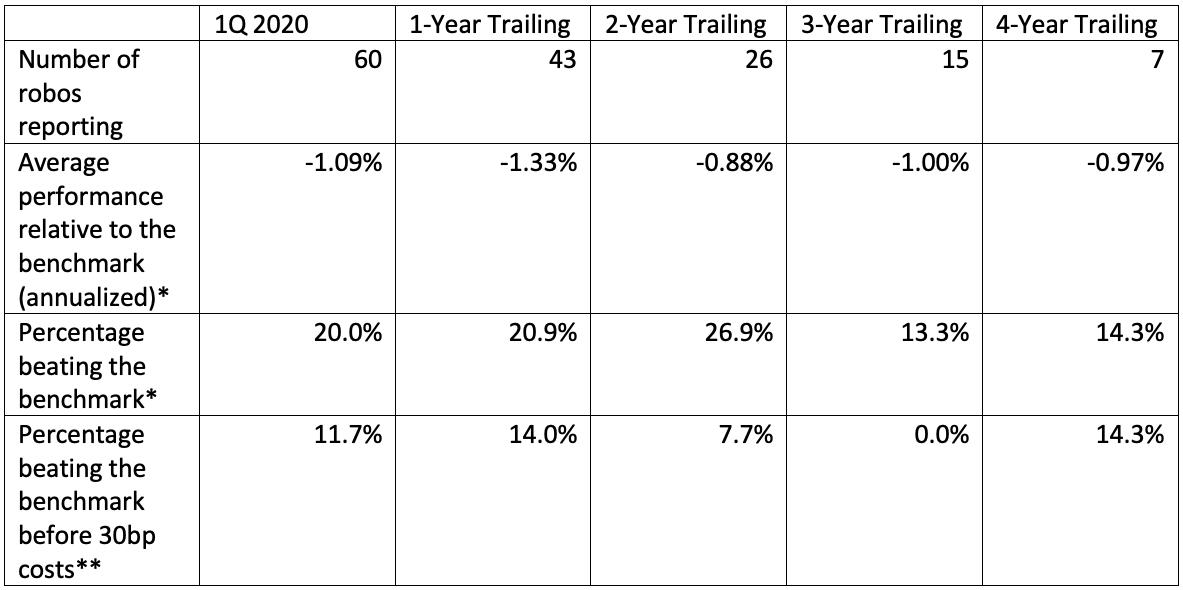

BEB tracks the performance of 60 robo portfolios, although it does not have full history for all of them. It compares each robo to a benchmark consisting of a 60/40 equity/fixed income ETF portfolio. It deducts 30 basis points annually from the benchmark to normalize for the expenses charged by the robo platforms.

Here is a summary robo performance relative to that benchmark:

* This shows performance after 30 basis points has been deducted from the benchmark’s returns.

** This shows performance without deducting 30 basis points from the benchmark’s returns.

A key takeaway from this table is that robos underperformed their benchmarks in every time period available, including Q1 of 2020. The average underperformance was approximately 1% for each of those time periods.

Given that four-year performance data is available for only seven robos, it is premature to write their obituary. But the fact that so few robos outperformed a passive benchmark over all the periods measured by BEB is a stern warning to investors. This data measures the aggregate performance across all robos. It is possible that, over time, a robo may emerge from the 60 studied by BEB that exhibits the skillfulness to outperform a passive benchmarks. But, given the large-scale failures documented in this table, that possibility is unlikely.

To put this in perspective, S&P measures the performance of actively managed mutual funds relative to passive benchmarks through its SPIVA scorecard. Since 2001, only twice (in 2011 and 2014) did actively managed mutual funds perform worse during a one-year period than the robos after costs did in the above table (20.9%). Investors would be better served in a randomly chosen active mutual fund than in a robo advisor.

Read the full article here by Robert Huebscher, Advisor Perspectives